AQST - Aquestive Therapeutics: Anaphylm's Top-Line Data Could Reveal A Game-Changer In Q1

2024-01-19 17:05:19 ET

Summary

- Aquestive Therapeutics is nearing a key topline readout for its Anaphylm sublingual film, a potential groundbreaking oral epinephrine treatment for severe allergic reactions.

- If the data is positive, Anaphylm could be heading for a possible New Drug Application (NDA) in 2024, with a potential commercial launch in 2025.

- Aquestive faces risks from regulatory hurdles, competition from other epinephrine treatments, and potential financial setbacks.

Aquestive Therapeutics ( AQST ) is quickly approaching a key topline data readout for the Anaphylm (epinephrine) sublingual film that is slated for Q1 of this year. The company announced in December that they have commenced the first patient dosing in its Phase III pivotal study evaluating Anaphylm’s pharmacokinetics “PK” and pharmacodynamics “PD”. If the data is positive, Anaphylm would be heading towards a possible NDA in 2024 as a groundbreaking oral epinephrine candidate in the multi-billion dollar severe life-threatening allergic reaction and anaphylaxis market. In my previous Aquestive Therapeutics article from November of 2022, I discussed how I was “all-in” on AQST-109 (Anaphylm) due to its immense commercial potential, and that outlook remains the same despite the share price rising ~167% since its publication. As a result, I believe investors need to be prepared for these slated catalysts and have a game plan for the AQST position for 2024.

I intend to provide a brief background on Aquestive Therapeutics and Anaphylm. Then, I will discuss the opportunity, as well as the risks for Aquestive. Finally, I reveal my plan for my AQST going into this critical data readout.

Background On Aquestive Therapeutics

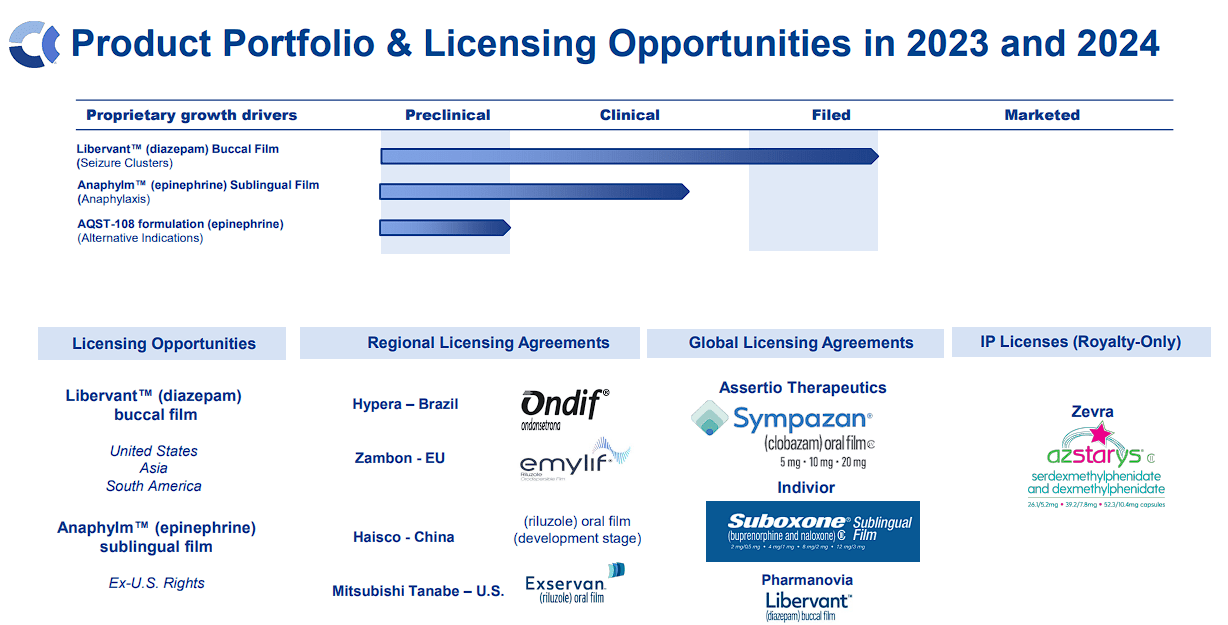

Aquestive Therapeutics is advancing medicines with their unique delivery technologies. Aquestive's core technology, PharmFilm , is integral to its product portfolio, with key formulations like AQST-108 (epinephrine) and Libervant (diazepam) targeting various indications globally through strategic licensing agreements. PharmFilm is a thin film that can absorbed in the patient's mouth and allows for the delivery of complex molecules in an orally administered format.

Aquestive Therapeutics PharmFilm Overview (Aquestive Therapeutics)

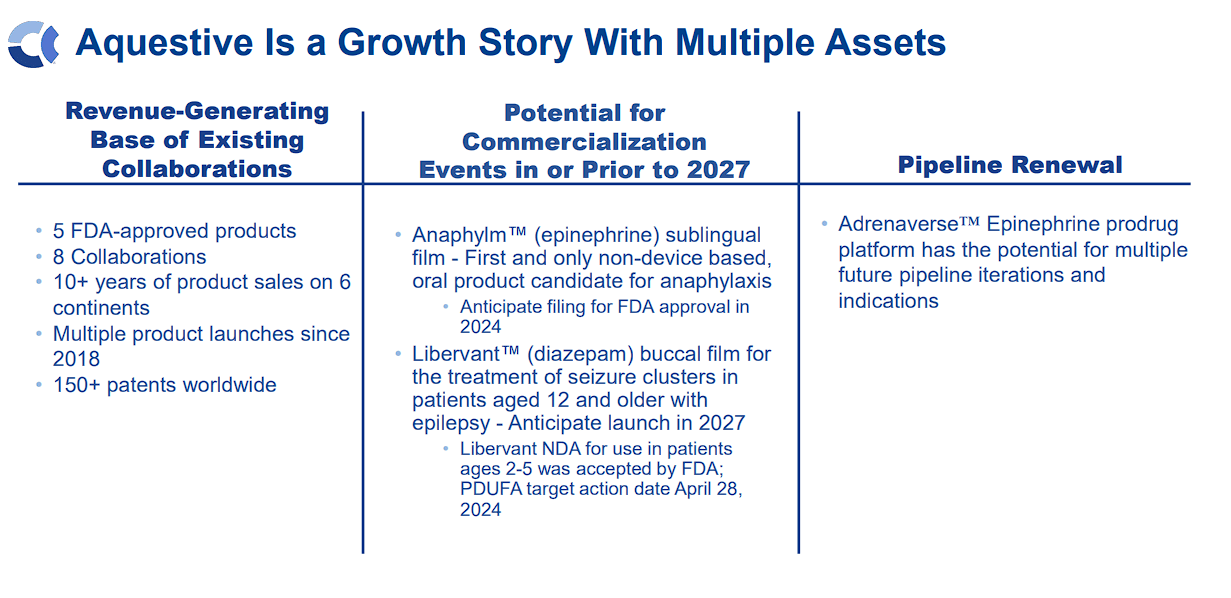

Aquestive's focus extends to treating diseases of the CNS, with both early and late-stage pipelines. With five commercialized products and several collaborations, Aquestive has proven its drug development and commercialization capabilities.

Aquestive Therapeutics Pipeline (Aquestive Therapeutics)

{kind=link}

The company's pipeline renewal includes the “Adrenaverse” prodrug platform, holding the potential for several future iterations and indications using epinephrine.

Aquestive Therapeutics Growth Prospects (Aquestive Therapeutics)

{kind=link}

In the coming years, Aquestive aims to grow collaboration revenue, obtain FDA approval for Anaphylm in the U.S., and launch Libervant in the U.S. by 2027.

Taking A Look At Anaphylm

Anaphylm (Formerly AQST-109), an epinephrine sublingual film, has the potential to be the first and only non-device-based, oral treatment for anaphylaxis. Anaphylm stands out as a polymer matrix-based epinephrine prodrug that is comparable in size to a postage stamp and weighs less than an ounce. Its distinctive feature is that it dissolves in contact with saliva, removing the need for water or swallowing during administration. The packaging is designed to be compact and easily portable, similar to the dimensions of a credit card. The company made Anaphylm's packaging robust enough to survive various weather conditions, such as exposure to rain and UV from sunlight.

Thus far, Anaphylm has demonstrated favorable PK and PD parameters, providing a rapid and clinically effective response. In clinical trials, Anaphylm has exhibited a favorable safety profile, with the majority of reported adverse events being mild or moderate in severity. The cardiovascular adverse event profile aligns with approved comparators, underlining Anaphylm’s safety and tolerability.

The current Phase III study includes two parts, intended to comprehensively gauge the performance and safety of Anaphylm versus approved epinephrine delivery products. Part A, a three-period study, will pit Anaphylm 12mg against an epinephrine autoinjector and epinephrine manual intramuscular injection. Part B will test a single dose of Anaphylm 12mg against EpiPen and Auvi-Q and the manual IM injection. The primary goal is to match the PK and PD following the single administration of Anaphylm to single administration of epinephrine IM injection in healthy adult subjects.

Anaphylm’s Implications

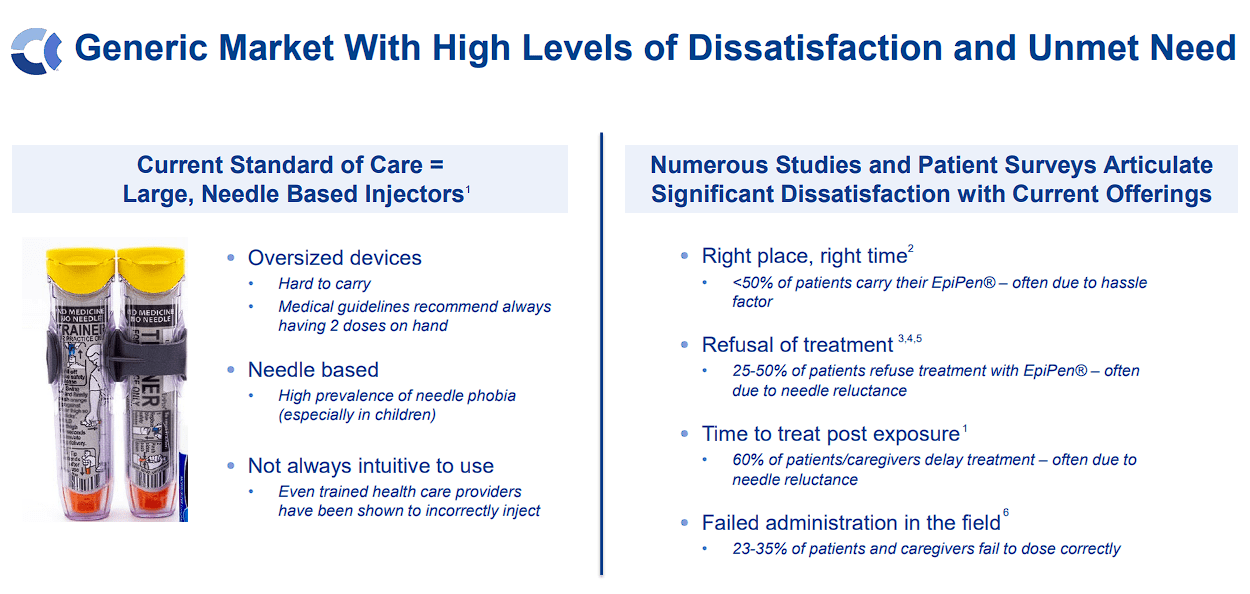

The big opportunity comes from Anaphylm’s potential to be the “first and only non-invasive”, oral epinephrine product that produces similar results comparable to auto-injectors for the emergency management of acute allergic reactions, including anaphylaxis. The epinephrine market is trending towards significant growth, with Anaphylm presenting a unique and patient-friendly alternative to current standards of care. So, Anaphylm addresses the frustration and limitations of contemporary injector products.

Aquestive Therapeutics Epinephrine Market Overview (Aquestive Therapeutics)

{kind=link}

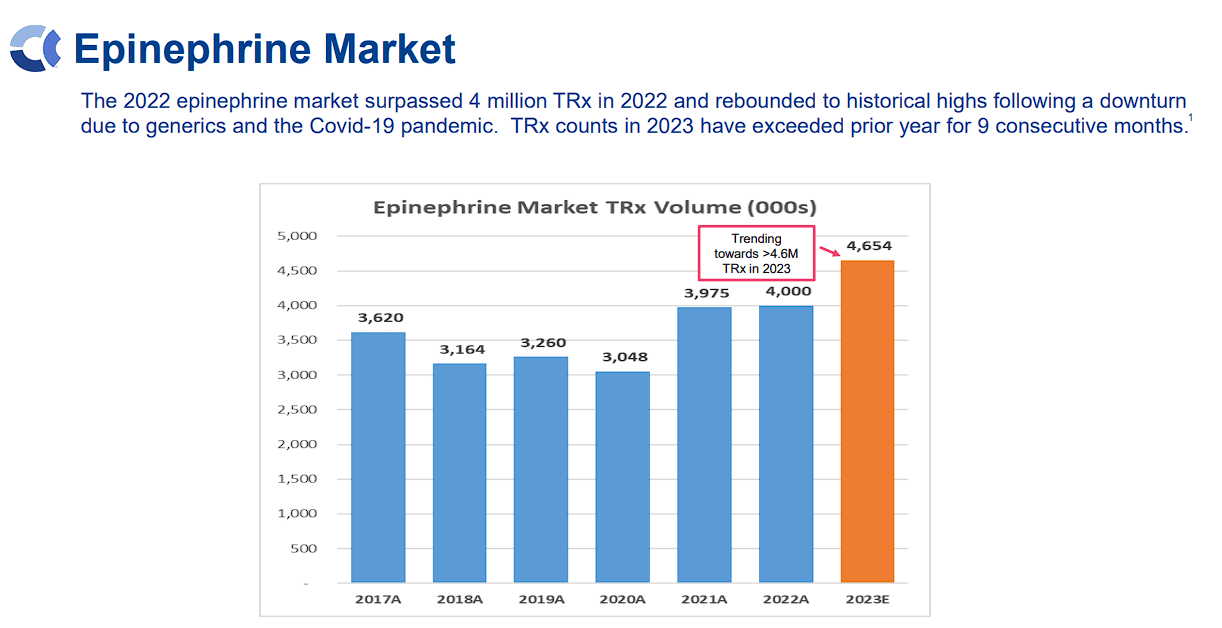

If approved Anaphylm could benefit from a large and growing epinephrine market, which surpassed 4M TRx in 2022, and was on pace for more than 4.6M in 2023, which is expected to produce a $2.83B global market.

Aquestive Therapeutics Epinephrine Market Overview (Aquestive Therapeutics)

{kind=link}

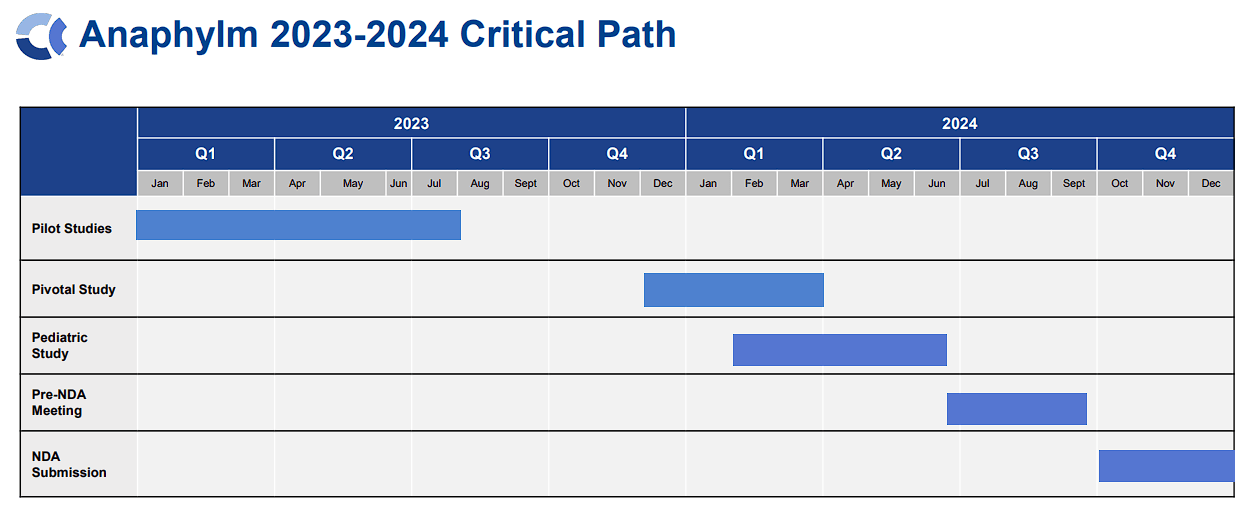

Therefore, the potential approval of Anaphylm would be a monumental event for Aquestive. The company anticipates filing Anaphylm’s New Drug Application (NDA) with the FDA in Q4 of this year, which should put a potential commercial launch in 2025.

Aquestive Therapeutics Anaphylm Critical Path (Aquestive Therapeutics)

{kind=link}

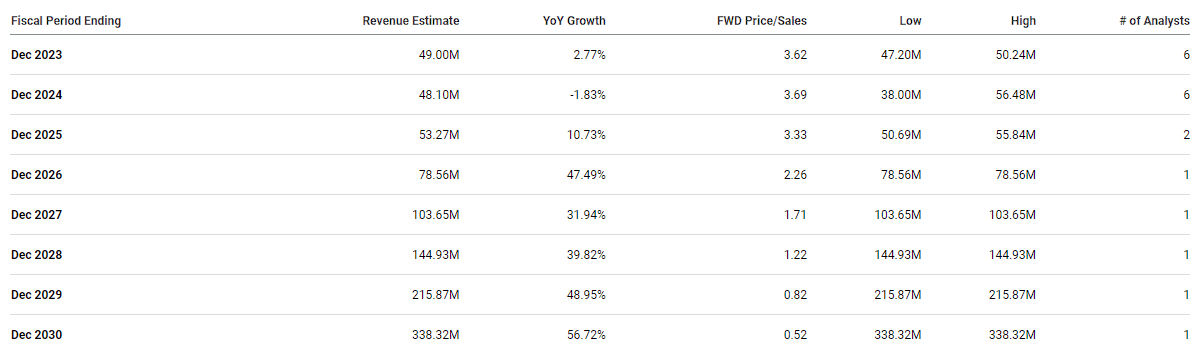

A potential commercial launch in 2025 ought to deliver significant revenue growth for Aquestive in the coming years. In fact, the Street expects Aquestive to report strong double-digit revenue growth for the remainder of the decade and break $300M at some point in 2030.

Aquestive Therapeutics Revenue Estimates (Seeking Alpha)

{kind=link}

Although the company has other sources of revenue and pipeline products, we have to expect that Anaphylm is the primary contributor in these models. So, I think safe to say that Anaphylm is critical to Aquestive’s success in both the near-term and long-term.

Anaphylm's Impact On Valuation

I have been covering AQST for some years now, and throughout that time, Aquestive's cheap valuation has been one of the primary attractions of the ticker. I have pointed to the company's projected revenue growth, which has consistently indicated that the ticker was trading well under the sector median forward price-to-sales of 4x. Currently, AQST has a ~$145M market cap, which would be around 3.6x price-to-sales for the 2023 revenue estimate, so it is already undervalued in one metric for its current commercial performance. That valuation is expected to improve in the coming years as Anaphylm taps into a global epinephrine market that is expected to hit nearly $5.8B in 2032 . Anaphylm would only need to claim roughly 5% of that market to hit the Street's forecasts for the end of the decade. Even if the company out-licenses the product, Anaphylm doesn't need to become the dominant epinephrine product on the market to meet the Street's numbers and dramatically change Aquestive's long-term outlook. Over the past twelve months, Aquestive has pulled in $48.1M in revenue with $26.6M in gross profit with $48.5 in total OpEx, leading to roughly -$22M in net income. That loss could easily be eradicated in a few years of revenue growth, or an upfront payment from out-licensing.

Admittedly, we don't know if Aquestive will hit the Street's estimates, however, they do illustrate how Aquestive can go from being slightly undervalued, to absurdly undervalued by the end of the decade thanks to Anaphylm upside potential.

Keep in mind, that this analysis is removing all other sources of revenue that Aquestive has now, and any other potential revenue streams, including Libervant, that may contribute in the future.

Risks To Consider

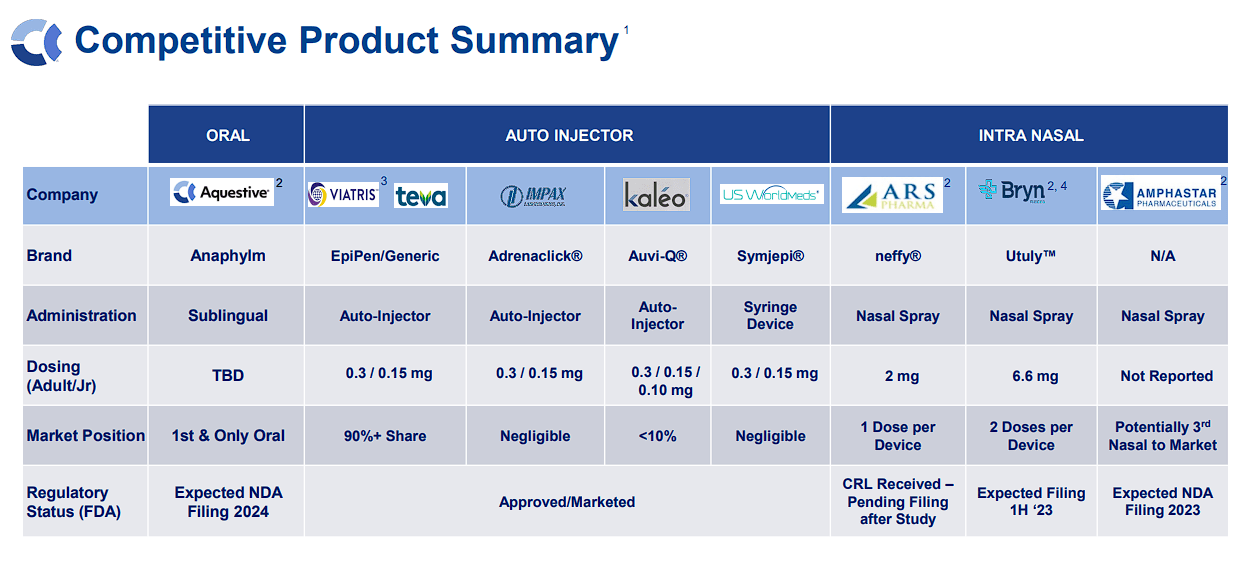

Like any pharmaceutical company, Aquestive faces risks such as regulatory hurdles, clinical trial setbacks, and market competition. Aquestive operates in a competitive arena, contending with other companies developing epinephrine treatments for similar indications.

Aquestive Therapeutics Epinephrine Competition (Aquestive Therapeutics)

{kind=link}

In addition to auto-injectors, Aquestive will most likely have competition from intra-nasal epinephrine devices. Indeed, Anaphylm has some competitive advantages over the current competition, including being a non-invasive sublingual film. However, I believe we have to expect some patients would consider an intra-nasal option, which is a more common route of administration.

In addition, the company still has to face risks from external factors, economic conditions, and unexpected challenges that may impact Aquestive's performance. Moreover, the company only had $24.92M in cash at the end of Q3, which will most likely not be sufficient to fund a commercial launch. Admittedly, we don't have a clear idea of what the expenses would be for a commercial ramp-up for Anaphylm because we don't have their game plan to reference. It appears as if the company is going to continue with out-licensing, which would limit any additional expenses. However, if the company decides to "go-it-alone" in commercialization, they would have to hire an army of reps to hit the highest prescribing allergists, and possibly scale up from there. Of course, the company could also decide to find a commercial partner for Analphylm, which would probably involve an upfront payment, milestones, and royalties. As a result, we cannot forecast the company's cash burn going forward at this time, but investors should note that Aquestive has a track record for dilution, and accept there is a strong likelihood of a fundraising event at some point this year. Although I wouldn't expect a devastating level of dilution to fund a company that has reduced their expenses over the past couple of years, any possibility of an offering tends to put a dark cloud over the ticker until the threat has been resolved.

Considering these risks, I am sticking with a conviction rating of 3 out of 5 and will remain in the “Bio Boom” speculative portfolio.

My Plan

Aquestive Therapeutics' Phase III clinical study for Anaphylm marks a significant step forward for the company and positions them as a potential game-changer in the field. As the study progresses and topline data is anticipated in the first quarter of 2024, the investment community eagerly awaits the data, which could indicate a potential approval and commercialization of this groundbreaking orally delivered epinephrine product.

I do expect the data to be positive and should point to a potential approval in 2024. However, I think most of the market is expecting the same results, so a potential "sell the news" event might be on the table following the data release... especially if the buying volume is low and bulls have been showing weakness throughout the quarter.

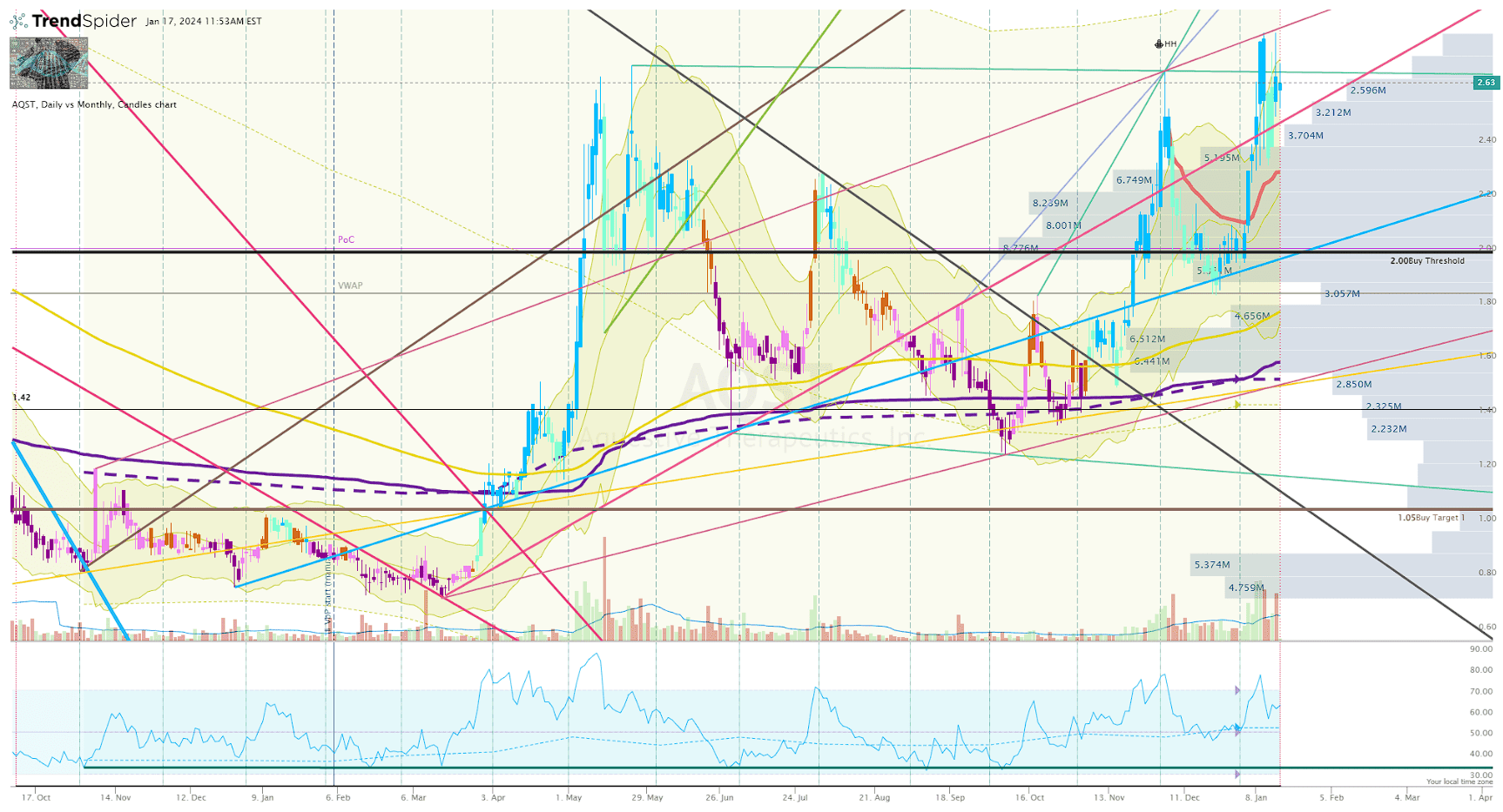

Looking at the Daily Chart, we can see AQST trading above my Buy Threshold with a potential double-top setup at $2.75 per share. If the ticker fails to break above this level over the course of Q1, I suspect we will see a potential sell the news as investors look to book profits on a spike, and short sellers anticipate weakness and a void below.

AQST Daily Chart (Trendspider)

{kind=link}

If this occurs, I will consider booking profits on the spike and will look to reload if the share price drops below my Buy Threshold, which is the maximum I am willing to pay for AQST considering its current technical rating.

If the share price rises above $3 per share before the data readout, I will look to book profits ahead of the data release and will set a large buy order below my Buy Threshold. If the share price sells off ahead of the data release, I will wait for the data release and will add to my position once I identify and strong reversal setup.

Long term, if the data is positive, I expect to maintain my AQST position for at least five more years and the ticker will remain a “Top Idea” in the Compounding Healthcare investing group. However, if the data does not support approval or is inferior to contemporary products, I will sell the majority of the position and will consider revisiting the ticker towards the end of the year.

For further details see:

Aquestive Therapeutics: Anaphylm's Top-Line Data Could Reveal A Game-Changer In Q1