AQST - Aquestive Therapeutics: Waiting To Buy After FDA Goes Halfway With Libervant

Summary

- After 8 months of waiting for an update from the FDA, the agency finally announced a tentative approval for Aquestive's Libervant. Unfortunately, the company cannot market the product.

- Aquestive Therapeutics recently reported their Q2 earnings, which revealed a beat on revenue with the EPS in-line with expectations. Aquestive has upped their full-year guidance for both revenue and EPS.

- I review Libervant's approval and Aquestive’s Q2 earnings for investors.

- I discuss some downside risks and how I plan on managing my AQST position in the near term.

- AQST remains a “Top Idea” in the Compounding Healthcare Seeking Alpha Marketplace.

Being a longstanding Aquestive Therapeutics ( AQST ) shareholder is becoming a challenge. We waited roughly 8 months for an update from the FDA on Libervant's potential approval, only to be informed that the FDA believes the product is worthy of approval... but not allowed to be on the market. Consequently, the market punished the ticker as investors begin to doubt that Libervant will make it to the market in the near term. Despite the recent setbacks, AQST remains a "Top Idea" in the Compounding Healthcare Seeking Alpha Marketplace Service, thanks to the ticker's discount valuation and long-term upside potential. The company's Q2 earnings report revealed a beat on revenue with the EPS in-line with expectations. What is more, the company upped their full-year guidance for both revenue and EPS. As a result, I am willing to accumulate shares of AQST while we wait for the company to make their next move Libervant.

I intend to review the company's Q2 earnings and will point out a few bullish highlights for investors. Then, I will provide my views on the quarter. Furthermore, I take a look at the company's valuation and will defend my decision to accumulate shares of AQST. To conclude, I update my plans for my AQST position.

Semi-Approved

On August 31, 2022, Aquestive declared that the FDA " granted tentative approval for Libervant," the company's diazepam buccal film product for the "acute treatment of intermittent, stereotypic episodes of frequent seizure activity (i.e., seizure clusters, acute repetitive seizures) that are distinct from a patient's usual seizure pattern in patients with epilepsy 12 years of age and older."

The company explained

that a "Tentative approval" means the FDA has determined that Libervant " has met all required quality, safety, and efficacy standards for approval but, due to an existing FDA regulatory grant of orphan drug market exclusivity for Valtoco, a diazepam nasal spray product, Libervant is not yet eligible for marketing in the United States. As a result of the FDA determination, the Agency cannot give final approval for Libervant until the expiration or inapplicability of the orphan drug market exclusivity, including, for example, by court order, a selective waiver of the orphan drug exclusivity, or a reversal of the FDA's decision and determination that Libervant is "clinically superior" to Valtoco."

When reading the company's press release, it appears as if the FDA had some issues with Libervant and the effect of food on the absorption of diazepam. However, as stated in the August 31 update, the company believes that have the data that addresses that concern and that " Libervant has the distinct advantage of being able to be readily administered when needed without regard to food, providing an important benefit to patients ."

Aquestive did submit crossover study results to the FDA that showed " the effect of food on the pharmacokinetics of Valtoco in healthy adult subjects. " According to Aquestive, the data indicated that Valtoco's Cmax was reduced by 48% if it was administered after a high-fat meal compared to Valtoco administered in a fasted state. In addition, Valtoco's Tmax doubled from 2 hours to 4 hours when administered after a high-fat meal. Aquestive also submitted data from a comparative study with Libervant to the FDA, but the agency " concluded that the information Aquestive submitted was not sufficient to overturn the Agency's previous conclusion regarding the lack of food effect for Valtoco" due to " the lack of a common reference standard between the two studies. " (all support contained in August 31, 2022 update).

So, Libervant is safe and effective enough to be approved but doesn't have the green light to be on the market due to Valtoco's orphan drug exclusivity. It looks as if the company has to convince that Libervant is clinically superior to Valtoco if they want to get on the market in the near term… otherwise, they are waiting roughly five years for the orphan drug exclusivity to expire.

What is Next?

It appears as if the company is going to have to meet with FDA and discuss their options, but it looks as if they are going to have to run a comparative study with both Valtoco and Libervant. This comparative study will most likely have to show the impact of ingesting food on Cmax and Tmax. If Libervant outperforms Valtoco, Aquestive could have enough ammo to gain marketing approval.

Once the study is complete, the company should be able to submit the results and the FDA can make their decision. This submission should not require a review cycle like a regulatory submission. So, I do not anticipate the FDA taking a prolonged period of time to make a decision.

Now, it is just a wait-and-see what Aquestive and the FDA will agree on for the path going forward. In the meantime, investors should be on the lookout for a potential ex.-U.S. partnership for Libervant.

My Thoughts on The Plan To Get "Full Approval"

To be honest, I had a gut-wrenching feeling that the company was going to have to wait until Valtoco's orphan drug exclusivity to end in order to get Libervant on the market. But now, I am breathing a sigh of relief after hearing the company's plan of targeting the food impact for demonstrating superiority and getting Libervant fully approved.

One might think that demonstrating superiority in one specific circumstance might not be sufficient to declare that Libervant is superior to Valtoco, however, one should consider how that could play out in a real-world scenario. Keep in mind, that Valtoco's label does not state that there is a decrease in concentration and duration if Valtoco is administered following a meal. So, we should accept that patients using Valtoco are unaware of this possible issue. Considering that most people eat two or three meals a day, we have to agree that a Valtoco user could be susceptible to an inadequate dosage for a large portion of their day. Rescue meds are supposed to be operative in almost every circumstance possible to ensure the patient is getting an adequate amount of the drug in a short period of time. Not enough of a drug and too slow of uptake in essence removes the rescue label in my opinion. To me, this appears to be a major issue for the agency and should help Libervant win the argument for market approval.

I understand that running another study will cost money and will take some time to complete. However, a comparative study is not a full-blown Phase III clinical trial and should only take "a few weeks" to "two months" from start to finish. As a result, I am supportive of the study because the data might be the reason Libervant gets on the market to address the 1M Epilepsy patients that deal with refractory seizures. What is more, the company could also use the data and analysis when marketing Libervant to show superiority over Valtoco.

One could question whether the FDA will see the food issue as a strong enough case for claiming superiority. However, I will point out that the company stated that one of the FDA's concerns in Libervant's 2020 CRL was how food might impact the drug's efficacy. Considering the FDA was willing to issue a CRL for Libervant and mentioned this food concern, I would have to imagine they would be willing to consider it as an argument for showing superiority and supporting full approval. On the other hand, the FDA could determine that comparative study results are not sufficient for full approval.

Q2 Review

Although the market is currently reacting to the Libervant update, I believe investors ought to take a look at Aquestive's Q2 results to get a better perspective on the company's overall performance. As presented in Aquestive's Q2 results and business update from August 2 , total revenues in Q2 were $13.3M, down from $15.3M in Q2 of last year. Although this was a decrease, if you eliminate the one-time $2M milestone from KemPharm ( KMPH ) in Q2 of last year, total revenue essentially remained flat year-over-year. Still, Aquestive reported a $16.3M net loss for the quarter, which was up from the $12.4M in Q2 of last year.

In terms of financials, Aquestive worked hard to raise supplementary capital and reduce expenses, thus, extending the company's cash runway. Aquestive was able to finish Q2 with $17.7M in cash and cash equivalents. Furthermore, Aquestive announced a purchase agreement with Lincoln Park Capital Fund, which allows the company to sell up to $40M of AQST common stock to Lincoln Park over a 36-month period of the purchase agreement. What is more, Aquestive closed on an $8.5M registered direct making net proceeds of around $7.8M . Into the bargain, the company still has their standing ATM option when they need to tap the market for additional funds.

The better-than-expect revenues reported on August 2, in combination with expense reductions encouraged Aquestive to revise their full-year 2022 guidance with total revenues projected to be between $46M and $49M, which is up from $42M to $47M. The company also adjusted their non-GAAP adjusted EBITDA loss of about $37M to $43M, down from $51M to $58M. Moreover, Aquestive believes their non-GAAP adjusted gross margin to come in at roughly 70% to 75%.

My Thoughts on the Quarter

I believe the quarter was not as bad as the market has perceived. Indeed, the company's net loss per share has widened, and the company saw a drop in total revenues. However, the drop in revenue is mostly associated with a one-time milestone payment of $2M from KemPharm that occur in Q2 of last year. So, product revenues were basically flat year-over-year, which was better than analyst expectations. What is more, the increase in expenses was impacted by severance payments. Therefore, the elevated loss was not entirely caused by reoccurring expenses and could be a one-time speed bump as the company works on continues to work on reducing expenses.

Moreover, the market seems to have also overlooked the company's 2022 guidance update. The fact the company is expecting a notable improvement for their full-year non-GAAP adjusted EBITDA loss shows that their commercial performance is solid and their expense management will be effective. So, Aquestive should be leaving 2022 in better shape despite the share price suggesting the contrary.

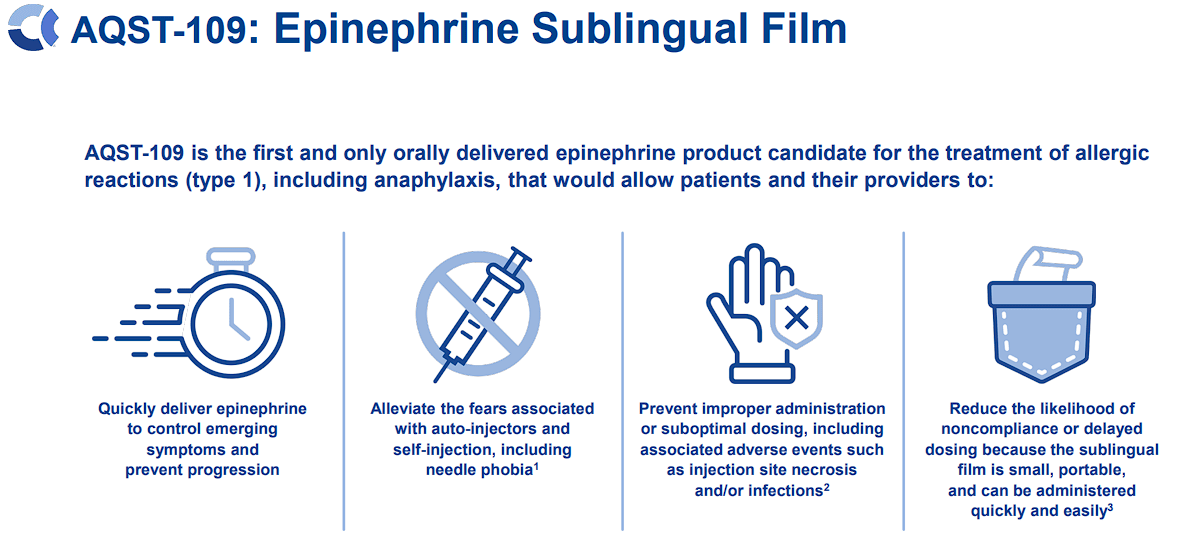

Another item to note is the fact the company is directing our attention toward AQST-109, which they believe is where they should devote their " resources , time, energy and cash. " Indeed, the AQST-109 anaphylaxis program has been at the center of my bull thesis due to its potential benefits over auto-injectors and its massive market of over 40M Americans that " are at risk of experiencing a severe allergic reaction, including anaphylaxis. " The company has produced impressive data for AQST-109, including Tmax levels that are comparable to EpiPen and data from the EPIPHAST study that revealed AQST-109's potential to be a rescue med in a variety of situations.

AQST-109 Highlights (Aquestive Therapeutics)

{kind=link}

Considering AQST-109's potential to launch into a $1.5B market , I have to agree with the company's elevation of this program.

If I was to summarize the quarter, Aquestive performed better than the market and the earnings headlines are suggesting. Moreover, Aquestive is working to get the company to profitability by reducing expenses and managing their cash flow while we wait for a potentially massive pay-off with AQST-109.

A Valuation Check

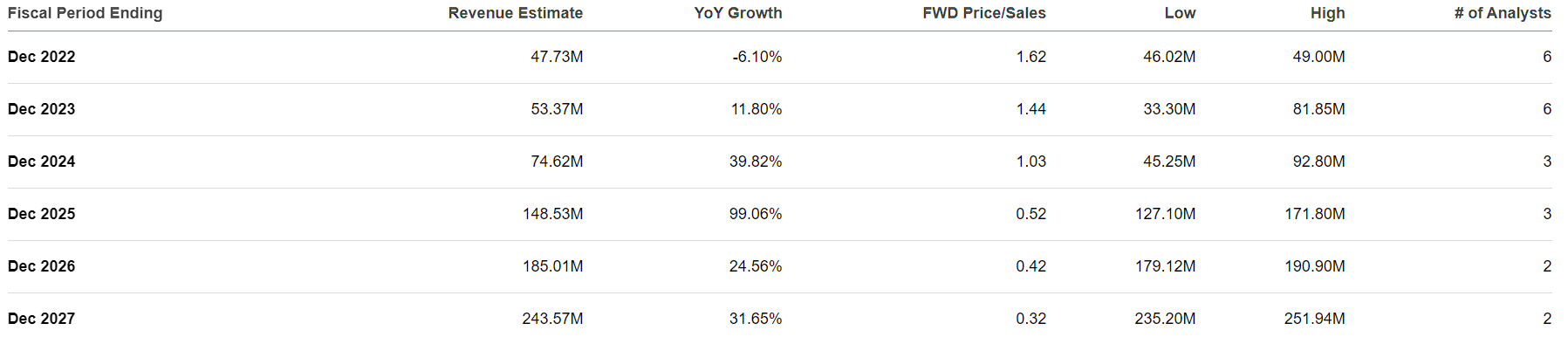

My thesis has been centered on the company's valuation, and the ticker is still trading at a substantial discount for its projected sales.

Aquestive Therapeutics Revenue Estimates (Aquestive Therapeutics)

{kind=link}

For 2022, the Street now projects Aquestive will pull in $47.83M for 2022, which is roughly 1.62x price-to-sales and 2.42x EV-to-sales. Seeing that the industry's average price-to-sales is 5x and EV-to-sales is 4x, we can say AQST is undervalued for its expected 2022 numbers.

If AQST was valued in line with its peers, it would be trading around $4.50 per share... for this year's projected revenue. Keep in mind, that the 2022 estimates do not include potential revenue from Libervant and AQST-109 . So, there is prospective revenue growth that would amplify AQST's discounted label.

An Offsetting Downside Risk

Despite my bullish outlook on AQST, I must concede that the company is almost certainly going to report losses for 2022 and probably for 2023. Although the company has several financing options, investors need to accept there is a strong possibility there will be some level of dilution in the coming years. This risk will most likely weigh down the share price until breakeven is in sight and the company has the cash runway to get there.

If the FDA fails to eventually green-light Libervant and generics erode Suboxone's revenue, we could see the breakeven point get pushed back. Obviously, this would increase the likelihood of dilution and possibly crushing the share price for a prolonged period of time.

Considering these risks, I still see AQST as a speculative ticker at this point in time. Therefore, AQST will stay in the Compounding Healthcare "Bio Boom" Portfolio.

My Plan

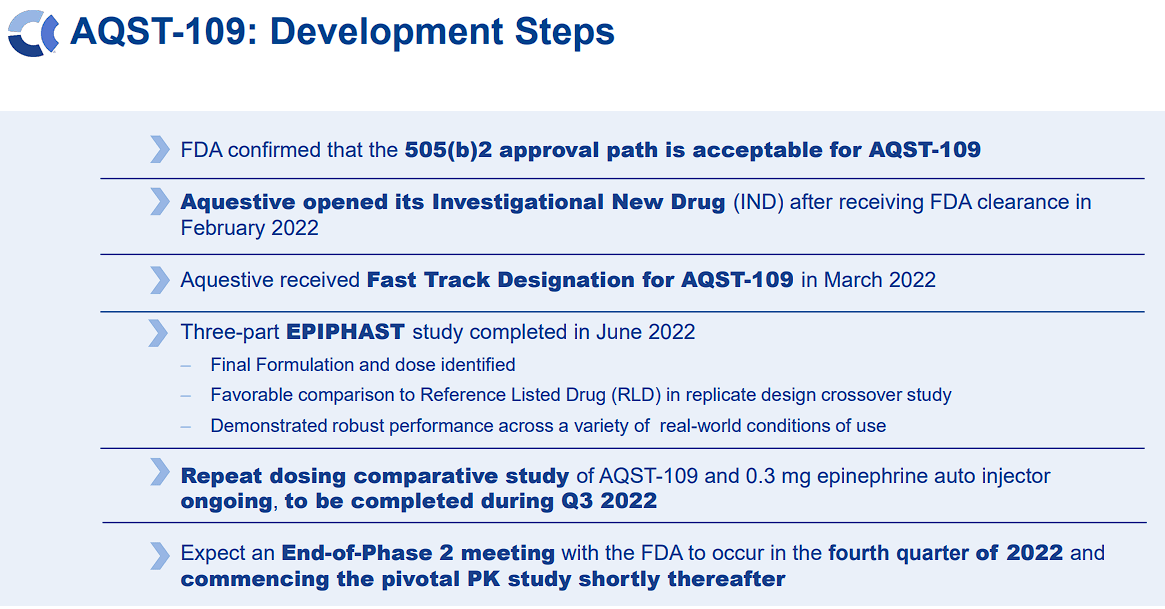

In my previous AQST article, I deliberated on how I was going to take advantage of the discounted price while we waited for Libervant's approval. As of now, I am going to remain aggressive with my cost-average strategy despite the uncertainties. I will continue to accumulate under the buy threshold of $2 per share and will increase my share sizing if the share price returns to under $1.05 per share. In addition, I will also increase my sizing if the results from the EPIPHAST II study show AQST-109 has at least equal to EpiPen, or the company reports that the FDA is in support of their comparative study for Libervant.

AQST-109 Development Steps (Aquestive Therapeutics)

{kind=link}

Once I have amassed a respectable position, I will look to secure profits at my AQST Sell Targets in order to transition the position to a "House Money" state. If the share price returns to my Buy Targets, I will resume buying AQST and will repeat the process.

Long term, I am still dedicated to maintaining an AQST position for at least five more years in anticipation the company will get AQST-109 across the finish line and quickly move to profitability.

For further details see:

Aquestive Therapeutics: Waiting To Buy After FDA Goes Halfway With Libervant