CA - ARC Resources: If Gas Bottoms ARC Could Rip Higher

2023-04-29 08:00:00 ET

Summary

- ARC has made a double-bottom in the mid-$10s and then in the last few weeks lurched through its 200 day SMA, near where it trades now.

- Gas seems to have stabilized in the low $2s and see a modest rebound as we get into injection season.

- We think ARC is attractive at current levels to investors who believe gas is due for a break higher.

Introduction

ARC Resources (AETUF) has been a disappointment since peaking in June of last year. The company has declined precipitously since last November when gas was still over $7.00 MCF, and there was a plausible case that gas might mount an assault on previous highs... if only . If only Europeans would keep ordering tanker loads of LNG for the winter...that never came.

A warm European winter combined with the outage of Freeport LNG, and the arrival of another couple of BCF/D from the Permian, and brimming inventories , knocked struts out of a rally thesis for gas recovery in 2022. I had rated them a hold at the time thinking that earnings would disappoint in Q-3.

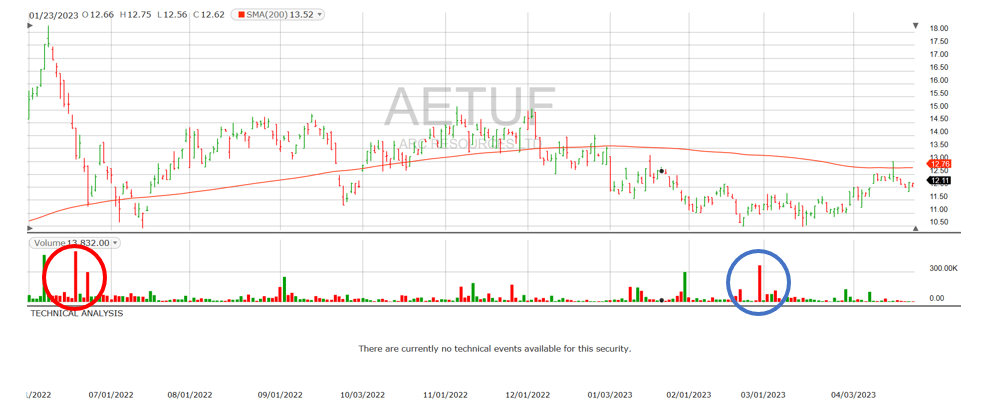

The "Smart Money" (Institutional Investors) was way ahead of the average Joes and Janes, and in a move nakedly telegraphed in June, someone dumped a massive 504.75 K shares @$19.05 per share-(see red circle). The stock then traded in a $13-15 range for most of the next six months, before trending down and finally making a double-bottom at $10.50 in February, with another 300K + share capitulation move as we entered March (see blue circle). From there the stock has rallied into the low $11's, from where it's made a run into the $12's in the past couple of weeks, and poked its head above the 200 day SMA in early April. Is this the start of something big? Let's see.

{kind=link}

The thesis for ARC Resources

ARC is Canada's third largest gas producer and it is number one producer of condensate, heavy ends of natural gas with API gravities between 50-80 typically. Oil-liquids below 50 API, makes up a minor contribution to ARC's revenues. Much of what the company is developing today came as a result of the all-stock merger with Seven Generations Oil in 2021 . As noted in the introduction to this article, ARC is interesting in part because of its size and reserves, but also due to the fact they are primed for growth. The slide below lists the "drill-ready" projects that will drive volumes and growth in the next couple of years.

ARC Opportunity list (ARC Resources)

Noteworthy as well is the recent agreement between British Columbia and the Treaty 8 First Nations . This provides a framework for set aside of key areas valued by the tribes and orderly development free of tribal litigation for assets outside these key areas. Terry Anderson, CEO of ARC comments on the impact of this settlement on ARC-

"The agreements executed between the BC government and the Treaty 8 First Nations pertain strictly to Crown lands. All our existing production in BC is on private or freehold land and we continue to receive permits there. Therefore, we have a clear line of sight to fully execute the 2023 program as planned."

Company filings

ARC is noteworthy, in addition to strong core assets, for adroit marketing of its products that drive above average realizations. The slide below shows how ARC shifting gas to various export hubs enables the company to maximize returns.

{kind=link}

It seem too simple to say, but if you can't move it out the basin to market, it does no one any good. ARC does a good job of this historically.

A few words on ARC's Montney assets

We have discussed the Montney on numerous occasions. It is a world class basin with ample gas, gas liquids, and crude oil assets. There are ample basin exits by pipeline for its production west to toward the nearing-completion gas liquefaction plants at Kitimat, and south to the Gulf Coast refining and LNG liquefaction complex.

Another attribute of the Montney is that is a "layered" reservoir with multiple targets that be accessed from a single wellbore. Similar in fashion to the Permian basin with its 6-7 different horizons spread out in various configurations as you go from the Midland basin to the Delaware basin. So too is the case with the Montney comprised of the gassier Upper, Middle, and Lower sections. Above that lies the Montney-Doig a frequent source of wet gas .

With thousands of identified new drilling locations on their premiere acreage blocks, ARC has a long runway of internally generated revenue streams. At a development rate of ~150 wells per year the company can adjust its plans to meet market surges or declines without resorting to the capital markets.

Some catalysts for ARC

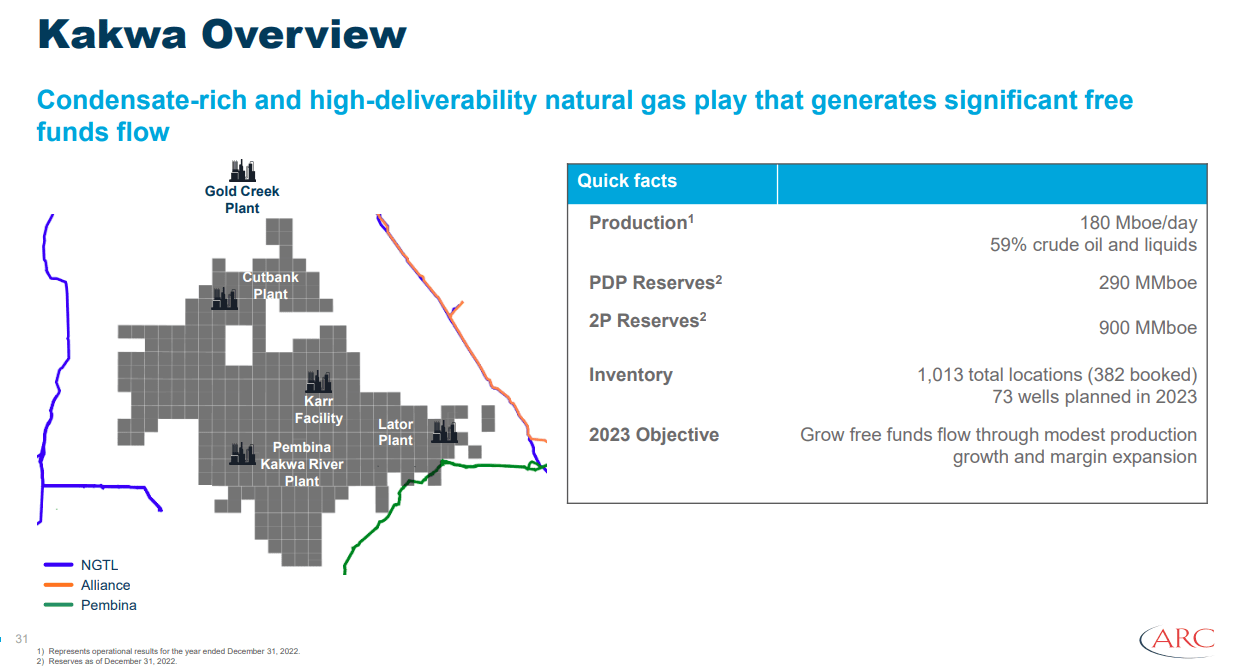

Condensate rich Kakwa was mentioned on the slide showing ARC's Montney footprint as a key item for development in 2023, following a major ramp to 180 K BOEPD in 2022. Terry Anderson, ARC CEO commented about the plans for Kakwa in the Q-4 analyst call-

"Meanwhile, well performance is exceeding expectations with Kakwa delivering some of the strongest condensate wells in Canada. And finally, we have confirmed that wider spacing implemented last year is improving long-term well performance. Pairing this with well cost reductions, we achieved a lower sustaining capital and further improved capital efficiencies at the largest condensate producing asset in Canada."

{kind=link}

Condensate is most commonly used as a feedstock for ethane production related to plastics and other petro-chemicals manufacturing. Pricing for condensate is often at a premium to other liquids production, and drives the interest in its production. ARC noted in the Q-4 call that it had received realizations of $107 per barrel for condensate. As with other ARC assets Kakwa is blessed with multiple export opportunities to take advantage of market imbalances that create pricing opportunities.

Attachie West sanction

CEO Anderson describes Attachie with 6 bn BOE of 2P reserves as the best development opportunity for ARC in 2023. Consisting of wet and dry gas reservoirs, ARC forecasts it to be a free cash flow generator for most of the next decade. Attachie has over 1700 identified so far unbooked drilling locations. Once sanctioned later this year, Attachie will require ~$700 mm in inflation adjusted capex to develop. Commencing in year four, capex reverts to maintenance levels and Netbacks rise to ~$500 mm per year for the next seven years.

Attachie funds flow forecast (ARC Resources)

Q-4, 2022 and Q-1, 2023 guidance ()

Production, funds flow and free funds flow per share registered 2% to 7% above consensus. ARC Q-4 capex ran $383 million and generated approximately $600 million or $0.96 per share of free funds flow. On a full year basis, ARC invested $1.4 billion which is within guidance and generated $2.3 billion of free funds flow, a 35% return on capital employed-ROCE. A pretty good showing.

ARC's prowess in moving molecules around also contributed to outperformance in the quarter. In periods of regional price dislocation, ARC has historically captured strong margins and this quarter was no different. This was due to long standing physical transportation agreements put in place years ago that would be difficult to replicate today.

The benefits of their market diversification, a low-cost structure and a diversified commodity mix, in which revenue was split approximately 50-50 between natural gas and liquids, contributed to a 67% margin in the quarter. On that note, ARC realized $107 per barrel for its condensate in the quarter, with light oil and condensate production of 86,000 barrels per day.

Looking ahead to 2023. Production and capital spending guidance remain unchanged. The plan is to invest $1.8 billion to deliver average production of 345,000 to 350,000 BOE per day. First quarter production is expected to be lower than fourth quarter of 2022 due to unplanned third-party pipeline outages impacting production in BC. These are anticipated to be fully restored this month. Offsetting the third-party outages is stronger-than-forecast base production which will support consistent production growth over the balance of 2023. Included in the 2023 budget, ARC invested $140 million in water infrastructure at Kakwa. This will expand margins by reducing corporate operating costs by approximately $60 million per year or $0.50 a BOE once fully commissioned in the second half of 2024.

In 2024, capital spending is expected to decrease by roughly 15%, excluding Attachie, while production is expected to be flat or higher than in 2023. The decrease in capital spending is due to several factors. The completion of the Sunrise expansion and water infrastructure investment at Kakwa, the absence of onetime investment to restore production in BC and lower anticipated base declines at Kakwa.

ARC continued to strengthen its balance sheet in the fourth quarter by reducing debt by an additional $240 million. At year-end, net debt was $1.3 billion or 0.4x funds flow, inclusive of the $1 billion of investment-grade senior notes outstanding. In 2022, they initially put forth the free funds flow allocation framework to return 50% to 80% of free funds flow to shareholders and executed to that plan. Through growing base dividends and repurchasing shares, ARC returned 71% of free funds flow to its shareholders with the remaining 30% used to further strengthen the balance sheet.

As debt was reduced, the range of returns to shareholders was increased to 50% to 100% of free funds flow and the company anticipates being at the middle or top end of that range in 2023.

Company filings

Hedging

This was costly in 2022, running nearly ¾ of a billion for the year. The company continues to take a conservative approach in 2023/4 with about 1/3 of forecast gas hedged for this year. Their goal is primarily to put a floor on price to ensure cash flow for operations. This is a fairly normal practice for gas drillers and leaves the other fraction exposed to spot prices for growth.

Risks for ARC

ARC has bet the ranch on Attachie. If for some reason they don't FID it in 2023, a significant source of future cash flow will be suspect. Analysts on the call asked some probing questions about the sanction status of the project and got mostly deflection for their efforts. CEO Terry Anderson comments on the progress toward FID-

"We are getting bits and pieces of information as we go through this from governments. ARC has been engaged, I guess, with the Ministry of Mines, Energy and Low Carbon Innovation in BC as well as BCOGC. The intention is for us to understand the process more so than anything else. We understand some of the basic details that is involving the agreement. But logistically, we want to understand how the permits will be issued and how the process -- what is the process in terms of getting the projects moving on. So that's really what we are waiting for."

There is no reason to be pessimistic about Attachie reaching FID, but Anderson used a lot of verbiage that would have been unnecessary if the path was completely clear.

Your takeaway

ARC's stock has been trading in a rock-solid range in the upper $11's to low $12's, a 35% decline from June's high. You'll remember my comment about the "Smart Money" leading the pack here. This is a 1.5X multiple to EV/EBITDA on a TTM basis, and an absurdly cheap $11,142K per flowing barrel.

It is obvious these assets are undervalued and that may bring the Smart Money back in. The news on gas has been so uniformly bad, that no gas oriented companies are getting a bid currently. But, capital seeks a return and gas seems to have been making a bottom over the past month. Big investors are faced with a choice of pay 5-10X EBITDA for liquids focused companies, or taking on some risk for an outsize reward at a later time. My bet is that it's risk on.

I was critical about the lack of clarity on Attachie in my comments on risk. That concern noted, my expectation is for it go forward and it wouldn't surprise me to hear that it's gotten approved in early May when they report Q-1, 2023. This will lead to a rally in the stock as this cash flow is critical to their thesis.

I think investors can take a position in ARC at current prices with relatively little risk in a stable or rising gas price environment. Analysts are bullish on ARC with a BUY rating and price targets of $15-18.00 per share in the next year. I think if we get any kind of move back toward $2.50 MCF for gas that $18 target is achievable. For those looking for income, ARC is paying a 3.66 YOC dividend of $0.44 per share.

For further details see:

ARC Resources: If Gas Bottoms, ARC Could Rip Higher