MCD - Arcos Dorados: A Strong Exposure To LatAm Through McDonald's

2023-09-27 05:41:58 ET

Summary

- Arcos Dorados is the largest franchisee of McDonald's in Latin America, operating in 20 countries where it has exclusivity to operate McDonald's.

- The company has a clear growth strategy focused on opening more profitable restaurants and implementing digital solutions.

- Despite the valuation gap with its peers, ARCO has strong financials and is well-positioned for expansion in the region.

Editor's note: Seeking Alpha is proud to welcome Moram Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Arcos Dorados Investment thesis

Arcos Dorados (ARCO) is trading at a significantly lower valuation compared to its peers, making it an attractive investment opportunity in a rapidly growing region, Latin America. This investment also comes with reduced uncertainty due to being the biggest franchisee of McDonald's (MCD) globally, of which Arcos Dorados holds exclusive rights in over 20 countries in the region.

Exclusivity for McDonald's franchisee in 20 Latin American countries: ARCO enjoys exclusive rights across 20 high-potential Latin American markets, including major economies like Brazil, Mexico, Colombia, and Argentina.

Margin recovery: Despite the challenges posed by the COVID-19 pandemic and inflationary pressures, the company has demonstrated a robust ability to recover and maintain healthy profit margins.

Attractive Valuation: ARCO currently boasts significantly lower valuation multiples when compared to its industry peers, suggesting strong potential for capital appreciation.

Gaining market share in an unpenetrated market: In a largely untapped and rapidly growing market, ARCO is strategically positioning itself to capture substantial market share

What is Arcos Dorados?

Arcos Dorados represents McDonald's brand in Latino America and the Caribbean, being the largest franchisee in terms of revenues (4% of the total) and number of restaurants (6% of worldwide restaurants). It has an exclusive partnership to own, operate and sub-franchise McDonald's in 20 countries in South America and the Caribbean (in all the most populated countries: Mexico, Brazil, Argentina, Colombia, Peru etc.) where the company already operates 2,313 restaurants at the end of the first quarter. 29% of its restaurants are sub-franchises, although the share of revenues from them is only 4.5% (this number has been quite stable during the last five years).

As you may already know, the franchising business is of much better quality, with higher margins but lower revenues. We want to make clear that Arcos Dorados is not comparable to McDonald's. While McDonald's main income stream is the rental income that the franchisees pay, ARCO is the one paying the royalty fee to McDonald's. Arcos Dorados' main revenue source is the operations of the restaurants.

Arcos businesses are much more similar to a normal restaurant chain. They make an initial investment to buy or lease the land, the equipment and the building to later either operate it or sub-franchise it. If the revenue source was the royalty fee from the sub-franchises, we would be talking about a different kind of business.

The royalty fee expected to be paid to McDonald's is around 6% of total revenues in 2023 and 2024. We think it will probably rise slightly onwards. This is why McDonald's EBITDA margin is an extraordinary c.50% , and Arcos stays around 10% . The royalty fee from sub-franchised restaurants to Arcos is 5%.

The company divides its geographic revenues into three different regions: Brazil, NOLAD (North Latin America - main countries are Mexico, Costa Rica, and Panama), and SLAD (South Latin America - main countries are Argentina, Chile, and Colombia). In 2022, evolution of the revenue per region since Covid has been as follows:

Data: company, Source: Moram.eu

The operating margins are much higher in Brazil (13.1%) vs 6.7% and 8.5% in NOLAD and SLAD, respectively. This is mainly due to the higher percentage of sub-franchised restaurants in Brazil. When analyzing the margins in future results it is important to understand the mix between regions. For 2023, we expect the Brazil division to perform very well with also significant growth for the other two regions.

Why do we believe that an opportunity exists?

We were initially attracted to Arcos mainly for two reasons:

The opportunity to gain exposure to South America with a defensive approach. This is, having a clear view on what is the dynamics affecting the company (trends on food and labor inflation, customer demand, etc.), and limiting the country risk that would have investing in only one country of Latin America or the Caribbean.

The strength of McDonald's brand and the disparity in valuations with other public restaurant chains.

As we continued deepening into it, we liked the cared strategy of growth for the coming years backed with excellent operations from recent history. All the sector was deeply affected by Covid and Arcos as one of the main players in the industry has strengthened its competitive and financial position. Now, the strategy is clear, open more restaurants of the most profitable kind the company operates in strategic locations and implement digital solutions that drive the ARPU up.

Let's analyse the feasibility of their strategy, examine their financials, and compare them with their peers to get a better idea of the investment opportunity's magnitude. Additionally, we will provide our perspective and conclusions.

As you can observe in the graph, the number of restaurants has remained stable during the last five years. As already mentioned, the perspective for the next years is to accelerate the openings:

Data: company. Source: Moram.eu

Own elaboration. Most of the closings were in Venezuela, driving down the Caribbean results with the subsequent decision of the management to divide this division into NOLAD and SLAD.

McDonald's brand is one of the best-known brands around the world. And the defensive nature of the business has also been proven during the pandemic and the recent inflation wave. Systemwide comparable sales grew at a rate 2x to 3.3x inflation in 2022. For Q1 2023, it has been 1.7x, with minimum of 1.5x in each division.

When accounting for systemwide comparable sales, Arcos takes into consideration both the restaurants they operate and the sub-franchised. With this metric, we have a more global view of what is going on in the demand.

Arcos's strategy has been very carefully developed even before the pandemic. With a strong bias to boost sales through the Digital, Drive-thru and Delivery channels, the so-called 3Ds strategy:

Digital: In 2022, the digital channels (the mobile app, delivery, self-order kiosks and order ahead) comprised nearly 41% of total revenues . This number has scaled up to 47% in Q1 2023 and we expect this trend to continue thanks to the leveraging of more than 15 million MAUS.

For 2022, 17% of revenues were identifiable sales, from which Arcos can get data from the customers to be more efficient in marketing. They want to grow this number to 40% by 2025. This will be an important factor to drive growth in the top-line as the ARPU is much higher when the company can address the customer with better data. The ARPU in identifiable sales has grown significantly from $38 in 2020 to $55 in 2022.

Drive-thru: Almost exceptionally biased by the Covid impact, the sales more than tripled between 2019 and 2022, with a continuation of the positive outlook during the first months of 2023 with a 13% growth. As of today, 50% of restaurants have drive-thru and 90% of openings will also have this option because the idea is that this will be the percentage of FS respect to the total. The drive-thru is very efficient compared to in-stores sales as the ARPU is higher and the costs are slightly lower.

Delivery: The third leg of the 3D strategy is also performing quite well with a 40% increase in Q1 23 vs Q1 22. QSR delivery prices are between 15% and 20% higher than pick-up prices, more than offsetting the additional cost.

KROLL

The company divides its restaurants into 4 types: Free-Standing (50% of the total), In-Store (12%), and Mall Store and Food Court (38%). Despite being already the more common type of restaurant, another leg of the strategy is to increase even more the percentage of Free-Standing restaurants, which are much more profitable as they give the opportunity to sell through drive-thru and a better option for delivery. Every new unit increases the average sales of the unit restaurant. The plan of the company is that 90% of the new restaurants will be Free-Standing.

To decide in which areas to make new openings, the strategy is clear:

Open new cities and unpenetrated areas, mainly with FS restaurants and Fill Penetrated areas with gaps with small footprint buildings.

For the years to come, we consider it to be a big advantage to be the first movers. Imagine an area of 10,000 inhabitants. The first QSR to occupy this area can develop their operations and earn normal profits. But potential entrants will think twice as there may be no space for 2 QSR. We consider the company to be well established to start with this acceleration in the number of openings for the following years.

On its last investor's day, the management targeted to open 1,000 during the next 10 years. This is an absolute 45% growth from today's figures. And we have no doubt there is enough potential market. Currently, there is one restaurant per every 240,000 inhabitants, while in the US there is one McDonald's per every 24,000.

If we compared the number of McDonald's restaurants per GDP PPP in the US, ARCO would have to open 2.6 times the number of restaurants as of today to match the figures in the US. Of course, we may think that (maybe for cultural reasons) Latin America and the Caribbean won't reach these figures. But what is clear is that there is still room to grow at a high pace.

In the first months of the year, the company targeted 75-80 openings for 2022, with heavier weight in the second half of the year. They will also conduct 250 modernizations. This will translate into $350 million in Capex. The business is able to generate all the cash needed for these investments and they have discarded any capital increase or issuing of bonds.

Despite the +45% increase in share price during the last year, another important reason why we have decided to present Arcos is the attractive financials and valuation.

Financials And Valuation

As mentioned earlier, Arcos Dorados' revenues depend on sales in its own restaurants (95%) and its sub-franchises (5%). However, the margin for the sub-franchises is 58%.

Like the entire industry (as discussed in our Good Times Restaurants thesis), Arcos Dorados' margins have been significantly impacted by the effects of COVID-19. The situation in South America was worse and lasted longer than in Europe and the United States. Additionally, inflation has further affected their margins in 2021 and 2022. To mitigate these challenges, the company has implemented price increases and continued to open new restaurants, resulting in revenue growth of over 25% year-on-year.

It is important to highlight (as it is one of the major risks we identify) the currency hedging strategy. The company's financial strategy includes addressing foreign exchange risk. A significant portion of its cash flow is generated in various local currencies, while certain liabilities are denominated in U.S. dollars. To manage this exposure, the company focuses on sourcing locally when possible and implements a risk management policy. This policy involves employing a rolling hedges strategy, hedging up to 50% of projected exposure for nine months or more. These measures aim to mitigate the impact of foreign exchange fluctuations on the company's financial position.

Data: company; Source: Moram.eu

In SLAD, the margins were particularly bad because it was the most affected region by Covid, being the one with the most closings. The margins in Brazil are higher due to the larger percentage of restaurants that are sub-franchised. For the years to come, we expect these margins to improve slightly due to a more controlled labor and food and paper costs for all the divisions as well as synergies & economies of scale.

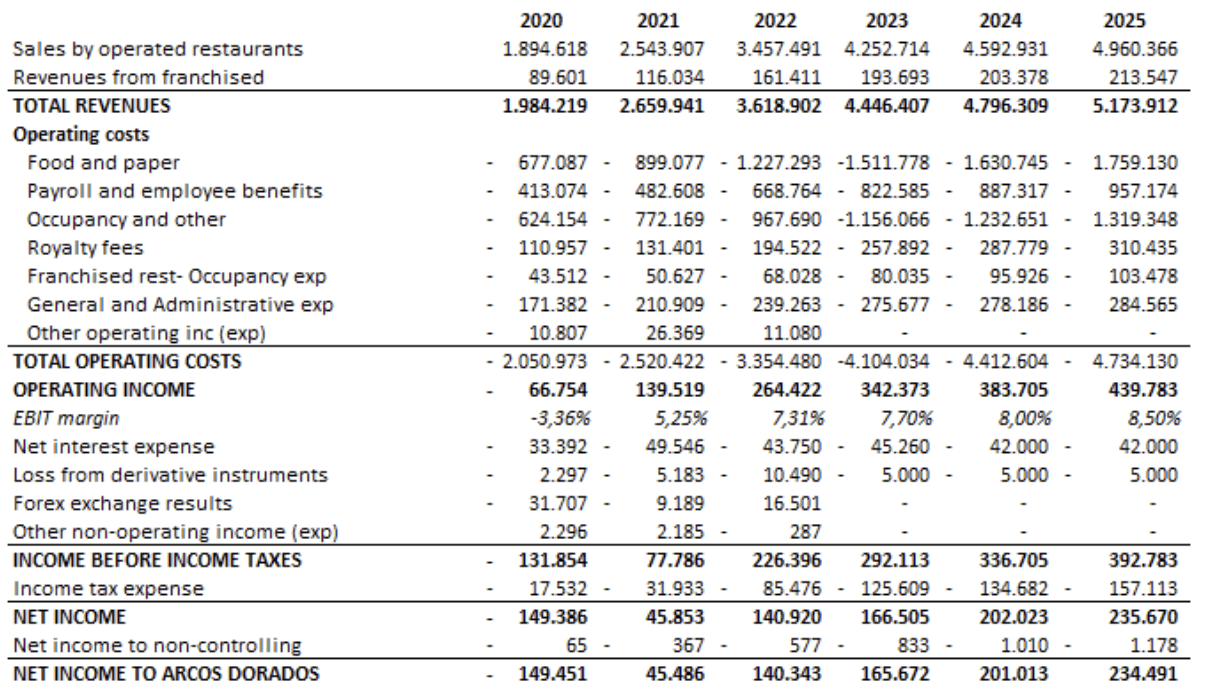

Our estimations for the income statement for the following years is as follows:

Our estimations for Arcos Dorados (Moram.eu)

{kind=link}

This year's top-line growth will be higher than usual thanks to the recovery of the physical sales and the continued good performance of the digital sales. For 2024 and 2025 we have estimated a high-single digit growth thanks to the opening of new restaurants. Recall: 75-80 to be completed in 2023 and with no stop in the pace in the mid-future.

We estimate that the food and paper costs and employee expenses will remain stable in the forecasted period. We have recalculated the royalty fees with the 6% recently introduced. The fixed costs (G&A and occupancy) will slightly decrease over the years thanks to the leveraging. This will bring the EBIT margin up from 7.3% in 2022 to 8.5% in 2025. We think it is more than reasonable given the gain of scale, the opening of more profitable restaurants, the higher ARPU and a more normalized job and raw materials markets.

We do not expect Arcos Dorados to issue debt during these years and estimate an interest rate around 6%. We also expect a tax rate close to 40% for the forecasted period, with 2023 above the normalized effective tax rate.

With this scenario, the company is trading at around 12 and 10 times net earnings of 2023 and 2024, respectively. Looking at EBITDA, Arcos is trading at a bit more than 5 times 2023's EBITDA.

We believe that a conservative multiple for is 8 times EBITDA, which is almost half of QSR. However, we model in the highest region risk and the lower quality compared to other powerful businesses. With this we estimate a fair value of $16 per share, which implies that the share is trading at a 60% discount versus our estimated value.

{kind=link}

By making a simplified calculation, Arcos' enterprise value (EV) can be estimated as ($2 billion + $715 million - $201 million=2.5B), and the trailing twelve-month ((TTM)) EBITDA, as mentioned earlier, is $424 million, with over $480 million of EBITDA estimated for the full year 2023.

Debt

Arcos has $736 million in debt and a cash position of $231 million. With a trailing twelve-month EBITDA of $408 million, we believe that the debt is well-controlled, especially considering that the interest rates are fixed. The net debt/EBITDA ratio stands at 1.23. (Covenants Net Debt / EBITDA in the three banks are the same, 4.5x)

Data: company; Source: moram.eu

In recent years, the company has conducted several tender offers to repurchase a portion of its bonds in the market. They intend to do so again if the opportunity arises. However, given the current market conditions, they believe it does not make sense to proceed with such offers at the moment.

We understand that certain risks, such as the dual share structure and the perception of higher country risk and currency risk in Latin America compared to the US, may contribute to the valuation gap. Also the option of a potential de-listing. However, we believe that these factors alone do not fully explain such a significant gap in valuation.

Risks

Breach of Master Franchise Agreement ((MFA)) with McDonald's: The possibility of Arcos to run the business depends on the MFA with McDonald's which expires in 2027. The resolution of a 10 years extension will be known before August 2024. If there is a material breach of the MFA, McDonald's has the right to terminate the contract.

Royalties: McDonald's has not increased its royalties to its franchises for the past 30 years, but it has just raised them from 4% to 5% in the United States. While this move does not affect Arcos Dorados since it only operates in Latin America, it opens the door for McDonald's to replicate the same move in these countries in the future.

Political instability: The political instability in some countries of Latin America can lead to impoverishment as has happened in Venezuela where Arcos has been forced to shut down some restaurants. New and more strict tax or environmental regulations may potentially harm the business.

Currency exchange: Related to point above but so significant that deserves a point for itself. All revenues and expenses and most of assets and liabilities are in currencies different from the USD. Any depreciation of the local currency against the USD affects negatively the level of revenues presented in the financial statements.

Reputational issues: Arcos Dorados may face reputational challenges related to concerns about the nutritional value of fast food, environmental sustainability in food production and packaging, labor practices within their franchises, or even intoxication cases as it happened in other QSR as Chipotle (CMG) or Taco Bell (YUM).

Conclusion

Arcos has recovered well from the pandemic and is ready to expand their footprint through Latin America and the Caribbean. Arcos has shown their capacity to increase prices further than inflation. The competitive position is excellent being the main QSR restaurant in South America and gaining market share over the last years.

We have been pleasantly surprised by this company, and as we mentioned earlier, we believe it is an interesting way to gain exposure to an emerging geography with the added security of partnering with a brand like McDonald's. The exclusivity agreement in all countries, but especially in Mexico and Brazil, is particularly appealing to us. We also believe that the valuation gap with its peers is excessive given the risks we see.

For further details see:

Arcos Dorados: A Strong Exposure To LatAm Through McDonald's