CA - Aritzia: Not A Buy Despite A 50% Decline In Its Value

2023-09-29 12:09:08 ET

Summary

- Aritzia shares have experienced significant volatility, with a 50% decline, largely due to inflation and weak macro conditions.

- Concerns over comp sales decline, weak operating margin, and high inventory levels are expected to ease due to improvements in IMU, lower product costs, and a decline in warehousing costs.

- The challenging macro environment and potential downside risks make the current valuation unfavorable, leading to a Hold rating.

Investment Thesis

Aritzia ( ATZAF ) shares had been on a rollercoaster since the pandemic, with the shares climbing over 200% till the end of 2022 before inflation and the weak macro environment caught up with them, rendering the shares down over 50% for the year.

Comp sales declines, weak operating margin, and elevated inventory levels remained a cause for concern going into Q2, however, the pressure is likely to ease going forward driven by IMU improvements, lower product costs, and a decline in warehousing costs. However, we believe, given the considerable challenging macro environment that pressured the middle to high income earners, its core segment, we continue to remain uncertain with potential downside risks. We believe current valuations do not offer a favorable risk-reward, and we initiate a hold .

Company Overview

Aritzia is an integrated design house, offering a wide range of exclusive brands within the Everyday fashion category. It designs apparel and accessory collections for its fashion brands, including Wilfred, Tna, Babaton, Sunday Best, Le Fou Wilfred, and Denim Forum. It serves its customers through its 115+ boutiques across the US and Canada as well as through its online website.

Historical Track Record

Aritzia reported strong growth, historically driven by the continued expansion of its boutiques along with its unique positioning in everyday fashion, leading to strong brand resonance across a wide range of consumers. However, COVID led to the shuttering of its boutiques which significantly jolted the company's operations while digital growth outpaced overall expectations, and it managed to end the year with a 13% sales decline, albeit at the cost of its profitability due to the sticky fixed and rental costs. It reported strong HSD comp sales growth during the FY19-FY20 period while FY21 and FY22 remained exceptions due to COVID shutdowns before again ramping up during FY23 posting strong 20%+ comp sales growth.

Historical Comp Sales Growth

Company, Author

However, the FY23 revenue growth rate came at the cost of profitability as a result of a decline in gross margins due to markups and warehousing costs, along with inflationary pressures, while SG&A expenses also spiked as a result of wage hikes.

| Particulars |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| FY23 |

| Revenue |

| 874 |

| 981 |

| 857 |

| 1,495 |

| 2,196 |

| Adj. EBITDA |

| 161 |

| 173 |

| 77 |

| 289 |

| 351 |

| EBITDA Margin |

| 18.4% |

| 17.6% |

| 9.0% |

| 19.4% |

| 16.0% |

| Adj. Net Income |

| 95 |

| 97 |

| 26 |

| 177 |

| 215 |

| Net Income Margin |

| 10.8% |

| 9.9% |

| 3.0% |

| 11.8% |

| 9.8% |

Challenging Quarter

Aritzia reported a tough quarter for Q2 FY24 with a comp sales decline of 4.3%, one of the first in a really long time excluding COVID-led disruptions, as a result of softening consumer demand echoed by management last quarter, and higher competitive intensity as well as lapping tougher comps (Q2 2023 revenue was up over 120% to pre-pandemic levels). What remained a surprise was the management highlighting that the product assortment and new styles were not well received by the customers, which remained the harbinger of its strong brand resonance and strong comp sales growth over the years.

We believe our second quarter top-line trend was impacted by the level of new styles in our product assortment...The trade-off was at as we faced bandwidth constraints, our level of new style development was not optimal.

- Jennifer Wong, CEO, Aritzia Inc.

Retail revenue increased 3% driven by an improved performance from new and repositioned stores (total boutiques increased by 4 YoY) partially offset by softer comparable sales. E-commerce sales declined 1% YoY as a result of softer traffic during the Summer sale period, offset by an improvement in conversion.

Gross margins declined 690 bps YoY as a result of similar challenges it faced during Q1 2024 including 1) Higher markdowns and product cost inflation 2) Fixed cost deleverage amidst declining comp sales and 3) additional warehousing costs ahead of its new distribution center which opened in late August. SG&A expenses as % of revenue deleveraged 400 bps as a result of a jump in wage costs and costs related to the distribution center amidst flattish sales growth. Adj. EBITDA margin declined 11.7 percentage points as a result of the decline in gross margin and SG&A deleverage. It reported an Adj. EPS of $0.03, declining significantly from $0.44 it posted a year ago as a result of weak operating margin and higher interest expenses due to new store openings.

The balance sheet position remained stable as the company ended with a cash balance of $76.5 mn and having drawn $100 mn from its $175 mn revolving credit facility for working capital purposes, which it intends to repay by the end of next quarter. Inventory position remains elevated as the net inventory position increased by 10% YoY as well as sequentially from $485 mn to $500 mn.

Management reaffirmed its FY24 guidance of sales growth of 2-7% YoY at $2.25-$2.35 bn including benefits from a 53rd week. It expects Q3 revenues to be flat or slightly down in line with current trends, again facing tough comparables. We believe the guidance is achievable driven by an improving momentum of its fall collection as well as growth largely driven from a 53rd week and new stores, assuming a mid-single-digit comp decline. Gross margin pressure is likely to ease, and it expects a 300 bps sequential improvement from Q3 and an overall 300 bps decline for FY2024, driven by higher IMU and normalizing product costs along with a decline in warehousing costs after the opening of its distribution center. SG&A expenses are also expected to increase 300 bps YoY, in line with its previous expectations as a result of higher wage costs.

Valuation

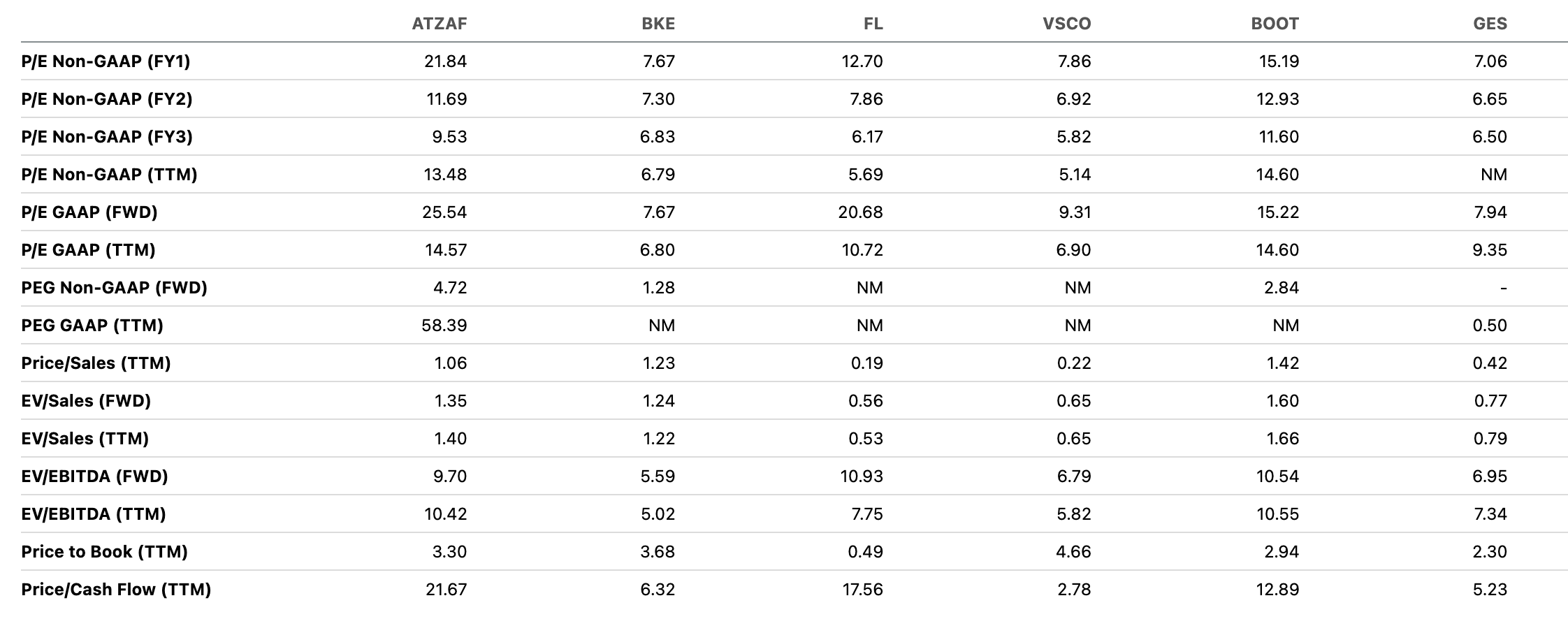

Aritzia still trades at a premium with FY25 P/E of 11.7x compared to its peers trading at 8.3x, however, below its long-term average of 21x Fwd P/E. We believe that given the current macroeconomic backdrop amidst a declining consumer confidence and student loan repayments worth over $1.7 trillion in US commencing soon warrant a significant discount with the company facing comp sales declines (as against strong HSD comp sales growth historically). We initiate with Neutral given the risk reward is not favorable given competitive intensity and macro pressures and await customer reception of their new product lines.

{kind=link}

Risks to Rating

Risks to rating include:

1) Prolonged macro pressure and declining customer activity can lead to a significant decline in comp sales growth

2) Competitive intensity can lead to a prolonged pressure on their gross margins

3) Upside risks include its cost savings from its newly opened distribution center can be higher than anticipated which can lift gross margins

Final Thoughts

Aritzia has strong brand resonance amongst its customers, and its trendy product lines have driven strong top-line growth over the years. However, the company's inability to develop product lines well received by the customers remains a focal issue for the quarter, while the rest of the narrative was largely in line with expectations. We believe the current valuation multiple does not offer a favorable risk-reward, and we remain on the fence and await to see how trends play out, particularly during Q3 amidst weakening macro and commencement of student loan repayments.

For further details see:

Aritzia: Not A Buy Despite A 50% Decline In Its Value