CA - Aritzia: Potential Path To Global Fashion Dominance

2023-11-21 05:32:17 ET

Summary

- Aritzia has grown revenue and EBITDA at a CAGR of 22%, as the business has successfully executed a strong growth strategy, underpinned by quality designs and customer engagement.

- Its trajectory has slowed, owing to macroeconomic conditions impacting demand. Although this is unsurprising, its working capital management leaves the business in a tough spot.

- Following this, which we expect to subside in mid-to-late 2024, we see healthy growth returning. Management is executing well, driven by new locations and effective social media marketing.

- When compared to its peers, the company’s financial performance is strong. Aritzia has achieved better growth and operates with superior margins.

- Our concern is that its poor working capital management and slowing demand will compound to contribute to a tough Q3/Q4.

Investment thesis

Our current investment thesis is:

- Artizia ( ATZAF , ATZ:CA )has the potential to be the next big fashion brand, with strong customer engagement, a rapidly growing following, expertise in design, and a solid growth strategy. Any concerns we have are around its short-term performance, which looks to be rapidly deteriorating.

- Beyond this point, growth is inherently uncertain due to how competitive the apparel industry is. For this reason, investors require a level of comfort that cannot be provided today. For this reason, we suggest caution.

Company description

Aritzia is a Canadian fashion brand founded in 1984, renowned for its contemporary and stylish clothing, accessories, and lifestyle products. With a focus on empowering women through fashion, Aritzia operates a chain of boutiques and an online platform, catering to a diverse customer base.

Share price

Aritzia's share price performance is a tale of two. Initially, the business achieved impressive growth, reaching returns of over 200%. Following this, it has declined substantially and fallen below its initial price. This is driven by both the wider market weakness and a decline in financial performance.

Financial analysis

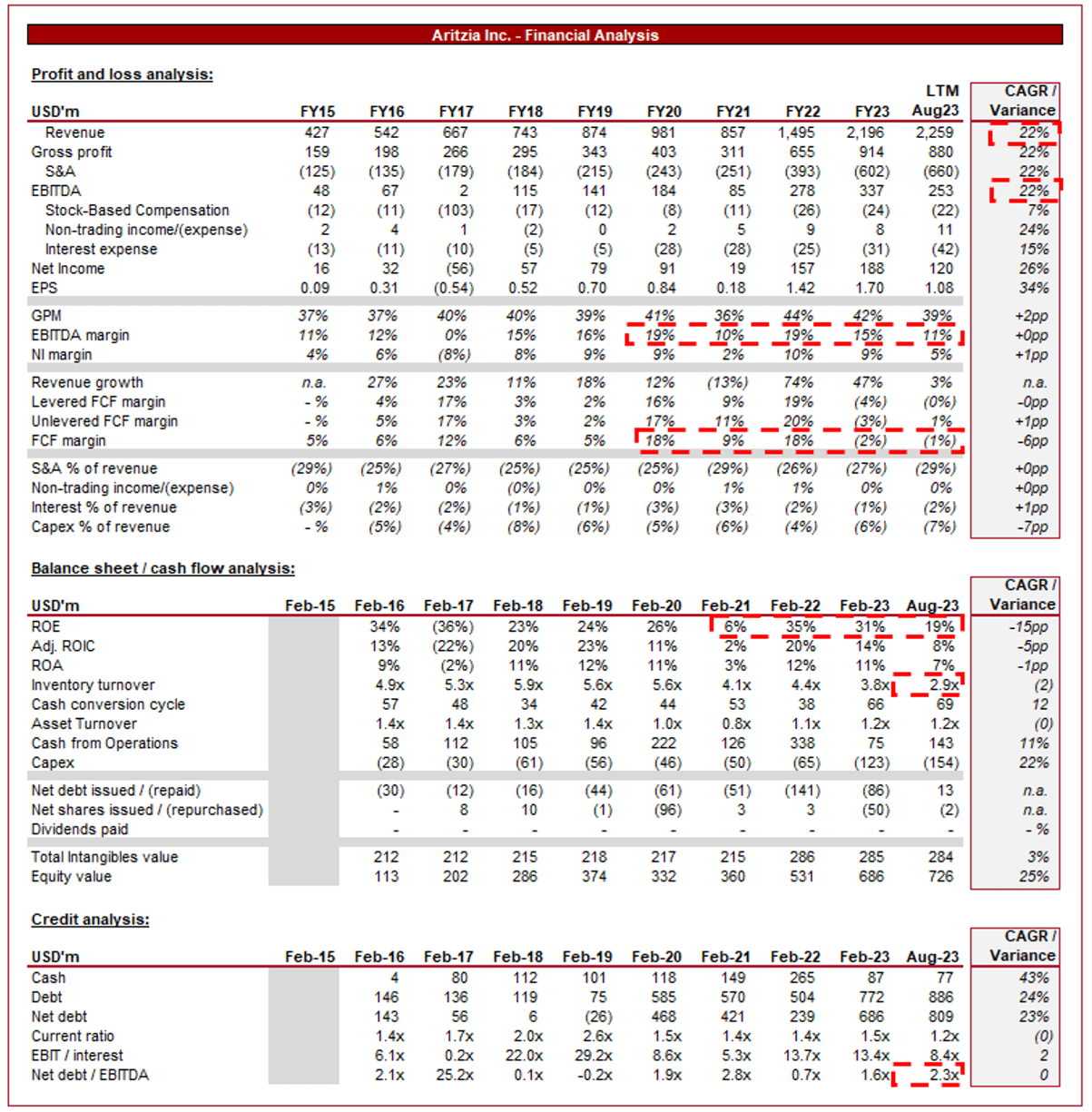

Aritzia financials (Capital IQ)

{kind=link}

Presented above are Aritzia's financial results.

Revenue & Commercial Factors

Aritzia's revenue has grown exceptionally well, with a CAGR of 22% during the last decade. Growth has been broadly consistent, with only a single decline attributable to the pandemic. In conjunction with this, EBITDA has grown at a comparable rate, although with far more volatility.

Business Model

Aritzia operates as a vertically integrated design house, fashion retailer, and wholesaler. It designs and manufactures a variety of women's clothing and accessories, selling its products primarily under exclusive brand names.

{kind=link}

Aritzia has excelled thus far in staying on top of fashion trends. Its design team has a keen eye for emerging styles and quickly incorporates them into their designs. This ability to respond rapidly to shifting fashion trends ensures that its offerings remain relevant and appealing. The fashion industry can be incredibly cut-throat due to ever-changing consumer trends but thus far, the business has managed this risk well. Its small brand portfolio allows it to experiment and adapt quickly.

{kind=link}

The company places itself in the "Everyday Luxury" segment. The company is essentially targeting consumers who are seeking higher-quality goods compared to the mass-market offering.

{kind=link}

Aritzia invests in creating an exceptional in-store and online shopping experience. Its retail spaces are carefully curated, offering a blend of aesthetic ambiance and personalized service. This is all part of selling the luxury experience and enhancing its brand. Online, it provides a user-friendly interface, a seamless checkout process, and good customer support.

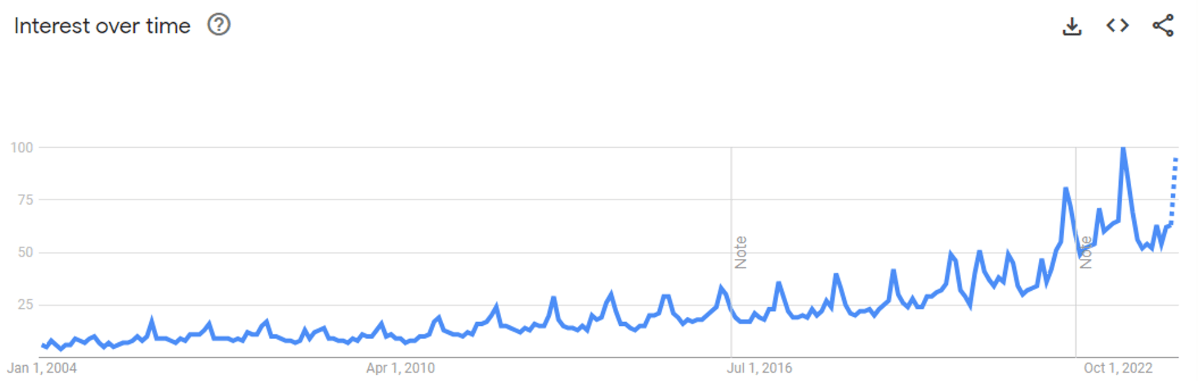

Aritzia invests significantly in marketing and branding efforts. It has collaborated with influencers, engaged in social media marketing (influencer marketing primarily), and participated in fashion events to create brand awareness. As the following illustrates, this has been very successful thus far. The key now is to maintain this trajectory and further expand its presence in the US.

{kind=link}

Its strong online and physical presence allows the company to integrate its online and offline channels effectively, offering services like click-and-collect and easy returns, providing a seamless shopping experience for customers.

{kind=link}

By controlling every aspect of the supply chain, it can ensure quality, maintain consistency in its designs, and react quickly to changing market demands. This, alongside the broader development of its brand, allows for premium pricing relative to the market.

Management's growth strategy involves three key factors:

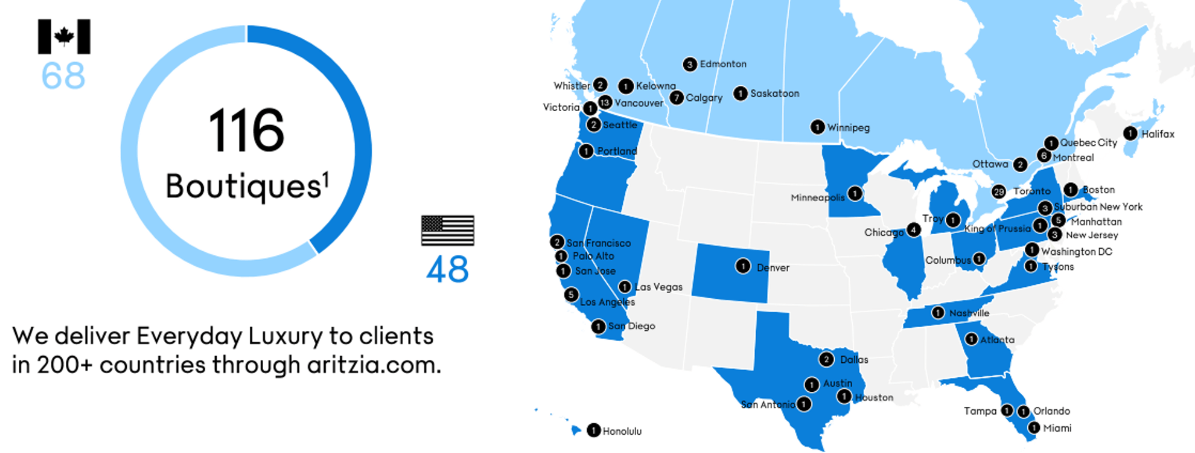

- Geographical Expansion - New store locations are currently driving strong growth, with a payback period of 12-18 months. Beyond just growth, Management is seeing brand improvement, client acquisitions, and greater e-commerce traffic.

- e-commerce - Investing in its online capabilities to both support its physical locations and better drive sales through the shopping experience. Examples of this include personalizing suggestions and a seamless buying experience.

- Increased brand awareness - Further developing its social community, with the objective of developing loyalty and awareness. This involves promoting its outspoken existing customers on social platforms, operating a VIP program, and continuing to develop relationships with influencers.

We concur with this growth strategy, with brand development being absolutely critical to maintaining its existing trajectory. The brand is clearly in a "hype" phase and so it is very important that as this subsides, the business does not fade to irrelevance. We see a nuanced approach to store expansion and brand investment, which is important to not dilute its luxury image.

Apparel Industry

We believe the following factors are critical to industry growth in the coming years:

- Strong Brand Identity - Developing a unique brand is absolutely critical to standing out within this industry. This involves creating a loyal customer following, one that is willing to consistently purchase products and also speak about them on social platforms.

- Focus on Millennials and Gen Z - Aritzia strategically targets the millennial and Gen Z demographics, staying in tune with the preferences and values of these consumer groups. This is the most lucrative demographic due to spending patterns, the most influential in the market, and also the one with the most resilient demand.

- Women Focus - Women currently comprise over 50% of the US population and control/influence over 85% of consumer spending . By successfully focusing on this segment, Aritzia is positioned for above-average growth.

- Fast Fashion - Fast fashion has materially impacted mid-sized brands, as consumers (influenced by social media) have flocked to converging styles offered by FF brands, which usually "follow" the designs of luxury fashion houses. Brands such as Aritzia have struggled with justifying their value proposition when consumers can find comparable designs at a significantly lower price. Globalization has accelerated this due to the ability to easily produce and export low-cost/quality products from the Far East.

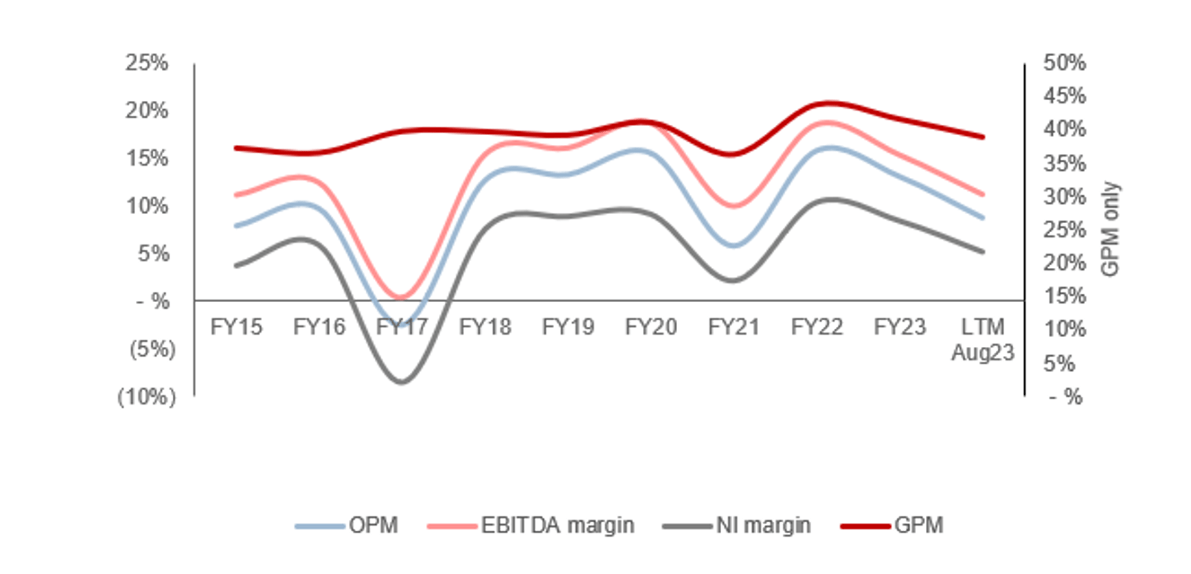

Margins

{kind=link}

Aritzia's margins have been incredibly volatile during the historical period, broadly moving cyclically with market demand. Its average level has been attractive, reflecting its vertical integration and brand-building exercise. This allows the business to minimize costs while charging an elevated price for its products.

Our view is that margins will continue to move in line with revenue growth, as Aritzia has not shown an ability to achieve a flexible cost base. This is not a surprising fact as in the luxury segment, the willingness of consumers to pay the full price or wait for a discount will materially impact margins beyond any other factor.

Quarterly results

Aritzia's recent financial performance has slowed, although remains better than many would expect. In its last four quarters, the company has achieved top-line growth of +37.8%, +43.5%, +13.4%, and +1.6%. In conjunction with this, margins have slipped in the LTM period, particularly in the last two months.

The growth achieved is impressive, although is a reflection of a significant investment in expanding the company's operations. On a comparable basis, revenue growth was negative in the last quarter. This is due to current macroeconomic conditions. With high inflation and elevated interest rates, consumers are feeling a squeeze on finances, even those in higher income brackets (although to a lesser extent), contributing to softening spending. Aritzia's ability to offset this for so long has been impressive, as even up until Q1'24, its organic growth was LSDs.

Our expectation is for current conditions to remain in the coming 2-3 quarters, as Central Banks remain focused on controlling inflation. This likely means the "bottom" has yet to be reached. We are currently of the view that expansionary policy could return in mid-to-late 2024, suggesting late 2024 (Q3/Q4) will be the bottom.

Key takeaways from the company's most recent quarterly results are:

- Interestingly, Management is of the belief its revenue slowdown in the last two quarters is materially impacted by missed opportunities in the level of new styles in its product assortment. We do think its organic trajectory is good and so this implies even greater resilience was possible.

- Despite the change in trajectory, the performance was better than anticipated. Management is focused on achieving operational progress toward its strategic priorities (focus on scalability in the medium term). The company has opened a new Toronto area distribution center and has meaningfully improved its inventory levels.

- Feedback suggests its new designs for FW are resonating well with its clients and should position it well for SS24, which it is now turning focus on.

- The boutique expansion is continuing to perform better-than-expected, which implies the company can enter a period of significant square footage expansion. Management is cognizant of this, although does not want to turn focus too far away from e-commerce.

Overall, the impact of the current economic conditions is unavoidable and is slowly being felt by Aritzia. Importantly, we think the company is taking the right steps to position itself for future growth and is laying the foundations for a growth push once demand conditions improve.

Balance Sheet & Cash Flows

Aritzia's balance sheet is relatively clean, with moderate debt usage. At a ND/EBITDA ratio of 2.3x, we do not see any solvency concerns, although the scope for raising further will be dependent on whether margins can sufficiently improve.

A key concern for us is that inventory turnover continues to decline (falling to 2.9x). Although Management has stated it is making good progress in reducing inventory, we believe there is evidence of serious near-term concerns. With GPM falling by 3% in the LTM period and 5% from FY22, discounting is clearly on the rise and likely at the highest extent possible given that EBITDA-M is significantly below FY23. This means selling inventory is a major concern as minimal progress has been made. The choice is either to forgo margins further or very slowly lift inventory turnover by remaining strict with discounting. The latter would normally be a moderate compromise but FCF margin is negative currently (-1%), which means the business may need to utilize short-term financing (as it already has in the LTM). Essentially, Aritzia has found itself in a short-term cash squeeze that will not materially damage the company but is an unneeded mistake. This is highly disappointing and illustrates naivety.

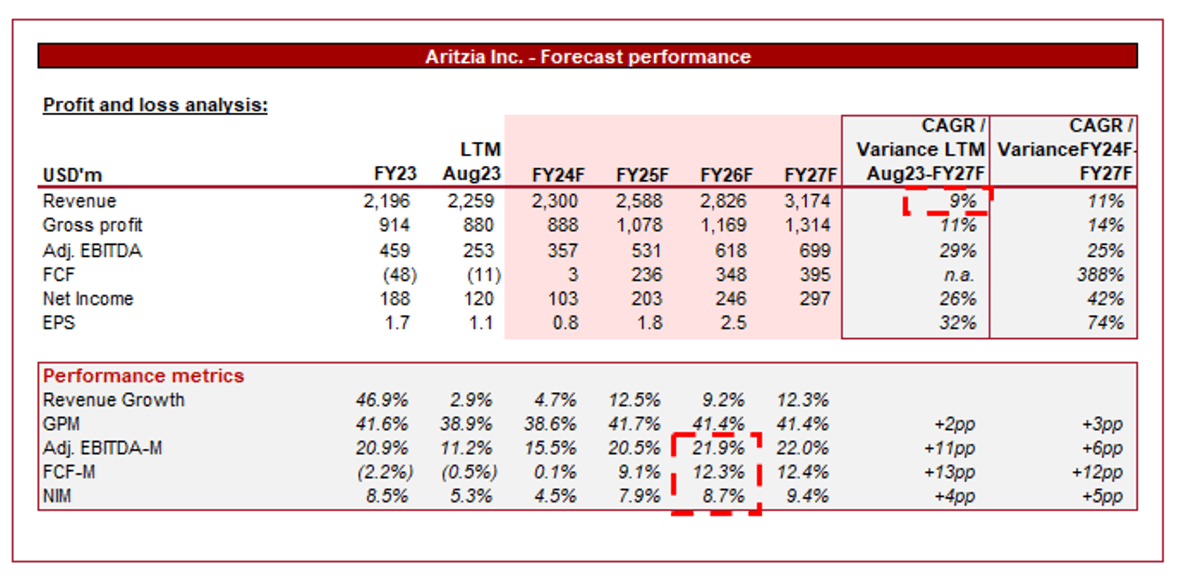

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 4 years.

Analysts are forecasting a natural reduction in its growth rate, although the level remains strong at 9%. In conjunction with this, margins are expected to broadly remain in line with its FY23 level. These forecasts are materially below Management's long-term guidance, as they expect a resurgence in growth to what has been achieved historically, alongside margin improvement.

We believe analysts are likely conservative, but broadly correct, with their growth forecast. Store growth and further e-commerce expansion will likely contribute to HSD growth, particularly due to clear brand strength. Consumers are resonating with its designs well, suggesting a good competitive position. Further, we think its long-term average margins will likely land at the levels analysts are suggesting, although remain highly uncertain. The key for Management is to achieve operating cost leverage and better inventory control, while it will be incredibly difficult to offset the cyclical nature of the industry.

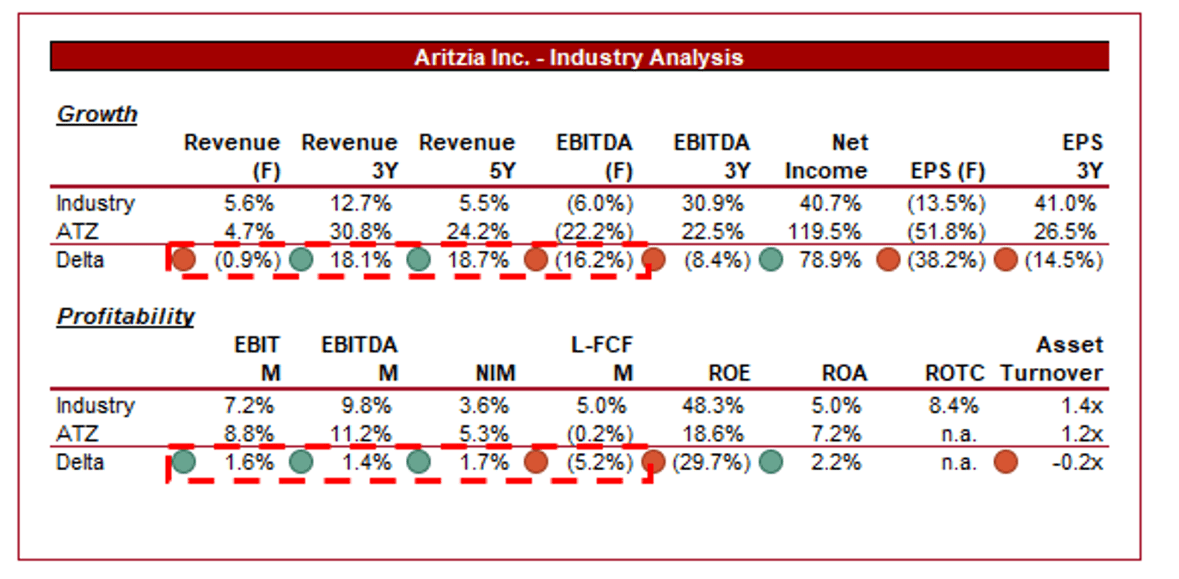

Industry analysis

Apparel Retail Stocks (Aritzia)

{kind=link}

Presented above is a comparison of Aritzia's growth and profitability to the average of the Apparel industry, as defined by Seeking Alpha (29 companies).

Aritzia performs reasonably well relative to its peers. The company has achieved outsized revenue growth in both a 3Y and 5Y period, reflecting its impressive expansion strategy. Its designs are resonating well with consumers and have allowed the business to successfully generate strong returns from its new locations and e-commerce strategy. This said, its growth in profitability metrics is less compelling, illustrating significant volatility far beyond the wider industry.

Further, Aritzia is more profitable than the peer group, which we attribute to its vertically integrated strategy. Given its scale, the scope for further improvement is there, although we are unconvinced by the ability to offset cyclicality.

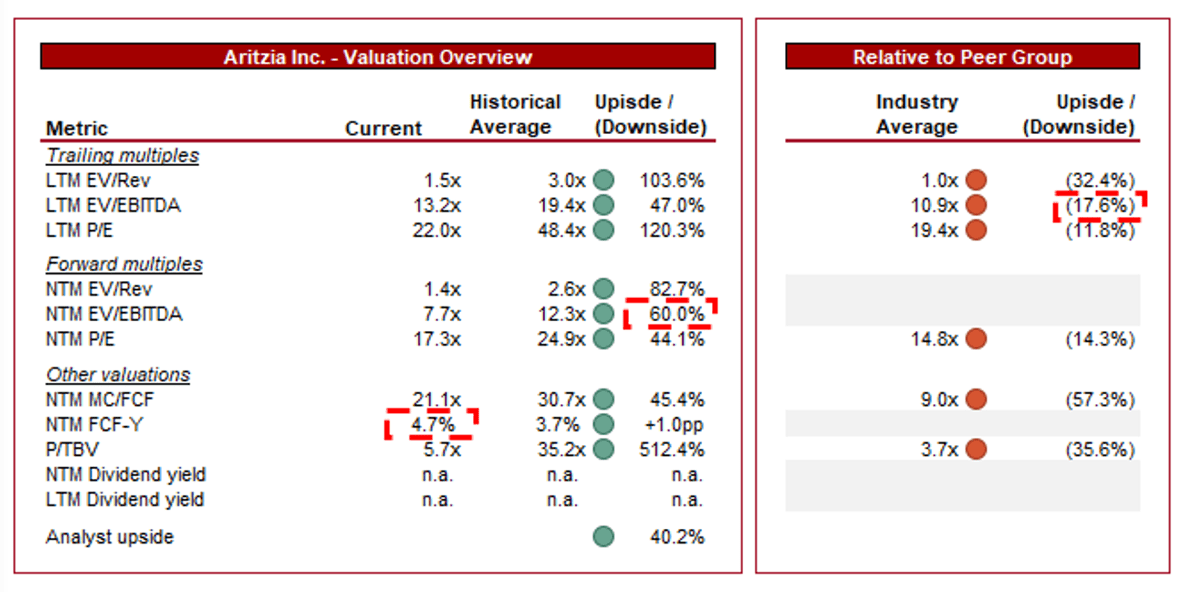

Valuation

{kind=link}

Aritzia is currently trading at 13x LTM EBITDA and 8x NTM EBITDA. This is a discount to its (short) historical average, reflecting its share price decline.

Aritzia is trading at an 18% discount on a LTM EBITDA basis and a 14% on a NTM P/E basis to its peers. This is despite the company's strong financial performance, suggesting investor hesitancy. We believe this is a reflection of the competitive nature of the industry, contributing to investor concerns about the longevity of Aritzia's brand. As we have discussed, the fashion industry is notoriously incredibly competitive and so its future trajectory is inherently highly uncertain. Unlike retailers and brand consolidators, Aritzia is reliant on a handful of small brands, none of which are "mainstream". Management is seeking to differentiate with its acquisition of Reigning Champ but this again has an uncertain impact on the wider business.

From everything we have seen, we do believe Aritzia can continue its current growth trajectory into the medium term, primarily due to its increased social media efforts and brand development thus far. This suggests the stock is undervalued at today's price. Analysts concur with this view, suggesting an upside of 40%.

Key risks with our thesis

The risks to our current thesis are:

- Economic downturns impacting consumer spending - The timing of economic recovery will materially impact Aritzia's return to strong growth.

- Failure to adapt to changing fashion preferences - A decline in the Interest of a brand in many cases can be out of the control of Management, but what can be controlled is creating compelling designs.

Final thoughts

Aritzia has done a fantastic job of developing a strong market presence in Canada, despite the high level of competition that has only increased through globalization. More broadly, there is a lot to like about how the company operates, with a design-driven approach, vertical integration, and reasonably good financials.

We believe it can continue its upward trajectory, as new locations are opened and its social media penetration improves. This said, the near-term appears concerning from a financial perspective, as demand slows and inventory accumulates. We do not believe, regardless of valuation, this is a good investment until these pressures are alleviated.

For further details see:

Aritzia: Potential Path To Global Fashion Dominance