NVDA - Arm Holdings: Priced For Perfection

2023-12-12 04:30:54 ET

Summary

- Arm Holdings is a dominant player in mobile application processors and is growing rapidly in cloud computing and IoT markets.

- Some licensees are designing CPUs to compete with Intel in the PC market, which could lead to significant growth in royalties for ARM.

- The company's rich valuation, high price-to-free-cash-flow ratio, and headwinds in the semiconductor industry pose risks for investors.

We will not deny that Arm Holdings ( ARM ) is an attractive business, with several tailwinds in its favor, including investors' current favorite "Artificial Intelligence" exposure, and as the company likes to remind its investors, Arm is the world’s most pervasive CPU architecture. These are some of the reasons that motivated SoftBank Group ( OTCPK:SFTBY ) to purchase ARM in 2016 for about $32 billion. SoftBank paid a high valuation, despite the uncertainty resulting from Brexit and ARM being a UK-based company.

Since then, the company has certainly diversified its end markets, with mobile going from close to two-thirds to less than half of its revenues.

Arm Holdings Investor Presentation

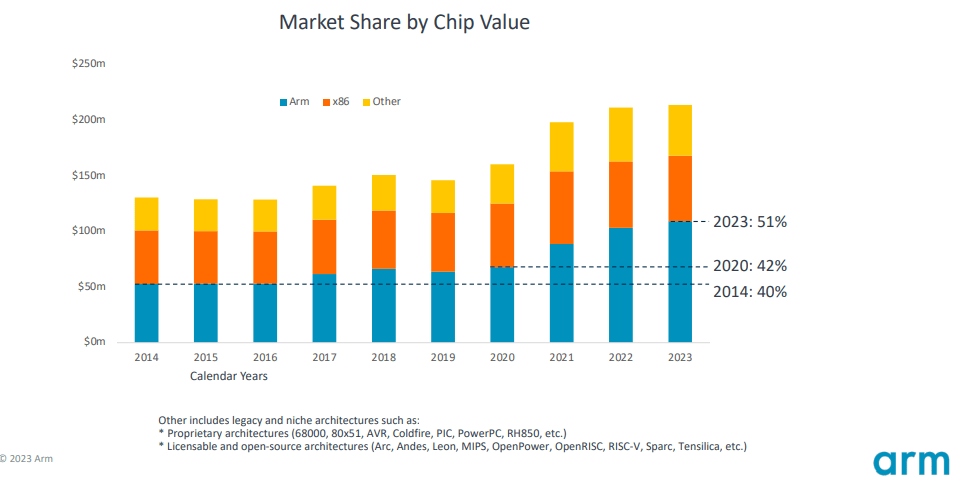

The power efficiency of its designs and vast software ecosystem has allowed the company to dominate in mobile application processors, where Arm's share is more than 99%, and Arm's value has been increasing in the new smartphone generation. Arm is also quickly growing in cloud computing, which is currently Arm’s fastest-growing market. Last quarter, Arm reported that its market share was around 10% and growing quickly. Another successful end-market has been IoT and embedded devices, where the company has approximately a 65% market share. All of these have led to ARM capturing a higher share of the market as measured by chip value.

{kind=link}

Things could get even better for the company, as some of its licensees are working to compete with Intel Corporation ( INTC ) using ARM technology to make processors for Microsoft ( MSFT ) Windows PCs. According to news reported by Reuters, NVIDIA ( NVDA ) and AMD ( AMD ) are designing CPUs to compete with Intel in the PC market.

Nvidia has quietly begun designing central processing units (CPUs) that would run Microsoft’s Windows operating system and use technology from Arm Holdings, two people familiar with the matter told Reuters.

This is obviously good news for ARM, as it could mean significant growth in royalties if its licensees are successful in competing for a share of this market. Apparently, Microsoft is encouraging them after seeing Apple ( AAPL ) increase its market share, in part thanks to its own in-house designed Arm-based chips which tend to be more power efficient.

IPOs Tend to Be Overpriced

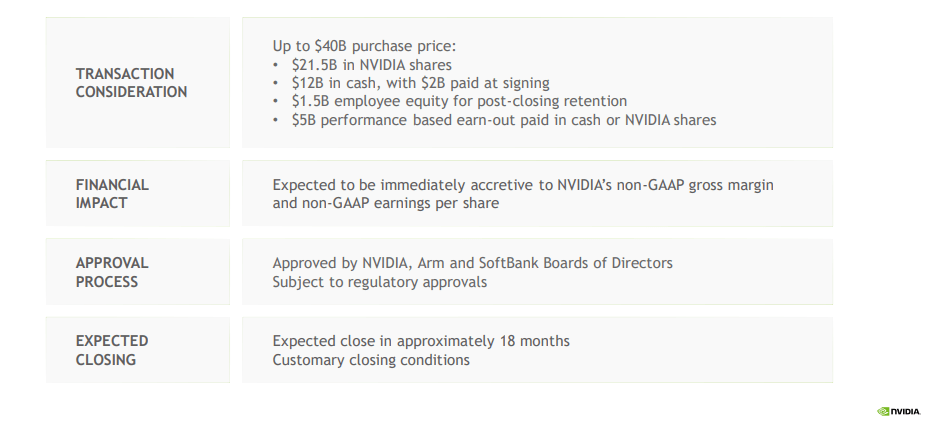

The big problem we have with the idea of investing in ARM Holdings is the rich valuation. It is important to remind readers that previous owners have a high motivation to time an IPO when it is likely to generate the most excitement and demand from investors. This tends to inflate valuations, making it hard for investors purchasing shares shortly after the IPO to beat the market. ARM is currently valued with a market cap of roughly $69 billion, and an enterprise value of close to $67 billion. This is more than twice what SoftBank paid for the company in 2016, and almost 75% higher than what NVIDIA offered for it in 2020.

In the last ten years, the Renaissance IPO ETF has underperformed most indices, including the S&P 500 index ( SPY ), the Dow Jones Industrial Average ( DIA ), and popular technology ETFs like the Invesco QQQ ETF ( QQQ ) and the Vanguard Information Technology Index Fund ETF Shares ( VGT ). We think this graph should give investors pause before they buy into the hype surrounding an IPO.

Financials

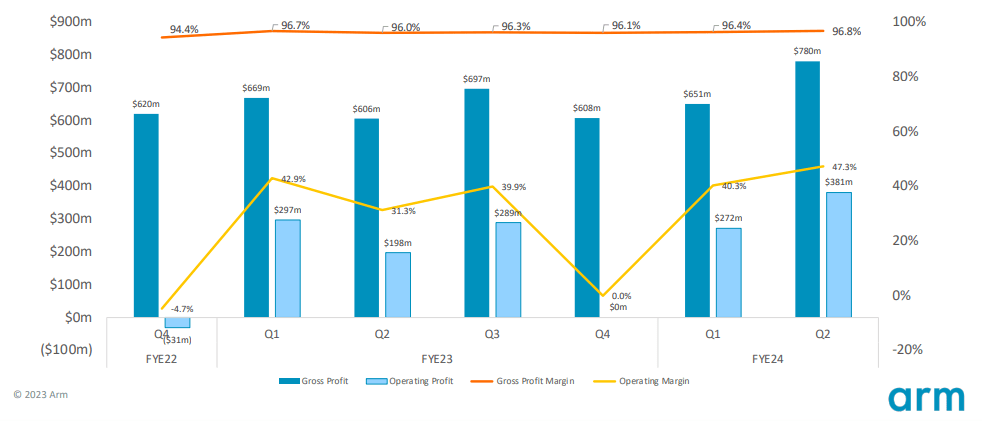

As previously mentioned, we are not debating that ARM is a very high-quality company. There are very few businesses that have significant revenue growth, gross profit margins of ~95%, and operating margins around 40%.

{kind=link}

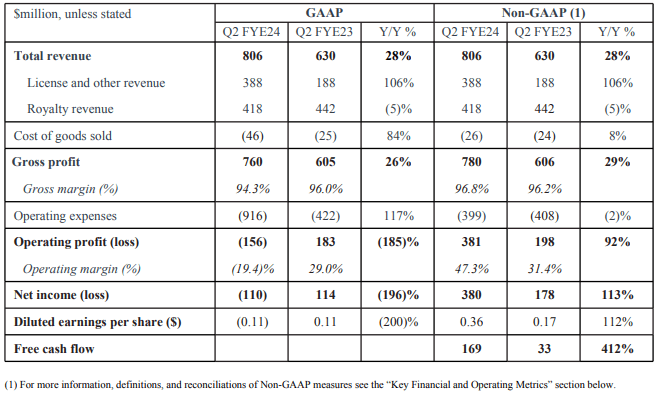

Still, when looking more closely things are a little bit less rosy. For one thing, the company actually reported a GAAP loss last quarter. In any case, we are more interested in the free cash flow the company was able to generate in the quarter, which was $169 million. If we annualize this number, it comes to $676 million. With a market cap of $69 billion, this puts the price/free cash flow at roughly 102x. Investors obviously have tremendous growth expectations baked into the current price.

{kind=link}

Current Headwinds

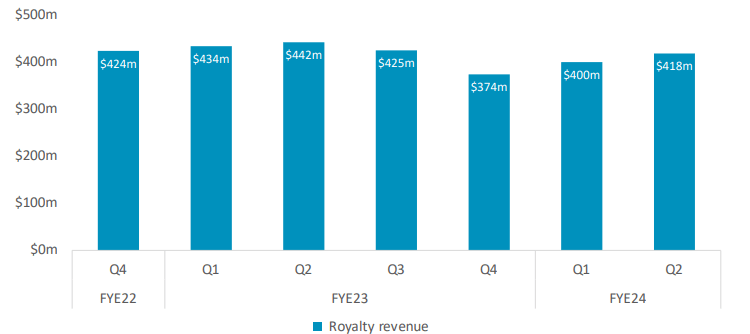

To make things worse for investors, the semiconductor industry is facing some headwinds, with chips shipped reportedly down ~6% year over year, mainly due to weakness in the smartphone and IoT segments. Despite many promising new applications and the AI tailwind, we are not seeing much growth in Arm's royalty revenue either.

{kind=link}

Relative Price to NVIDIA's Offer

What really has us scratching our heads is why investors are willing to pay almost 75% more than NVIDIA was offering in 2020. It is actually ~2x the price NVIDIA was offering if we remove the $5 billion which was a performance-based earn-out. In addition, NVIDIA could get the benefit of some cost and revenue synergies from the acquisition.

The acquisition did not take place because of regulatory opposition, with some ARM customers also voicing concerns. We believe the biggest change since then has been the new obsession many investors currently have with gaining AI exposure.

{kind=link}

High Licensee Churn

We think the growth investors are expecting will be difficult to achieve, especially with the company increasing the number of licensees at what we would describe as a relatively disappointing rate. At least when talking about the net numbers, it seems the company has been able to sign a reasonable number of new customers, yet the net number barely increases.

For example, its Arm Flexible Access program saw a net increase of just one customer, despite the company claiming more than 40 renewals and more than 18 new agreements signed, including companies developing a wide range of AI-related applications. If the company is signing a significant number of new customers, yet the net number barely increases, then the logical conclusion is that churn is relatively elevated.

Outlook

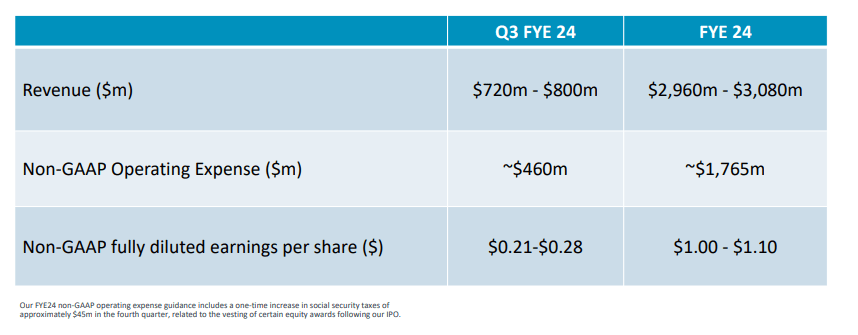

Arm already disappointed investors last quarter as the smartphone weakness continues, resulting in guidance below expectations. Management guided for revenue between $720 million and $800 million, compared to consensus expectations of $780 million. Additionally, they projected $0.21 to $0.28 in adjusted earnings per share.

More importantly, in our opinion, revenue is likely to be around $3 billion for FY2024, putting the forward P/S multiple at a jaw-dropping 23x.

{kind=link}

Valuation

The company is currently trading with a market cap of close to $69 billion, and thanks to its net cash position the enterprise value is lower at roughly $67 billion. Still, we don't believe its valuation multiples are justified even with the AI hype. The company was telling investors during its roadshow that thanks to the AI tailwind it expected to reach revenue growth in the mid-20% range in fiscal 2025.

We are not the only ones questioning the valuation, several Seeking Alpha authors agree it is extremely stretched. Even Bloomberg has written that much of Arm's valuation relies on AI Hype. Morningstar ( MORN ) has also warned investors that they estimate the intrinsic value to be around $34 per share. Even compared to the "magnificent seven", many of which are also expected to benefit from AI, ARM is trading higher than almost all based on their forward P/E ratios, the only exception being Tesla ( TSLA ).

Risks

While we believe the biggest risk for investors buying Arm shares is the extremely high valuation, there are other risks they should also consider. One is that a lot of talent has left the company, with the company reportedly losing significant staff in the UK.

The company has also had a lot of issues with its China operations. In fact, Bloomberg found around 3,500 words detailing the company's risks in China in its IPO filing.

Conclusion

Arm is clearly a high-quality technology business with many attractive characteristics such as high margins, a recurring revenue business model, and the potential for above-average revenue growth. Its royalty revenue can continue for many decades, with the company sharing that it is still collecting royalties on products developed in the early 1990’s. Despite all these positive attributes, we find the shares extremely expensive and do not believe the expected revenue growth is high enough to justify the extreme valuation multiples. This is why we are rating the company a "Strong Sell", and would only consider investing at a much lower valuation.

For further details see:

Arm Holdings: Priced For Perfection