LOW - Armstrong World Industries: Highly Profitable Opportunity To Buy Now

Summary

- Net sales growth is slowing down due to lower consumer demand, but fundamentals remain strong.

- Long-term debt has been steadily declining despite recent acquisitions.

- Armstrong World Industries is an aggressive share buy-backer.

- AWI stock is highly profitable despite recent headwinds, and the dividend is safe.

- The recent share price decline represents a good opportunity for long-term dividend growth investors.

Investment thesis

Armstrong World Industries ( AWI ) is a company with a very long history behind it, and nothing indicates that this will stop being the case in the long term. The company's operations are highly profitable and its net sales have been increasing sustainably for the past few years, which makes the dividend and interest expenses sustainable. Furthermore, the company makes regular share buybacks, which increases the position of shareholders passively over time.

Still, the company is currently facing some headwinds that mainly include inflationary pressures and lower consumer demand. Furthermore, increasing interest rates are increasing the risk of recession in the US economy, which is generating uncertainty among shareholders, leading the price to fall by ~34% from all-time highs. But despite this, a strong balance sheet suggests that the company has enough room to maneuver to overcome such headwinds, so I think the current decline in the share price actually presents a good opportunity to obtain a decent dividend yield on cost for shareholders with a long-term time horizon.

A brief overview of the company

American Woodmark Industries is a leading designer, innovator, and manufacturer of ceiling and wall solutions in the Americas, and its products include mineral fiber, fiberglass wool, metal, wood, wood fiber, glass-reinforced gypsum, and felt. The company was founded in 1860, and its market cap currently stands at ~$3.6 billion, employing around 3,000 workers. It works with major customers such as Lowe's Companies ( LOW ) and The Home Depot ( HD ), as well as other direct customers and retailers.

Armstrong World Industries logo (Armstrongceilings.com)

The company's operations are mainly divided into two segments: Mineral Fiber, which generated 72% of the company's total net sales in 2022, and Architectural Specialties, which generated the rest. Under the Mineral Fiber segment, the company manufactures suspended mineral fiber and soft fiber ceiling systems, and under the Architectural Specialties segment, it manufactures and provides ceilings and walls made from metal, felt, and wood, for use in commercial settings. Nevertheless, around 70% of net sales are generated through distributors.

In March 2022, the company announced its Five-Year growth targets, which include revenue growth rates ranging from 10% to 13%, adjusted EBITDA growth rates ranging from 12% to 15%, adjusted diluted EPS ranging from 15% to 20%, adjusted free cash flow rates of 15% to 20% (Non-GAAP), but slowing demand, especially during the second half of 2022, are casting doubt on the feasibility of such projections.

Currently, shares are trading at $76.99, which represents a 33.74% decline from all-time highs of $116.20 on December 08, 2021. Lower-than-expected volumes in 2022, increasing input costs, and macroeconomic uncertainties due to rising interest rates by central banks in order to reduce inflation derived from the end of the worst periods of the coronavirus pandemic and the current war between Russia and Ukraine, are worsening the company's outlook in the short-to-medium term, but they are also, in my opinion, opening up the opportunity for dividend investors interested in acquiring shares at a reasonable price. But in order to understand the path that the company has been taking so far, it is very important to review the latest acquisitions and divestitures that have taken place.

Recent acquisitions and divestitures

In order to achieve sustainable growth, the management follows a quite conservative M&A strategy as its debt levels have been reduced despite the latest acquisitions.

In May 2018, the company acquired Plasterform, a 31-year Canadian manufacturer of ultra-expressive, durable, custom architectural cast ceilings, walls, facades, columns, and moldings, with annual revenues of around $10 million coming from operations in Canada, the United States, and Latin America. Later, in July 2018, it also acquired Steel Ceilings, a manufacturer of standard and custom aluminum and stainless metal ceilings, including architectural, radiant heating and cooling, and security solutions, with revenues of around $10 million per year.

In March 2019, the company acquired Architectural Components Group, a manufacturer of specialty custom wood ceilings and walls generating around $35 million in net sales per year, but in September 2019, it divested its WAVE joint venture in EMEA and the Pacific Rim, as well as Armstrong France and WAVE France, for ~$330 million. Nevertheless, in November 2019, the company acquired MRK Industries, a manufacturer of specialty metal ceiling, wall, and exterior solutions that generates annual net sales of around $14 million, with the aim of further penetrating the architectural specialties segment.

In July 2020, the company acquired TURF Design, a designer and manufacturer of acoustic felt ceilings and wall products that generates around $25 million in annual net sales. In August 2020, it also acquired Moz Designs, a California-based designer and manufacturer of custom architectural metal ceilings, walls, dividers, and column covers for interior and exterior applications that operates a 100% solar-powered, 30,000 sq. ft. facility, generating around $10 million in annual net sales. And finally, in December 2020, the company acquired Arktura, a California-based designer and manufacturer of ceilings, walls, partitions, and facades that generates around $40 million in net sales per year. This latest acquisition took place a month after the company acquired GC Products, a designer and manufacturer of glass-reinforced gypsum, glass-reinforced cement, molded ceiling, and specialty wall products.

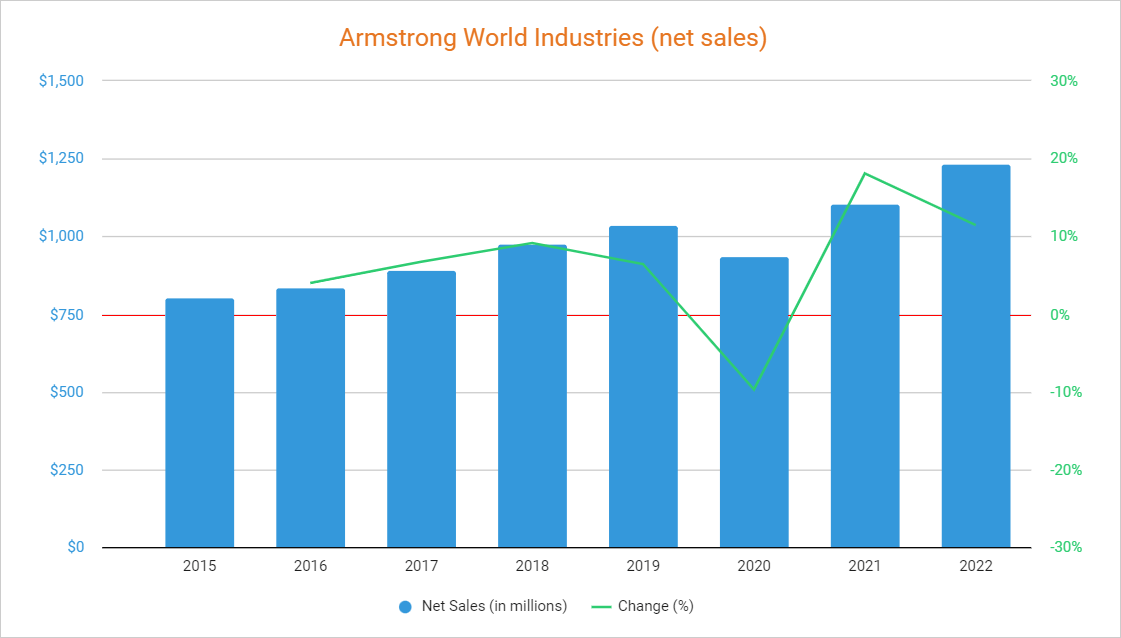

Net sales are expected to keep increasing

Thanks to recent acquisitions, as well as new product launches, the company has achieved very acceptable net sales growth rates in the past few years (except for 2020, the year of the outbreak of the coronavirus pandemic). In 2021, after the lift of mandatory restrictions around the United States and Canada, net sales recovered as they increased by 18.11% year over year (and by 6.60% compared to 2019). 2022 was also a good year as net sales increased by 11.43% year over year to $1.23 billion.

{kind=link}

And as for the last quarter of 2022, net sales increased by 7.79% year over year, but declined by 6.31% quarter over quarter, showing lower consumer demand. Nevertheless, net sales are expected to increase by 4% in 2023 to $1.28 billion, and by over 4.5% in 2024 to $1.34 billion, although such projections should not be taken for granted due to the current economic uncertainty.

In order not to rely solely on acquisitions for growth, the company periodically launches new products. In June 2018, it launched DESIGNFlex Ceiling Systems, which enables architects and designers to reinvent their ceilings by mixing and matching different panel shapes, sizes, colors, and textures in minimum orders as small as one carton that can be ready for shipment to the job site in only three weeks. Later, in June 2019, the company launched its ACOUSTIBuilt Seamless Acoustical Ceilings, a ceiling system that provides the look of drywall but performs like an acoustical ceiling.

In October 2020, the company launched its 24/7 Defend product portfolio, which offers affordable solutions that contribute to healthier, safer spaces, as well as cleaner air. And finally, in July 2022, the company announced a partnership with Price Industries to accelerate the development of holistic solutions to promote healthy indoor spaces and launched StrataCleanIQ, a ceiling-mounted filtration unit using MERV 13 filtration.

Furthermore, more recently, the company was just awarded the new terminal at the Pittsburgh airport, which should enable a net sales boost in the foreseeable future. But despite the increase in net sales due to these efforts and recent acquisitions, the recent decline in the share price has caused a relatively sharp decline in the P/S ratio, which currently stands at 2.896.

This means the company generates net sales of $0.35 for each dollar held in shares by investors, annually. This ratio is 9.58% lower than the average of 3.203 of the past decade, and a 48.75% decline from the peak of 5.651 reached at the beginning of 2018, which means investors are placing less value on the company's sales as margins (especially EBITDA margins) are showing signs of weakening and the American economy is entering in an uncertain territory due to interest rate hikes.

The company is highly profitable

The company has achieved double-digit year-over-year sales growth in the specialty segment for nine consecutive quarters, which has enabled healthy gross profit and EBITDA margins despite macroeconomic inflationary pressures. Strong pricing power and productivity initiatives have also made it possible for the company to remain highly profitable. In this sense, the trailing twelve months' gross profit margin currently stands at 36.42% while the EBITDA margin stands at 29.88%, which shows a very strong capacity to convert sales into actual cash.

Certainly, 2022 was overall a good year regarding profit margins, which were slightly impacted by lower-than-expected volumes in the Mineral Fiber segment due to inventory corrections and lower consumer demand, which is partially a consequence of a decline of back-to-office momentum. Also, Iron Ore prices, which are used for the manufacturing process of steel, are rising again, which is set to cause an increase in the cost of goods sold.

{kind=link}

But despite this, the gross profit margin remained very robust during the past quarter at 26.62% and the EBITDA margin at 30.44%. In this sense, the EBITDA increased by around 4% year over year during 2022 thanks to improvements in productivity in the company's mineral fiber plants and strong AUV growth in Mineral Fiber, strong Architectural Specialty sales, and earnings growth.

Debt keeps declining as the balance sheet gets stronger

Over the past 10 years, the company has managed to steadily reduce its debt load. In this sense, the company's long-term debt currently stands at $651.10 million while it holds $106 million of cash and equivalents. While it is true that net debt remained stable since the beginning of 2020, the company has acquired TURF Design, Moz Designs, Arktura, and GC Products during the period while paying out dividends and carrying out share buybacks, and therefore, the company's ability to reduce debt is not currently in question.

But what is more, apart from declining long-term debt and stable cash and equivalents of around $100 million, the company has also built up an inventory of $110 million from $60 million 5 years ago.

This means that the company has some resources to convert into cash, which may provide some room for maneuvering in the face of current inflationary pressures, lower demand, and economic uncertainty. But to delve even deeper into the company's ability to reduce (or manage) its current level of debt, it is very important to go deeper into its current cash payout ratio.

The dividend is safe as the cash payout ratio is low

In November 2018, the company announced the initiation of a quarterly dividend of $0.175 per share and, since then, it has increased its quarterly payout to $0.254 per share, which represents a 45.15% increase in the whole period.

But despite these raises and the recent decline in the share price, the dividend yield is low at 1.26% due to the fact that the management makes conservative use of its cash from operations in order to make room for share buybacks and further acquisitions. It should be said that said dividend yield is in the all-time highs range.

In the table below, I have calculated the dividend cash payout ratio by calculating what percentage of the cash from operations has been used each year for the payment of the dividend and interest expenses. In this way, we can find out the sustainability of the dividend through actual operations.

| Year |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| $203.2 |

| $182.7 |

| $218.8 |

| $187.2 |

| $182.4 |

| Dividends paid (in millions) |

| $8.6 |

| $35.6 |

| $39.2 |

| $41.4 |

| $44.2 |

| Interest expenses (in millions) |

| $39.2 |

| $38.4 |

| $24.1 |

| $22.9 |

| $27.1 |

| Cash payout ratio |

| 23.52% |

| 40.50% |

| 28.93% |

| 34.35% |

| 39.09% |

As we can see in the table, the company has managed to cover its dividend and interest expenses with less than 50% of the cash generated through its operations over the past five years, which suggests that the dividend is sustainable in the long term. As for the past quarter, cash from operations was strong at $63.2 million, but it's important to note that accounts receivable decreased by $6 million and inventories by $5.1 million while accounts payable only declined by $1.6 million. But even if we add annual capital expenditures of ~$75 million, the company's remaining cash from operations of $111.1 million in 2022 after covering the dividend and interest expenses is more than enough.

Thanks to this, the company has enjoyed excess cash that has allowed it, in addition to gradually reducing its level of debt and making acquisitions, to carry out share buybacks in order to passively increase the position of shareholders.

Share buybacks gradually increase investors' positions

During the past decade, the company has managed to reduce the number of outstanding shares by 23% to 45.44 million and, in the present, this reduction is a tradition that continues in force. This means that each share of the stock represents an ever-growing portion of the company, increasing thus per-share metrics.

In this regard, in August 2018, the company announced a share repurchase program of $150 million after the previously announced expansion of its share repurchase authorization from $400 million to $700 million. The share repurchase program was funded by the sale of certain subsidiaries comprising its businesses in Europe, the Middle East and Africa (including Russia), and the Pacific. This share repurchase program expired in October 2020, but the share buyback tradition has so far continued in 2021 and 2022.

Risks worth mentioning

Despite a strong balance sheet, high profitability, and what I consider a safe dividend, there are still some risks involved in investing in Armstrong World Industries that I would like to highlight.

- Around 92% of net sales generated in 2022 took place within the United States, which means that the company's operations depend mainly on the performance of the US economy as they lack sufficient geographic diversification.

- Rising interest rates in 2023 focused on reducing high inflation rates to more stable levels are creating an uncertain macroeconomic context, in which demand could be reduced even more due to recessionary risks.

- The company's cash generation capacity could be strongly affected if current headwinds intensify or recessionary risks materialize. Luckily, the company has a very sustainable level of debt, a share buyback tradition that it can pause, and a dividend that can be cut if necessary until headwinds are a thing of the past.

- A cut in the dividend or in buyback efforts would imply a lower return for shareholders and could, with great probability, have a great (negative) repercussion on the share price despite being measures focused on correctly maintaining the health of the company in the long term.

Conclusion

Despite the ~34% drop in the share price, I believe the company's fundamentals remain largely intact. Both gross profit and EBITDA margins remain at very high levels, which means that the company is highly profitable. Furthermore, the current level of debt and the dividend are sustainable at present. So far, the acquisition of companies that operate in the specialty segment has allowed the maintenance of very healthy profit margins despite the current complex macroeconomic context marked by strong inflationary pressures and lower consumer demand, but it is very important to keep in mind that these headwinds could intensify and that interest rate hikes could lead the US economy into a recession, so it is important to invest cautiously.

In this sense, although I believe that a dividend yield on cost of 1.26% is quite reasonable due to a low cash payout ratio, steady growth, and aggressive share buybacks, I think it would be a good idea to save an extra bullet in case the stock price falls further due to the risks I mentioned earlier in this article.

For further details see:

Armstrong World Industries: Highly Profitable, Opportunity To Buy Now