AQST - ARS Pharmaceuticals Vs. Aquestive Therapeutics; Neffy CRL Creates An Opportunity For Investing In Both

2023-09-22 19:18:44 ET

Summary

- Both ARS Pharmaceuticals and Aquestive Therapeutics are developing non-injectable epinephrine products for anaphylaxis, with potential to capture significant market share from current standard (auto-injectors).

- At current prices I expect that upside of either stock if successful will significantly outweight downside risk for the other stock, while upside potential from both stocks is not unlikely.

- Risks include regulatory delays (unlikely for SPRY but possible for AQST), several competing nasal epinephrine devices under clinical development (a major risk to SPRY) and precarious financial situation of AQST.

Thesis overview

Both ARS pharmaceuticals ( SPRY ) and Aquestive Therapeutics ( AQST ) are developing non-injectable epinephrine products for anaphylaxis, aiming to fill a significant unmet need considering limitations of current standard-of-care (epinephrine auto-injectors). SPRY is developing neffy , an epinephrine nasal spray, while AQST is developing Anaphylm , an epinephrine sublingual film. Both products could capture significant market share from epinephrine auto-injectors.

SPRY recently received an unexpected Complete Response Letter ((CRL)) by FDA requesting more pharmacokinetic data, despite prior positive AdCom vote and prior agreement to conduct such a study post-marketing. This caused a major dip in SPRY's stock price even though SPRY remains well-capitalized to withstand the delay. In my opinion, there should be no more regulatory surprises / delays for SPRY and neffy should be able to reach commercialization by 2H 2024 according to SPRY's estimation. The major risk to SPRY is competition by AQST, as well as other biotechs developing nasal epinephrine sprays. AQST is aiming for NDA submission by the end of 2024 and commercial launch in 2025. Therefore, the regulatory delay for neffy reduces the head start of SPRY over AQST and other competitors. On the other hand, in my opinion there is a good chance of regulatory delays for AQST (and other competitors) as well, and approval pathway for AQST may not be as risk free as someone would assume (discussed below).

Investing in both the stocks right now seems to be a reduced risk approach as I expect at least 1 of the 2 companies to be successful. At current stock prices the upside should be >100% for either SPRY or AQST within a 1-2 year time frame. Therefore, success of either company should outweigh downside risk if invested in both. Best case scenario there is upside potential for both stocks. A risk to this approach is that both companies fail due to regulatory delays or emerging competition (the latter prompting me to give a "Hold" rather than "Buy" rating to the proposed strategy to highlight the risk by competition). Of note, I invested in SPRY the day after the CRL at about $2.8. However, while preparing this article SRPY's stock price has already spiked significantly from the dip (up to +40% within 2 days) which increases the risk of the strategy by reducing SPRY's upside potential (the impact will depend on future potential peak price, the higher the price the lower the impact of the current spike). It may be preferrable to wait for SPRY's price to fall again before applying the above strategy although there is a risk it might never fall.

Implications of CRL for SPRY

On May SPRY announced favorable AdCom vote supporting approval of neffy based on available data in adults (16:6 in favor) and in children <18 years of age and ?30 kg (17:5 in favor). Subsequently, according to SPRY "FDA and ARS Pharma previously aligned in August 2023 on final physician’s labeling and a post-marketing requirement to conduct this study as informative for labeling".

Unexpectedly, SPRY announced receipt of a CRL by FDA requesting that a repeat-dose study under allergen-induced allergic rhinitis conditions be completed prior to neffy approval as opposed to previously agreed-upon post-marketing requirement. SPRY plans to appeal the issuance of this CRL. Regardless, SPRY anticipates a resubmission to the FDA in the first half of 2024 and an FDA action date in 2H 2024. SPRY anticipates cash, cash equivalents and short-term investments of about $195 million at the time of anticipated launch.

In my opinion, the CRL simply delays approval and I don't expect additional regulatory surprises. SPRY is very well-capitalized to withstand the delay without needing to raise cash. Furthermore, if all goes according to plan neffy would still be launched earlier than Anaphylm. However, several other companies are developing nasal epinephrine devices; Bryn pharma, Hikma Pharmaceuticals ( HKMPY ), Nasus Pharma, Orexo (OXROY), Amphastar Pharmaceuticals (AMPH). Considering potential for regulatory approval based on just pk/pd studies the pathway for approval of competing products could be fast. Delay by neffy's CRL could allow competitors to reach the market faster or soon after neffy which could negatively affect the market share captured by neffy. Nevertheless, to my knowledge none of the competitors have filled an NDA yet, although Bryn for example is aiming for an NDA filling this year. Despite competition, I expect delays for competition and I expect that SPRY should still have a head start in commercialization and could capture a significant market share.

It is worth noting here that marketing authorization application for neffy is also under review by the European Medicines Agency with a decision expected by year end 2023. I expect a positive decision. Submissions to other regulatory authorities in additional countries are planned for 2024. SPRY plans to form partnerships for commercialization outside US (with partnerships already established for Japan and China).

Potential regulatory risks for AQST

The regulatory pathway for non-injectable options for anaphylaxis treatment is complicated. Anaphylaxis is a life-threatening condition and timely effective treatment can be life-saving. Ideally, a randomized controlled trial would be conducted to prove non-inferiority of non-injectable options compared to subcutaneous auto-injectors and/or intramuscular epinephrine. However, conducting such a randomized trial is impractical and most likely infeasible (or would take too long to enroll). Notably, there are no randomized controlled trials for current standard of care (epinephrine injection) as well, and there will never be such a randomized trial as it would be unethical to have a placebo arm. Even more impressive is the fact that majority of epinephrine auto-injectors were approved without even pk data .

Based on the above, the "bracketing approach" has been agreed to be sufficient for regulatory approval. This means that non-injectable options can be approvable as long as pharmacokinetics/pharmacodynamics (pk/pd) are comparable to current standard-of-care, which is injectable epinephrine. From a pk/pd perspective subcutaneous autoinjectors appear to be more efficacious compared to intramuscular epinephrine, both of which are considered acceptable treatment options, the latter being the typical choice in the in-hospital setting. Despite variations in pharmacokinetics between approved products, all considered to have similar efficacy. Therefore, for approval non-injectable candidates only need to achieve pk/pd targets in between autoinjectors and IM epinephrine (hence the "bracketing" term). The rationale, also discussed in the recent AdCom, is that achieving these pk/pd targets should translate to similar clinical efficacy.

Considering successfully meeting pk/pd targets there is no biological reason to suspect that SPRY's and AQST's products would not be as clinically efficacious as standard-of-care. However, one should consider FDA's difficult position. Approving a product for a life-threatening condition without a randomized trial proving non-inferiority compared to current standard-of-care is concerning. Notable, a major point in SPRY's AdCom was the unmet need for a non-injectable option. Assuming no more regulatory delays this unmet need will be filled by SPRY's neffy. Therefore, although unfair, FDA may no be as lenient in approving AQST's candidate. In the absence of an unmet need, FDA may not be willing to be exposed to the risk of approving another non-injectable product without a randomized trial comparing to alternative options. The outcome of a potential AdCom vote for AQST's product could thus be unpredictable. Furthermore, post-marketing reports of unsuccessful use of neffy, albeit unlikely, could have a significant impact of the regulatory process for AQST.

Evidence for neffy

SPRY has completed 3 registrational studies and has an ongoing study for pediatric patients (for a detail presentation of the evidence I refer readers to SPRY's AdCom presentation );

- EPI-15; single and repeat neffy administration by healthcare practitioners in healthy subjects

- EPI-16; neffy administration by healthcare practitioners during experimental allergen-induced rhinitis (important to confirm that pharmacokinetics are not adversely affected by edema during an allergy event)

- EPI-17; self-administration in patients with history of severe Type I allergies (important to assess that patients can correctly use the device)

- EPI-10 (ongoing); pediatric study

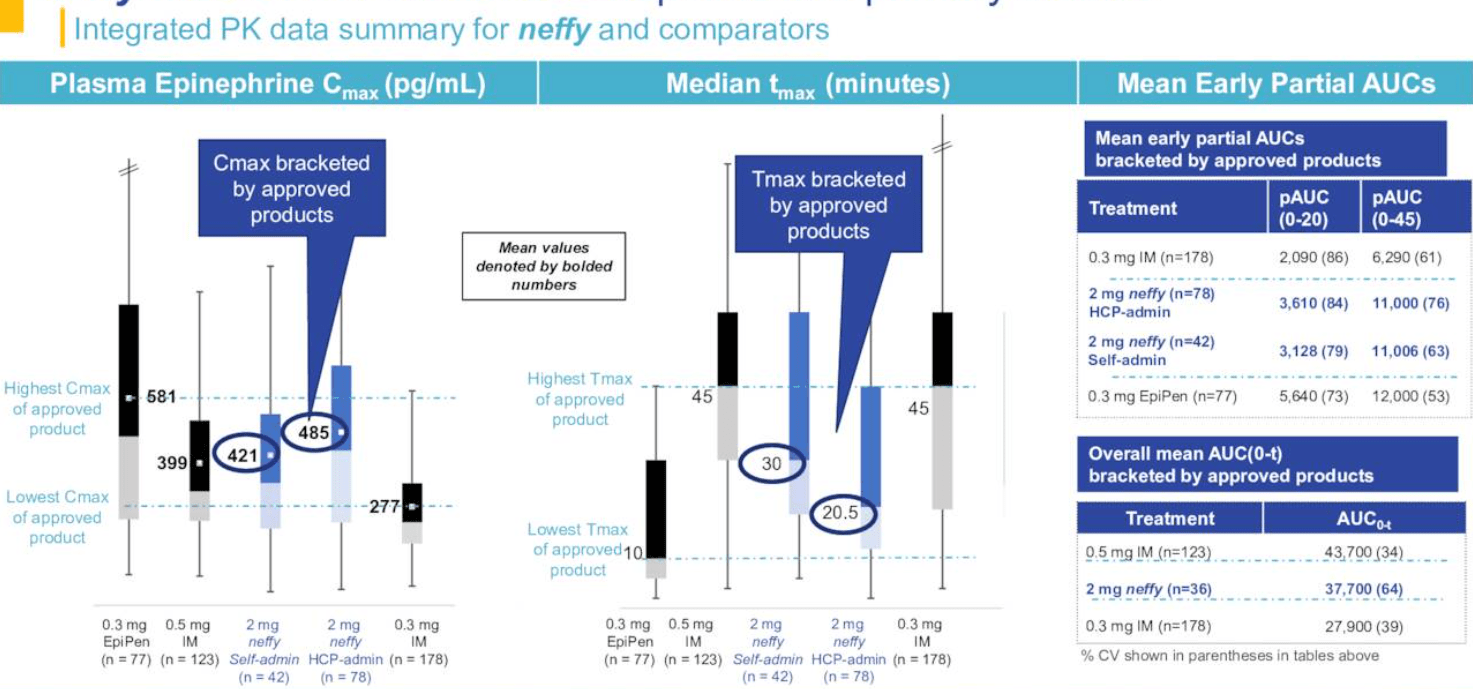

In registrational studies neffy has succeeded in meeting the primary endpoints, i.e. achieving pharmacokinetic ((PK)) targets in between the highest and lowest PKs of approved products (the so called "bracketing" that was explained above). Additionally, the hemodynamic response (=pharmacodynamic response), measured by systolic blood pressure and heart rate, after administration of neffy was comparable to some injection products including EpiPen, and was greater than 0.3 mg intra-muscular needle-with-syringe. These hemodynamic responses were within normal physiologic ranges that are typically experienced during exercise or climbing stairs.

Pooled pharmacokinetic data from Neffy's registrational studies (SPRY March company presentation)

{kind=link}

From a safety perspective, neffy was well-tolerated (no meaningful pain or irritation) among a total of more than 600 subjects (>1000 total doses). Importantly, for patients self-administering devices (n=132) approximately 14% of subjects dosed with EpiPen and 2% of subjects dosed with Symjepi experienced a potential blood vessel injection leading to a rapid bolus dose of epinephrine, which could lead to serious side effects including cardiovascular events and cerebral hemorrhage according to the FDA EpiPen label. Obviously, no subjects dosed with neffy experienced a blood vessel injection since it is not possible via the nasal route of administration. Also important is that the device was easy to use with no critical dosing errors observed.

Evidence and advantages of neffy (SPRY's 2022 Annual Report)

{kind=link}

Evidence for Anaphylm

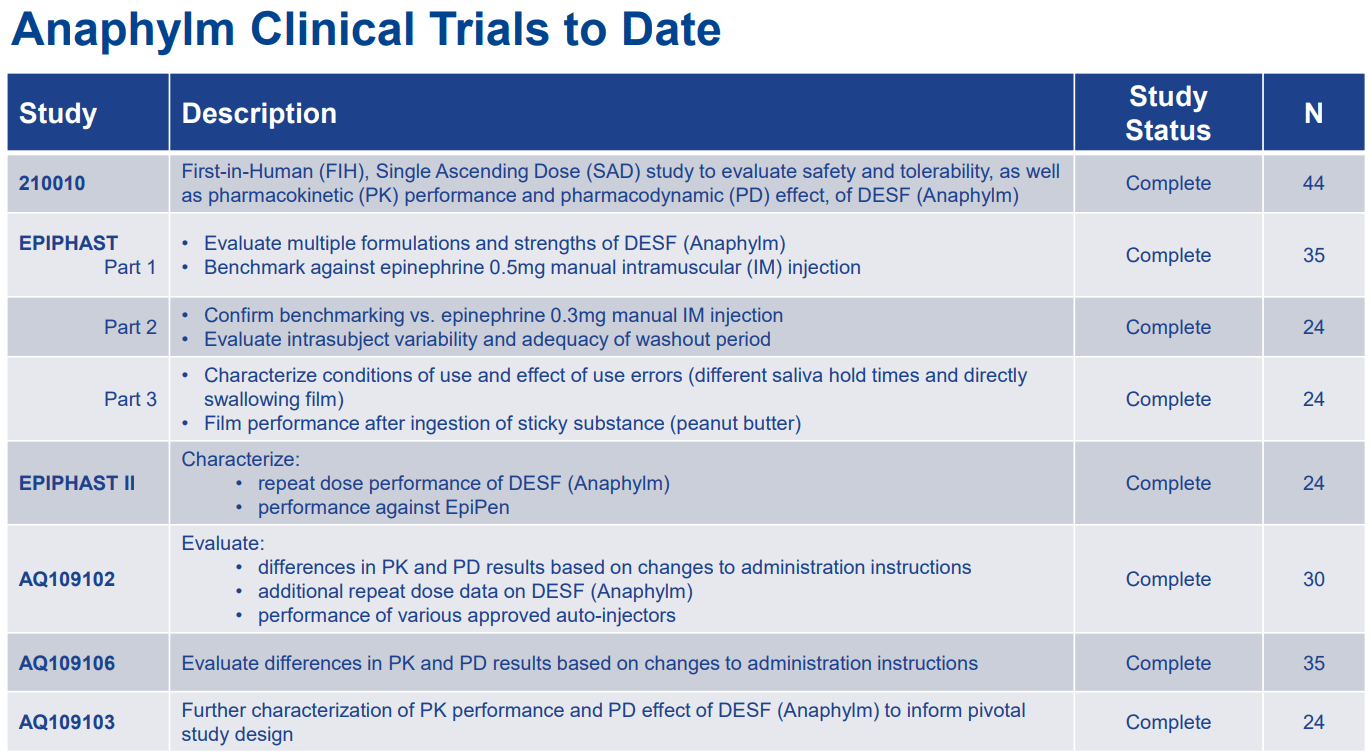

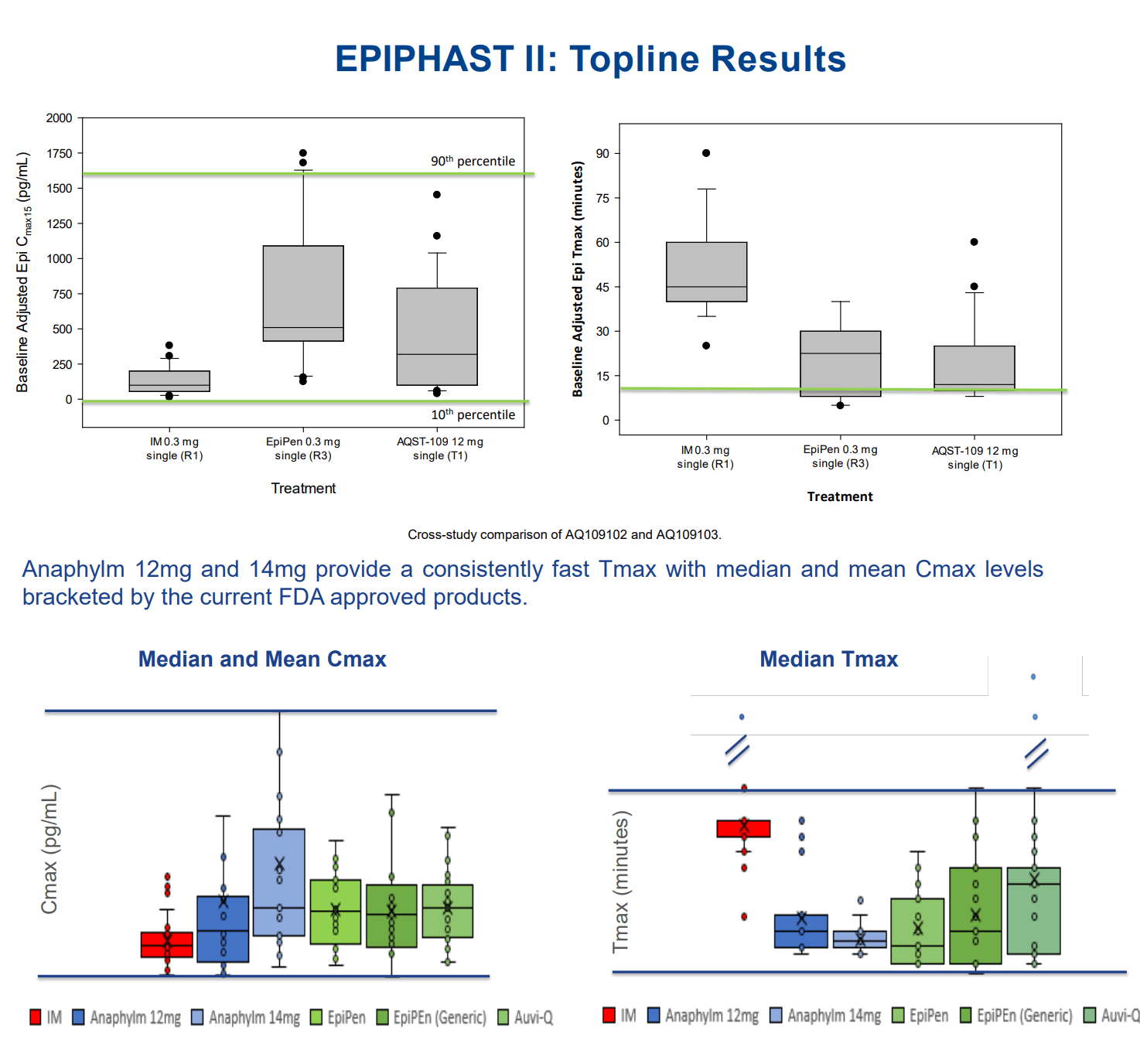

Anaphylm clinical trials conducted to date are summarized in the Table below. Similar to neffy, Anaphylm has achieved pk targets using the bracketing approach (Figure below). Notably, by indirect trial comparison Anaphylm seems to have a shorter Tmax compared to neffy, which could be a commercial advantage.

AQST company presentation Selected results from Anaphylm trials (AQST company presentation)

{kind=link}

{kind=link}

Based on these studies AQST has submitted to the FDA a protocol for a pivotal study and is expecting final feedback in October, initiation of the pivotal study in Q4 2024, and NDA submission in Q4 2024. Therefore, I would expect Anaphylm commercialization about a year later compared to neffy's anticipated launch if all goes well. However, I wouldn't be surprised if there are delays in AQST's anticipated timeline. Notably, SPRY had to do trials under experimental allergic rhinitis conditions to demonstrate efficacy under allergy conditions. Therefore, I wonder if something similar might be requested by AQST to confirm that angioedema doesn't negatively affect Anaphylm's pharmacokinetics.

Commercialization prospects; neffy vs Anaphylms vs auto-injectors

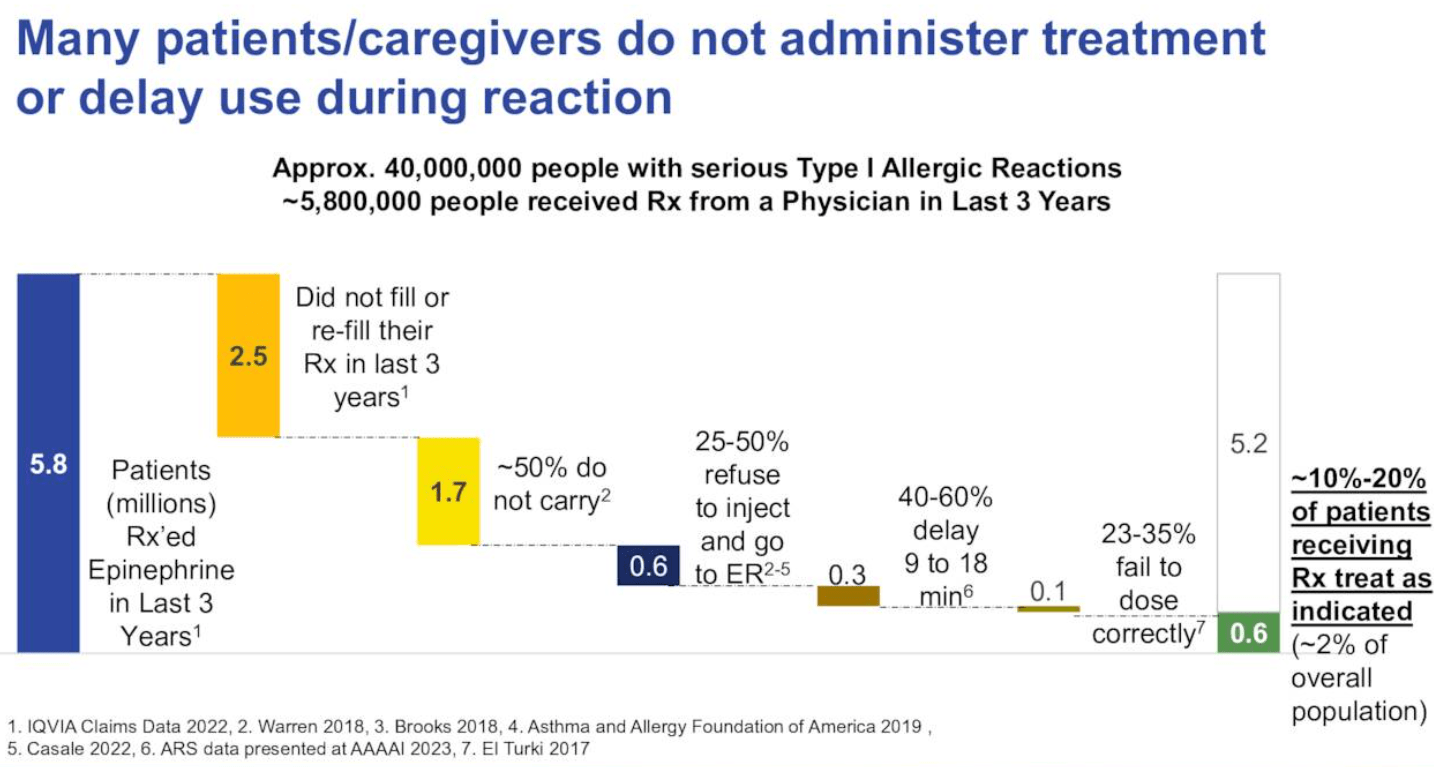

Current standard of treatment for anaphylaxis is epinephrine intramuscular/subcutaneous injection. Typically, affected patients have to carry an epinephrin auto-injector, which could be life-saving in case of accidental exposure to responsible allergens. The are many important problems/limitations with epinephrin autoinjectors; (1) Many patients are afraid of needles, especially self-administration, which can cause significant distress to some patients (as highlighted in the recent AdCom) or even reluctancy to use the autoinjector in a timely manner (or even at all). (2) Autoinjectors are relatively bulky to care. (3) There is the potential for accidental injury or accidental self-injection by care-givers (references 1 , 2 ).

According to the literature and SPRY's research the above limitations have the following consequences; Only 60% of prescription are filled / re-filled. Of patients filling their prescriptions, only 50% regularly carry the auto-injector, and of those 25% to 50% refuse to administer, while 40% to 60% delay administration by up to 18 minutes (resulting in prolonging troublesome symptoms, reducing quality of life and increasing the risk of complications or even death). Finally, even with training there is a high rate of dosing errors (up to 35%).

Limitations of epinephrine auto-injectors (SPRY March company presentation)

{kind=link}

Therefore, there is significant unmet need for non-injectable options. Both AQST's and SPRY's products overcomes all above limitations, being needle-free, easy-to-use and more portable options. Neffy is comparable in size to a wireless earbud case, while Anaphylm is even smaller and easier to carry and appears to have a shorter Tmx, which could be commercial advantages. Therefore, both products should have potential for significant marker penetration. SPRY has the major advantage of potentially reaching the market first, while AQST has the commercial advantage of being more portable. Delay by the CRL somewhat limit the head start that SPRY has over AQST. Nevertheless, there is a chance of regulatory delays for AQST as well, as explained above.

Comparison of the size/portability of different treatment options ( SPRY and AQST company presentation)

{kind=link}

Despite limitations, injectable epinephrine sales in 2021 in US were estimated at $1 billion . Notably, global epinephrine auto-injector market is estimated to reach $3.2-3.7 billion by 2028-2032 according to various estimation (references 1 , 2 , 3 ). Even capturing just 10% market share (which is very conservative considering advantages of non-injectable options) would mean potential peak sales of about $350 million, which would correspond to a fair enterprise value of $2.5B (considering EV/sales ration of 7.1 typical for biotechs). At the time of writing the enterprise values of SPRY and AQST were $98 million and $128 million, respectively.

The actual anaphylaxis market size potential may be even higher considering under-filling of epinephrine injection prescriptions. Furthermore, considering major advantages there is the possibility of selling at a premium compared to auto-injectors. On the other hand, fierce competition in the field could significantly limit revenue potential.

Financials

Based on the latest quarterly report SPRY had cash, cash equivalents and short-term investments of $252.2 million as of June 30, 2023. Operating expenses were $20.6 million (R&D $7.3 million, G&A $13.3 million). Therefore, SPRY is well-capitalized to withstand the regulatory delay. Notably, SPRY anticipates cash, cash equivalents and short-term investments of about $195 million at the time of anticipated neffy launch (2H 2023). The robust financial position of SPRY significantly de-risks the stock at current price.

On the contrary, AQST has a limited cash runaway. Based on the latest quarterly report cash and cash equivalents were $22.4 million as of June 30, 2023. Loss from operations was $4.2 million (revenues $12M, manufacture and supply $6.6M, R&D $3.5M, selling and G&A $7.4M. At this rate of cash burn AQST should have a runaway of about 5 quarters (i.e. up to Q3 2024). AQST anticipates NDA submission in Q4 2024. Therefore, there is significant risk of dilution before that.

Risks to the thesis

I remind here that the thesis is to invest in both stocks, based on the expectation that at least 1 of the 2 stocks will be successful. The obvious risk is that both stocks could fail due to regulatory setbacks or emerging competition. The latter is a major risk, especially for SPRY given competition by several other biotechs developing nasal epinephrine devices.

If I had to choose only 1 stock

My suggestion is to invest in both SPRY and AQST because of reduced risk and good upside potential by this approach. However, If I had to choose 1 stock the choice would be hard. Some could favor SPRY for the following reasons: de-risking by already completed registrational studies and positive AdCom, likely head-start in commercialization despite regulatory delay, robust financial position despite regulatory delay, short cash runaway for AQST and regulatory uncertainty for AQST (there might be surprises for AQST, which could be much worse than the CRL received by SPRY). On the other hand, long-term AQST has the potential overtake more market share considering portability advantage, better Tmax and less competition (SPRY will have to compete with other nasal epinephrine devices long-term). Furthermore, AQST has approved products and a pipeline which could limit downside risk (in contrast to SPRY who is a single-product company). Therefore, the decision to bet in only one of the two stocks is complicated and would be riskier in my opinion.

Conclusion

In my opinion, neffy's CRL offers a reduced risk approach to invest in non-injectable options in the anaphylaxis field by investing in both SPRY (ideally after waiting for a dip opportunity considering the +40% upside the last 2 days while preparing the article) and AQST. The rationale is that I expect at least 1 of the 2 companies to be successful, in which case the anticipated upside from current stock prices should outweigh the losses from the less successful stock. Best case scenario (not unlikely) is that both stocks have significant upside from current price levels. Profits could be larger if choosing to invest in only 1 of the 2 stocks assuming the correct choice is made. However, this also bears the risk of making the wrong choice in which case the downside risk would be considerable. Competition by other companies developing epinephrine nasal sprays is a major risk to the thesis.

Your feedback is appreciated

Please comment below if you have any feedback (negative or positive), if you spot any mistakes or if you believe I missed something important in the article.

For further details see:

ARS Pharmaceuticals Vs. Aquestive Therapeutics; Neffy CRL Creates An Opportunity For Investing In Both