HE - Artesian Resources: Why This Stock Is A Buy

2023-10-20 14:15:22 ET

Summary

- Artesian Resources Corporation is a water utility company that has historically provided low volatility and safety for investors.

- The need for water transcends economic cycles, making Artesian's stable supply of clean water a valuable asset.

- Rising interest rates and debt are concerns, but Artesian's strategic growth, insider ownership, and financial performance make it an attractive investment choice.

Introduction

Artesian Resources Corporation ( ARTNA ), a tiny yet indispensable utility based in the Delmarva peninsula, is a company that thrives on providing one of life's most essential resources - water.

In a volatile world, investors often crave safety.

We hear it in the news all the time… geopolitical threats, economic shocks, and increased regulation, it can feel like a constant drumbeat. Even investments that were once viewed as safe, like long-term bonds or a Hawaiian utility company, Hawaiian Electric Industries ( HE ), have experienced extreme volatility, albeit under different circumstances.

This leaves us investors with an important question to answer… is there anywhere safe left to hide? If even a utility company stock like Hawaiian Electric can be trashed can any investment truly be safe?

I think so.

While all stocks are subject to risks, they are not equally exposed.

Historically as an investment, Artesian's stock has been a beacon of low volatility and safety, offering a rare reprieve in the face of never-ending market turbulence. Yet, recently, it took a hit, with its share price plunging from its recent high of $63 all the way down to $40 a share.

But fret not, I think this is an opportunity to take advantage of a rare spot of weakness in an otherwise fantastic track record.

In this article, I aim to guide you through the "ebb and flow" of Artesian Resources' journey. We'll delve into the company's history, recent business performance, financial health, and valuation.

Company Overview

To understand Artesian Resources, we must first grasp its core business activities. This company is at the heart of the water utility sector, a realm often overlooked but indispensable for our daily lives. While the world evolves, the need for water remains constant, and this stability can be an extremely valuable attribute for risk-averse investors.

Unlike other commodities, the need for water transcends economic cycles and market upheavals. This constancy is deeply embedded in our daily lives, as water is a fundamental resource required for drinking, sanitation, agriculture, and industrial processes. Regardless of economic downturns or upswings, individuals, households, and businesses consistently rely on a stable supply of clean water.

After all, in an economic slowdown you might cut down on lavish meals and trips, but few in the developed world, if any, will drink less water to cut down on the utility bill.

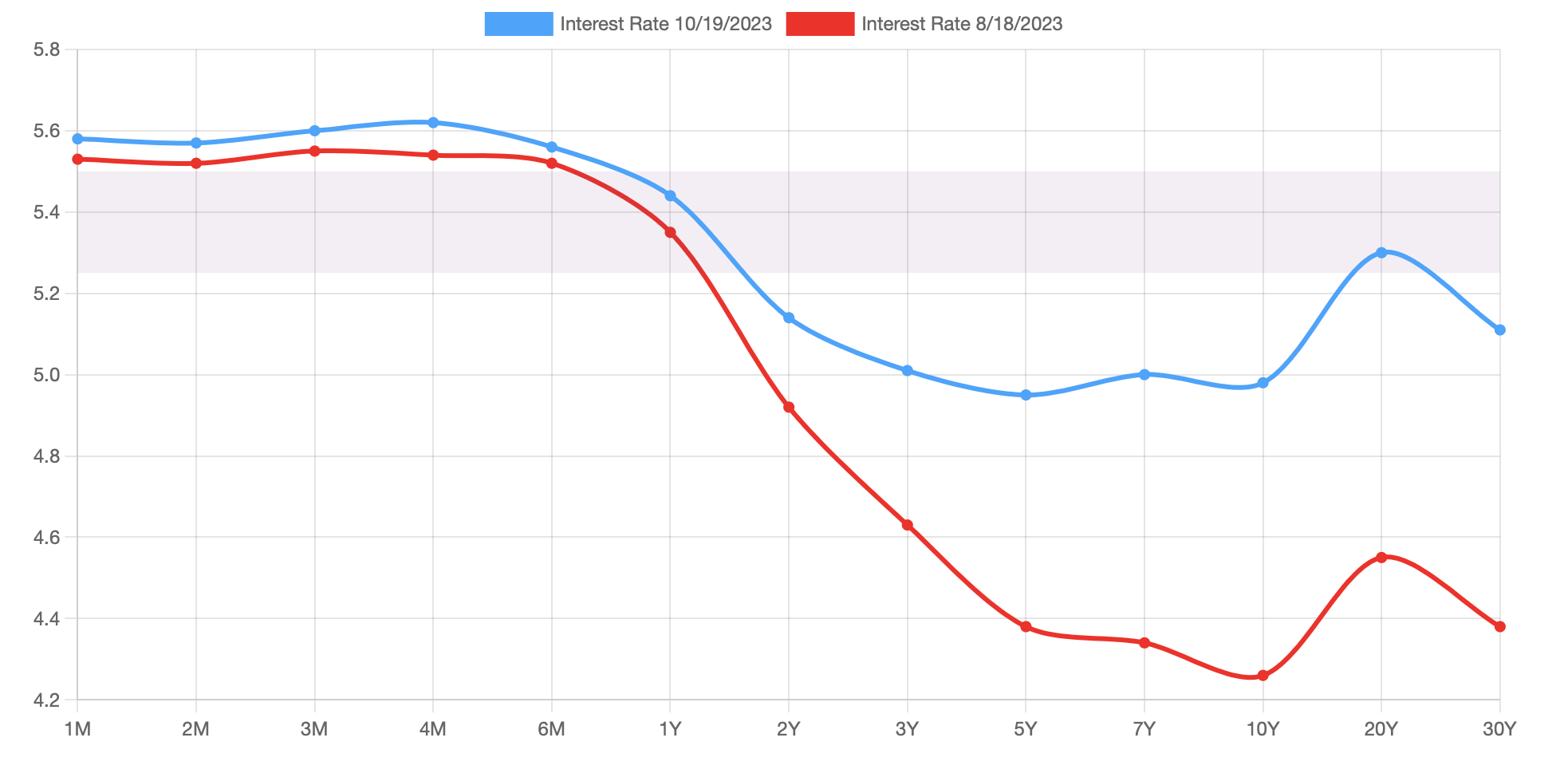

Rising Interest Rates

As a company with a significant amount of debt, it's important to discuss how the impact of rising rates will affect Artesian's $523M of liabilities.

{kind=link}

Over the last 2 months interest rates on the long end of the curve have risen dramatically. The 30-year interest rate in August was at 4.4% whereas now it's over 5%, these increases have huge implications on financing costs.

As the cost of financing goes up with increasing rates, it eats into a company's profitability. Since higher interest costs eat into a firm's earnings it reduces the amount of money available for reinvestment, dividends, or share buybacks, all of which can enhance shareholder value.

While interest expense is low for the moment, at just $9.3M over the last 12 months, I believe we should expect this to increase over the coming years as debt is refinanced at much higher rates, perhaps even doubling or tripling.

Over the past 5 years you can see there is a consistently increasing amount of cashflow that management must use to pay down the liabilities of the firm.

Growth Strategy

Artesian Resources' strategic approach involves a slow yet steady expansion through acquisitions primarily within its territory of the Delmarva peninsula.

This is a similar strategy compared to what has worked for many in the industry. Integrating acquired businesses with similar business models is often a smoother process, as the existing synergies and shared operational practices facilitate a more seamless transition, reducing potential disruptions and enhancing efficiency. As such, it's no wonder that many water utilities are actively expanding through acquisitions.

For example, it'll be much easier for Artesian to integrate the small water utilities it acquires than it would be for Microsoft ( MSFT ) to integrate Activision ( ATVI ). You can read more about that deal here .

A recent example of Artesian's strategy was its 2022 acquisition of the Town of Clayton's water system. Through this acquisition, Artesian will now provide water to an additional 7,000 customers and the local governments can redeploy the funds into other local developments/programs. While this acquisition is not a game changer, it's those incremental net gains which can produce shareholder returns over the long term.

Insider Ownership

One noteworthy aspect of Artesian Resources is its high level of insider ownership. When insiders hold a significant stake in a company, it often signals their confidence in its future. One of my favorite investors, Chris Mayer author of 100 Baggers was quoted as saying:

"I like investing with companies that have high insider ownership. I think it brings the alignment with shareholders closer together."

I agree with Chris Mayer, in most companies, the result of a poor performance results in a lower payday or losing one's job, at companies with high insider ownership the risks are far more severe as your savings could be destroyed as well. I believe that this is a strong motivator to drive the right sort of thinking from management.

In the case of Artesian Resources, the founders control the company through the B-Class shares ( ARTNB ) where they control more than 70% of shares outstanding. Given the long-term trajectory of the business, I am comfortable with this level of control, though others may come to a different conclusion.

Financial Performance

Despite such a simple business model, Artesian's revenue growth at 43% is best in class compared to peers York Water ( YORW ), American States Water ( AWR ), and American Water Works ( AWK ). Surprisingly, the second fastest growing was another small utility, York Water which was close behind at 42%, this goes to show that size is not everything in the world of utilities.

While Artesian has indeed grown revenues faster than its peers, its EPS growth is much more in line having grown 73% over the past 10 years. To an extent, this is understandable as the more acquisitive larger companies are able to extract more efficiencies through the larger deals they pursue.

While EPS growth leaves some room for improvement, in defense of Artesian, it's likely the case that due to its smaller size there may be a greater runway for future growth as their pool of target utilities is larger than big peers due to the large number of smaller municipalities.

The above chart shines a bright light that the impact of higher rates are having on the industry. Financing costs are skyrocketing for all these companies (except York Water) after having been most flat over the last decade. Luckily, Artesian's increase is relatively in line with the rest of the peers at a 29% growth from the 2013 levels.

Valuation

Looking at these companies' PE ratios we can see that Artesian trades at the lowest price to earnings multiple at 23.3x, this is relatively in line with its historical average.

American States Water, which has often traded in the 40x PE range is now down to 24.5x, which to me, is an indication that there is a risk that Artesian's PE could fall lower. But I would argue, that this is more so an appropriate realignment of these companies' PE ratios based on their similar business models and historical performance. I've not seen compelling evidence which indicated one company ought to trade at such a premium compared to the rest.

Conclusion

Artesian Resources, a small yet sturdy utility serving the Delmarva peninsula, has historically provided a haven of stability for investors. Recent stock price fluctuations, while noteworthy, do not diminish the company's long-term potential.

The steadfast demand for water, irrespective of economic cycles, underlines the unique value that Artesian offers. Rising interest rates and debt are concerns, but the company's strategic growth, substantial insider ownership, and impressive financial performance make it an attractive investment choice.

The waters may be a bit turbulent now, but the tides could change, and with it, the fortunes of Artesian Resources.

I rate Artesian Resources a "Buy".

For further details see:

Artesian Resources: Why This Stock Is A Buy