CA - Artis: Retail Asset Sales Reduce Risk Further For This 10.9% Yielder

2023-12-27 10:00:00 ET

Summary

- Artis has felt the issues with rising interest expense married to a short debt maturity profile.

- Retail asset sales of $222 million were done just before Christmas.

- We examine the setup and tell you why we believe Artis can pull this off.

Note: All amounts discussed are in Canadian Dollars. All issues primarily trade on the TSX.

On our last coverage of Artis REIT ( AX.UN:CA ) ( ARESF ), we fought back against the idea that the distress was terminal. Our analysis of the property values showed that it would be hard, if not impossible, for a buyer to lose out if they went long. We would still be encouraged further if Artis actually sold some office properties in the current market to help delineate the bull case.

It is hard to argue with those numbers, especially as Artis has shown the ability to unload industrial and retail properties at or above IFRS values. This all suggests that there might be some value here for the investor ready to go in with a longer term outlook. Artis is looking at alternatives here but there really is none outside of selling some office properties at good values to show that the market is wrong.

Source: Heavily Discounted REIT, Here Is One Way To Play It

We ultimately gave the common units a pass and went long the preferred shares on October 30, 2023 . Artis has been flat over the course of this but we did get an early Christmas present as the REIT announced decent sized asset sale.

Artis announced today that it has entered into an unconditional agreement to sell a portfolio of eight Canadian retail properties (the “Canadian Retail Portfolio”) for an aggregate sale price of $222.0 million. The Canadian Retail Portfolio comprises four properties located in Calgary, Alberta, totaling 293,660 square feet of leasable area and four properties located in Winnipeg, Manitoba, totaling 301,539 square feet of leasable area. The sale price of $222.0 million represents a price per square foot of $373, and the properties have approximately $80.5 million of mortgage financing. Proceeds from the transaction will be used to reduce overall debt. The sale price for the Canadian Retail Portfolio is in line with the REIT’s International Financial Reporting Standards (“IFRS”) fair values reported at September 30, 2023.

Source: Artis

Q3-2023

To put the asset sales in the right context, we need to see the Q3-2023 numbers. Those were released after our last article. The main numbers showed some big declines with revenues and net operating income ((NOI)) down over double digits. The adjusted funds from operations ((AFFO)) payout ratio reached 100%. This was just 62.5% a year ago.

{kind=link}

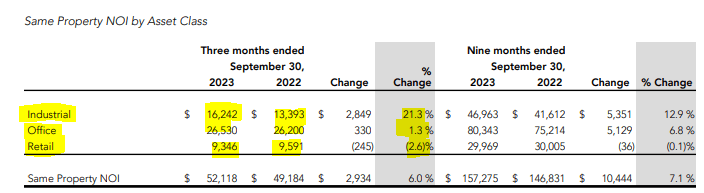

While those look like a scary level of deterioration, they are a deliberate results of asset sales. One way to parse through this is, is to examine same property level NOI. We can see that same property NOI still looks robust.

{kind=link}

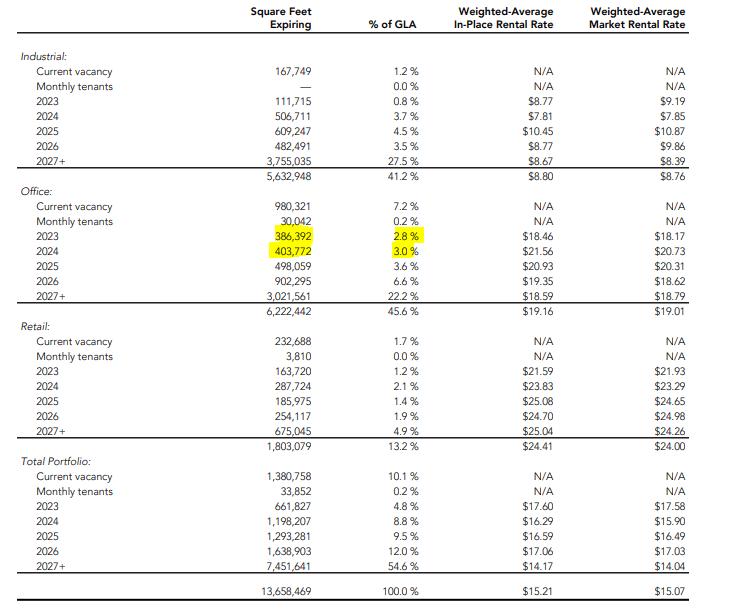

Some might be worried that the overall levels are not reflective of the problems in office. That is a fair point. The office segment is one where all the spotlight has been for diversified REITs. But Artis is looking solid on that front and while the office segment did not watch the barnburner of a performance that industrial delivered, it did ok.

{kind=link}

Equally importantly, lease maturities are minimal relative to its GLA for the next 12 months (15 months from Q3-2023 end date). Market rents while below the lease rates, are again, unlikely to break things.

{kind=link}

Outlook

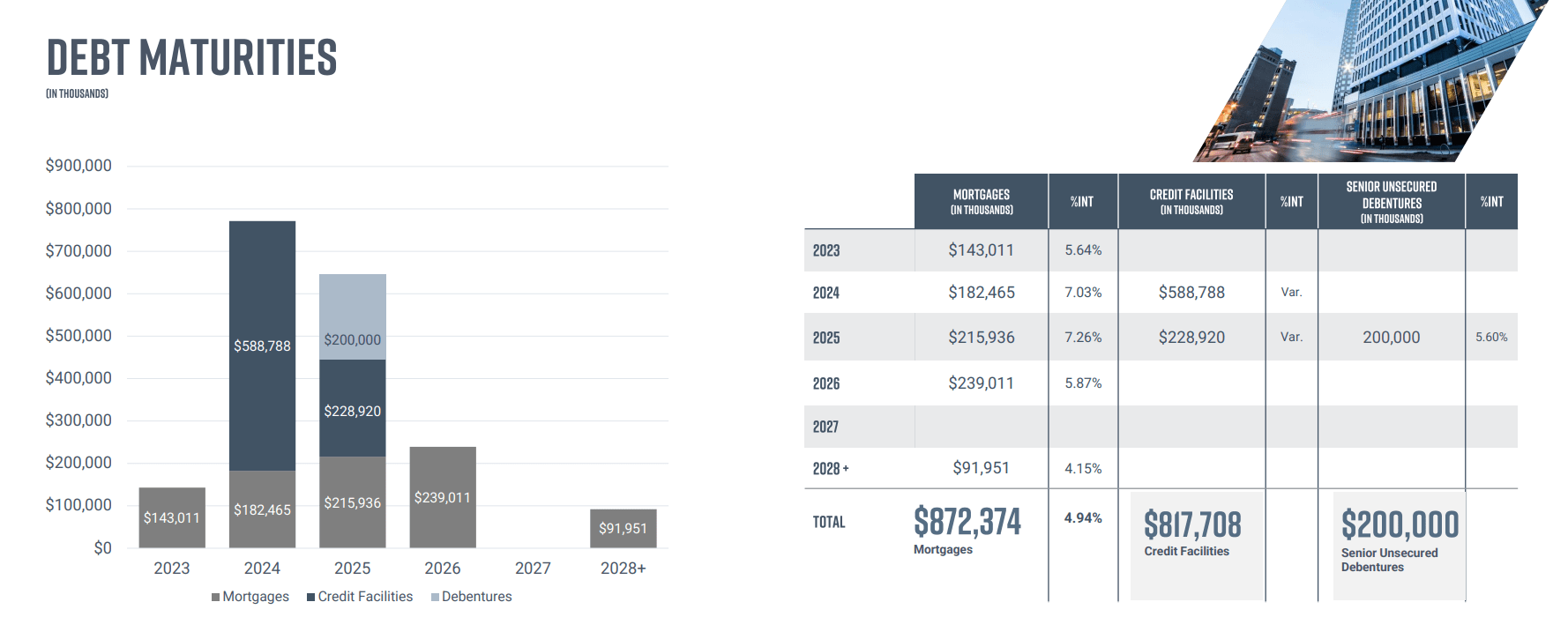

The albatross around the Artis neck was the debt maturities for 2024 and not the lease maturities. With over $750 million due in 2024, the REIT had its work cut out for it.

{kind=link}

The retail asset sale for $222 million, takes off a good chunk of this. This is happening in conjunction with a credit spread implosion.

Risk assets should be embracing this setup but Artis remains in the doldrums. This is really Artis' fault as no other REIT setup their debt maturities so poorly. It has cost them tons of extra interest payments and really limited their options. Artis is paying over 6.2% on average on its total debt and the bulk of the maturities are within 24 months. By comparison H&R REIT ( HR.UN:CA ), which is one where we were also critical of the debt structure was paying 4% on last check.

The weighted average interest rate of H&R's debt as at June 30, 2023 was 4.0% with an average term to maturity of 2.9 years. The weighted average interest rate of H&R's debt as at December 31, 2022 was 3.8% with an average term to maturity of 3.2 years.

Source: H&R REIT Q2-2023 Results

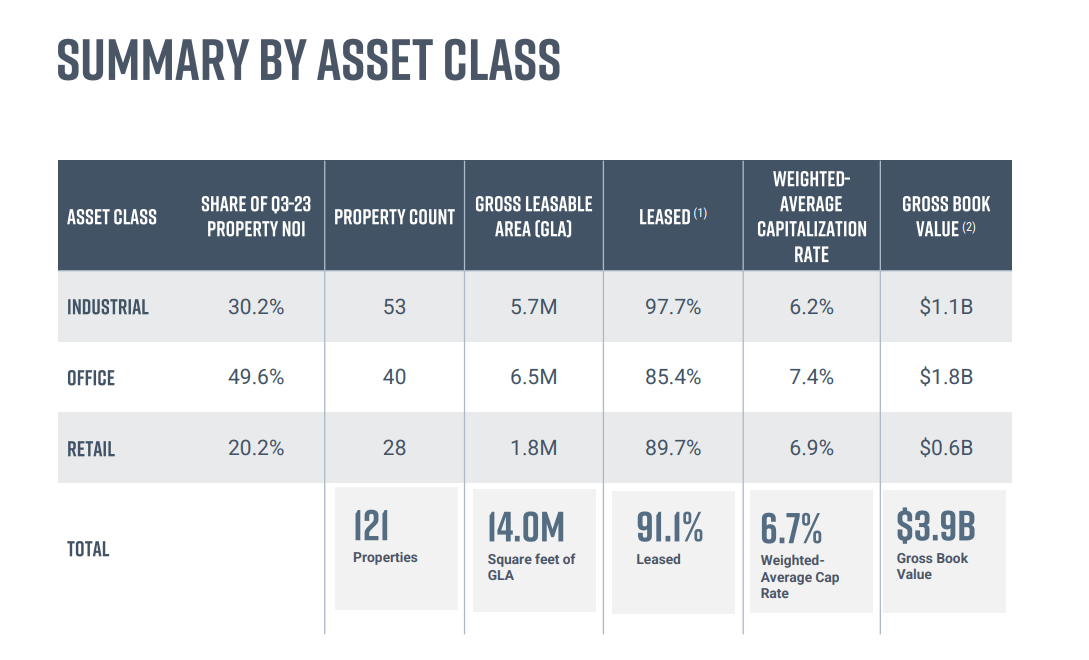

We think we likely need another $200-$300 million more of asset sales to make the market feel that the risk is finally off. We think we can definitely get that barring a complete meltdown in markets within two quarters. One must also be cognizant of the fact that Artis is using very high cap rates (low implied valuations) for industrial properties. This is a bit odd as same property NOI was up high double digits and most other industrial REITs are using a high 4 or low 5 number for cap rates.

{kind=link}

So selling $300 million of assets from there, likely way above IFRS, should fix Artis and we are likely to see a run to $8.00.

Verdict

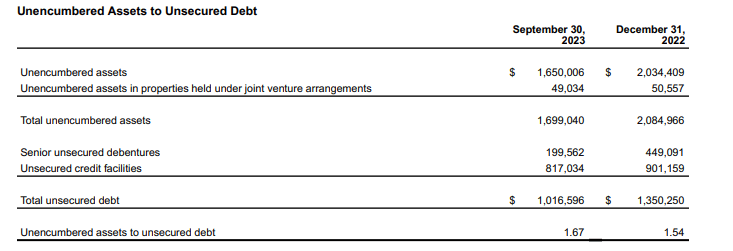

We think the buy setup is in place and a run 20% higher over the next 6 months seems highly probable. Artis will get this ratio of unencumbered assets to unsecured debt to over 2.0X by then and that should allow them to place some longer dated debt in place.

{kind=link}

Beyond that, Artis needs to keep its head down and keep selling assets. Even small hits under their IFRS value are fine as the market is valuing it at a 60% discount to its NAV. Once the debt maturities are addressed, selling a $1 asset for 90 cents can still make sense if they buy their own units back at 50 cents on the dollar. While we are rating the common shares a Buy, our caveat here is that we are still only long the preferred shares. We think the risk-reward still looks better on those two. We own Artis Real Estate Investment Trust PREF SHS I ( AX.PR.I:CA ). They pay 6.993% on par and currently yield 10.92%. They have a minimum reset feature (6% minimum on par), in case Artis extends its public career all the way till April 2028 .

We would also not get too comfortable with the 9.2% yield on the common units though. If things get rocky, that distribution will get cut in a heartbeat. Hence our preference for the preferred shares.

For further details see:

Artis: Retail Asset Sales Reduce Risk Further For This 10.9% Yielder