ASAN - Asana Earnings: Closer To Breakeven Profitability But Uncertainty Remains

2023-06-02 09:48:18 ET

Summary

- Asana's revenue growth rates have significantly slowed down, no longer making it a rapidly growing SaaS company.

- Despite the slowdown, Asana is improving its profitability profile, with significant improvements in operating profits and margins.

- The customer adoption curve has decelerated, indicating a shift in Asana's near-term prospects, warranting caution.

- The exact timeline for reaching breakeven profitability is uncertain, although Asana aims to achieve positive free cash flow before the end of calendar 2024.

Investment Thesis

Asana (ASAN) puts out a very mixed report . The negative aspect that is becoming increasingly clear is that Asana is no longer a fast-growing company. This is a company that's growing at 20% CAGR. Period.

The positive aspect is that Asana is rapidly improving its profitability profile. Case in point, during the most recently reported quarter, both Asana's GAAP and non-GAAP operating profits significantly improved, with its non-GAAP operating margins improving by a whopping 3,000 basis points compared with the same period a year ago.

The takeaway for investors is that from this point forward, Asana's breakeven profitability profile is now significantly closer.

Why Asana? Why Now?

Asana is project management and team collaboration. It's somewhat like Monday.com ( MNDY ) and Atlassian ( TEAM ), but without the open ''low code'' functionality that allows developers to customize their operations.

Simply put, Asana is more rigid. That suits certain teams that seek an intuitive interface with a focus on task lists, whereas Monday.com offers a customizable suite of drag-and-drop software for managing tasks.

There are plenty of other analysts on SA who will extol the praise of the co-founder and CEO Dustin Moskovitz, so I don't believe that insight is something worthwhile for me to repeat here.

Rather, I prefer to press ahead and get to the meat of my argument.

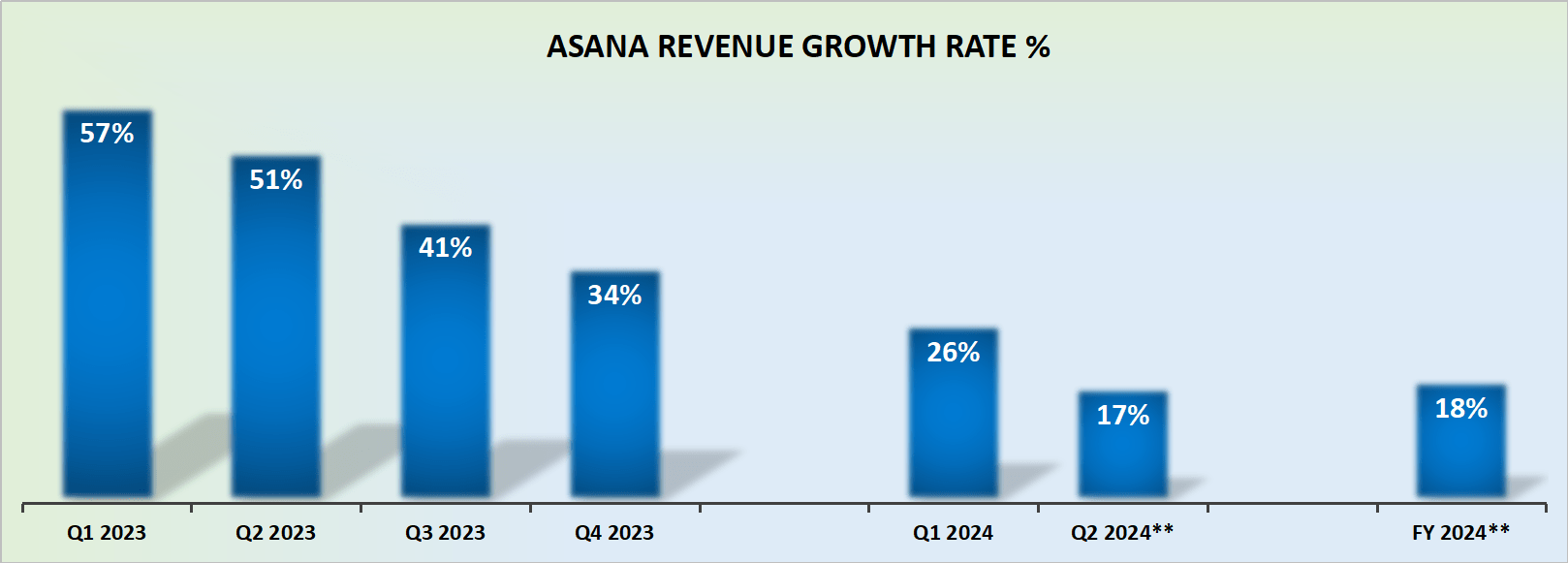

Revenue Growth Rates Are Slowing Down

{kind=link}

Asana's revenue growth rates are rapidly slowing down. This was a company that a year ago was growing at higher than 50% CAGR, and today the outlook for the next quarter is less than half of this.

Even if assume that the comparables become easier next year, the fact of the matter remains that Asana can no longer be perceived as a rapidly growing SaaS business.

Consequently, if the business is presumed to be growing at around 20% CAGR, investors will increasingly clamor and question, when will Asana start to become profitable?

Before attempting to answer this question, I ask that you consider this:

ASAN Q1 2023

What you see above is Asana's customer adoption curve for customers spending more than $5K until last year's fiscal Q1 2023.

At the time, Asana could be counted on for customer growth rates of mid-20%. And now?

ASAN Q1 2024

As of fiscal Q1 2024, the customer adoption curve has decelerated to 19% y/y. This insight alone should inform readers to approach Asana with caution. Evidently, something in Asana's prospects have shifted since last year.

Path to Breakeven Picks Up Moment, Or Does It?

{kind=link}

This time last year, Asana's free cash flow margins were negative 35%, while this time around Asana's free cash flows improved to negative 11%.

As we look ahead to fiscal Q2 2024, this is what Asana's Head of Finance Tim Wan said on the earnings call,

We expect non-GAAP loss from operations of $120 million to $110 million, representing an operating margin of negative 18% at the midpoint of guidance, down from negative 38% in fiscal year 2023

Simply put, Asana is clearly determined to improve its profitability profile. That being said, during the earnings call, Asana fell short of reiterating exactly when it would reach breakeven profitability.

And this complicates matters, because last quarter during Asana's earnings call management said,

Despite the uncertainty with the macro environment, we have increased confidence in our ability to be free cash flow positive before the end of calendar 2024, while balancing growth and profitability.

This leads to believe that Asana may not succeed in reaching positive free cash flow before the end of calendar 2024.

The Bottom Line

This quarter's earnings results contained both positive and negative aspects.

On the positive side, Asana is improving its profitability profile, with significant improvements in operating profits and margins.

This suggests that Asana's breakeven profitability is now closer.

The revenue growth rates for Asana have slowed down, with the company no longer being perceived as a rapidly growing SaaS business. Further, the customer adoption curve has also decelerated, indicating a shift in Asana's near-term prospects.

While Asana is determined to improve profitability, the exact timeline for reaching breakeven profitability remains uncertain. Asana aims to achieve positive free cash flow before the end of calendar 2024, but there are doubts about whether they will succeed in doing so.

For further details see:

Asana Earnings: Closer To Breakeven Profitability, But Uncertainty Remains