ASAN - Asana: Enterprise Expansion And The X Factor Are Big Plusses

2023-04-17 13:03:51 ET

Summary

- Sales & Marketing / S&M spending to strengthen enterprise go-to-market have been aggressive. S&M has been 70% - 80% of total revenue.

- Big seats landing leading to company-wide deployment in an enterprise setting is an ideal profitable growth strategy for Asana.

- S&M spend should optimize under new CRO and CMO appoints, as well as the X factor - Co-founding CEO Dustin Moskovitz.

Asana ( ASAN )'s IPO was one of the few tech IPOs I anticipated the most back in 2020. Co-founded by former Facebook ( META ) co-founder Dustin Moskovitz / DM and VP of Engineering Justin Rosenstein, Asana has gained a reputation as a visionary and product-focused cloud software company in the project management space. As a former VC and tech operator who has experienced Asana's product firsthand, I consider Asana an interesting company that merits further exploration as a growth investment opportunity.

Based on my overall findings, I am initiating my Asana coverage with a buy rating. As a caveat, it is a growth stock I recommend more as a long-term hold than as an opportunistic buy. As with any tech stocks facing the economic shocks from COVID-19 followed by inflation and overall increased pressure towards demonstrating a path to profitability, Asana has seen a considerable amount of selling pressure in recent years and is making strategic adjustments to reach profitable growth faster.

Briefly, here are a few key points driving my bullish call on the stock:

-

Asana is still early in its go-to-market reorganization to strengthen its focus on the enterprise segment. Once key leadership appointments, such as CRO, are made and the sales motion is fully ramped up, I expect revenue growth to reaccelerate anytime beyond the next 18 months. Asana's shift towards the enterprise segment is also a key factor in driving profitable growth. In general, company-wide deployment in an enterprise setting comes with a higher number of seats, switching costs, and price per seat.

-

Asana has demonstrated a commitment for operational efficiencies. Despite the aggressive investments in sales and marketing at certain times, I observed the signs of economies of scale kicking in the post-investment periods. The company also made a bold decision to layoff 9% of its workforce to improve operational efficiencies last year - a popular move among most tech companies, but still riskier to pull off at a company promoting best practice working culture like Asana.

-

Co-founding CEO Dustin Moskovitz is the X factor in Asana. As I highlight in the latter section of this article, DM's strategic intervention to purchase Asana's shares at times has shown a true long-term commitment, confidence, and belief in his vision.

In this coverage, I am sharing Asana's pros and cons across my view of its financials, market landscape, and management team. I account for all of these factors in my thesis as I set a 5-year target price for Asana.

Market Landscape And Positioning Review

Cloud project management / PM and collaboration software is a large market with different vendors competing along the SMB and enterprise segments. Asana suggested their overall TAM to roughly be ~$50 billion in 2025.

A typical PM tool helps teams manage projects and workflows more effectively. It allows users to create tasks, assign them to team members, and track progress. It offers features like team collaboration, project timelines, and custom templates. Some vendors, including Asana, offer more advanced features, such as AI-driven to-do recommendations.

There is a real chance for company-wide expansion to gradually happen more naturally in the adoption roadmap of PM than in other cloud tools. More often than not, a specific department that purchases a PM solution and has good experience with it will start expanding the usage for cross-functional projects that draw in other departments. This is an opportunity that many vendors aim to capture by refining their pricing model and features around that particular use case. As a result, many of these PM vendors have seat-based pricing tiers. It means that landing a 20-people small team within an enterprise client with 5,000 employees with complex PM workflows in some cases is preferable to landing a company-wide deal with an SMB with 150 employees.

{kind=link}

In the PM space, Asana has been a household name among SMBs and mid-sized businesses. In the early years, it was often compared to Trello ( TEAM ), whose tool has been more focused on Kanban-style PM. Given its drag-and-drop and intuitive UIs, Trello comes across as a simpler solution, while Asana generally has a steeper learning curve and a better fit as a more comprehensive enterprise PM tool.

In addition to Asana and Trello, there are several vendors that G2 considers market leaders in the PM space, such as Smartsheet ( SMAR ) and Monday.com ( MNDY ). Overall, these vendors have overlapping features that address cross-functional PM team collaboration in different approaches. Smartsheet is more of a PM tool that combines project management with spreadsheet functionality and UI. Monday.com is a PM tool that also caters to specific needs of certain functions such as sales and marketing by having a built-in CRM within their platform.

Considering the moderately non-standard ways of how PM tools can integrate into a particular client base's workflows, every vendor can strategically develop a PM tool that is customizable enough to fit within the workflows of most departments, yet is powerful enough to address the specific needs of departments with more standardized processes like sales or marketing. In a way, this means creating a PM product that has the capability to replace existing CRM, support helpdesk, and other operational tools, expanding the scope of PM and the TAM in the process.

Q4 And Financial Review

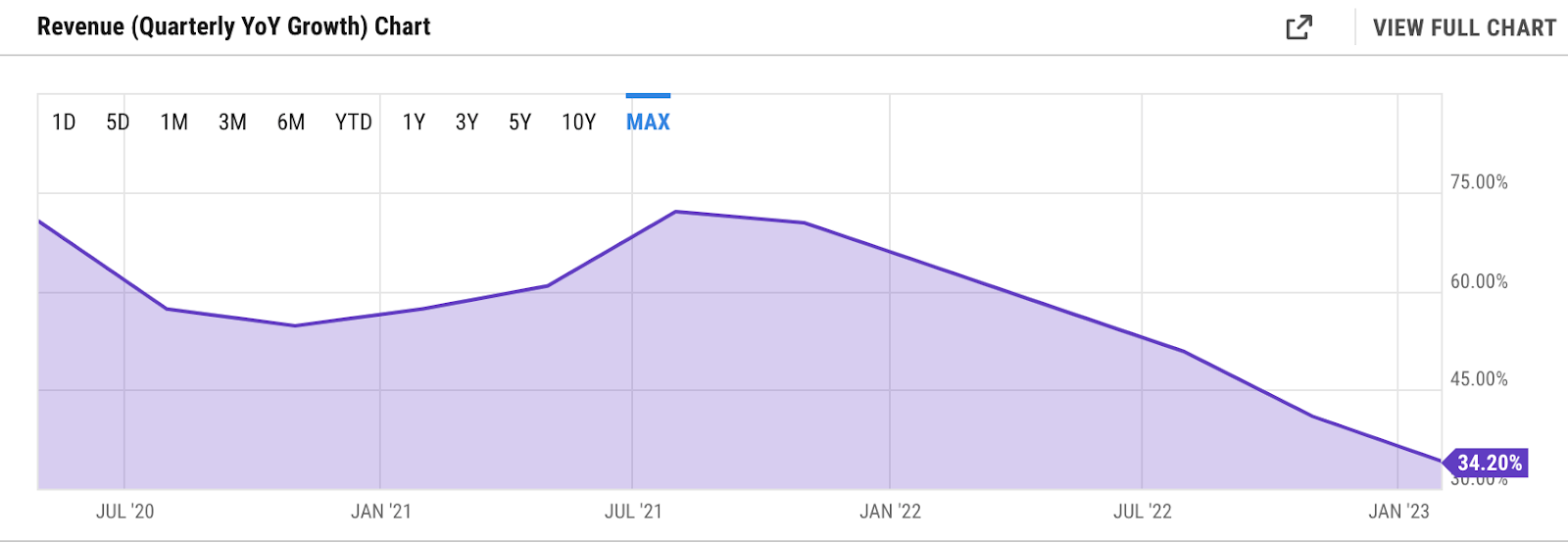

In Q4 2023 , Asana narrowly beat the revenue guidance with a revenue of $150.2 million, a +34.2% YoY growth. For the full year, Asana grew 45% YoY with a FY 2023 revenue of $547.2 million.

Asana continued its convincing progress in winning enterprise deals, highlighted by the 80% YoY growth in revenues from customers spending $100k+. In Q4, we learned that the $100k+ segment made up around 25% of the total revenue already. The segment also already outperformed the lower-pricing $5,000+ segment in terms of net retention rate / NRR. While the $5,000+ segment's 120% NRR is sufficiently strong, the 135% NRR achieved in $100k+ segment is impressive.

YCharts - ASAN quarterly YoY growth

{kind=link}

Overall, it was a relatively solid Q4 and FY 2023 performance by Asana, considering the tougher macro environment. Zooming out over the past two years, we see how growth has been affected by the macro issues.

The bad news is that the macro issue is expected to continue into FY 2024, and has already baked into the growth forecast of most cloud software stocks, including Asana. For FY 2024, Asana expects revenues of $638.0 million to $648.0 million, which is merely a 17% - 18% YoY growth, bleak in comparison to FY 2023.

Up until today, Asana has also done well in maintaining and expanding gross margins. Q4 Non-GAAP gross margin of 90.5% was impressive and is already an ideal figure for a target model. Overall, this has been an area where Asana historically tends to do well, since gross margin has consistently trended upward from 81%+ since 2019 to 90%+ today, with little regard towards macro issues.

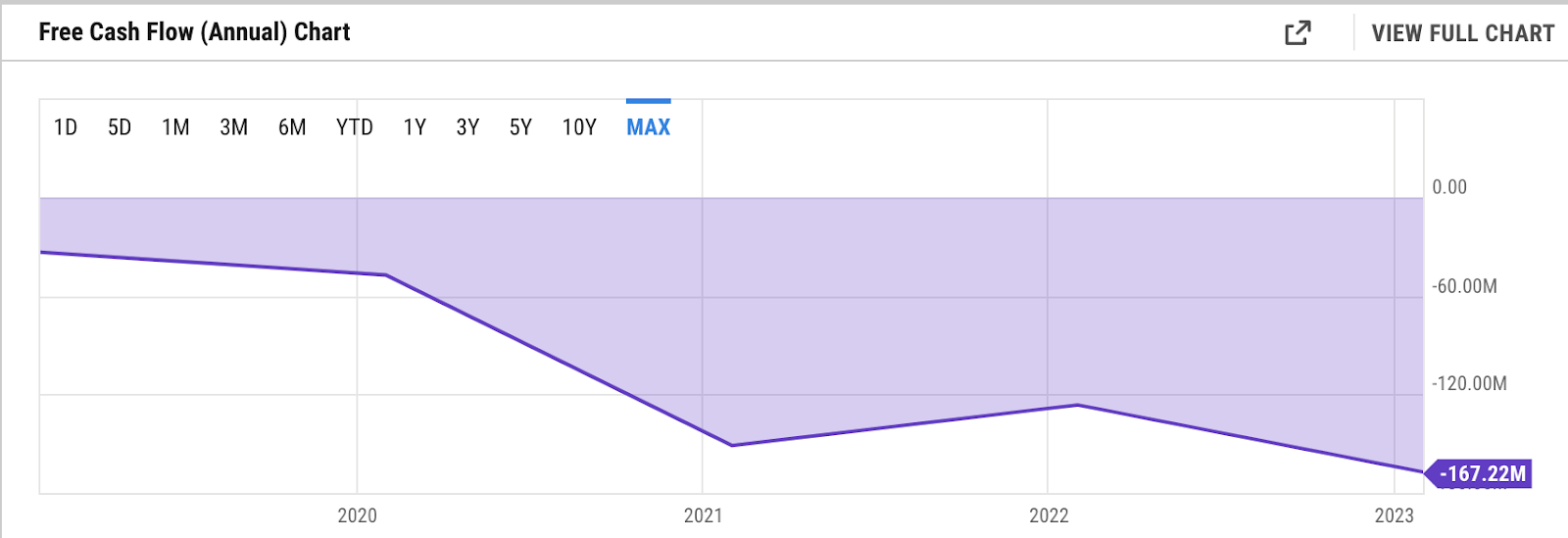

The outlook on operating profitability and cash flow generation is a little different and has been subject to scrutiny.

{kind=link}

Overall, FCF burn has increased significantly since 2020 as the company made a series of large investments primarily into Sales and Marketing / S&M every year, which has also widened net losses gradually over the same period.

{kind=link}

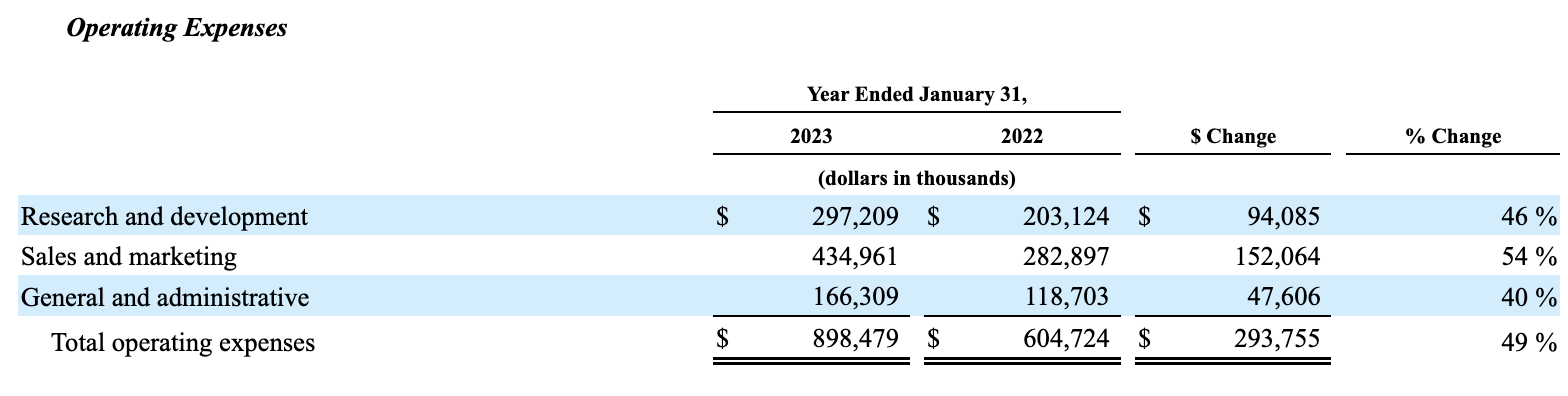

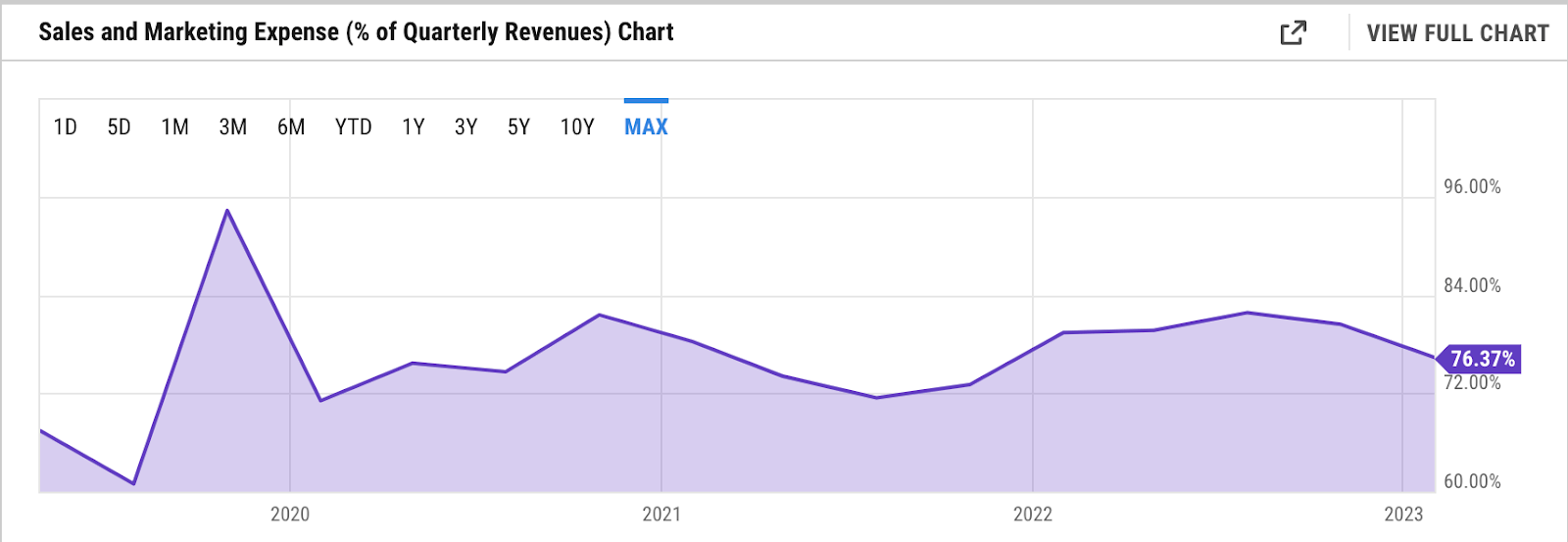

The warning shots fired by the critics are justifiable. Over the past few years, Asana has been aggressively spending roughly 75% - 80%+ of its revenue towards S&M every quarter as it expects to strengthen its enterprise go-to-market. S&M spending even reached 90% of revenue pre-pandemic. In fact, S&M has been the single expense item that has grown much higher (50%+ annually) than the rest.

YCharts - S&M as % of revenue ASAN

{kind=link}

As I am considering the other side of the views as part of my bullish call, there are two key counterarguments to the critics. First, given the importance of enterprise expansion, S&M enhancements are necessary. What I however expect to see is a gradual downtrend of S&M as % of revenue over time to demonstrate economies of scale, as highlighted by the CFO, Tim Wan, in the Q4 earnings call:

Yes. I think R&D as a percent of revenue will be relatively flat. And I wouldn't say sales and marketing is a cut. I think the way to think about it is really a reallocation of where those resources were in prior years or even last year where we're still focused kind of on the SMB and where we direct in many of those resources towards moving upmarket.

So I think you'll continue to see leverage like you saw this past this last quarter in sales and marketing, and you'll continue to see leverage in G&A. And then I would expect R&D to be relatively flat on a year-over-year basis.

Historically, as the company intended, I have seen S&M as % of revenue dropping in certain quarters over the last few years typically after a peak quarterly S&M spend. These downtrends, however, have not been consistent. While I feel that the macro issues also played a part in it, the figure will likely trend much better in the next 18 months under the newly-appointed leaderships overseeing S&M. In Q4, Asana brought in a new CMO, new head of customer experience, and announced that they are hiring a new CRO.

Finally, Asana has demonstrated an ability to take a pragmatic approach to improve cost structure. I think the 9% of global workforce cut was bold for a company championing modern work culture like Asana. While details aside from the $9.3 million one-time incurrence towards severance and benefits were not disclosed, I expect that the S&M headcount might have a significant share in the cut, given Asana's desire to refocus towards higher-tier geographies where enterprise deals are more abundant. In turn, this will further positively affect S&M spend.

The X Factor

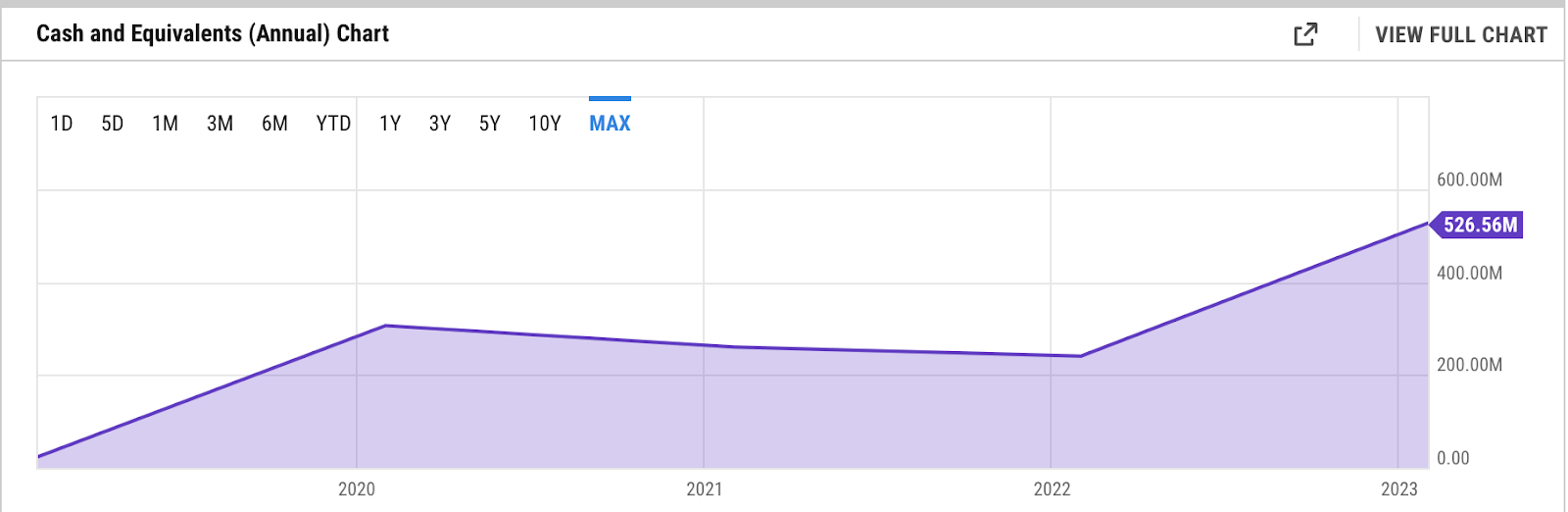

No one else in Asana's management team deserves the most discussion other than its co-founding CEO Dustin Moskovitz / DM, who since 2021 has personally made over $1 billion worth of share purchases in private placement transactions. The accumulated figure is also to increase further as per his announcement to do another share purchase during the Q4 earnings call.

YCharts - cash and equivalents ASAN

{kind=link}

Given Asana's historically negative operating cash flows, DM's share purchases have significantly improved the company's balance sheet with fresh cash injections. Asana's FY 2023 ending cash balance of $526 million, for instance, was made up primarily of the $350 million worth of share purchase by DM in late 2022 . Without the share purchase, Asana would have finished the year with less than $200 million in cash.

A multi-billion dollar CEO funding his own venture is not unprecedented, but given the stage of Asana, it was truly something unexpected at the time of my earlier evaluation at pre-IPO. It is safe to say that my view on Asana today may have weighted more towards the other side in absence of this X factor.

Valuation

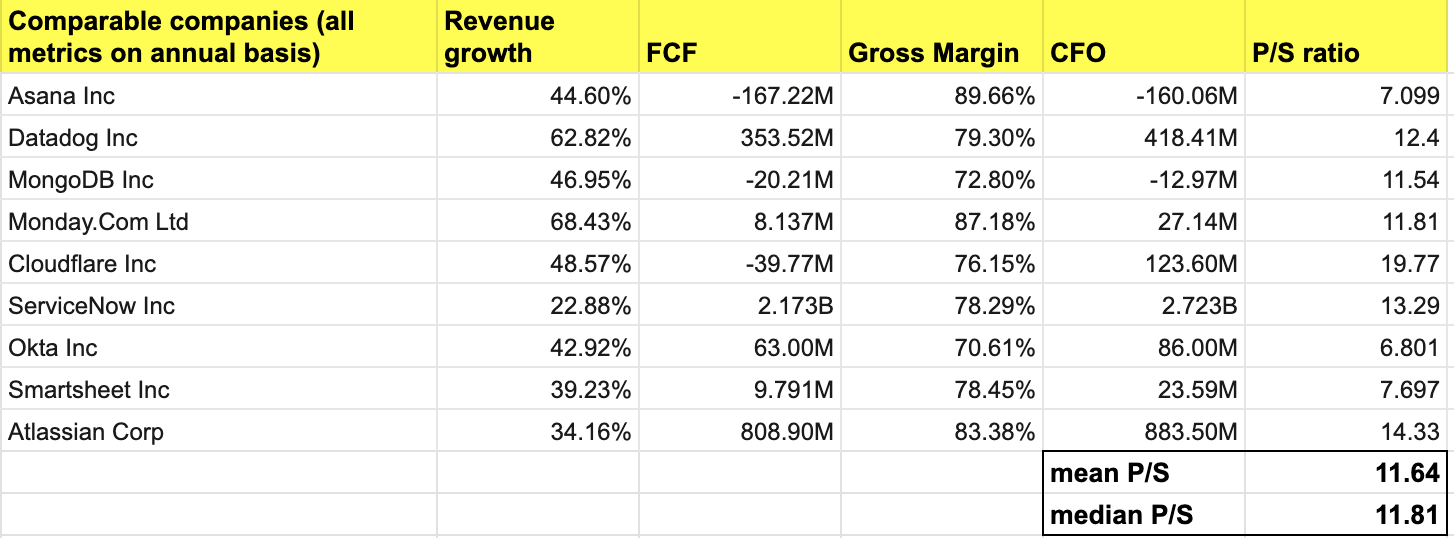

In setting the FY 2028 price target, I estimated the forward P/S for Asana based on the median P/S of cloud software stocks with similar characteristics in at least one or more parameters such as go-to-market, target segment, and services.

ASAN comparable companies - author's own analysis

{kind=link}

Many of the stocks in this universe maintain positive FCF, CF from operations, 70 - 90 % gross margins, and also have annual revenue growth rate roughly between 35% - 60% (except for ServiceNow). In general, these are the ideal financial characteristics I expect Asana to possess in FY 2028, and as such, they serve as the basis of selection for the comparable universe.

I ended up with a median forward P/S of 11.81. Interestingly, this is the P/S of Monday.com, which is the direct competitor of Asana. Monday.com has very strong numbers across different parameters, and can certainly represent an ideal target model for Asana. Moreover, with 68.4% revenue growth and positive FCF and CFO in FY 2023, Monday.com's score of 70 in the rule of 40 is highly impressive.

In my bullish scenario, I expect Asana to reaccelerate annual revenue growth to 30%+ starting in FY 2025, to reach 40%+ growth in FY 2027, and to finish FY 2028 with 50%+. I assigned a slower revenue growth rate than Monday.com's to account for the significant difference in market cap. In this scenario, Asana has a $29+ billion market cap in FY 2028, over 4x the size of Monday.com today. I would also expect Asana to have at least a high single-digit FCF or CFO margin, which should put Asana's rule of 40 comfortably above 50+.

Applying the current Monday.com P/S of 11.81 to FY 2028 revenue of $2.4 billion with ~30% share dilution since FY 2024, I arrived at an FY 2028 target price of $104 per share.

From today's level, I also project the share price to appreciate by 20% a year. I think it is a fair return expectation considering the growth rate of the business. Applying that 20% yearly return as the discount rate to estimate the PV (present value) of the FY 2028 price, I arrived at a PV price per share of ~$42.

It simply means that ~$42 is the highest price level to initiate a long position to earn at least a 20% yearly return until FY 2028, where the target price of $104 will be observed under our bullish scenario.

The projection suggests that Asana is an attractive buy today. At ~$18 per share today, it trades at ~57% discount to that ~$42 maximum entry point.

Risk Factors

As per the Q4 deep-dive in the prior section, Asana's ongoing sizable S&M spend will continue to be a noteworthy risk factor. Despite my optimistic view that it should decrease as % of revenue under the new leadership, it will take time for new executives and enterprise S&M hires to ramp up into full productivity.

As such, there is little room for execution-related mistakes, which will lengthen the payback period and put further pressure on profitability, cash flows, and ultimately share price.

Asana's strong growth has also not been followed by strong cash flow generation from its core operation. It has been relying much more on cash flows from financing than operating activities, a big part of which is the series of share purchases from DM, the X factor.

There is definitely a risk for Asana to over-rely on financing cash flows since it creates an impression of an unsustainable business model. The recent upmarket move is meant to target higher-sized enterprise deals that eventually will impact operating cash flows positively. Over the next 18 months, it then becomes critical for Asana to demonstrate a path to positive FCF, in absence of which, the current call should then be reassessed.

Conclusion

Asana is another growth stock that fits our thesis, given its ambition to penetrate further into the enterprise segment to secure future high-valued growth expansion opportunities. Asana's historical cash burns and losses have been subject to scrutiny. However, when seen within the context of a challenging macro situation and strategic shift towards the enterprise segment, the profitability outlook is expected to improve.

In Q4, we learned how the management was able to take a bold move to cut 9% of the workforce in an effort to improve operational efficiencies. In the end, the co-founding CEO's demonstrated long-term commitment and skin in the game through a series of share purchases also present a major sense of safety and trust for investors.

For further details see:

Asana: Enterprise Expansion And The X Factor Are Big Plusses