ASAN - Asana: Looking Forward To Where It's Going

Summary

- Asana was a bubble stock. In hindsight, this is now so obvious. The problem is that you can't invest in hindsight.

- What matters in investing is where the stock is heading, not where it's been.

- Everyone knows the key issue facing Asana that the business is highly unprofitable.

- But I don't believe investors are giving enough consideration to the fact that next year Asana will be free cash flow positive.

Investment Thesis

Asana ( ASAN ) is a company that helps teams organize and coordinate their work.

There are plenty of reasons not to consider Asana. The main reason is that the business is highly unprofitable on a GAAP basis. That being said, I wonder whether that insight isn't already being factored into its share price.

Because, believe it or not, the company is still expanding at a 30% CAGR right now. Additionally, 2023 comparables ought to get slightly easier.

Simply put, I don't believe that this is a dead company walking. There's enough to like about Asana that I do not believe that this is the time to throw in the towel.

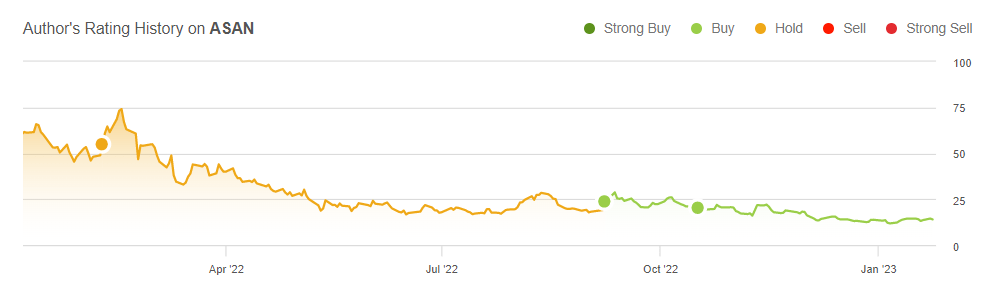

Investors Want Nothing to With ASAN

Without a doubt, Asana's stock price has declined during the previous 12 months. It underperformed not just in comparison to the overall market, but also to its peers.

In the interest of full transparency, I should add that while being neutral on the name at the beginning of the year, I became bullish on it way too early, as it turned out.

{kind=link}

However, I contend that investors are currently overly pessimistic about a company that is obviously still growing at a reasonable rate, much like how they were overly enthusiastic about this founder-led company on the way up.

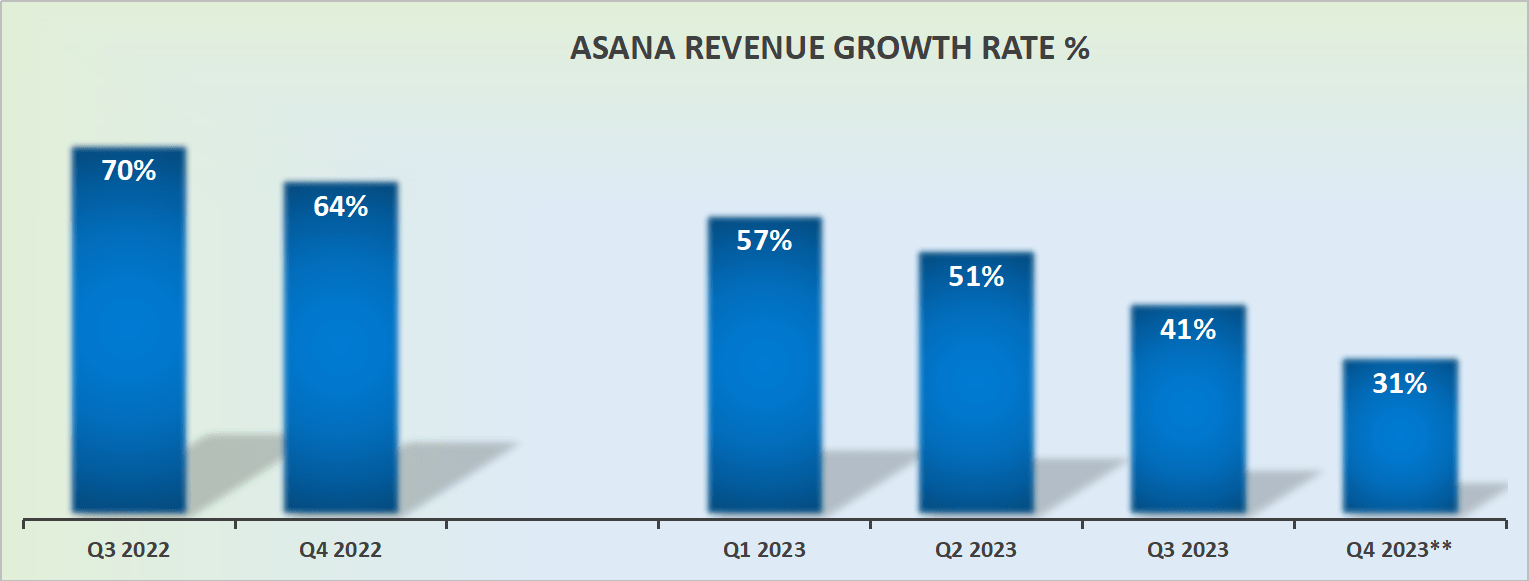

Revenue Growth Rate Slow Down, But Not So Dramatically

{kind=link}

Asana's guidance for fiscal Q4 2023, points to 31% y/y growth rates at the high end. That is despite the really high comparable with the prior year's quarter.

However, following this quarter, the remainder of fiscal 2024 (not calendar, but fiscal) should be against steadily easier comparables.

As a result, I think Asana may really end up growing at 20% to 25% CAGR in fiscal 2024, which in the current economic climate is actually rather good.

{kind=link}

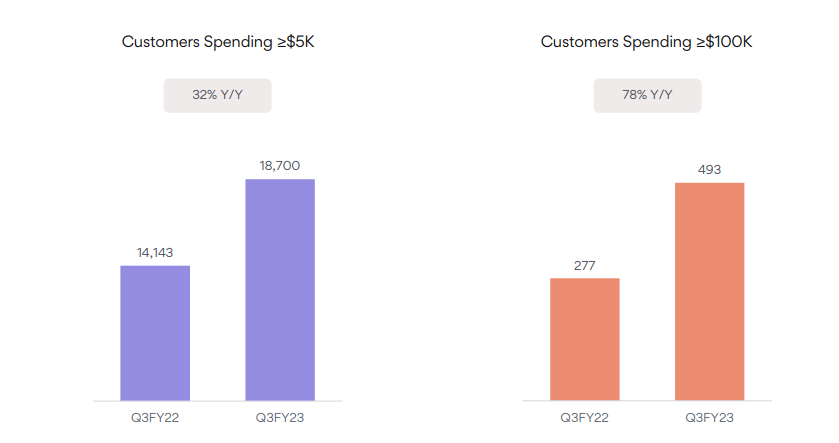

Anyone who keeps up with this company will also be aware that its growth rates are still amazingly robust amongst its larger clients. That ought to support the idea that Asana will nonetheless put up respectable financial results in spite of the present unstable business environment.

After all, this is what Asana was built for, to support large departments' project management and collaboration workflows.

With this in mind, next, we'll get to the main reason why investors are eschewing this name.

Free Cash Flow Won't Turn Positive Until 2024

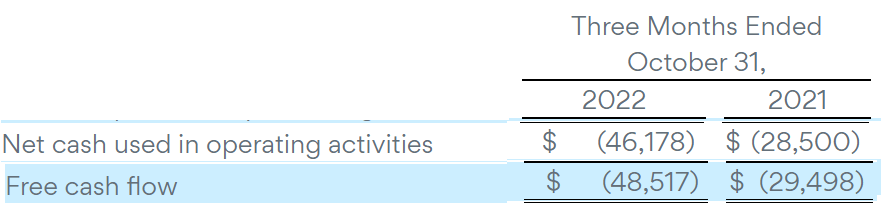

The table that follows shows Asana's free cash flow profile.

{kind=link}

The business' free cash flow is not only negative. But it appears to be moving in the wrong direction. If the purpose of a business is to make free cash flow, Asana is evidently struggling here.

For Q3 2023, its free cash flow margin was negative 34%. And yes, this figure includes Asana's stock-based compensation. Asana's SBC was up 86% y/y, growing at more than twice the rate of Asana's revenue growth rates.

Nonetheless, Asana maintains that in 12 months it will turn a page and deliver to shareholders what they so badly crave.

"Despite the uncertainty with the macroeconomic environment, we still expect to be free cash flow positive before the end of calendar 2024, while balancing growth and profitability." Q3 Earnings Call

ASAN, Challenging to Value

We all know that Asana's struggling to translate its revenues into free cash flow. We also know that paying 5x sales can be too high a premium if the business ultimately ends up reporting 1% free cash flow margins.

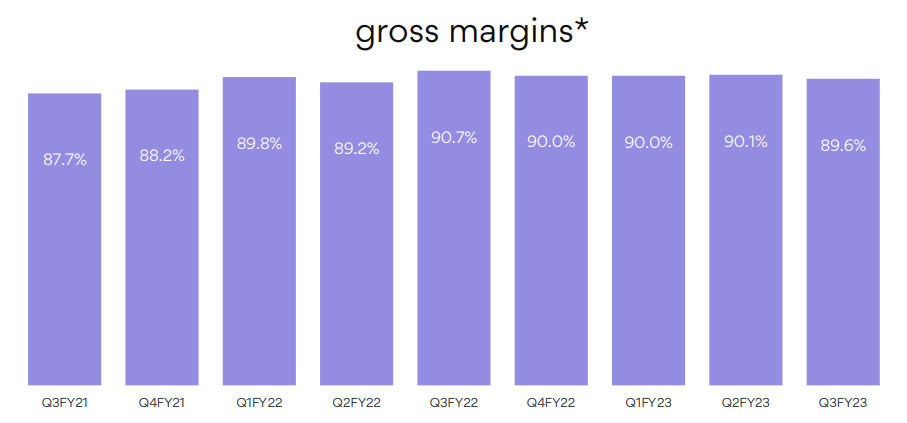

But I believe that with Asana's gross margins so high, there's plenty of room for the company to trim back some fat.

{kind=link}

Can Asana's stable free cash flow margin get to 10%? If that were the case, that would imply that Asana is priced at 42x forward free cash flow. That's not an absurd multiple.

The Bottom Line

The main question that investors need to form some view on is whether Asana can translate its very high gross margins of approximately 90% into 10% free cash flow.

The business is clearly growing, I don't believe that anyone disagrees with that premise. Hence, if Asana's free cash flow line stops hemorrhaging and convinces investors that it can get to 10% free cash flow in the coming few years, it's dead money for a while longer, but it's not a dead cause.

For further details see:

Asana: Looking Forward To Where It's Going