ASAN - Asana: No Reason Not To Buy

2023-10-02 01:13:08 ET

Summary

- Asana, a workflow and collaboration software vendor, remains undervalued despite a 40% year-to-date increase in stock price.

- CEO Dustin Moskovitz's continual insider purchases signal management's confidence in Asana's direction.

- Upside catalysts for Asana include the ongoing shift to remote and distributed teams, a massive global TAM, star leadership, and a high gross margin profile.

- The company is passing the one-year anniversary of when seat expansion slowed last year, creating easy comps if macro conditions improve.

- The stock trades at a cheap <5x FY24 revenue multiple.

In general, like most investors, I've been substantially increasing my exposure to cash this year as interest rates have risen. It doesn't make much sense to buy into stocks at a premium valuation multiple when earnings yields offer such a low premium versus risk-free rates.

I'll make an exception, however, for growth stocks that have seen sharp recent dips despite excellent fundamentals, and Asana ( ASAN ) is a great example here. The workflow and collaboration software vendor still remains up ~40% year to date, but in my view, given its premium growth profile and rapid progress in margins, I think the stock remains substantially undervalued.

Also of note: CEO Dustin Moskovitz, a former Facebook ( META ) co-founder, keeps buying up shares . Though many market-watchers have attributed Moskovitz's continual purchases as a signal of a committed founder who is willing to "go down with the ship," I think it's a positive signal of management's confidence in Asana's direction.

I remain bullish on Asana and continue to recommend buying the stock on dips. I last wrote on Asana in July when the stock was trading north of $20; since then, not only has valuation substantially improved, but the company has also exceeded relatively modest growth targets and raised the low end of its guidance range for the year.

To me, the long-term bull case for Asana remains very much intact. As a reminder to investors who are newer to this stock, here is my updated rundown of upside catalysts for Asana:

- Asana's long-term demand will be bolstered by the ongoing shift to remote and distributed teams. More and more companies are embracing a distributed working model, if not a fully remote one. With fewer in-person touchpoints, software tools become critical to keeping teams together and in sync.

- Massive global TAM. Asana believes it has a $51 billion TAM by 2025 and is applicable to the global base of ~1.25 billion information workers. By that metric, Asana's current user base represents only <5% of the global eligible workforce.

- Star leadership and insider buying. Asana continues to be led by its founder Dustin Moskovitz, who keeps buying shares as the stock dips.

- Land and expand. Asana adopts the classic software go-to-market playbook, which is to prove its concept and value with smaller teams at first, but eventually expand to entire organizations and companies. Dollar-based net retention rates are clocking in above 140% for companies spending more than $100,000 annually on Asana, a leading indicator that Asana's traction among larger enterprises is growing.

- Huge gross margin profile. Asana's pro forma gross margins are in the ~90% range, making it one of the highest-margin software companies in the market. While the company isn't profitable today, that gross margin profile gives Asana plenty of leeway to scale profitably when it's larger, as nearly every dollar of incremental revenue flows through to the bottom line.

Stay long here and join Moskovitz in buying shares on the dip.

Q2 download

One of the core things to note about Asana is that while it was previously known for being monstrously unprofitable, the company has leveraged both the natural scale inherent in its high gross margin profile plus expense discipline to drive substantial bottom-line progress this year.

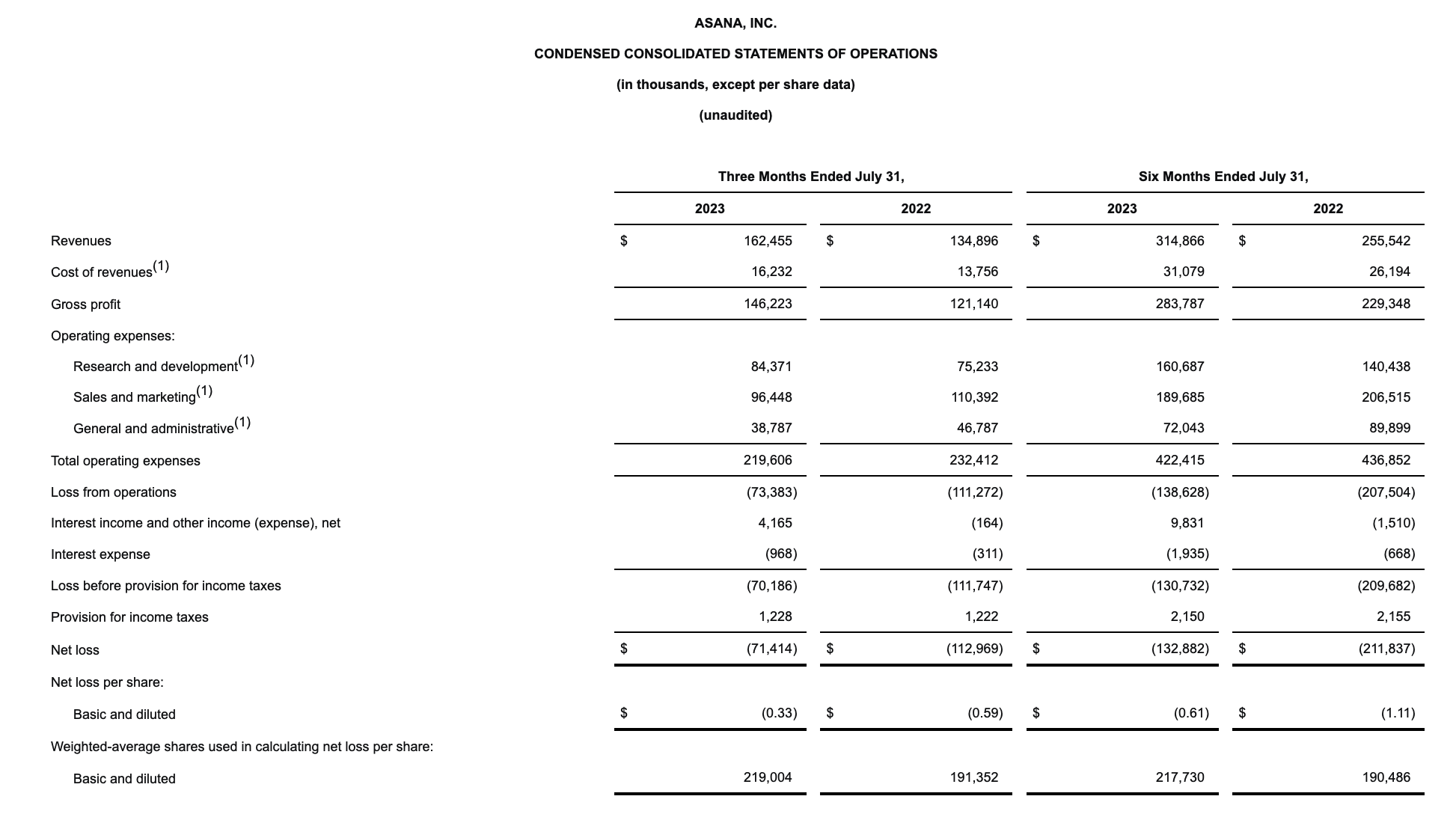

The most recent Q2 earnings release is shown in the chart below:

{kind=link}

Asana's revenue grew 20% y/y in the second quarter to $162.5 million. Though this decelerated six points versus Q1's 26% y/y growth rate, the company beat Wall Street's expectations of $157.8 million (+17% y/y) by a respectable three-point margin.

The macro trends weighing on Asana are widespread, not company-specific. As a seat-based subscription software company, the company is impacted as its customers reduce headcount and slim down expenses. And on the new deal front, enterprise budgets are being subjected to much tighter scrutiny, slowing down deal progress.

In spite of this, management believes Asana is seeing stabilizing ground. Per Moskovitz's prepared remarks on the Q2 earnings call:

Even with continued macro headwinds and heightened budget scrutiny in the enterprise, sentiment seems to be stabilizing. Customers are looking for ways to consolidate their vendors, getting more ROI out of everything they’re doing, and they’re turning to Asana. Asana can help to achieve their goals and objectives more efficiently and faster than ever before. In fact, we have seen an increase in multi-year commitments both year over year and sequentially, in the quarter [...]

In the first-half of the year, we have been working through the macro headwinds, and we continue to focus on our enterprise playbook, improving sales execution, and building substantial enterprise leadership, most recently announcing the arrival of our new Chief Revenue Officer, Ed McDonnell."

COO Anne Raimondi additionally added that in spite of broad-based headwinds, Asana has noticed a number of situations in which customers are consolidating their software spend and choosing to retain Asana, eliminating competitors in the process.

She also added that the company is passing the one-year mark of when seat expansions started to dramatically slow last year, impacting net retention rate trends. If headcount and seat trends begin to rebound, this will provide an easy comp and a fantastic growth driver going forward.

Margins are the core area in which Asana excelled this quarter. Importantly, the company sliced down sales and marketing expenses as a percentage of revenue to 49%, down 21 points from 70% in the year-ago Q2. On a nominal basis, sales and marketing expense fell -16% y/y to $79.6 million, excluding stock-based comp: indicating a prudent management team conscious of using a time of slower growth to review its operating structure.

Combined with solid 90% pro forma gross margins, Asana was able to deliver a pro forma operating margin of -6.4%, a 40-point improvement versus -46.4% in the year-ago Q2.

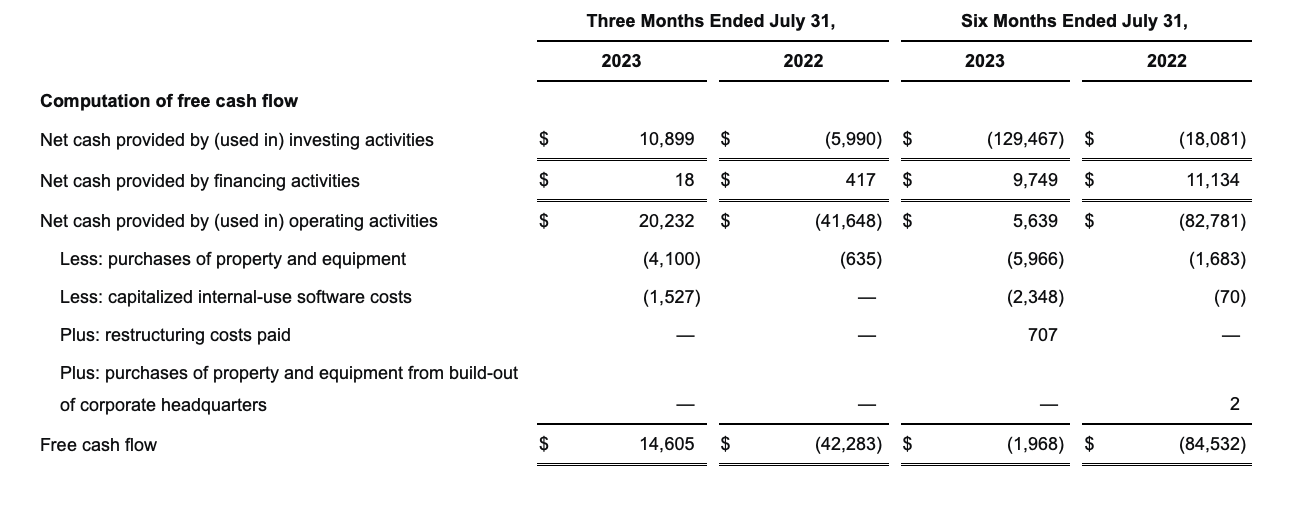

Note as well that YTD free cash flow burn has slimmed down to an essentially breakeven -$2 million, versus an -$82 million burn in the year-ago quarter.

{kind=link}

With over $500 million of cash on its balance sheet, and with minimal debt, we have no concerns about Asana's ability to navigate through the current macro downturn and get to the point of expanding seats again.

Valuation and key takeaways

At current share prices near $18, Asana trades at a market cap of $4.02 billion. After we net off the $537.5 million of cash and $45.5 million of debt on Asana's most recent balance sheet, the company's resulting enterprise value is $3.53 billion.

Meanwhile, for the next fiscal year FY24, Wall Street analysts are expecting Asana to generate $733.3 million in revenue, representing 13% y/y growth. Considering Asana's current growth rates are clocking in at 20% y/y and the easier comps versus this year's lack of seat expansion and tougher enterprise deal cycles, it's likely that this consensus estimate is highly conservative. Nevertheless, even taking consensus at face value, Asana's valuation stands at just 4.8x EV/FY24 revenue - quite cheap for 20% growth, 90% gross margins, and rapidly scaling profitability.

All in all, there's a lot to like about Asana from insider purchases, substantial margin gains, a large TAM, and a path to renewed sales growth. Take advantage of the dip here to buy.

For further details see:

Asana: No Reason Not To Buy