ASAN - Asana: Positive Signals But No Reason To Own Yet

2023-08-31 11:24:21 ET

Summary

- Asana stock is down almost 90% from its all-time highs.

- Positive signals include trajectory towards profitability, AI investments, and strong customer retention.

- However, growth patterns show moderation, profitability is too distant in the future, and the AI offering is not yet too compelling.

- With a 2026 P/E ratio of about 70, the stock does not present an opportunity for investment.

Asana ( ASAN ) stock has seen its ups and downs in the last years and is now almost 90% down from its all-time highs.

There are certain positive signals that could potentially encourage existing investors. Asana's trajectory towards profitability gained some momentum in the recent quarter, coupled with strategic AI investments and a commendable record of customer retention. Furthermore, the company showcases a robust balance sheet, being nearly debt-free and having substantial cash reserves.

However, a closer examination unveils certain nuances. Notably, growth patterns show signs of moderation, which raises questions about the potential trajectory of its sales. Additionally, while Asana's AI product shows promise, it doesn't appear to be a revolutionary game-changer that would lead to expansive growth like in the case of Nvidia ( NVDA ). The company is also not even close to profitability, and given its current trajectory, justifying the current valuation seems almost implausible.

The good: Asana displays some promising signals

To start with, we need to acknowledge and appreciate certain developments that indicate Asana does progress towards a better future and might exhibit a turnaround at some point.

First of all, the company has exceptionally strong customer retention. Hence, in the quarter ended in April, Asana had a dollar-based net retention rate (DBNRR) of over 115% among customers with more than $5,000 in annualized spend and over 130% among those with more than $100,000 in annualized spend.

The company's ability to consistently retain its customer base showcases its ability to actually deliver value to the users and maintain customer satisfaction. This strength not only establishes a steady revenue stream but also underscores Asana's advantage in a market where customer loyalty is a crucial metric of success. To elaborate, a DBNRR exceeding 100% signifies that Asana can sustain revenue growth even without attracting new customers. And the recurring nature of the company's SaaS sales suggests that Asana could (potentially) swiftly enhance its margins by prioritizing profitability (gross margins are about 90%).

Dollar-Based Net Retention Rate (Asana FQ1 earnings presentation)

{kind=link}

This brings us to the second point: profitability. The company still burns money, but there are some signs indicating Asana is very slowly moving towards profitability. In FQ1 2024, despite a 26% increase in sales, the company managed to slightly reduce its operating expenses from $204,440 to $202,809 compared to a year ago. As a result, loss per share improved drastically, shifting from negative $0.52 the previous year to negative $0.28 in the April quarter. This improvement is indeed significant and represents a necessary step forward.

Thirdly, Asana has a relatively secure balance sheet. The company boasts a robust cash reserve of more than $520 million (incl. marketable securities) and maintains a low long-term debt burden of about $46 million. This financial foundation not only enhances Asana's capacity to weather market fluctuations but also positions it favorably for strategic growth initiatives, like AI.

Indeed, Asana has recently announced new AI-focused ventures, which can make the product more attractive for the enterprise customers. These include improved executive reporting, streamlined goal standardization, the capacity to plan projects with clear data visualization, and more. The AI features promise to help companies automate work and improve collaboration, thus directly contributing to clients' profit margins. Therefore, AI can become Asana's selling point that would convince new customers to try the product.

The bad: the valuation is almost impossible to justify

Despite the positive points outlined above, it is still hard to recommend ASAN as a buy.

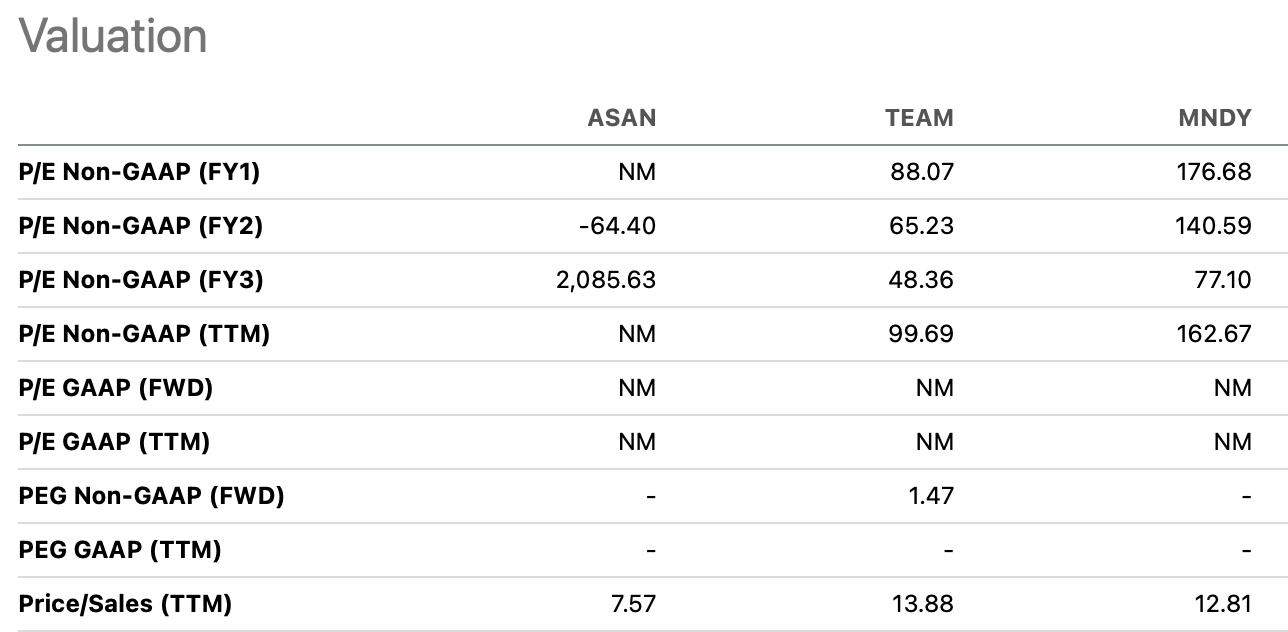

Firstly, Asana's revenue expansion shows clear signs of a slowdown, as the quarterly sales growth rate has been declining over the last 2 years. A similar trend is observable in the case of Asana's primary competitor, monday.com ( MNDY ), albeit with the latter exhibiting a growth rate nearly twice as high. Another competitor, Atlassian ( TEAM ), does not exhibit this evident decline in revenue growth.

This development might well continue into the future, as corporations are less willing to spend money on additional software and services amidst the prevailing economic uncertainty.

Secondly, despite ongoing efforts to reach profitability, Asana continues to incur substantial operating losses each quarter, with approximately $65 million in losses reported in FQ1 2024. Adding to this concern, EPS projections suggest that Asana will not attain profitability until late 2026. Even then, the company's valuation is based on an over 70 P/E ratio for 2026 EPS, a figure that becomes increasingly difficult to rationalize considering the backdrop of a decelerating growth rate. With this valuation, Asana looks significantly worse than any of its competitors.

{kind=link}

Additionally, the role of AI within Asana's offerings presents a nuanced perspective. Although AI-driven features are likely to provide valuable improvements for existing customers, the notion of AI dramatically increasing productivity to unprecedented levels remains uncertain - it is simply not a game-changer for the company's offering yet.

Moreover, Asana's AI application relies heavily on the high quality of data and tracking within clients' businesses. Drawing from my seven-year experience as a data analyst, such optimal conditions are almost never observed. Therefore, as of now, AI may not serve as a primary selling point, given the absence of compelling evidence for a revolutionary leap in productivity outcomes.

Key takeaway: there is no compelling reason to buy ASAN, though this may change in the future

Asana's recent trajectory towards profitability, strategic AI investments, and strong customer retention provide positive signals for existing investors. The company's robust balance sheet enhances its strategic position and reduces the risks of going out of business any time soon.

Although the positive aspects mentioned earlier are notable, recommending ASAN as a buy remains challenging. Growth moderation, uncertainties about the transformative potential of AI, and the prolonged path to profitability suggest caution. If the current EPS projections hold true, ASAN is now valued at approximately 70 P/E ratio for 2026 EPS. With this valuation, investors are better off taking a stake in one of the competitors.

While Asana faces challenges, it still worth noting that the current situation might evolve in some distant future, making it a somewhat intriguing stock to monitor over time.

For further details see:

Asana: Positive Signals, But No Reason To Own Yet