ASAN - Asana Q4 FY2023 Preview: Will Wednesday's Earnings Report Sink ASAN's Red-Hot Stock?

2023-03-07 11:43:17 ET

Summary

- After staging a ~50% rally off of its all-time lows in early January, Asana is going into its Q4 FY2023 earnings report with some solid momentum in the stock.

- However, based on recent performance, macro headwinds, and management's lukewarm guidance for Q4, I don't expect to see any fireworks from Asana this quarter.

- While macro headwinds are likely to remain persistent, peer earnings give hope for an earnings beat. Overall, I am nervous and excited to read management's commentary and outlook for 2023.

- From a long-term perspective, Asana looks undervalued by ~30%, and investors buying here could generate 25% CAGR returns here over the next five years.

- Hence, I continue to rate Asana a "Strong Buy" at $17, with a strong preference for staggered accumulation.

Introduction

In its relatively short trading history as a public company, Asana ( ASAN ) has undergone an entire boom-bust cycle - a big liquidity-fueled boom in 2020-21 followed by an epic bust in 2022. Having IPO'd at $21 per share, ASAN headed to the mid-teens in a matter of weeks. Thereafter, a tremendous amount of hype drove investors into chasing Asana's robust growth in 2020-21 (like most other high-growth tech names). In November 2021, Asana's stock peaked at $145.79 (~90x EV/S) right around the time of the Fed's pivot to Quantitative Tightening. As I see it, the Fed's pivot to a tighter monetary policy regime pricked the bubble in Asana.

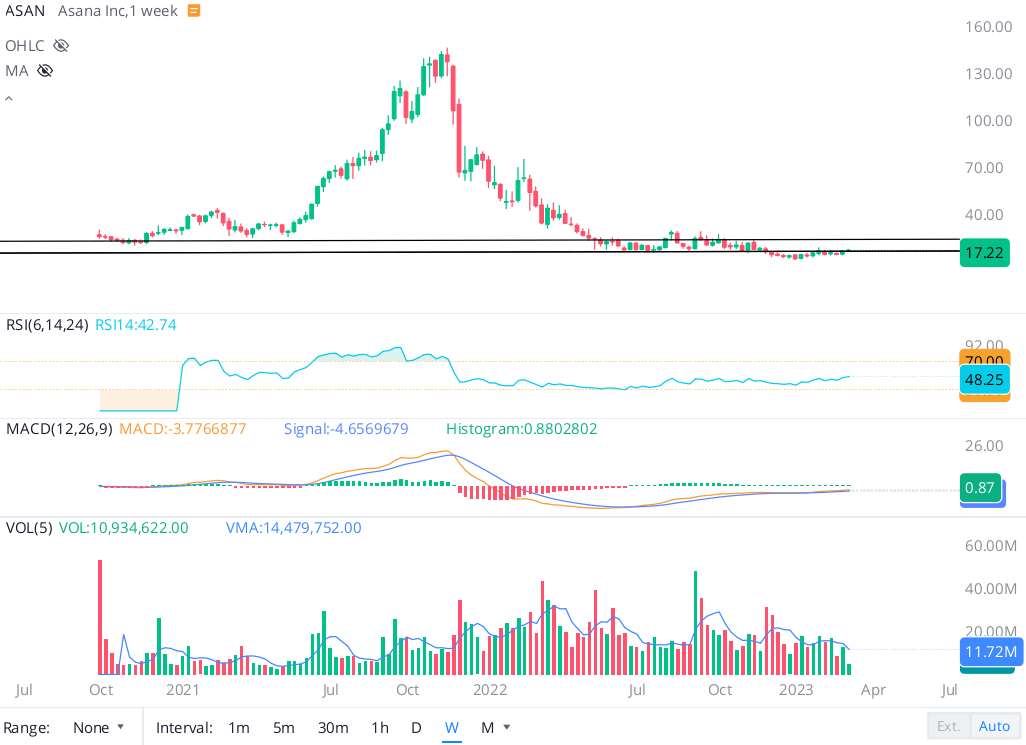

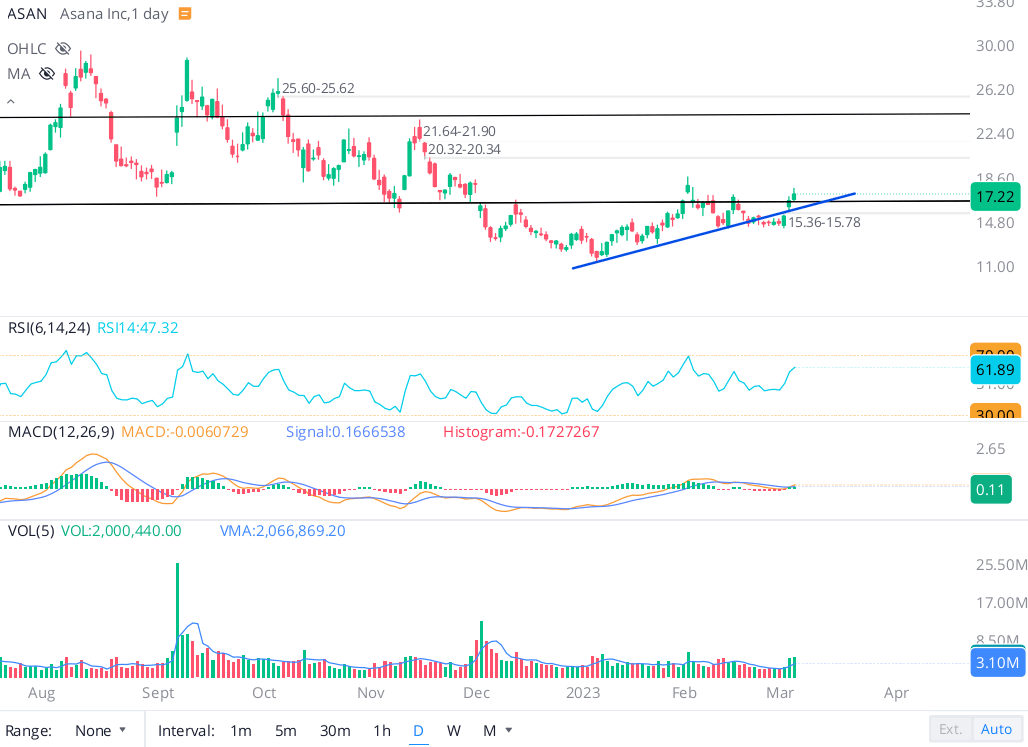

After experiencing a vicious sell-off, Asana's stock is back to where it started its journey as a public company, and it has been showing some signs of stabilization in a tight range around its IPO price. Since May 2022, ASAN's stock has been forming a Stage-1 base pattern in the range of $16-$26 per share as seen below:

{kind=link}

In early January, Asana hit an all-time low of $11.32 per share; however, a ~50% jump in the stock has carried ASAN back into the Stage-I base. As you can observe on the chart, Asana's stock has established a bullish channel pattern in recent weeks with a series of higher highs and higher lows (marked in blue on the chart below).

{kind=link}

With Asana having re-entered the Stage-I base pattern (currently trading near the lower end of this base), I think Asana could be a solid contrarian bet for long-term investors willing to hold for 3-5+ years. However, Asana's Q4 earnings report could yet throw a spanner in the works, and in my view, a breakdown of the $15-$16 levels could be extremely negative for the stock.

On the other hand, a positive report tomorrow could enable an extension of the rally in ASAN, and a near-term re-test of the top end of Asana's Stage-I base at ~$26 shouldn't be written off.

In this note, I will provide a preview of Asana's Q4 FY2023 report and share my rationale for investing in ASAN at the current levels. However, let's start our discussion with a brief review of Asana's Q3 FY2023 results.

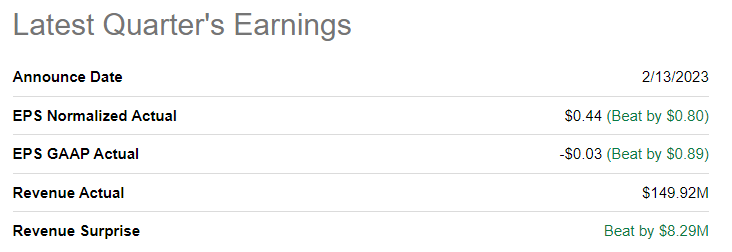

How Was ASAN's Previous Earnings Report?

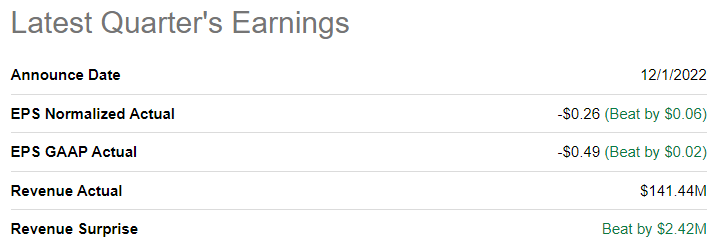

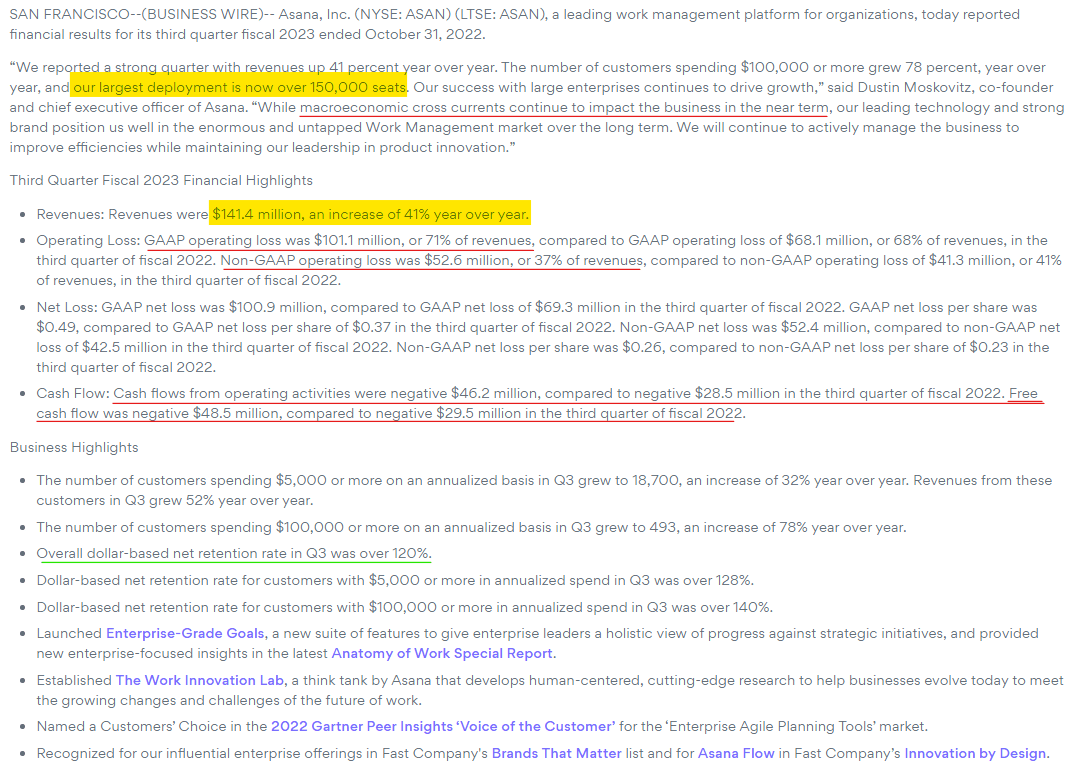

In Q3 FY2023, Asana delivered marginal beats on both top and bottom-line estimates; however, a challenging macroeconomic environment continued to haunt the work management software company with growth decelerating further during the quarter.

{kind=link}

Throughout 2022, Asana's revenue growth rates have been decelerating, and this trend continued in Q3, with revenue growth slowing down to 41% y/y. While Asana's net retention rates are still robust at >120, a challenging macroeconomic environment is taking its toll on Asana's business.

{kind=link}

A revenue growth slowdown in this environment is acceptable, but Asana's margin profile is just terrible (GAAP operating margins of -71%). Even if we remove SBC spend of 30% of revenue, Asana is a highly unprofitable business entity. In Q3 FY2023, Asana reported a negative FCF of -$48M, and I think it is fair to view Asana as a cash-burning furnace at this time.

Fortunately, Dustin Moskovitz (Asana's Founder and CEO) has shown a willingness to put his money where his mouth is in terms of financing Asana until it gets to FCF breakeven:

According to Dustin Moskovitz [CEO], Asana is still set to reach breakeven free cash flows by the end of 2024, and he re-iterated this stance in the latest earnings conference call:

{kind=link}

Since Asana currently has a net cash position of ~$550M, I see no immediate liquidity concerns here (despite Asana burning ~$50M per quarter). Now, let's look at what to expect from Asana's upcoming report.

What Is The Earnings Forecast For Asana?

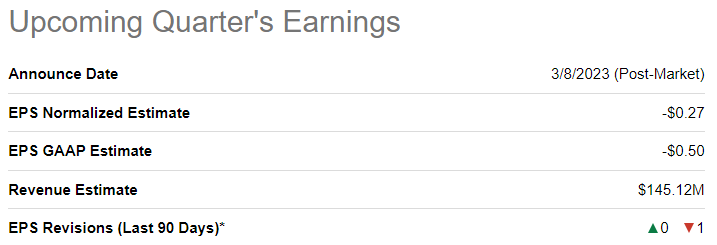

As you may already know, Asana is all set to report quarterly earnings in post-market hours on Wednesday, March 8, 2023.

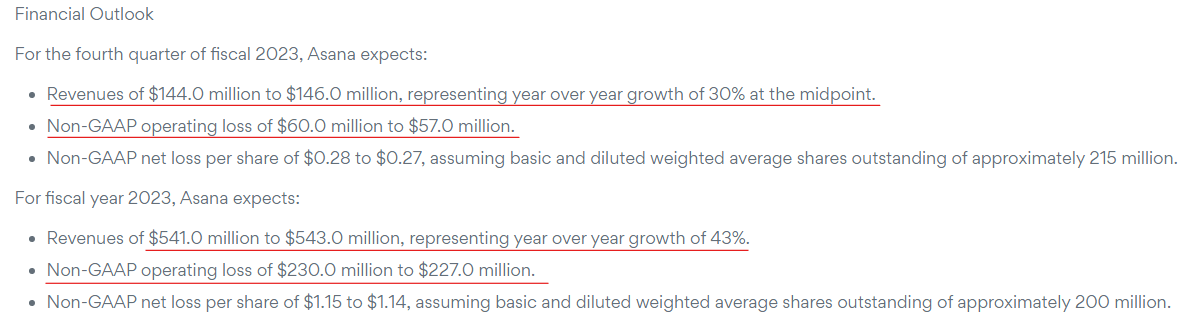

For Q4 FY2023, Asana's management has guided for revenues of $144-$146M (growth of ~30% y/y at the midpoint of the guidance range), which marks further deceleration in revenue growth.

{kind=link}

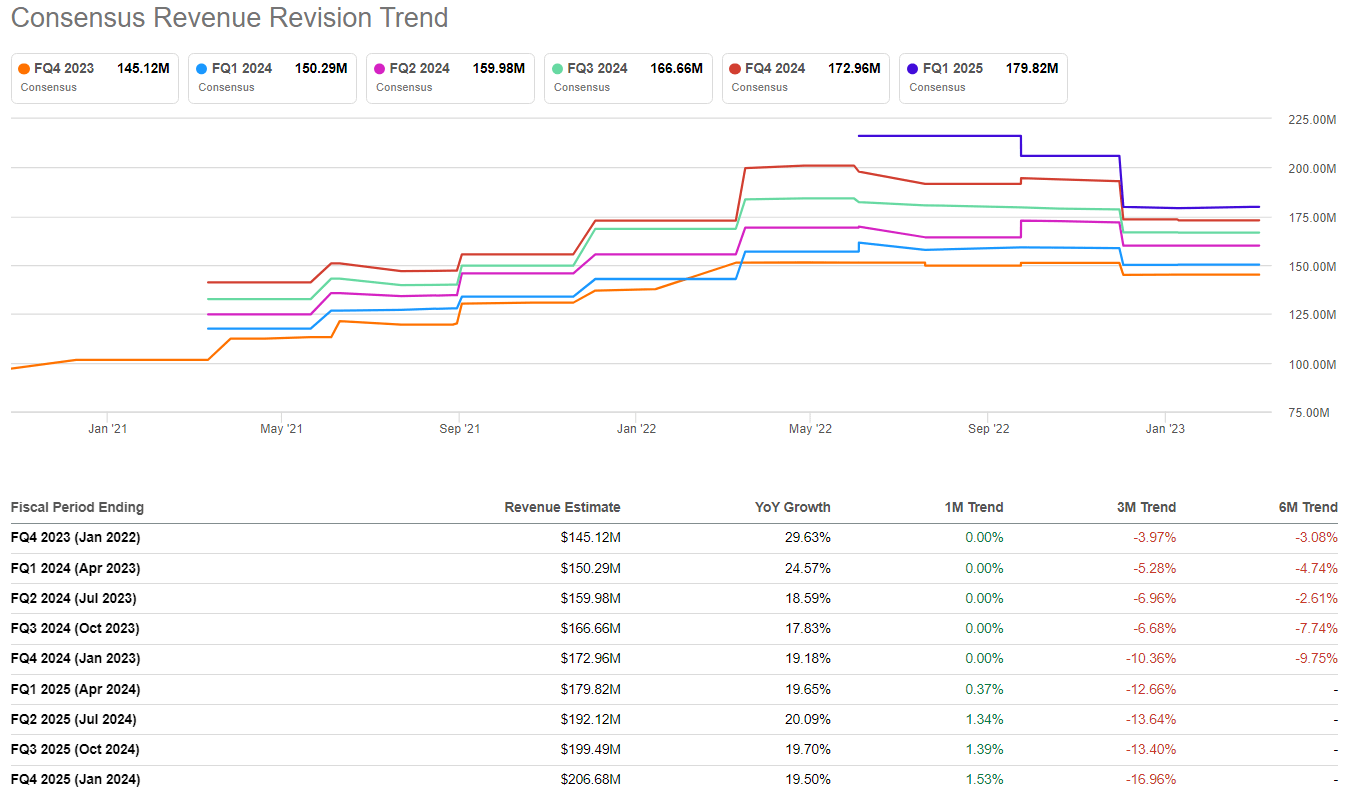

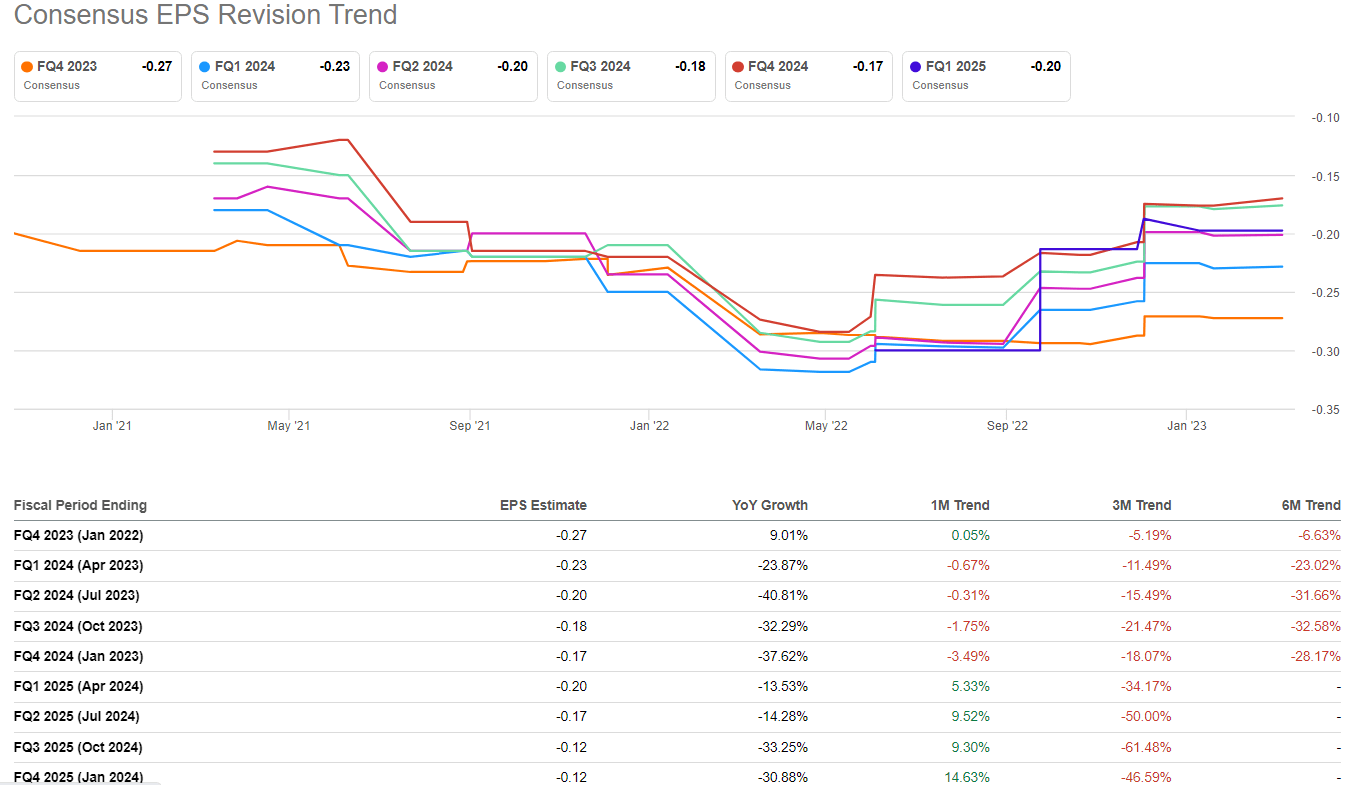

Now, this sales guide was a real shocker to investors at the time of its release as it fell well short of consensus analyst estimates going into Q3 FY2023. Since then, analysts have revised Asana's revenue and earnings estimates lower as you can see in the charts below:

{kind=link}

{kind=link}

Going into Q4 FY2023, consensus analyst estimates for Asana's Q4 report now stand at -

- Revenue: $145.12M (vs. management's guidance of $144-$146M)

- Normalized EPS: -$0.27 (vs. management's guidance of -$0.28 to -$0.27)

{kind=link}

Clearly, Wall Street analysts are not optimistic about Asana beating management's guidance in Q4 FY2023.

The revenue growth slowdown is concerning, but there's not a lot Asana's management could do about the macro environment and ~30% growth is nothing to sneeze at. That said, with growth slowing down drastically, I do hope to see Asana's management driving improvements on the margin front in tomorrow's report.

Can Asana Beat Earnings Expectations?

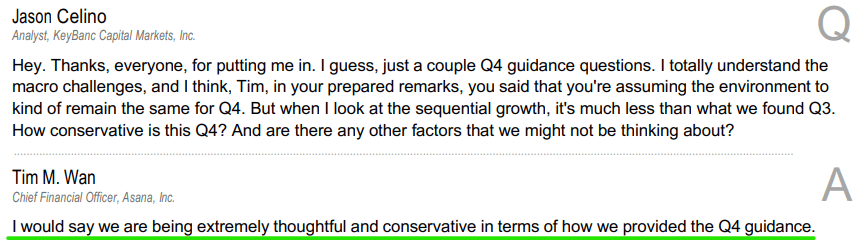

As we noted earlier, consensus analyst estimates have moved lower to end up in line with management's guidance for Q4 FY2023; however, Asana's CFO, Tim Wan, explicitly stated during their Q3 earnings conference call that their guidance is conservative (a weak macro environment is baked in here).

{kind=link}

Now, as you may know, we own a basket of work management software names that includes monday.com ( MNDY ), Smartsheet ( SMAR ), and Asana. Of these, I have preferred to buy Monday in recent months due to far superior financial performance as shared here - monday.com Stock Is No Dot Bomb

And for Q4 FY2023, Monday delivered a stunning beat on both top and bottom lines, whilst also providing a robust outlook for Q1 and FY2024:

{kind=link}

In recent quarters, Monday has maintained its business momentum far better than its peers. However, with Monday fighting against the same macro headwinds as Asana, I believe that Monday's outperformance is a good sign for Asana's end-market demand. And this is why I wouldn't rule out the possibility of an earnings beat from Asana. As I see it, Asana could easily deliver yet another marginal earnings beat for Q4 due to sandbagging from management. That said, I don't expect any massive fireworks from Asana this quarter, and to be conservative with my valuation, I have modeled Asana with a Q4 revenue of $145M.

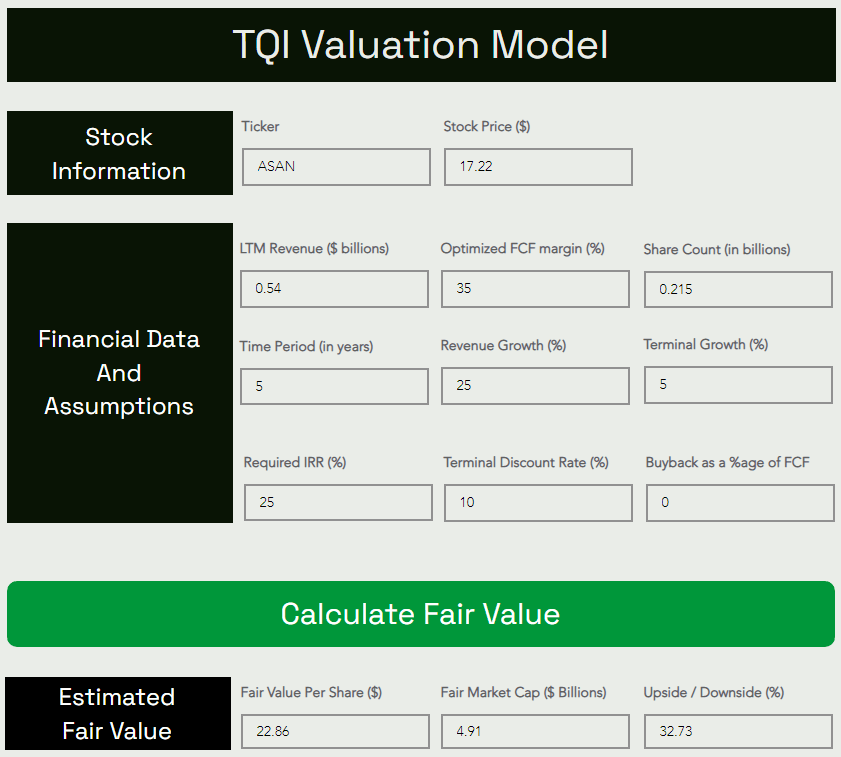

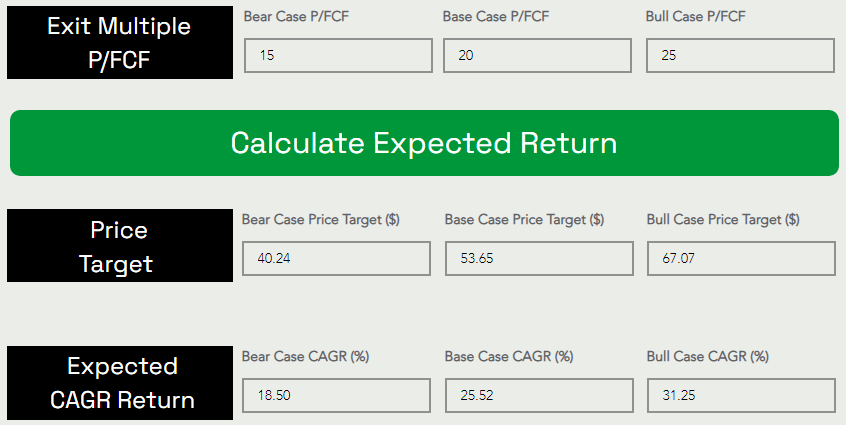

My Fair Value And Expected Returns For ASAN

{kind=link}

{kind=link}

According to TQI Valuation Model, Asana is currently undervalued by more than 30% and is worth $22.86 per share. Furthermore, an investment at $17.22 per share into Asana could generate a 5-yr CAGR return of 25.52% from current levels. Since this expected return is greater than my investment hurdle rate of 20% for high-growth stocks, I deem Asana a buy.

Bottom Line

Despite a sharp revenue growth deceleration, Asana's modern work management platform is still growing at a rapid clip. While the macroeconomic environment is likely to remain challenging, Asana's robust gross margins should allow the company to deliver operating leverage with scale. Now, management's FCF breakeven target timeline of CY2024 seems far-fetched at this point, with non-GAAP operating losses standing at -41% of revenue in Q3 FY2023. That said, positive free cash flow is certainly not out of the reach of a business with superb unit economics (Asana's GM: 90%) and high stickiness (Asana's NRR: 120%+).

After assessing Asana's valuation and testing it through TQI's Quantamental analysis process in one of my previous articles -

I view it as a strong buy for long-term investors. As a short-term play (<12 months), investors are better off skipping Asana due to weak quantitative factor grades and a broken technical chart. I don't have a crystal ball, and I am not sure where Asana's stock will bottom out eventually (or if it has bottomed out already).

Source: Asana Q2 FY2023 Review: Dustin's Vote Of Confidence Overshadows Growth Deceleration

Within TQI's Moonshot Growth Portfolio, we own a ~1.2% position in Asana at $18.09 per share, and I intend to continue to accumulate more shares slowly for the long haul over the coming weeks and months. Asana's current margin profile and cash burn rate make it a very risky bet in this challenging macroeconomic environment; however, a net cash position of $550M and Moskovitz's financial backing means liquidity shouldn't be a big concern. Also, I think Asana will get to positive free cash flow (and profitability) in due time. Considering the risk/reward on offer, I like the idea of accumulating Asana shares in a staggered fashion over 6-12 months.

Key Takeaway: I rate Asana a "Strong Buy" at $17, with a preference for staggered accumulation.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

For further details see:

Asana Q4 FY2023 Preview: Will Wednesday's Earnings Report Sink ASAN's Red-Hot Stock?