ASAN - Asana: SaaS Leader With Huge Insider Buying

Summary

- Asana is a software company which is a leader in team management solutions to improve productivity and alignment.

- The company reported solid financial results in the quarter, beating both revenue and earnings estimates.

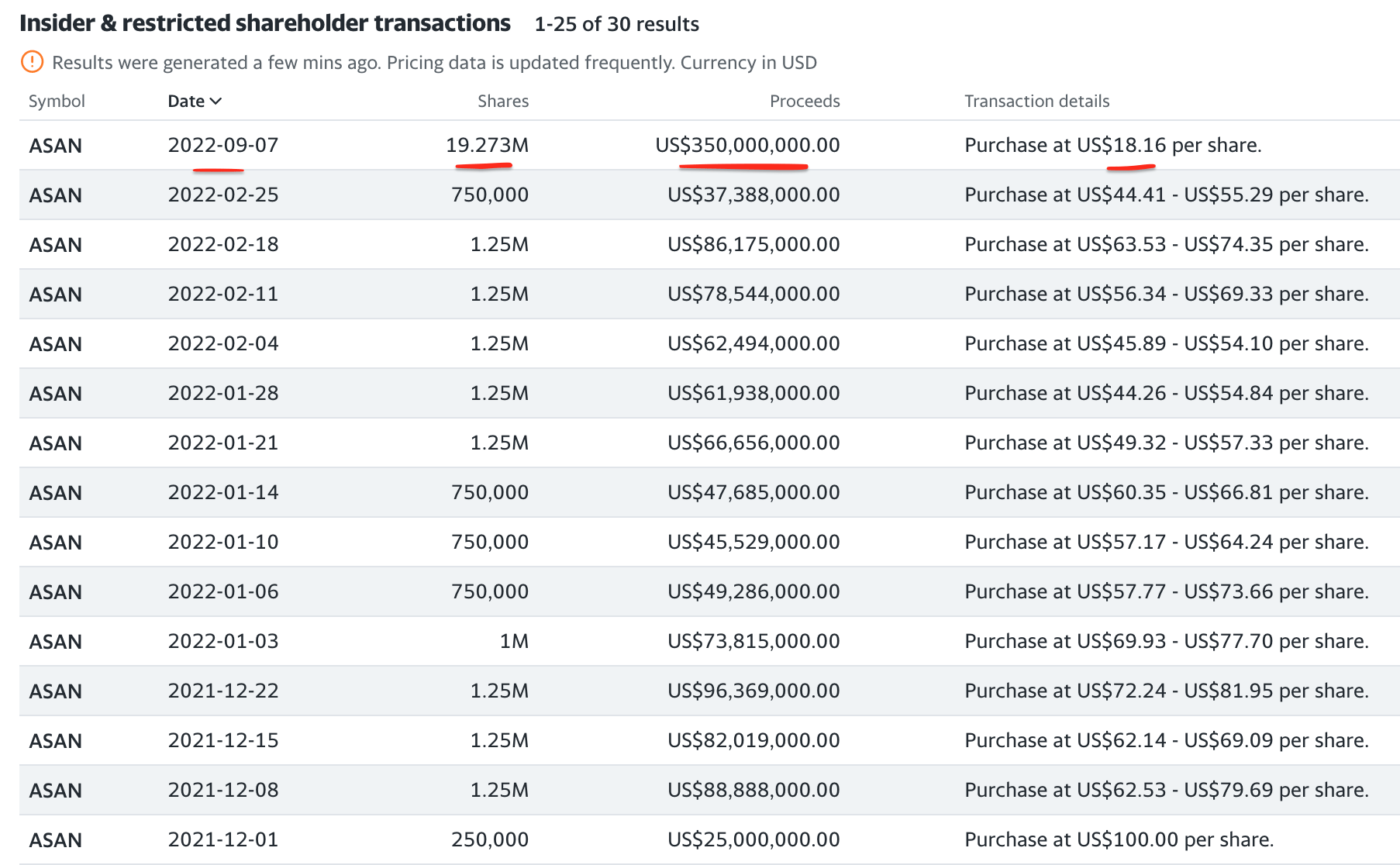

- Its founder and CEO Dustin Moskovitz purchased a staggering $350 million worth of shares at an average price of ~$18/share. (September 2022 report).

Asana (ASAN) is a leading software company that is focused on the team management space. The company has an elite list of customers which includes 80% of the Fortune 100 and major names such as Spotify, Accenture, and many more. Asana reported strong financial results for the third quarter of the fiscal year 2023, as it beat both top and bottom-line growth estimates. The company has burnt ~$100 million worth of cash last quarter. However, Asana does have a unique competitive advantage most other companies don't have. This is its billionaire founder and CEO Dustin Moskovitz, who is the co-founder of Facebook (META) and owns approximately half of the company. As the old saying goes "follow the money" and in this case, the founder has invested over half a billion dollars in the last few quarters alone (full insider transaction further down). In this post, I'm going to break down the company's business model, financials, and valuation, let's dive in.

SaaS Business Model

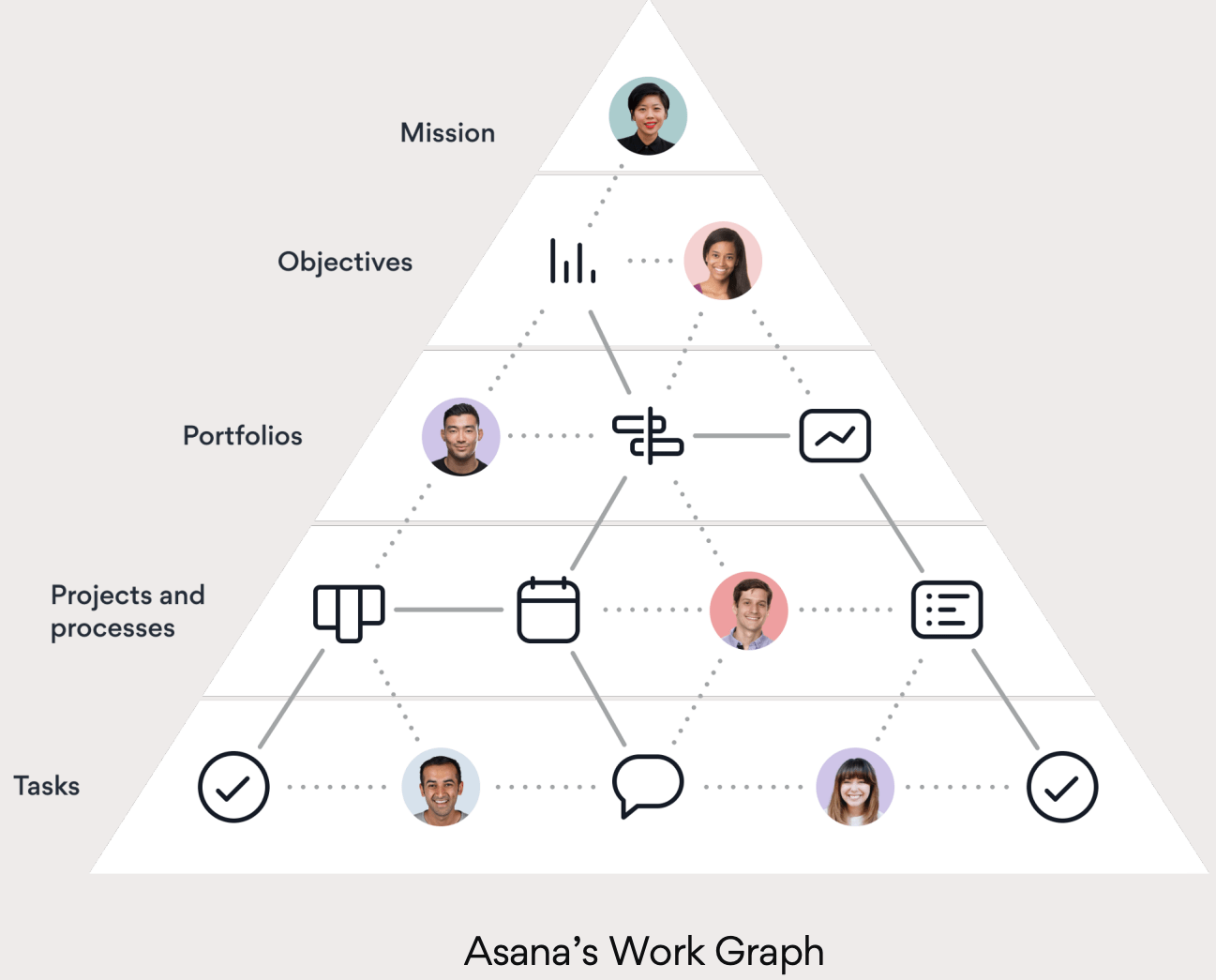

Asana's mission is to help improve work productivity through its user-friendly software platform. Asana uses "work graphs" to organize projects and help with alignment between teams. This starts with a "mission" such as "launch a successful product". Then this cascades down to individual objectives, "portfolios", individual projects, and tasks.

{kind=link}

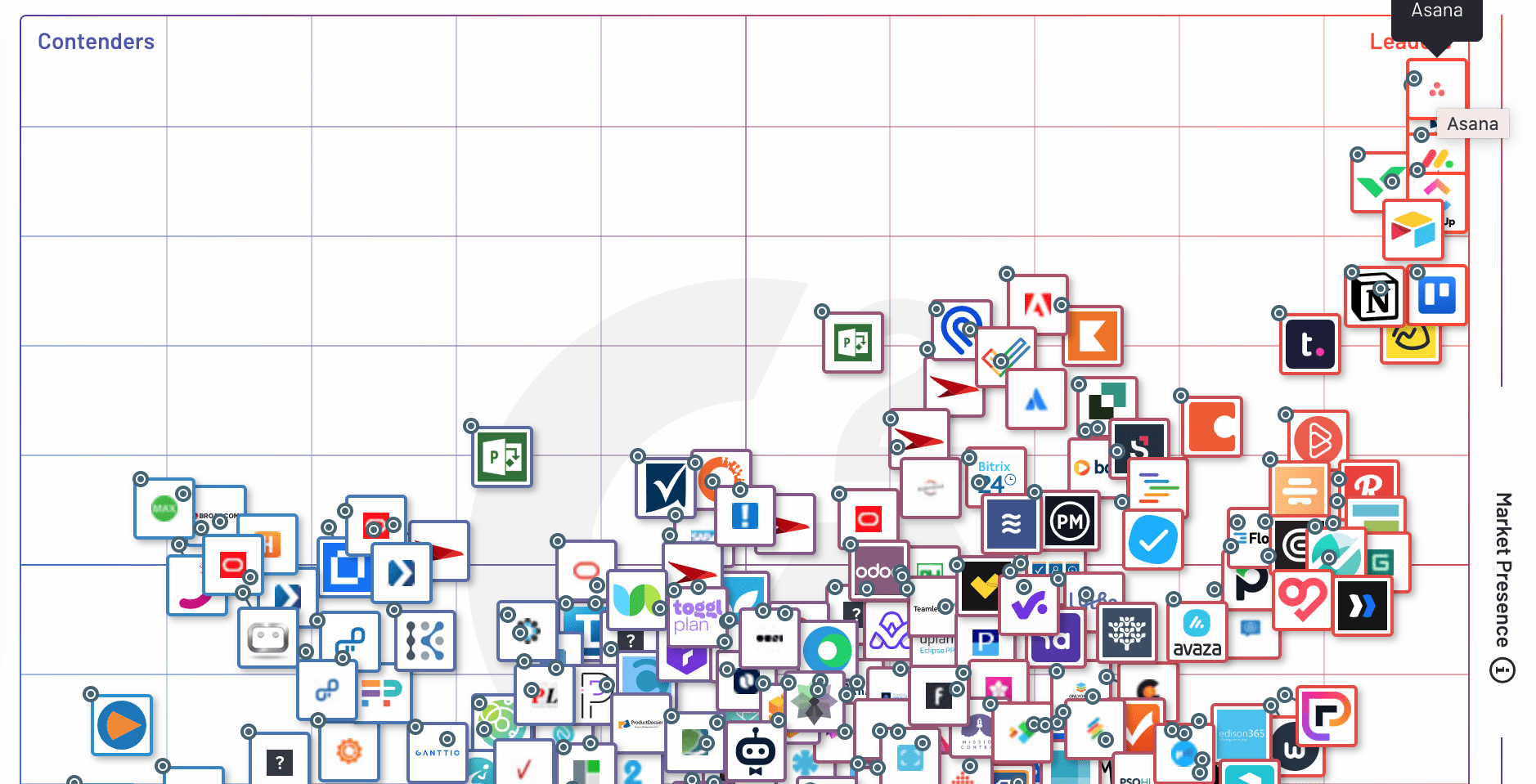

The Asana platform basically helps to reduce unnecessary time in meetings and emails, so team members can focus on the execution of tasks. This makes the platform extremely popular with project management, marketing, and go-to market teams. According to popular software review company G2, Asana is ranked as a "leader" in project management platforms for both market presence and performance. G2 ranked Asana at the top of its list, as it has the most number of reviews at over 9,000. However, it was interesting to see Monday.com has a higher star rating of 4.7 out of 5 stars. This is greater than Asana which has a 4.3 out of 5-star rating.

{kind=link}

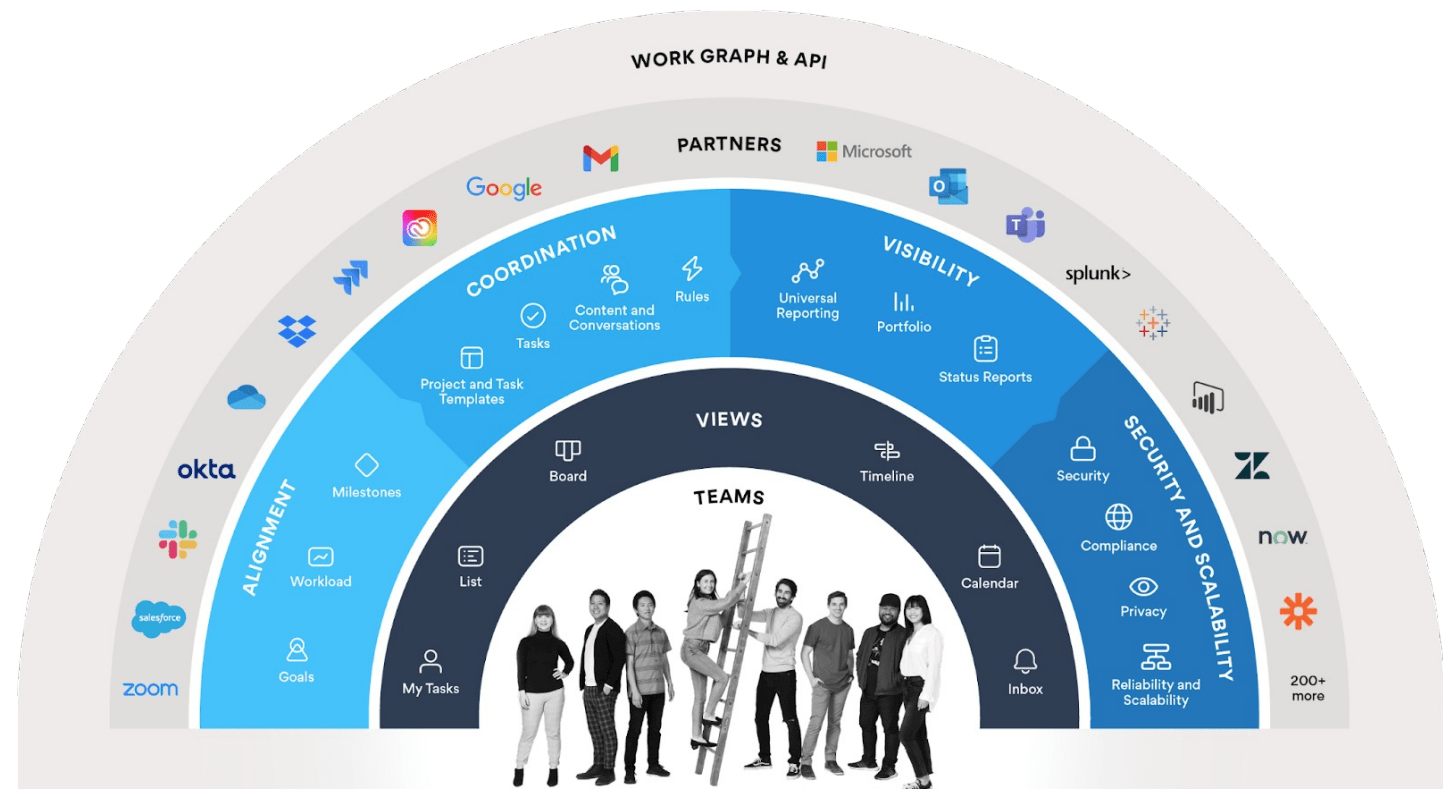

The beautiful thing about Asana is it has enabled various integrations with many applications from Salesforce (CRM) to Zoom and even Jira for Product Management. These integrations also enable "automation" to be set up between applications to help save time on repetitive tasks. One of my favorites is an artificial intelligence tool called "adam.ai", which automating sends meeting actions to Asana with a two-way sync. AI is a growing industry and we have recently seen the rise of the viral platform, ChatGPT . Therefore, this could be another huge market Asana could invest in to improve product functionality above smaller competitors.

{kind=link}

Growing Financials

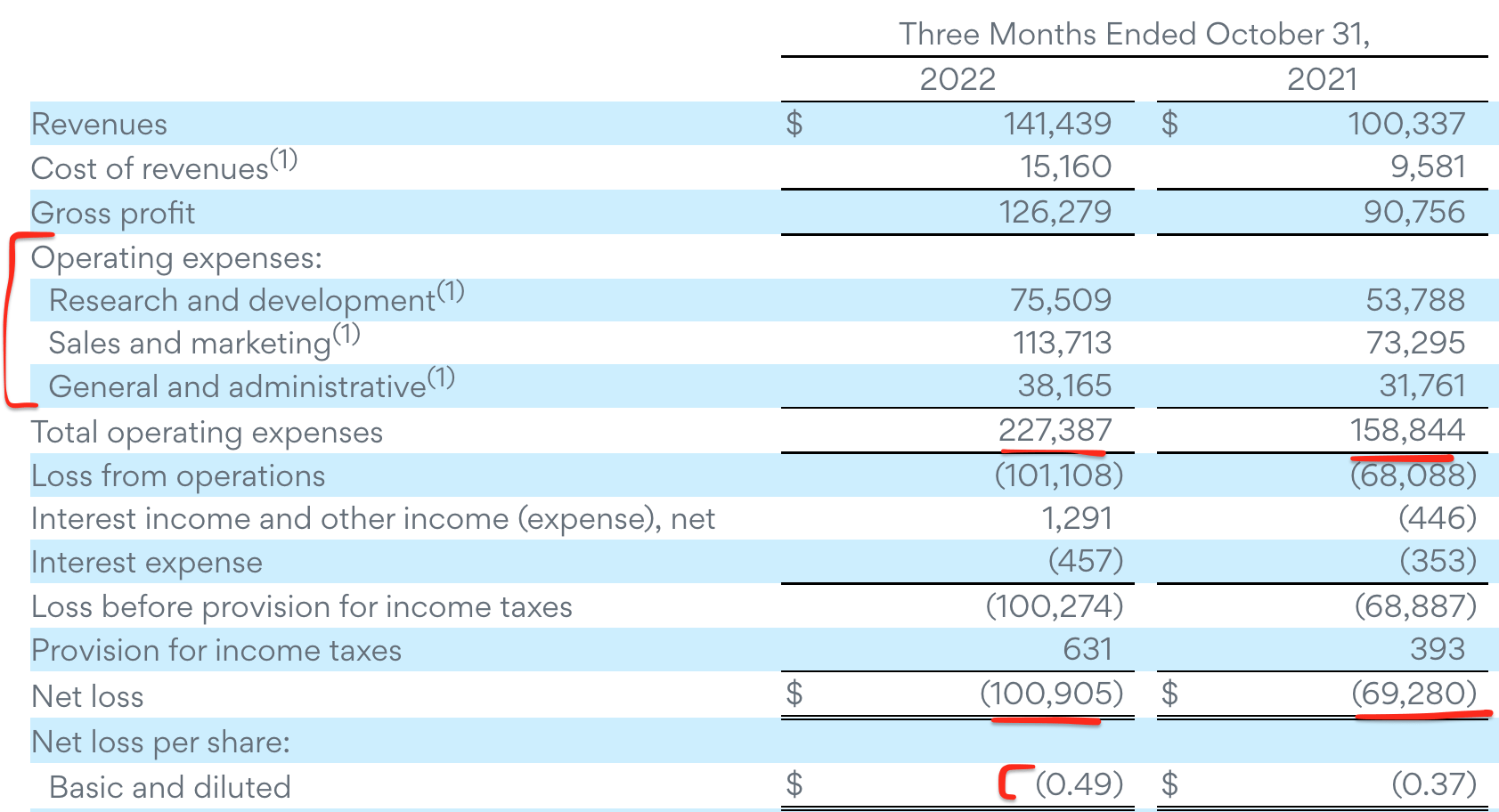

Asana reported solid financial results for the third quarter of fiscal year 2023. Revenue was $141.44 million, which surpassed analyst estimates by $2.42 million and increased by a rapid ~41% year over year. This resulted in an annualized quarterly revenue run rate of $566 million. The United States contributed to the majority (61%) of its revenue and increased by 47% year over year. This is a positive sign given a strengthening dollar has been a major issue for companies, with large portions of international revenue. In Asana's case, the company reported a 500 basis point headwind to international revenue growth and a 200 basis point headwind to overall revenue growth, which is minimal. This was driven by International revenue which account for 39% of the total and increased by 33% year over year.

Asana's strategy has focused on growing its customer base and increasing its number of "high ticket" customers. Approximately 73% of its revenue is derived from customers which spend over $5,000 per year. This segment increased by a blistering 68% year over year. Its "high ticket" customers which spent over $100,000 per year with the company increased by an outstanding 78% year over year to 493. This is a positive sign as large enterprise customers tend to be more "sticky" and offer a greater potential account value, which can be expanded over time. I believe having large companies also helped with "new logo" acquisition as it gives confidence to companies of all sizes. For example, when I evaluated Asana for a client I saw the name " Amazon ( AMZN )", as a customer which gave me more confidence in the product.

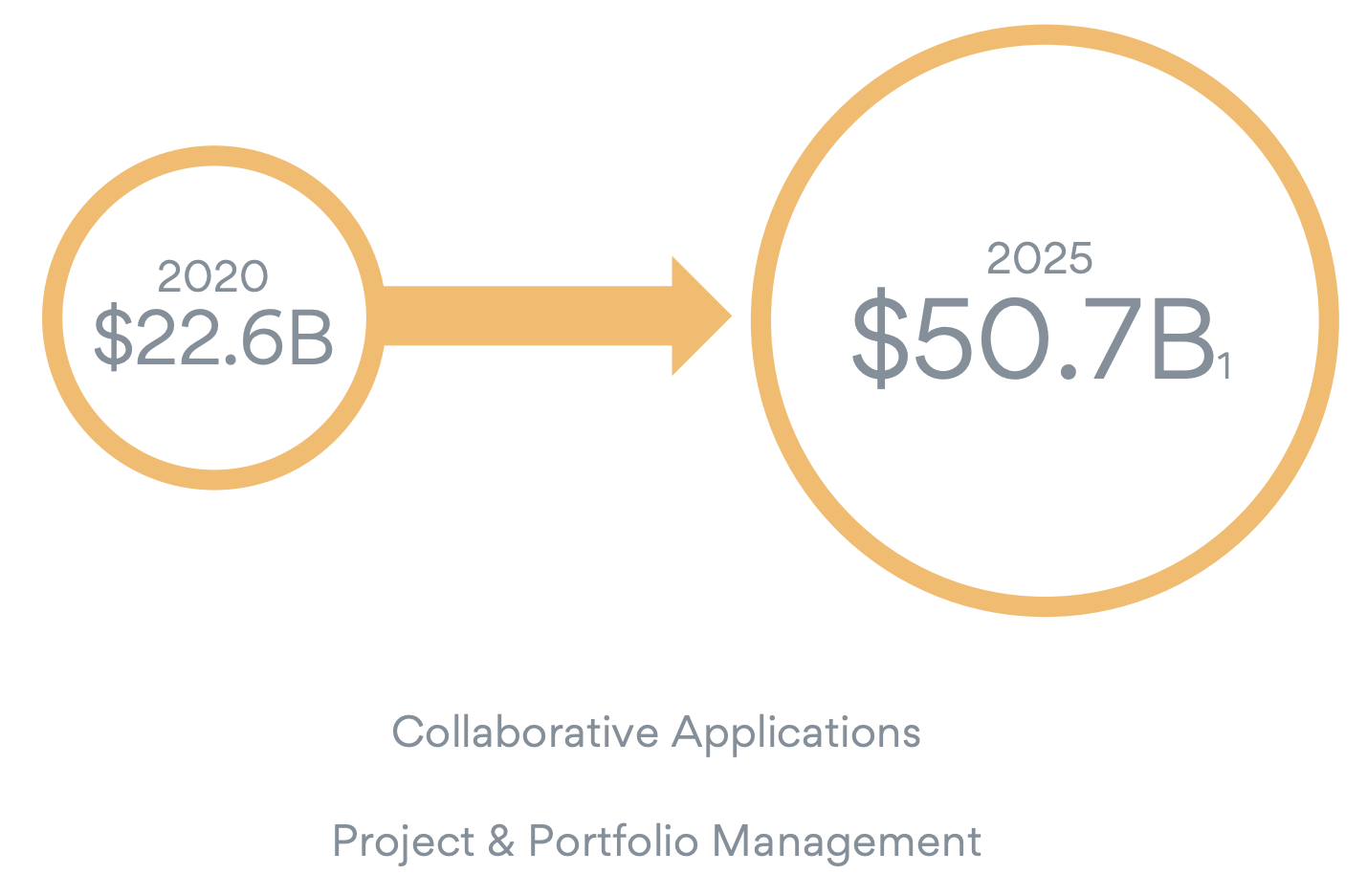

An Asana-cited study, estimates its total addressable market for its collaborative applications and Project & Portfolio management tools, will grow to $50.7 billion by 2025. Therefore, the company has plenty of runway for further customer growth.

{kind=link}

The beautiful thing about Asana's platform is it also has inherent "stickiness" built into it. Once teams start to upload their data and learn how to use it effectively, it becomes a daily part of their work lives. Therefore, changing to an alternative product (even if slightly cheaper) would be unlikely.

Asana's metrics back up my hypothesis, the company reported a strong dollar based net retention rate of greater than 120%. This means customers are staying with the platform and spending more. The majority of its customers paying over $5,000 per year has a net retention rate of 128%. Whereas its larger customers (as predicted) have a higher retention rate of over 140%.

Onto profitability and margins, Asana reported earnings per share [EPS] of negative $0.49, which beat analyst estimates by $0.02. However, this metric was worse (more negative) than the same quarter last year with negative $0.37 EPS reported. This was driven by a 43% increase in operating expenses to $227.4 million. As a percentage of total revenue, its expenses are ~161% which is simply eye-watering. Over time, I would like to see this improving and it is very possible given Asana is a software company that is inherently scalable.

Asana expenses (Q3,FY23 report)

{kind=link}

A positive is a large portion (81%) of its expenses were invested into Sales & Marketing, thus there is a method behind the madness. As I mentioned prior the team management software industry is a huge opportunity, and platforms in this space generally have high retention. Basically, this means we are seeing a "land grab" currently with project management platforms, as they aggressively aim to capture customers. As once they have the customer onboarded, the likelihood of them staying is strong. Alternatively, if they sit back and don't invest aggressively for growth, then another competitor could eat market share and hold it for a considerable period. This would leave other "enterprise" SaaS companies fighting for "scraps" in the long tail of mid-market SMBs.

The Billionaire Founder - Asana's secret weapon

The bold strategy of burning lots of cash to grow is only really possible with a brave and well-capitalized founder/CEO. In this case, I mentioned prior that Asana's founder and CEO is Dustin Moskovitz, the co-founder of Facebook. The CEO has a net worth of ~$9.6 billion and owns ~49% of all shares outstanding. Moskovitz has been loading up on millions of dollars' worth of shares, as the stock price of Asana has been falling. The latest transaction I could find was from September 2022. In that transaction, Moskovitz purchased 19.273 million shares, at an average price of $18.16 per share, which is higher than the ~$11 share price at the time of writing. The amazing thing about this latest purchase is it was worth a staggering $350 million which is not a small amount of cash by any means and substantially higher from prior purchases which have ranged from between $25 million and $86 million.

Founder Dustin Moskovitz insider buying (Yahoo finance/SEC data)

{kind=link}

Back to Asana's financials, the company has $545.4 million in cash and short-term investments on its balance sheet. In addition, the company has just $258 million in total debt. Its debt isn't an issue but its ~$100 million cash burn per quarter is. If this doesn't decline, the company has just over 5 quarters of cash left before it may have to raise more capital, which would dilute shareholders. For any other business, this would be an issue but given the company's billionaire founder who is actively buying shares, I suspect he will save the company. The founder/CEO also has the ability to purchase the other ~50% of the business and even take it private, which is a possibility nobody (except me) seems to be talking about.

Advanced Valuation

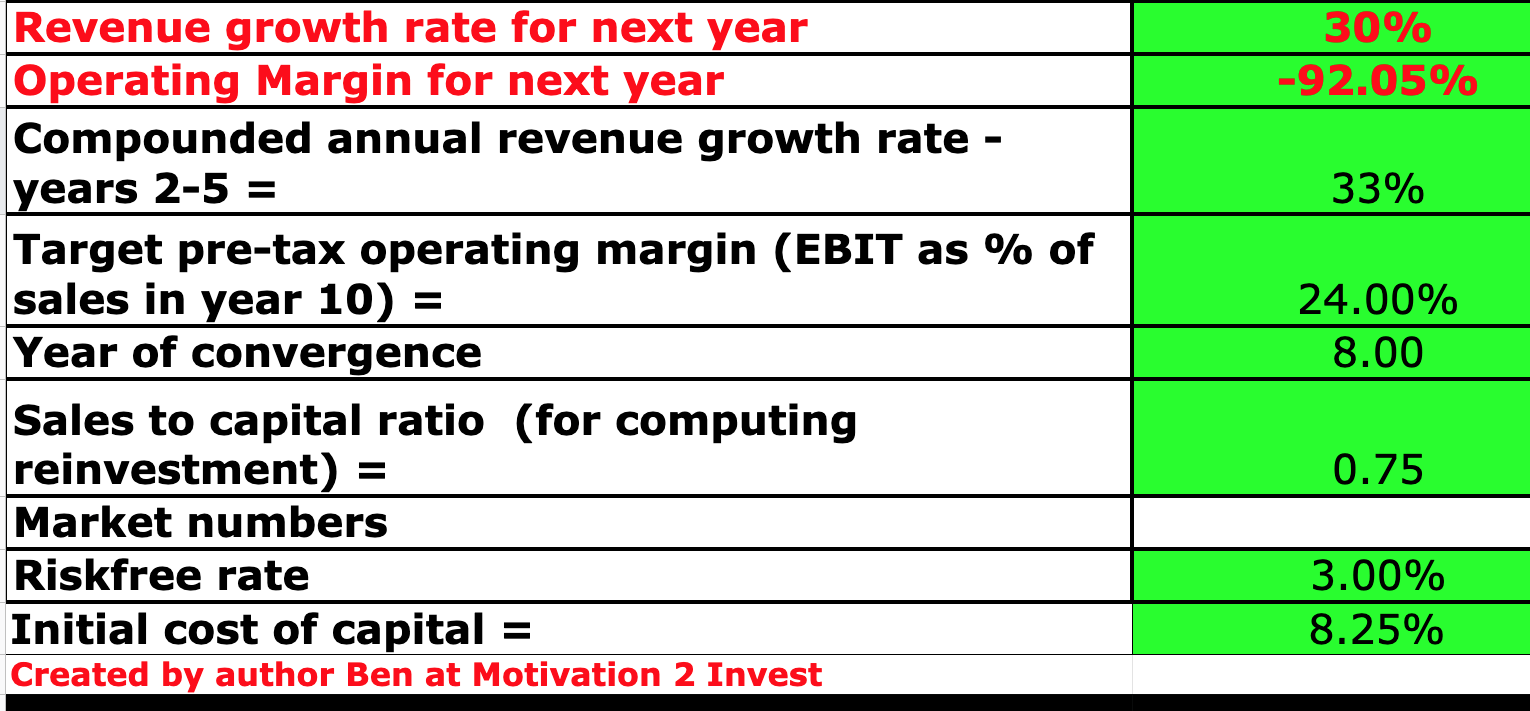

To value Asana, I have plugged its financials into my discounted cash flow model. I have forecast 30% revenue growth for next year, which is fairly conservative and less than the prior 41% growth rate. I forecast this to be driven by the forecasted recession and macroeconomic conditions, which I will discuss more in the "Risks" section. However, in years 2 to 5, I have forecast 33% revenue growth per year, as economic conditions improve.

Asana stock valuation 1 (created by author Ben at Motivation 2 Invest)

{kind=link}

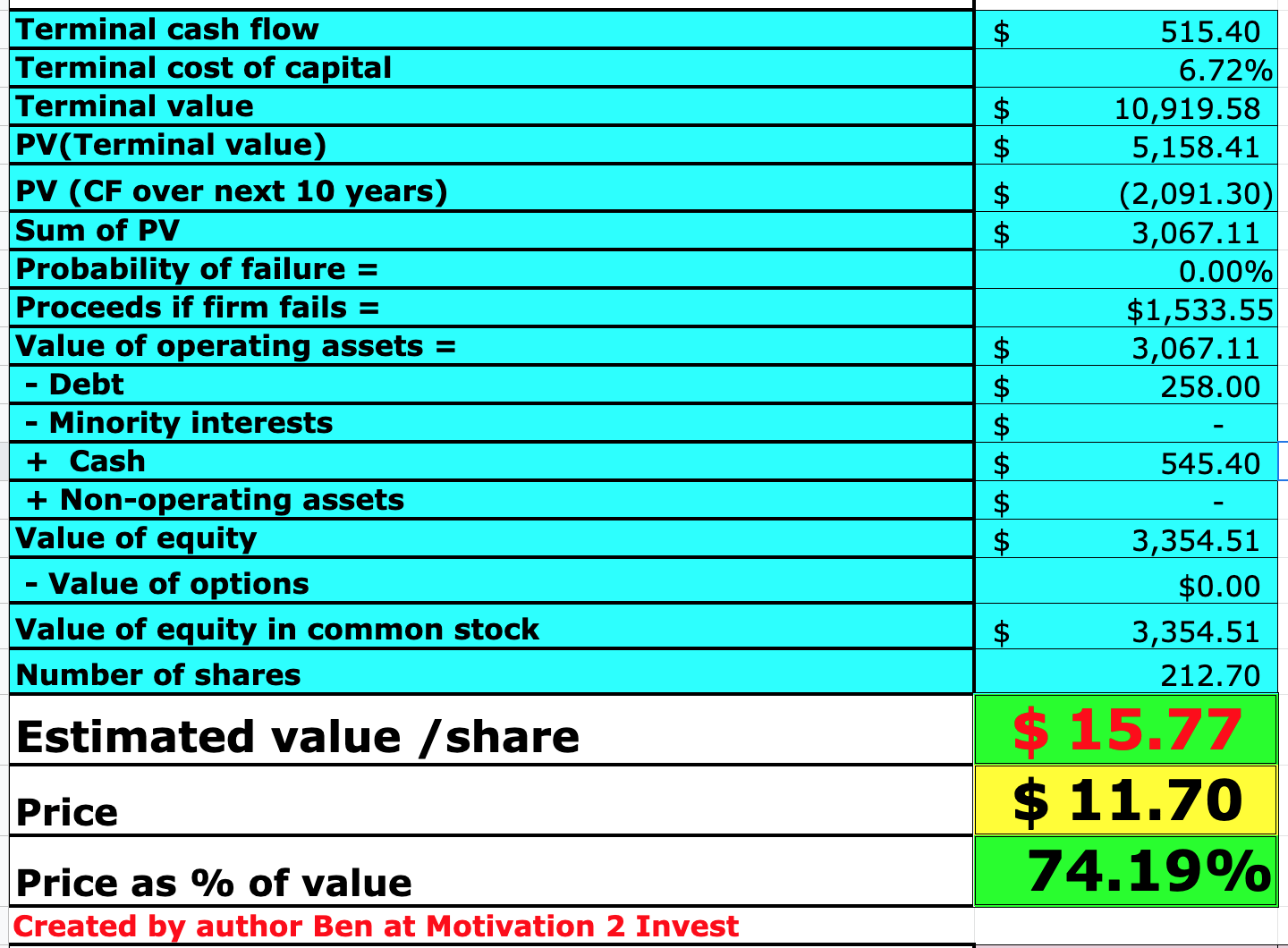

To increase the model accuracy, I have capitalized R&D expenses which has lifted net income. In addition, I have forecast a 24% operating margin over the next 8 years, which is slightly above the 1% average for the software industry. This is still a long way off, but assuming the company can keep growing its top line, operating leverage is inevitable.

Asana stock valuation 2 (Created by author Ben at Motivation 2 Invest)

{kind=link}

Given these factors I get a fair value of $15.77 per share, the stock is trading at ~$11.7 per share at the time of writing and thus is ~26% undervalued (with conservative growth estimates).

As an extra datapoint, Asana (purple line) trades at a price-to-sales ratio = 4.6, which is significantly cheaper than historical levels. In addition, the stock is trading cheaper than other project management stocks, albeit it does have worst margins.

Risks

Recession/Cash Burn

As mentioned prior many analysts are forecasting a recession in 2023. This will likely result in longer sales cycles and slowing growth. In addition, Asana's management noted that as its business customers slow down hiring this will cause a slowdown in its natural product expansion. I discussed details of the cash burn prior and that the company's founder will likely be the savior if expenses don't reduce over time.

Final Thoughts

Asana is a leading software company and is poised to benefit from the growth in the productivity tool industry. The company has a strong customer base of leading enterprise customers and super high product retention. Management is investing aggressively for growth which is a "risky" strategy. However, given the company has a billionaire founder who is aggressively "buying the dip", the business effectively has a "backstop", on major cash flow issues. Its stock is undervalued intrinsically and relative to historical multiples, thus it could be a great long-term investment.

For further details see:

Asana: SaaS Leader With Huge Insider Buying