ASAN - Asana: Strong Positioning But The Stock Is Not Cheap

2023-07-27 15:00:00 ET

Summary

- Asana, Inc. is a leading provider of collaborative work management applications that enhance productivity for individuals, teams, and organizations.

- The company is integrating AI into its product architecture to incentivize customers to upgrade to higher-tier plans and drive seat growth.

- Despite Asana's superior growth trajectory, its premium valuation and negative operating margins limit its near-term upside, leading to a hold rating for the stock.

Thesis

Asana, Inc. ( ASAN ) holds a prominent position as a leader in collaborative work management applications, effectively enhancing productivity for individuals, teams, and organizations by effectively addressing coordination challenges in the workplace. Its unique work graph, a proprietary architecture, is central to mapping out tasks, assigning responsibilities, outlining the execution process, and serving as a comprehensive record for associated work. As a result, users rely heavily on Asana as their primary and dependable source of information while collaborating both internally and externally. However, I view the risk/reward balanced at the current level due to ASAN's premium valuation compared to peers. Hence, I assign a hold rating to the stock for now.

Q1 Review and Outlook

Asana started the year on a positive note, reporting slightly higher revenue and better-than-expected profitability. Despite facing macro headwinds, such as longer sales cycles and seat pressure, Asana observed "pockets of the market stabilizing." The company reported steady demand at the top of the sales funnel and stable conversion rates from free to paid subscriptions. Looking ahead, Asana has adjusted its FY revenue guidance, raising it by $1 million or 0.2%, aligning it with consensus estimates. Additionally, the company has reset its PF (pro forma) operating margin guide higher by 160 basis points or 18%. Asana remains committed to achieving positive free cash flow on a quarterly basis, aiming to reach this goal before FY25.

Asana faced some macro headwinds in Q1, with longer sales cycles and customer downgrades primarily driven by lower headcount, especially in the technology sector. As a result, the dollar-based net revenue retention rate (DBNRR) for all customers, as well as those spending over $5K ACV and over $100K ACV, each declined by 5 points sequentially. The DBNRR for all customers, at over 110%, is now lower than that of a few years back when it stood at over 115%, despite starting at a lower level. The management expects the company's overall DBNRR to "trend lower, particularly in the lower end of the market."

Nevertheless, there are positive signs for Asana. The company reported stable logo churn and low churn rates among its largest accounts. Asana's largest deployment has reached an impressive 200,000 paid seats, a growth of approximately 50,000 seats compared to the previous period. Overall, Asana's performance demonstrates potential and promising growth opportunities, particularly with the integration of AI features. However, addressing profitability challenges and overcoming macro headwinds will require sustained efforts over multiple quarters.

Work Graph Differentiates Asana

Asana is actively integrating artificial intelligence into its product architecture through what it calls the "Asana Work Graph." Under the umbrella of "Asana Intelligence," the company plans to offer various AI-related features and functionalities. These include a priority inbox, goal-based resource management, health check, and instant summaries. The aim is to help users surface priority tasks and receive recommendations for joining specific projects. Asana expects that this integration of AI will have several positive effects on the business. Firstly, it will incentivize more customers to upgrade to higher-tier plans to access additional functionality. Secondly, it will drive seat growth as businesses recognize the value of AI-powered features. Thirdly, there is the potential for introducing an additional SKU or add-on offering that is priced based on consumption. However, it's important to note that these AI-related developments are not yet factored into Asana's FY24 guidance.

{kind=link}

Valuation & Financial Outlook

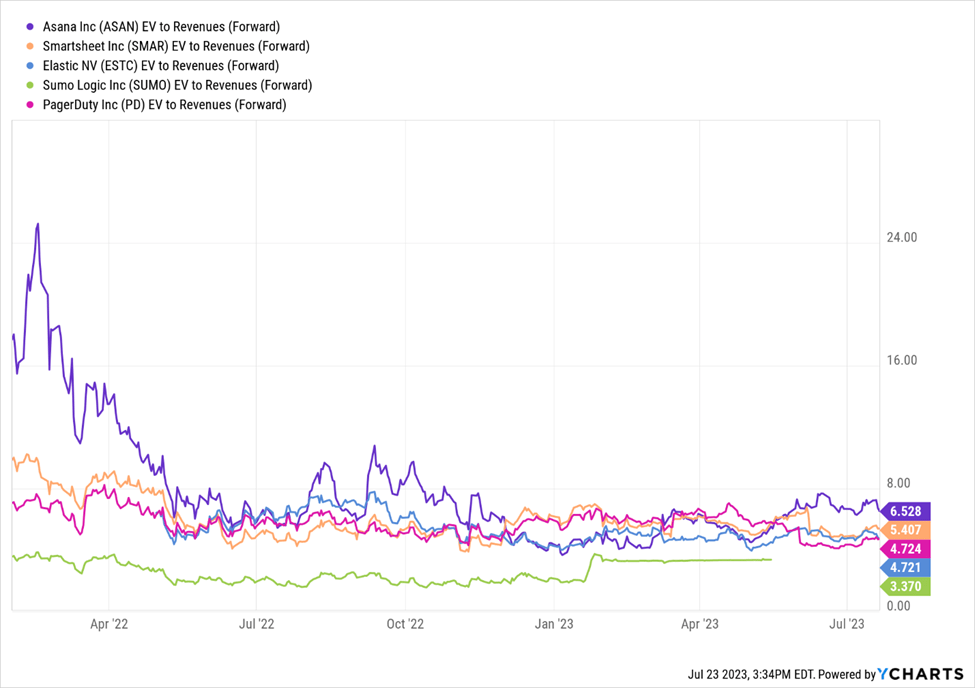

I examine a group of comparable companies to inform my view of Asana's valuation and rating. Given Asana's robust growth profile yet above-average losses, I consider the EV/revenue multiple to be the most relevant valuation metric, with a focus on the calendar year 2025. My comp groups include companies with products and use cases similar to Asana's and other software companies that, on average, demonstrate high revenue growth but have low or negative GAAP operating margins. Asana's valuation remains rich. Trading at 6.7 times FY24E revenues, the company's shares command a significant premium compared to a peer group of software companies with good growth but low or negative operating margins.

I certainly appreciate Asana's superior growth trajectory, but the continued forecasted losses make the possibility of further multiple expansions difficult. Asana's growth is decelerating with margin contraction. In FY23, it achieved 44% growth with a (74%) GAAP operating margin. However, for FY24, the consensus is expecting a 17-18% growth . The combination of slower growth and declining margins may raise questions about the pull-forward of revenue, spending efficiency, and competitive pressures.

Moreover, the work management space is becoming more competitive. Asana has shown strong product vision and leadership in the market, but its competitors are also scaling and improving at different rates. Microsoft's offerings, such as Power Platform, Planner, Project, Loop, and Ally.io, along with its ability to leverage Teams/O365, pose significant competition. Hence, I view the risk/reward as fairly balanced at the current price levels and informing my hold rating on the stock.

{kind=link}

Conclusion

Asana stands as a prominent front-runner among collaborative work management applications, effectively enhancing the productivity of individuals, teams, and entire organizations by addressing various workplace coordination hurdles. With Asana, users can confidently rely on a unified platform when collaborating with both internal and external groups, ensuring a consistent and reliable source of information. Although I believe that Asana's unique product differentiation will enable it to maintain its position as a leading force in this category, I see limited upside from here in the near term due to a premium valuation multiple and the company's negative operating margins. Hence, I view the stock as a hold at current levels.

For further details see:

Asana: Strong Positioning But The Stock Is Not Cheap