SAH - Asbury Automotive: Driving Superior Returns Through M&A

2023-09-18 21:50:36 ET

Summary

- Asbury’s revenue has grown at a CAGR of 11%, driven by the production of EVs and the post-pandemic boom in sales.

- We expect demand and growth to remain strong, owing to an aged vehicle population, the EV transition, services sales growth, business development, and M&A.

- We believe Asbury is an attractive proposition due to its M&A focus and well-balanced business model. We expect shareholder distributions to accelerate in the coming years.

- Asbury’s margins are respectable, although we expect some erosion as demand softens. Management is taking the correct steps to protect them.

- Asbury is facing near-term headwinds due to macro conditions, but we believe there is sufficient margin of safety due to its >10% FCF yield.

Investment thesis

Our current investment thesis is:

- We consider Asbury an attractive investment opportunity due to the development of its business model toward lucrative segments. The company is expanding into growing markets, investing heavily in expanding its services revenue (e.g. Financing and Parts), and developing its brands in line with industry trends (Such as Clicklane). The key value driver within this industry is to utilize a growing national Dealership network to expand “Other” revenue streams, which Asbury is doing fantastically.

- We believe this will allow the company to generate market-leading margins, at a time when the industry is experiencing downward pressures due to slowing demand.

- Current economic conditions represent near-term headwinds but we believe the business development is sufficient to make Asbury attractive now. From a valuation perspective, there is a good margin of safety, owing to its incredible FCF yield.

Company description

Asbury Automotive Group ( ABG ) is one of the largest automotive retail and service companies in the United States. Headquartered in Duluth, Georgia, the company operates a diverse portfolio of dealership brands across multiple states. Asbury primarily sells new and used vehicles and provides a wide range of automotive services, including maintenance and repair.

Share price

Asbury’s share price performance has been fantastic, returning over 300% to shareholders and significantly outperforming the wider market. The majority of this has occurred post-pandemic, with industry tailwinds driving an improvement in financial performance.

Financial analysis

{kind=link}

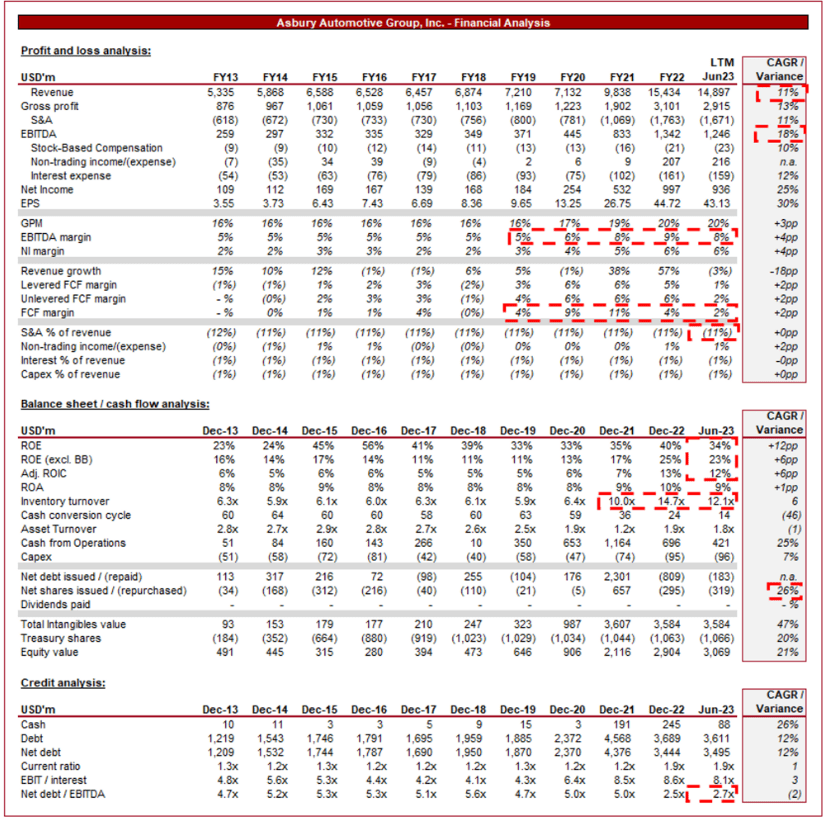

Presented above are Asbury's financial results.

Revenue & Commercial Factors

Asbury’s revenue has grown at a CAGR of 11%, a respectable achievement given the broad consistency YoY. The company experienced a clear acceleration in FY21 and FY22, exploiting tailwinds to improve its financial performance.

Business Model

Asbury operates a diversified portfolio of dealerships representing various automotive brands. This diversification allows the company to cater to a broad customer base with different brand preferences and levels of service expected. This portfolio has been developed through an acquisitive strategy and quality organic development, leveraging shared expertise.

{kind=link}

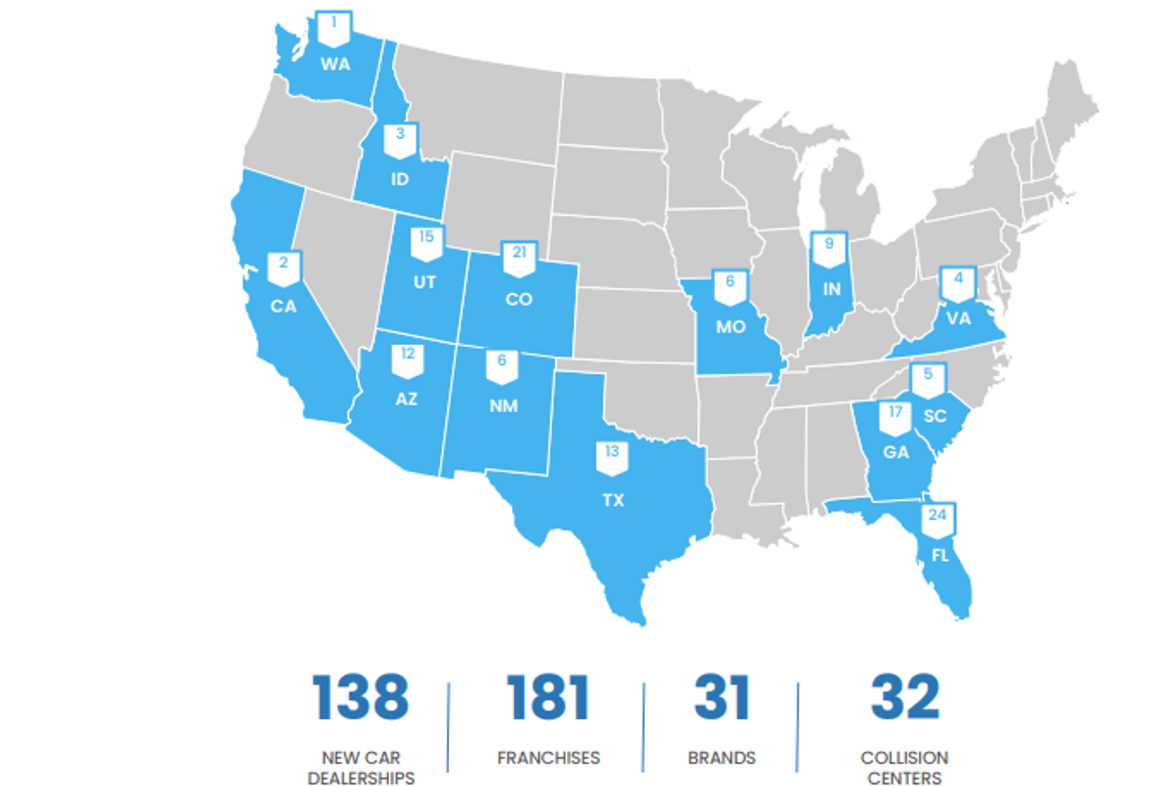

This broad portfolio has allowed Asbury to achieve impressive US expansion, with 138 Dealerships across the country and 181 franchises. This is a critical success factor within the industry, as consumers want to see the car they are going to purchase/ have easy access to support, so the benefits of a national network are substantial, allowing for convenient movement of vehicles and utilization of Collision Centers.

{kind=link}

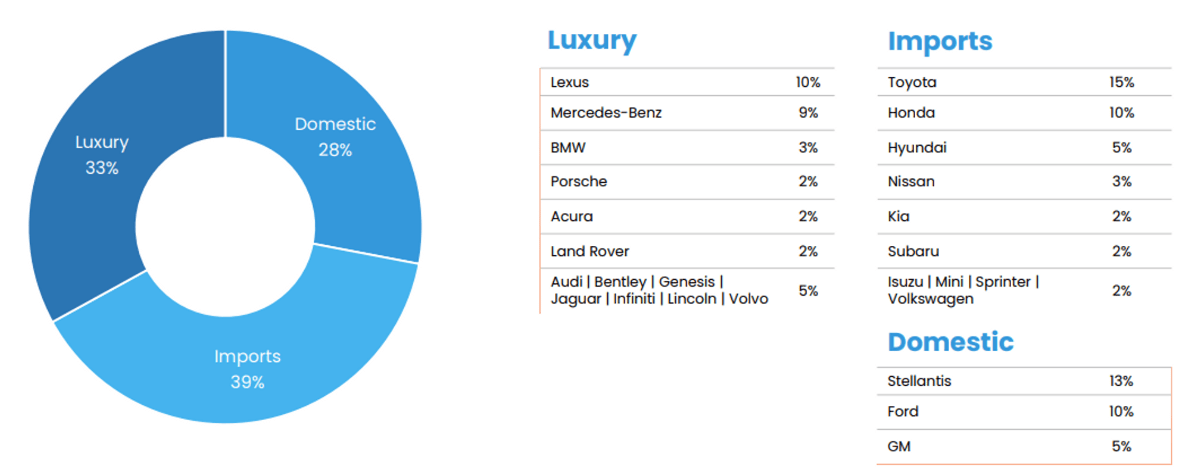

The core of Asbury's business is the sale of both new and used vehicles. New vehicle sales are typically more profitable than used ones, but the used vehicle market provides steady revenue streams and higher volume. Asbury’s brands provide a wide variety of brands, with an almost equal weighting toward Luxury, Domestic, and Imports. This means almost every US individual has access to a vehicle they may want from an Asbury’s dealership, maximizing its chance of winning a sale. From a downside perspective, this reduces the risk of dependency on any particular brand or segment to maintain its trajectory.

{kind=link}

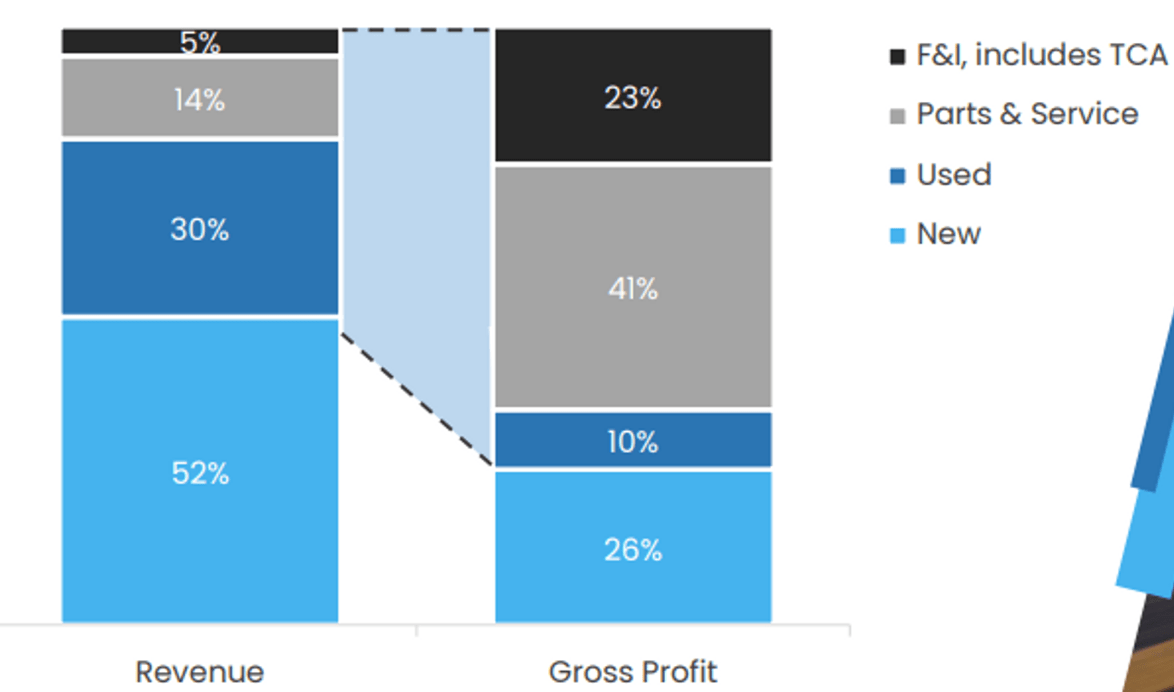

Automotive dealerships generate significant revenue from servicing vehicles and selling parts. Asbury's service centers provide maintenance and repair services, including routine maintenance, warranty work, and collision repair. Further, Asbury offers financing and insurance products to customers. Both services are highly profitable and “where the money is made”, with further benefits due to less volatility and a smoother revenue curve. As the following illustrates, P&S and F&I, which together are only 19% of revenue, contribute 64% to GP. This has contributed to a focus on expanding these services, naturally, with Asbury shrewd in acquiring and developing brands with a strong relationship with clients and/or scope for F&I integration. “Total Care Auto” is a stand-alone insurance company fully integrated with Asbury’s dealerships that provides attractive profitability and customer retention. Management believes EBITDA from this segment (currently c.$80m) will more than double by FY25.

{kind=link}

Like many modern automotive retailers, Asbury has a strong online presence. Customers can browse inventory, schedule service appointments, and even complete some of the vehicle purchase process online, which has become increasingly important in the digital age. The “end goal” is to allow for hassle-free online purchases with financing arranged or a stress-free route to finding an appropriate vehicle. The traditional dealers have faced competition from many e-commerce-only dealers, although we believe Asbury’s brand value, vehicles stocked, and national presence have made it a compelling proposition following the development of its e-commerce capabilities. Asbury is betting on its brand “Clicklane”, which is an online car buying network with new, used, and certified pre-owned cars (end-to-end solution), to enhance its exposure to the online trend. Clicklane’s revenue is forecast to grow from $2.1b in FY23 to $8b in FY25.

Management’s strategy for shareholder value creation centers around two key factors:

- Operational Excellence - Management is seeking to utilize its current (and future) scale to achieve a decline in average costs, with a focus on shared competencies and functions. Furthermore, the company believes highly in attracting top talent, being this will facilitate strong margins.

- Capital Deployment - Management’s capital is utilized in two key areas. Firstly, the objective is to acquire additional dealerships that meet the company’s investment criteria, namely accretive on a returns basis. Additionally, to maintain a high standard at current locations. Secondly, operate a reasonable leverage ratio so as to allow for growing returns to shareholders via buybacks.

We broadly like the strategy, although would have expected to see more regarding commercial improvement of existing locations. Realistically, the view is likely that once the brand is wholly integrated, all improvements will come from operational efficiency or group-level transformational exercises.

Automotive Industry

The automotive industry has historically been fairly uneventful, with incremental technological development driving any real volatility in sales. In recent years, however, there has been significant disruption.

The EV transition has contributed to an uptick in sales, as a growing number of consumers are seeking to adopt this new technology. This is due to a number of reasons, including running costs, the price of EVs relative to others, and sustainability efforts. With Governments legislating heavily around traditional ICE-powered vehicles, the expectation is for strong growth to remain, in both the new and used segments.

Despite this transition, the average US vehicle fleet age continues to increase, reaching a record 12.5 years . This implies a broad base of consumers are holding onto their vehicles, with greater access to parts/workshops, as well as improved vehicle quality. This should ensure resilient demand for parts and a healthy used car market in the years to come, as aging implies a greater need for servicing and an impending new purchase.

The pandemic also provided a once-in-a-lifetime opportunity to increase sales, with supply unable to meet demand due to supply-chain constraints. This contributed to a material imbalance, allowing dealerships to hike purchase prices and improve margins. This is slowly unwinding as semiconductor chips are delivered and demand softens further. The expectation is thus for a “reversion to the mean”, although we believe the improvements delivered by Management in recent years should put the business in a better position.

Asbury has been strategically expanding its dealership portfolio through acquisitions of new dealerships in different regions and representing various automakers. This has allowed the company to tap into different markets and customer segments. Facilitating this is the nature of the dealership industry, which is highly fragments nationally. Due to this, Asbury is able to identify a large pipeline of targets, giving it a long runway for further bolt-ons.

Asbury competes with other automotive dealership groups, both publicly traded and privately held. Major competitors may include AutoNation ( AN ), Sonic Automotive ( SAH ), and Penske Automotive Group ( PAG ), among others. Competition is based on factors such as brand representation, customer service, pricing, and location.

Economic & External Consideration

Current economic conditions represent a major issue for the business. Following an extended period of high inflation and elevated interest rates, consumers are deferring or canceling big-ticket purchases, with a focus on protecting finances. Compounding this is the higher interest rates, with many consumers now priced out of acquisitions, as lenders turn defensive.

In the company’s most recent quarter:

- Sales declined (5)%, reflecting reduced demand for vehicles, primarily in the used vehicle segment (-20%). This is expected given the demographic that is more inclined to purchase used vehicles is more greatly impacted.

- New car sales grew +4% (+8% on a Same-store basis), reflecting partially an overhang post-pandemic, as supply slowly unwinds. We expect this segment to slow.

- F&I declined (18)%, as the higher rates negatively impacted origination.

- P&S grew +1% (+6% Same Store), reflecting impressive resilience despite market conditions.

Broadly, this has been an average quarter. Importantly margins have not materially declined, implying operational improvements and cost controls are working to offset softer demand.

Margins

{kind=link}

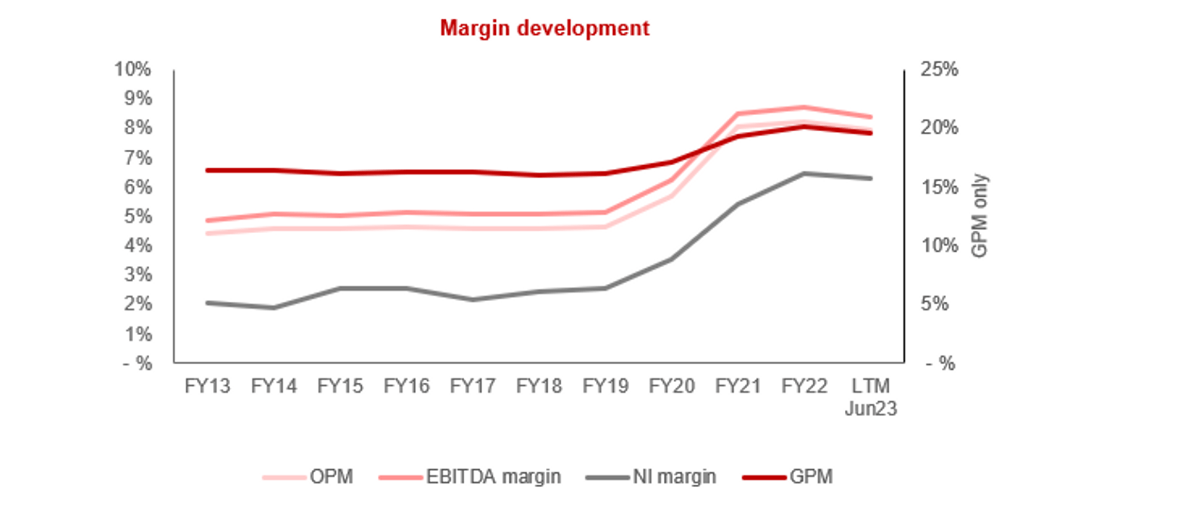

Asbury’s margins have been impressively consistent, reflecting the mature nature of the industry and the lack of scope for improvement. The uptick following FY20 is a reflection of the demand/supply mismatch following the supply-chain issues. We expect margins to soften in the coming years, although not necessarily back to prior levels. Asbury and its peers are focused heavily on maintaining the current levels, with active pricing and aggressive selling of services. Our expectation is that EBITDA-M ladders down to 6-6.5% by FY26.

Balance sheet & Cash Flows

Asbury’s current ND/EBITDA is 2.7x, with interest comprising 1% of revenue. At this level, we are broadly comfortable with debt, although Management is seeking to deleverage further. This creates the potential for increased distributions in the near future, as well as further M&A.

Most recently, Asbury announced a deal to acquire Jim Koons Automotive Companies , which has over $3b in revenue (2022) and 20 dealerships. We really like this acquisition, as it gives Asbury exposure to one of the fastest-growing regions in the US.

Industry analysis

{kind=link}

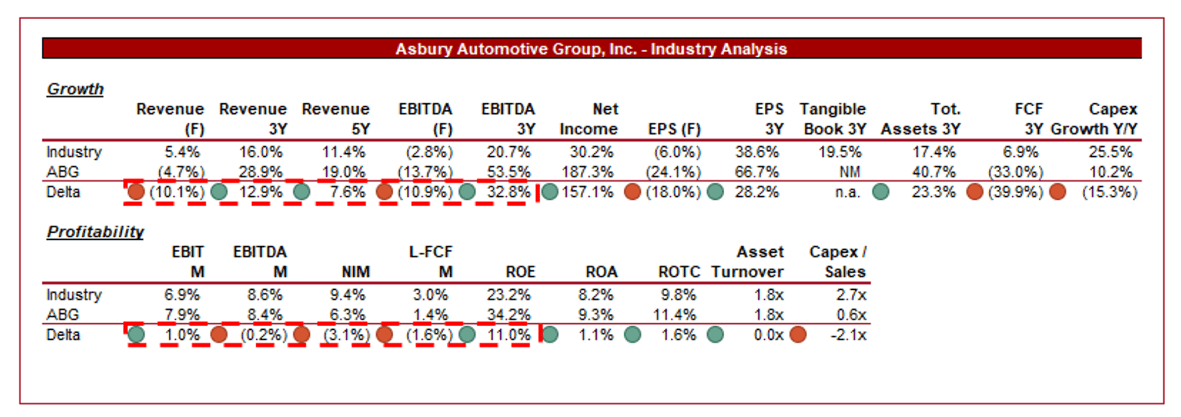

Presented above is a comparison of Asbury's growth and profitability to the average of its industry, as defined by Seeking Alpha (21 companies).

Asbury is performing modestly relative to its peers. The company’s growth has been strong, particularly in the near term, owing to M&A activity. The key for us is that its 3Y EBITDA and 5Y Revenue are higher, implying the company has been above-average in exploiting the post-pandemic industry tailwinds.

Its weaknesses are margins. The company is noticeably below average, although can at least boast a better ROE. This is primarily due to the weighting in the peer group toward parts-only businesses, that will naturally have higher margins. Purely compared to dealers, Asbury is a leader.

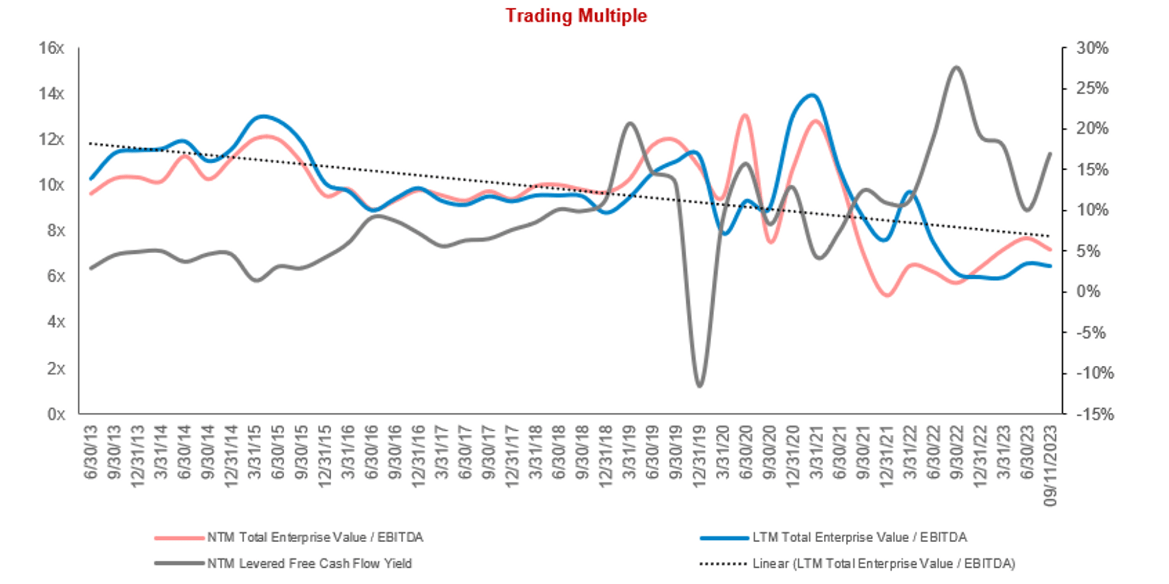

Valuation

{kind=link}

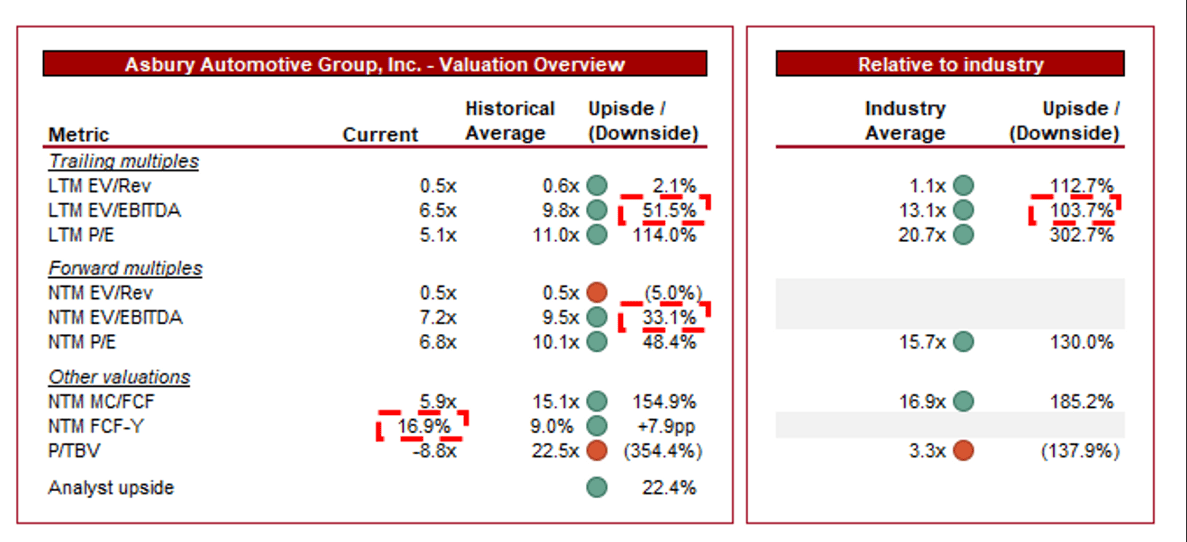

Asbury is currently trading at 7x LTM EBITDA and 7x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average appears reasonable, given the significant risks associated with margin contraction. This said, the degree is too large in our view, owing to the commercial development.

Further, the company is trading at an over 100% discount to its peers, both on an LTM and NTM basis. This appears extreme. The company has achieved better growth, has scope for further operational improvements, and is comparably profitable to its direct competitors. Once again, this is a case of investors fearing a substantial margin decline.

What confirms the business being undervalued for us is the growing gulf between the company’s current valuation and its NTM FCF yield. Why its valuation has traded down, its FCF yield is significantly above average, implying greater value for shareholders today.

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- EV development - The growth in the EV segment has the potential to be a key driver in the coming years, particularly as we move toward the legislative deadlines for traditional ICE-powered vehicles in various nations. With Asbury’s broad brand diversity, its risks are diversified.

- Interest rate development - As discussed above, rates are critical to both sales growth and increased F&I activity. For this reason, the downward movement of interest rates from the current level is a key risk to how growth transpires in the coming years.

Final thoughts

Asbury is a fantastic company. The business has grown commendably, underpinned by quality M&A due diligence, a strong group business model and integration, and a razor-focused Management team that understands its optimal value drivers. We believe the circular approach of “acquiring/building dealerships > expanding F&I and P&S > reinvest and distribute > repeat” is a compelling proposition with a strong runway.

A number of its peers are conducting a similar strategy, some of which we like (such as Lithia ( LAD )). With Asbury, however, there are quality platforms (Clicklane and TCA) that alone are forecast to drive substantial growth. When partnered with its current leading economics, Asbury appears incredibly well placed.

Surprisingly, Asbury’s valuation does not mirror its attractive commercial position. We suspect investors are overly concerned about near-term struggles. Although we believe this will be painful, the medium-term upside far outweighs any downside in the coming quarters.

For further details see:

Asbury Automotive: Driving Superior Returns Through M&A