NXPI - ASML: Ignore The Destruction Of Demand - Effective Monopoly Remains Unchallenged

2023-05-13 10:00:00 ET

Summary

- With a likely recession by H2'23, 15 years after the previous downturn, it is natural that ASML's EUV orders may be delayed or canceled in the near term.

- However, with its backlog extending through 2025, we do not expect any material impact on its 2023 performance, with the company also reaffirming its forward guidance.

- Considering that no recession lasts forever, this is merely a normalization after hyper-pandemic demand.

- ASML remains strategically positioned as one of the most important supply chains in the semiconductor chip industry, with an "effective monopoly on the world's most advanced chip-making machines and technology."

- Investors may want to add this stock to their well-diversified tech portfolio, at the next retracement to the March 2023 support levels.

The Economic Downturn Is Only Temporary - ASML's Dominance Remains Unchallenged

ASML Holding N.V. ( ASML ) is the latest semiconductor supply chain company to be impacted by the economic downturn, the resultant demand destruction, and the volatile geopolitical issues between the US and China. The latter of which we have previously covered in our previous article here .

ASML now projects that up to 20% of its backlog is attributed to China, comprising up to 50% of its Deep UV systems. It is important to note that these lithography systems are used to manufacture semiconductor chips in the mid-critical and mature end-markets, such as EVs, renewable energy, and industrial products, amongst others.

Therefore, depending on how the actual ban is shaped , whether only comprising its newest tech EUV or including the mature Deep UV systems, we believe the impact on the company's top/ bottom line and the global semi-supply chain may be more impactful than expected.

For now, ASML highlights that most of the Chinese backlogs remain trade export compliant, with orders reverting to the older 1980s Deep UV series, instead of the 2050s or 2100s series to avoid "being blocked." This strategy may potentially preserve its sales in the intermediate term, if stricter rules are not imposed.

Meanwhile, the DUV and EUV maker may have been hit by the semiconductor demand destruction, with the world's largest foundry, Taiwan Semiconductor Manufacturing Company Limited ( TSM ), potentially canceling or delaying 40% of its EUV shipment.

The same cadence has been observed with memory chipmakers , such as Micron Technology ( MU ) and Samsung ( SSNLF ), where capital expenditures and production cuts have been announced. These likely comprise part of ASML's reduced net bookings of €3.8B in FQ1'23 ( -39.6% QoQ and -45.7% YoY ), comprising only 21% (-15 points QoQ and -13 YoY) for memory systems.

However, orders from Intel Corporation ( INTC ) may remain intact, attributed to its ability in recapturing some of its ongoing capital expenditure through Smart Capital . The list includes government incentives from the CHIPS Act in the US and the EU, refundable investment tax credits, and Semiconductor Co-Investment Program [SCIP] with Brookfield Asset Management.

Combined with ASML's expanded total backlog of €39B by FQ1'23 (-3.4% QoQ and +34.4% YoY), we believe its intermediate-term prospects remain more than excellent, since it is "almost 2x this year's system sales ."

Furthermore, headwinds from China likely pose little risks, with demand likely to be diverted to other locations, as similarly highlighted by NXP Semiconductors ( NXPI ) in the recent Bloomberg New Economy conference. Kurt Sievers, the CEO of NXPI, said:

What I think for our industry is sometimes hard to deal with is there doesn't seem to be a clear roadmap on what to expect going forward. (Around 38% of NXP's sales are to Chinese manufacturers, about half of which are processed and then re-exported to Western buyers.) A lot of that going forward could eventually move out of China, which doesn't harm us. We will just follow where our customers are moving. ( Reuters )

In addition, the long-term demand for semiconductor chips will not wane, attributed to the sustained cadence towards IoT and data center post-pandemic, significantly aided by the recent AI boom and sustained decarbonization progress through EVs and renewable energies through 2050.

Therefore, we believe the moderation in ASML's backlog is only temporary, attributed to the peak recessionary fears and volatile geopolitical issues, with demand likely rebounding once these headwinds lift, possibly by 2025.

So, Is ASML Stock A Buy , Sell, or Hold?

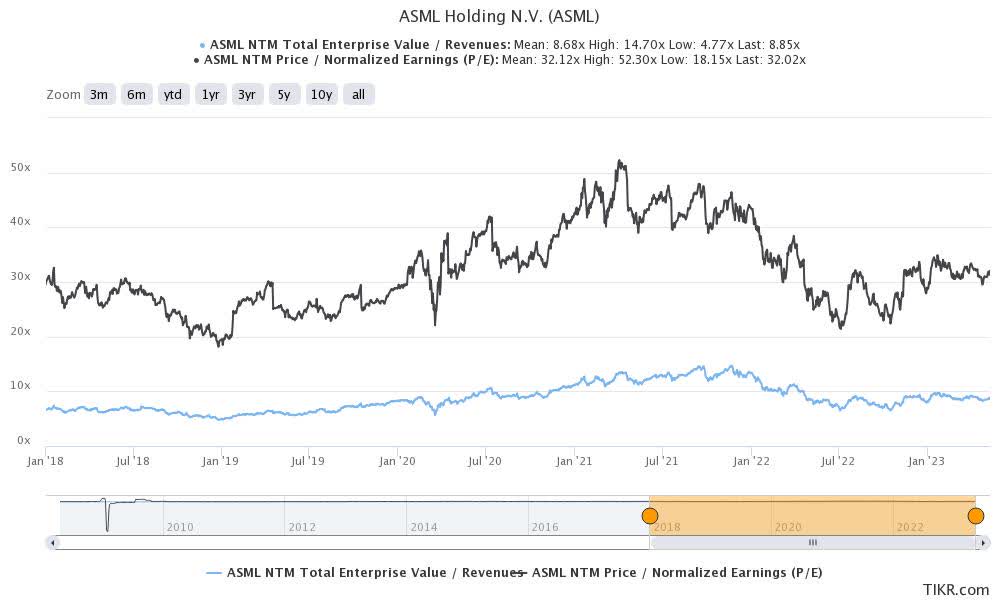

ASML 1Y EV/Revenue and P/E Valuations

{kind=link}

ASML is currently trading at an EV/NTM Revenue of 8.85x and NTM P/E of 32.02x, higher than its 3Y pre-pandemic mean of 6.33x and 26.78x, respectively. Otherwise, it is nearly in line with its 1Y mean of 8.69x and 32.13x, respectively.

With the company projected to record an exemplary top and bottom-line expansion at a CAGR of 18.2% and 28% through the economic downturn in 2025, the optimism embedded in its valuations is unsurprising, compared to the normalized CAGR of 20.9% and 26.6% between FY2019 and FY2022.

This is on top of the FQ1'23 outperformance , with the DUV and EUV maker recording double revenue and EPS beats, while guiding FY2023 net sales growth of approximately €26.46B (+25% YoY). Assuming that it sustains stellar gross margins of over 50% and a minimal increase in operating expenses between +5% to +10% YoY, we may also see the company record an expanded EPS of $18.00 (+27.3% YoY) then.

In addition, ASML remains strategically positioned as one of the most important supply chains in the global semiconductor chip industry. Combined with its " effective monopoly on the world's most advanced chip-making machines and technology," it is no wonder that the stock has also recorded impressive recoveries thus far.

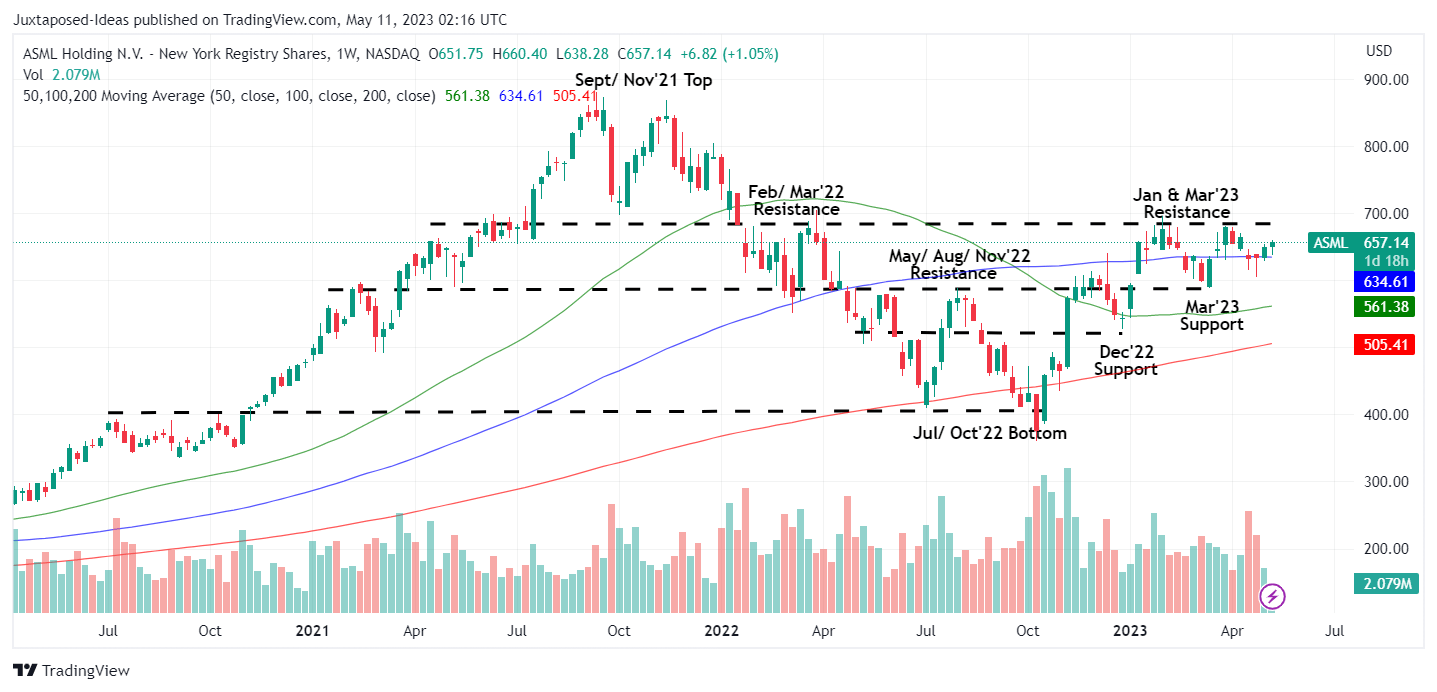

ASML 5Y Stock Price

{kind=link}

ASML has already rallied by another +20.2% since our previous Buy article in December 2022, with it successfully rebounding from the recent March 2023 bottom. However, the stock has also notably failed to break through the previous January and March 2023 resistance levels, potentially triggering more downward pressure ahead, due to the volatile geopolitical issues.

ASML 10Y Returns

{kind=link}

While we similarly hold the belief that ASML may continue to record excellent returns ahead, it is also important to highlight that most of its 10Y gains of +731.01% have occurred during the past three years of hyper-pandemic valuations.

With the increased likelihood of a mild recession by H2'23, recovery only by 2025, and the sustained inventory correction in the global semiconductor industry, we suppose that the stock may potentially retrace in the short term, potentially retesting its March 2023 support levels.

As a result, we recommend interested investors monitor the uncertain macroeconomic outlook a little longer and add the ASML stock at the March support levels of $580s for an improved margin of safety, if not at the December 2022 levels of $550s.

The latter level may also provide an expanded upside potential of 32.7% to our moderate price target of $730, based on our projected FY2024 EPS of $22.80 (+27% YoY) and its NTM P/E of 32.02x.

For further details see:

ASML: Ignore The Destruction Of Demand - Effective Monopoly Remains Unchallenged