CA - ATCO: Go For The Dividend Aristocrat Not The Dividend King

Summary

- ATCO has three segments, but the bulk of the earnings come from Canadian Utilities.

- The latter has delivered 50 consecutive annual dividend increases.

- We examine valuation at both the parent and the daughter level and make a suggestion.

Investors love utilities the most when they hate other sectors. Certainly, the bear market over the last 12 months has shown the value of being defensively positioned. While not the pulse-pounding ride that investors came to love during the 2020-2021 era, it would be fair to say that utilities, as measured by Utilities Select Sector SPDR ( XLU ), delivered.

While one can appreciate the 21.5% outperformance, it does leave us uncomfortable. The key reason is that utilities are about the worst shape we have ever seen them in. This comes from an absolute valuation perspective as well as comparing their returns to the risk-free rate.

So can we own defensive assets like Utilities here? The answer is, "yes, but only if you're careful." We go over one that we like today.

ATCO Ltd.

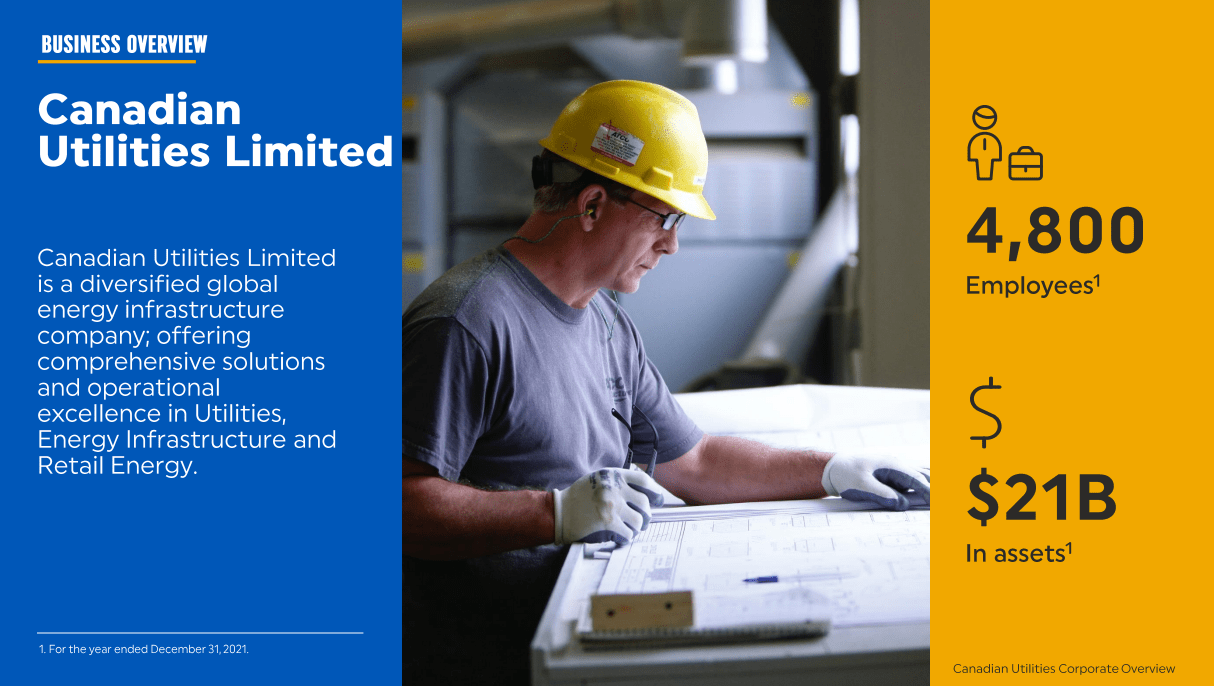

ATCO's ( ACLLF ) ( ACO.X:CA ) ( ACO.Y:CA ) primary asset is its 53% stake in Canadian Utilities Ltd ( CDUAF ) ( CU:CA ). Depending on who you ask, that stake is worth about 80%-90% of the company's ultimate value. So, on paper, ATCO appears as a diversified holding company (and we will get into the other parts as well). In practice, it's about as close to a utility company as you can get. To get a sense of what it does, we need to look at CU and how it's valued today.

Canadian Utilities is a holding company with primary assets consisting of regulated utilities in the province of Alberta, Canada.

{kind=link}

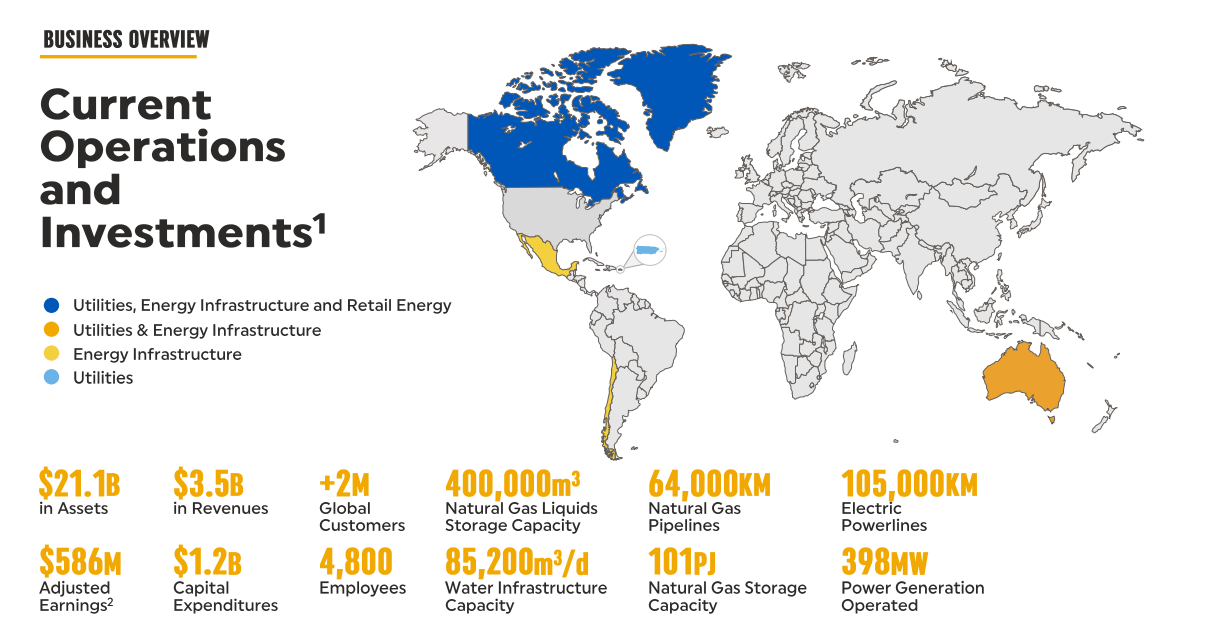

While Alberta forms the bulk of its assets, the company has expanded its footprint across a few different areas of the globe. The map below breaks down how its assets of utilities, energy infrastructure, and retail energy transmission are distributed.

{kind=link}

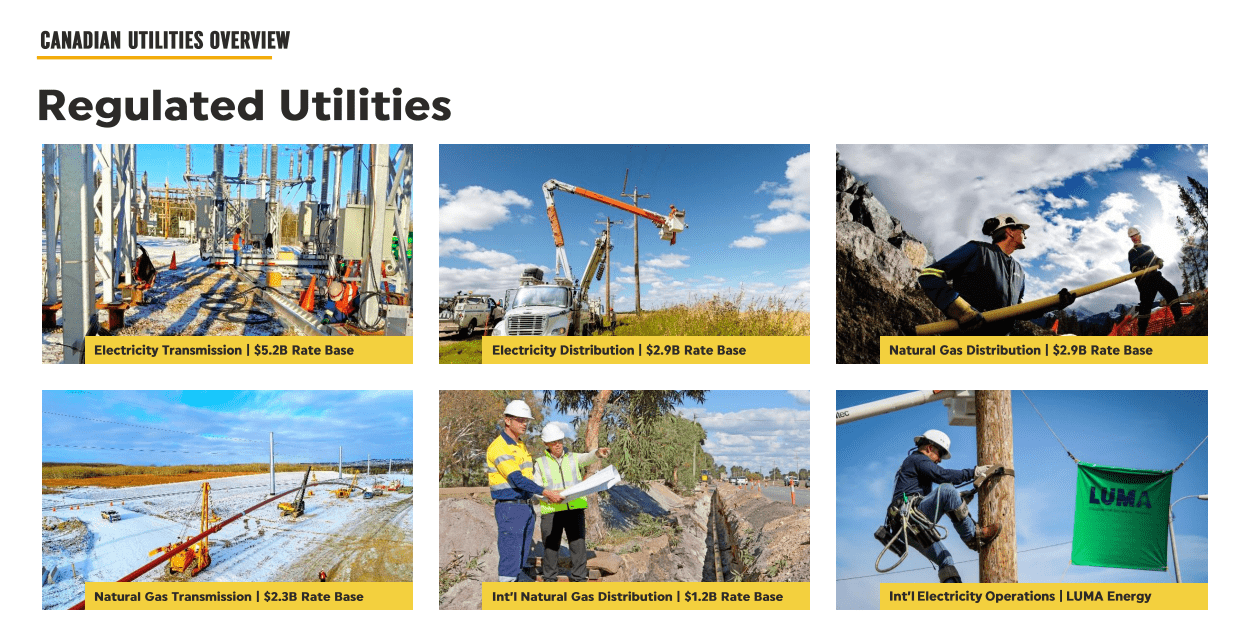

The bulk of these assets and investments earn returns in a safe and highly dependable manner.

{kind=link}

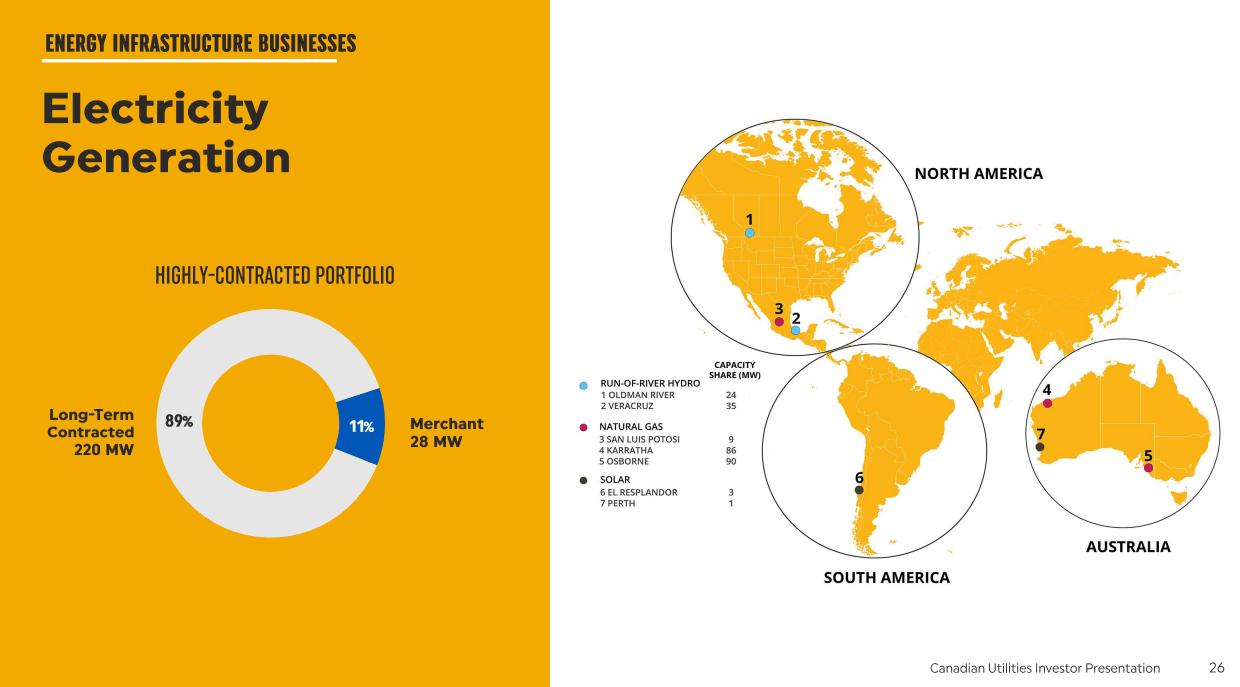

Even on the electricity generation side, the company keeps its exposure to a bare minimum and has contracted the bulk of its production at fixed long-term rates.

{kind=link}

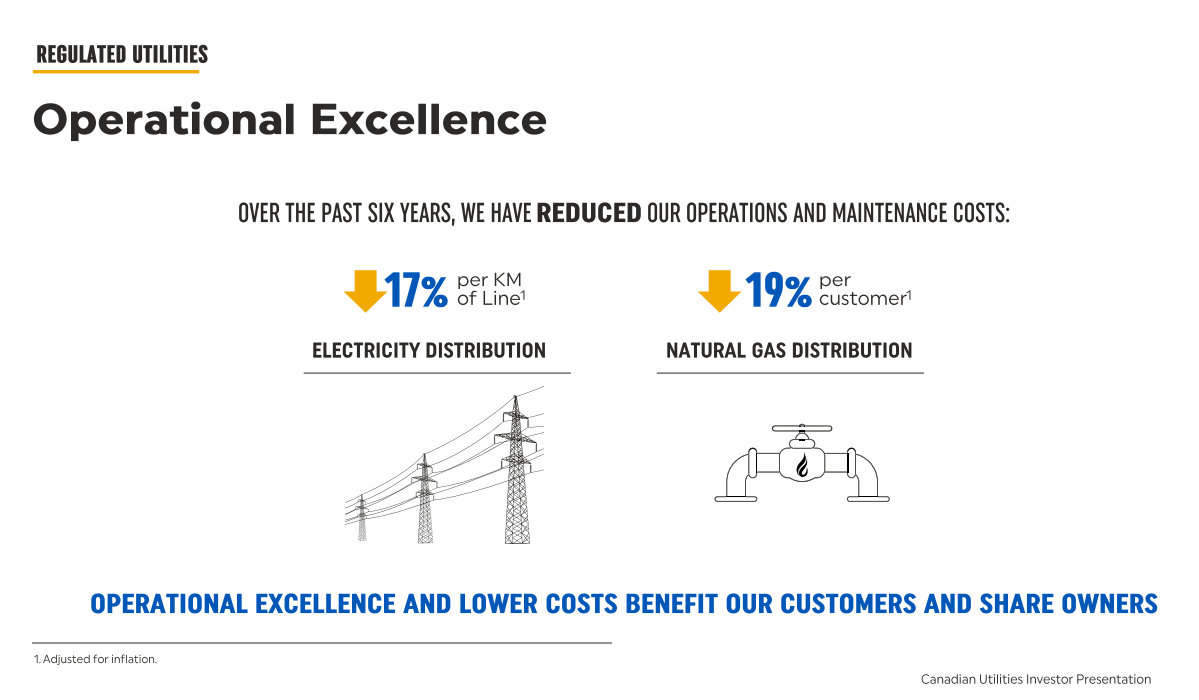

With a fixed base of highly predictable earnings, CU has gone on to invest for growth and capturing returns from a pathway to lower carbon use. This has consisted of becoming more efficient from an operational perspective.

{kind=link}

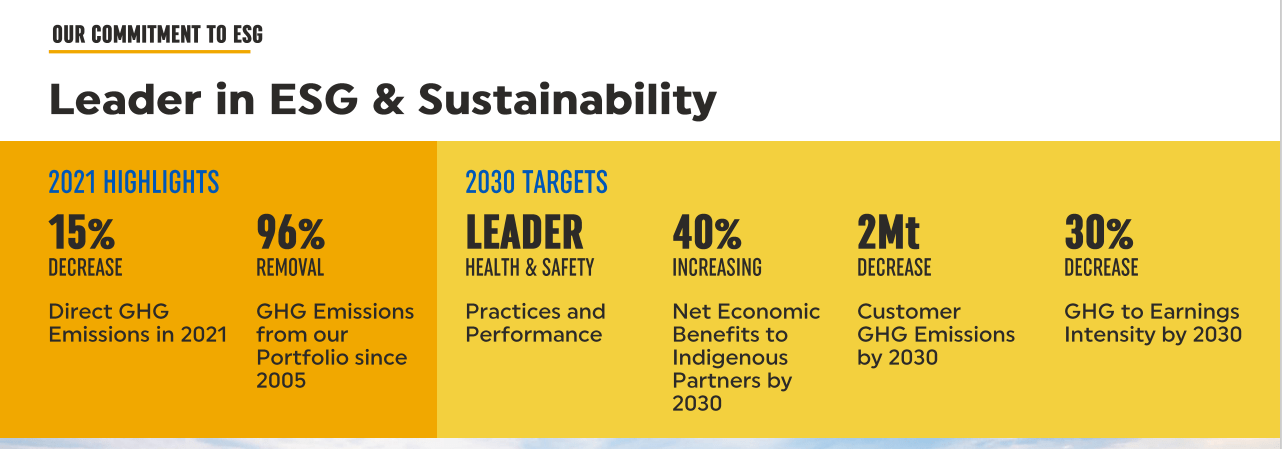

It also has come from increasing green sources of energy while maintaining quality heat and electricity delivery in exceptionally challenging conditions.

{kind=link}

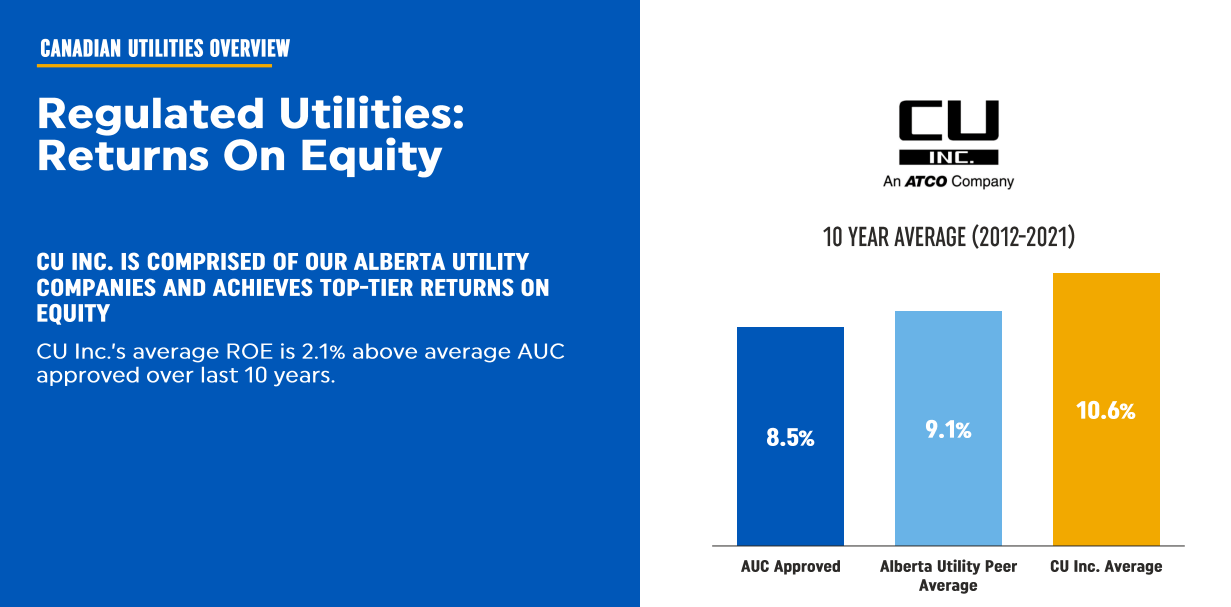

Over time, CU has delivered remarkable returns on equity while having an extremely low beta.

{kind=link}

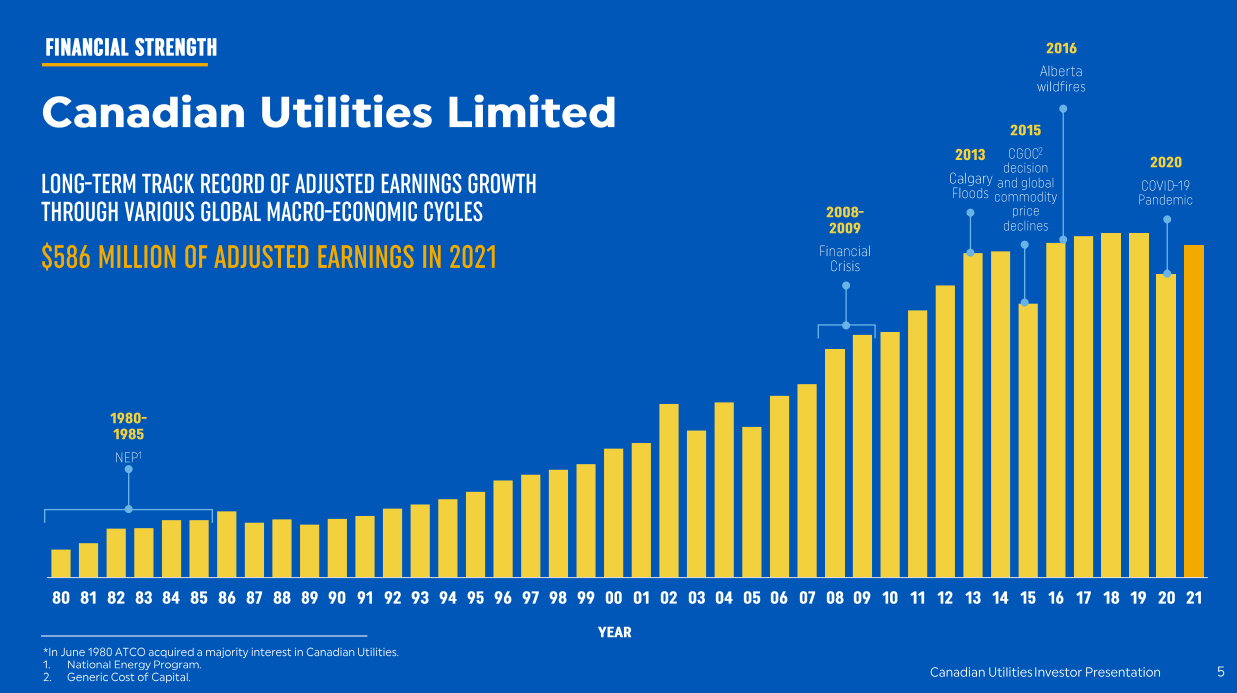

An extension of those returns on equity can be seen in the evolution of adjusted earnings over the last three decades.

{kind=link}

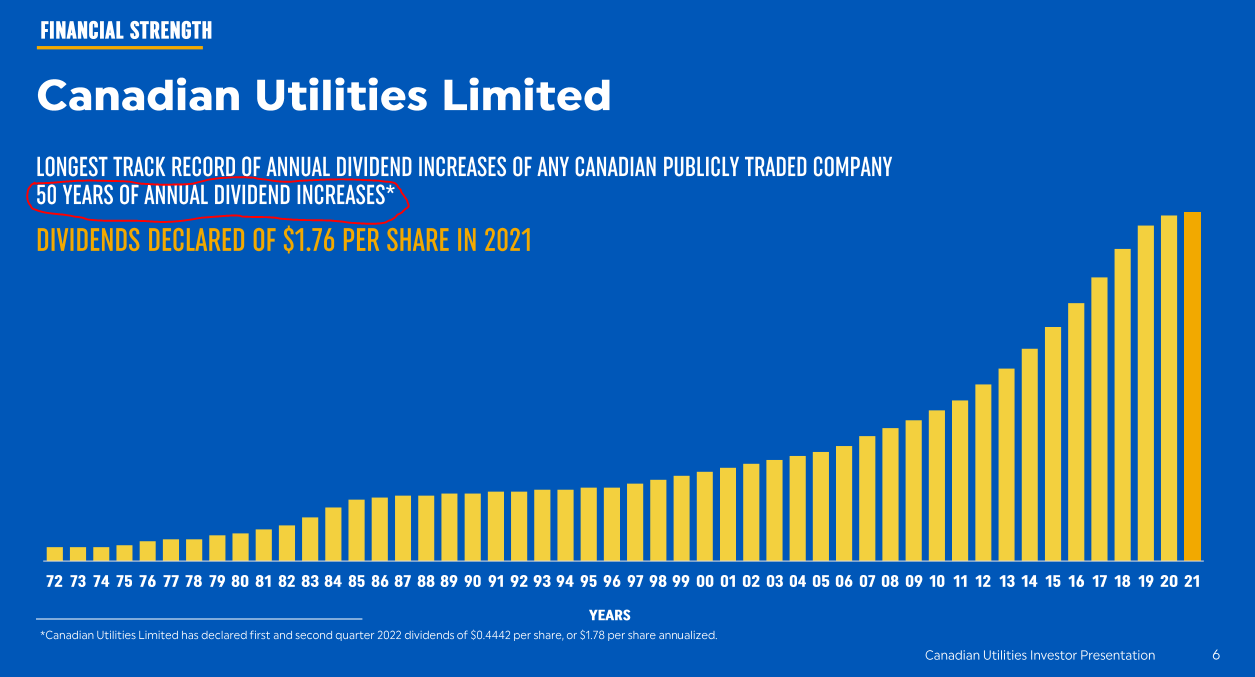

Those consistent earnings have allowed CU to pay out a growing dividend that now has spanned five decades.

{kind=link}

Q3-2022 and Valuation

Too many investors have chased poor returns by stopping their due diligence as soon as they find a long-term dividend growth record. While we get the appeal of a steadily growing dividend, valuation always comes first and one must look at recent results as well as expectations for the near future. In the most recent quarter (Q3-2022), CU delivered one of its best expectation beats by earnings of 45 cents a share (consensus was at 38 cents). This was driven by another strong operational performance in the face of strong inflationary headwinds. Expectations are for about 65 cents in Q4-2022, and CU should land up with about $2.40 for the year. Looking out further, though, CU should make about the same in earnings in 2023 and 2024.

Where's the growth?

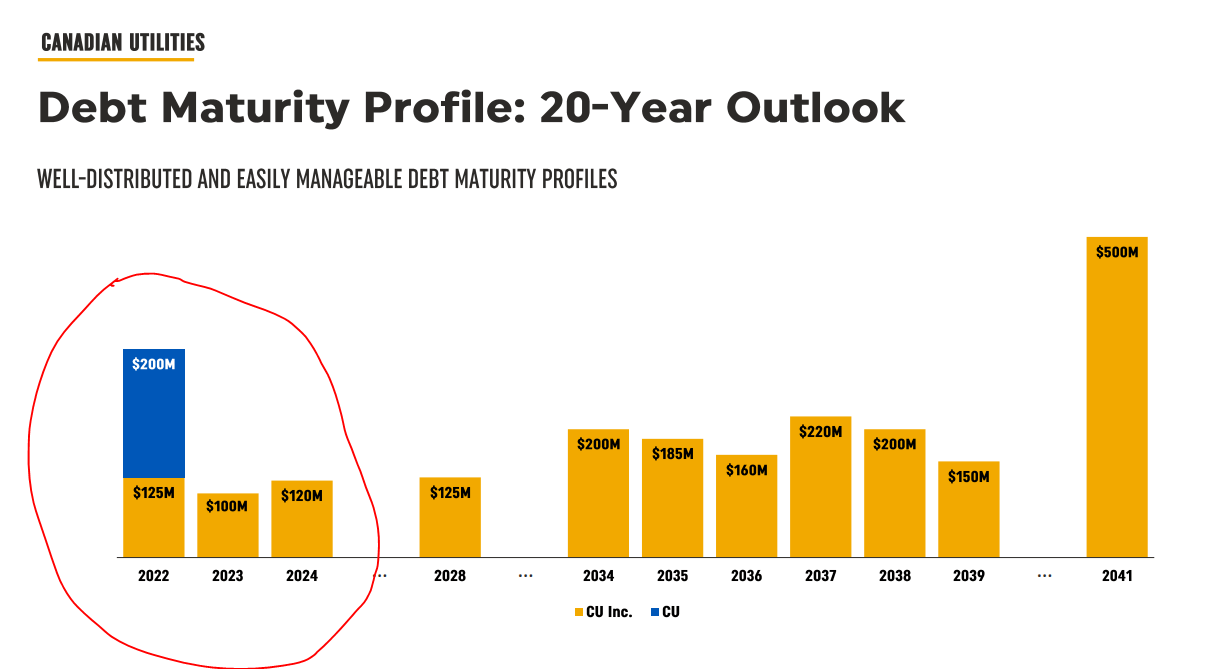

Here lies the lesson of how interest rates can really move to dial even on companies with well-spread-out debt maturities. The headwind to earnings per share comes from the limited refinancing, which will be at higher interest rates, as well as the growth investments which require more debt issuance.

{kind=link}

In fact, CU's EBITDA is expected to grow by about 2.5% in both 2023 and 2024, but earnings will stay flat.

On the valuation front, CU is trading at about 16X earnings, and that multiple is about the same regardless of which year you use for computations. What you have to determine here is whether that multiple is fair for a slow-growth company. Even when CU has adapted to the higher interest rates, your best case is about 3% growth a year. 16X multiple is about fair to us and relative to its Canadian peers, we think CU is slightly undervalued on this metric.

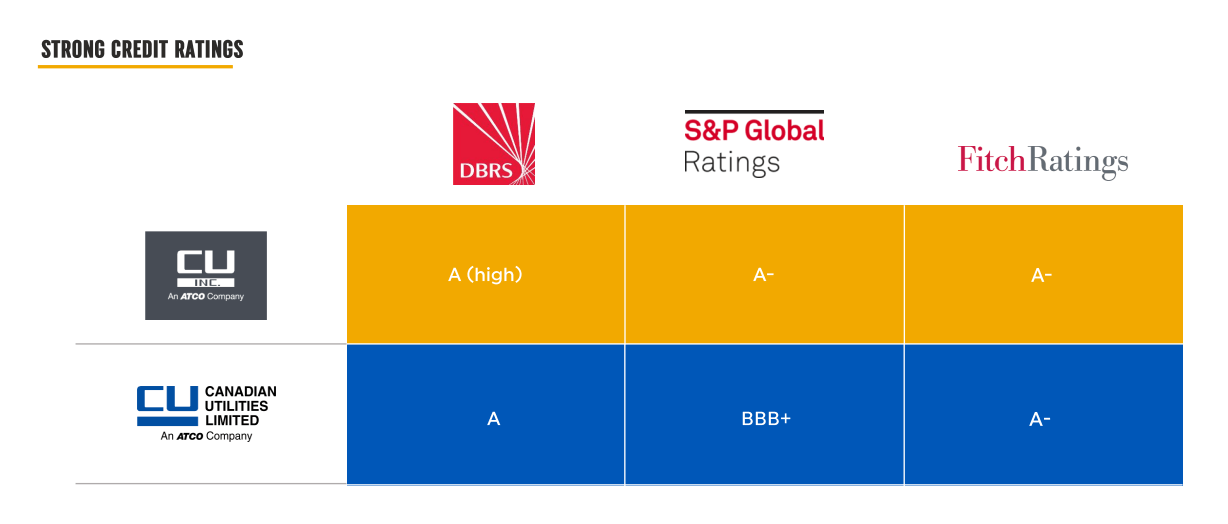

One additional point that helps here is that CU has the lowest debt to EBITDA in this group at 5.2X. Both Emera Incorporated ( EMA:CA ) and Fortis Inc. ( FTS ) are teetering past the 6.0X mark and EMA's risks in particular are quite high . CU's debt ratings are a strong source of comfort here when combined with the relatively lower valuation.

{kind=link}

We think CU makes a solid investment as a utility at the current price. You are likely to get 7% total returns here over the long term, with 5% coming from the dividend and yield.

The Specific Case For ATCO

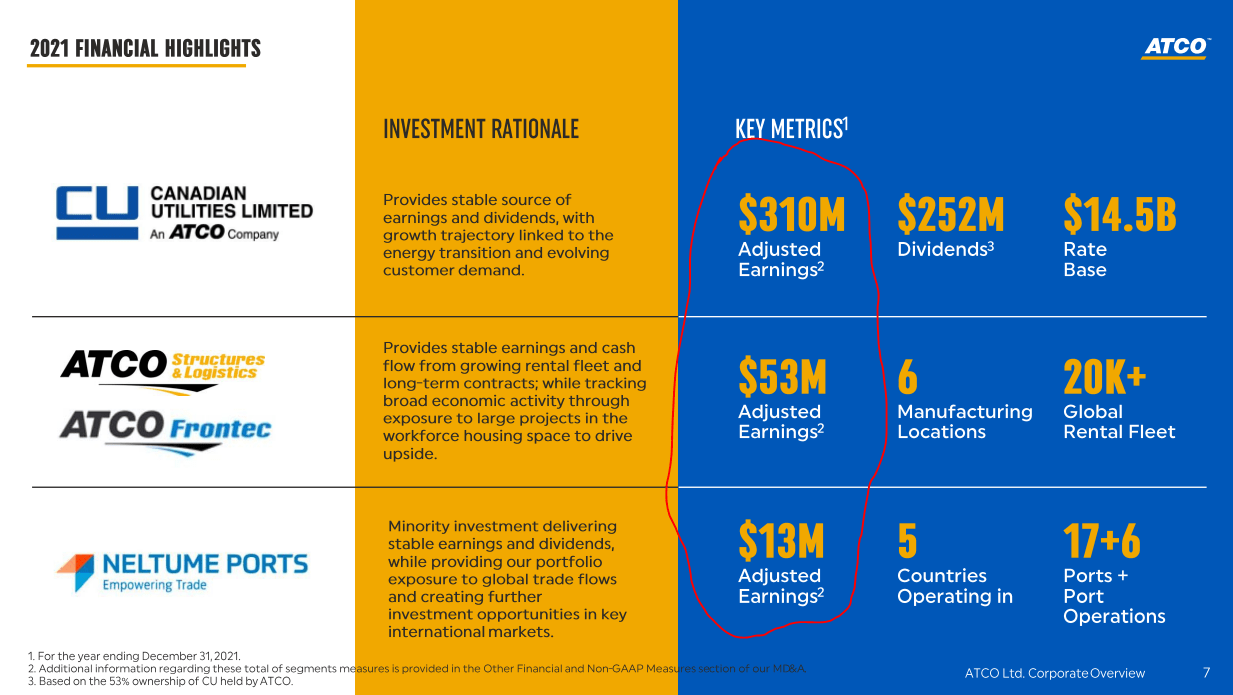

If you like CU, then the natural extension of that is to see if ATCO makes sense as well. As we previously mentioned, the bulk of the valuation for ATCO derives from CU. Added to that are the structure and logistics segment that ATCO owns as well as the investment in Neltume Ports.

{kind=link}

Those two non-utility segments are worth about $1.0-$1.5 billion in our opinion. So the kicker here is that ATCO's current market capitalization is less than even the directly held stake in CU. At about 53% of the $10 billion market capitalization of CU, ATCO should be worth at least $5.3 billion. Instead, it is worth about $4.85 billion.

Occasionally a discount like this has a simple explanation, where the parent carries additional debt beyond the consolidated amount from the daughter company. ATCO does carry about $500 million of corporate-level debt. But that's offset by about $300 million of additional corporate-level cash. Overall, using the sum of the parts method, it appears that at current prices you get the CU stake at a 6% discount and get both the other businesses of ATCO Structure and Logistics and Neltume Ports, for free. Assuming these are worth at least $1.0 billion (the low end of our estimates), ATCO appears modestly discounted here and has a 20-25% upside.

Another way to compare the differences is to look at the P/E ratios. This would adjust for the CU stake as well as the inbuilt discount. We can see that 25% discount in the P/E ratio (12 vs 16) there as well.

Verdict

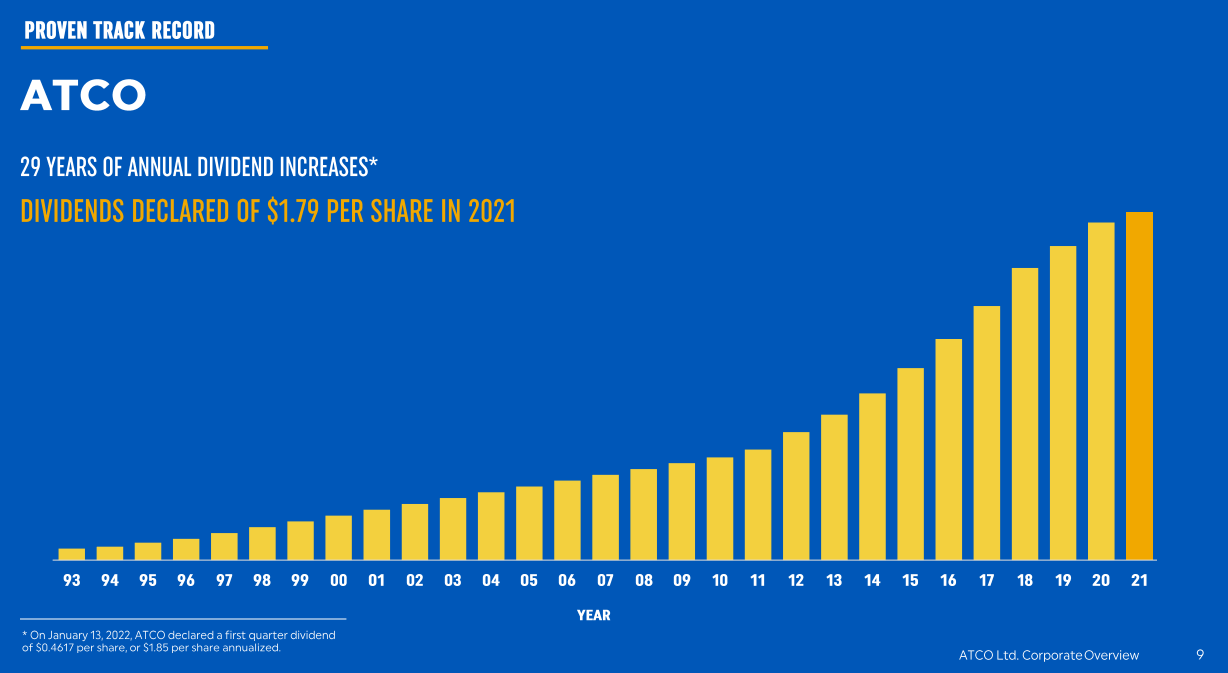

The fast-growing segments of ATCO are unlikely to move the needle any time soon. We certainly would not invest in ATCO for only that side of the equation. But you're getting a discounted utility at a bigger discount, and that's the main appeal. 12X earnings multiples are unheard of within utilities, especially with such low debt to EBITDA. That low debt to EBITDA is the final icing on the cake. As ATCO has additional earnings at the corporate level, its debt to EBITDA whittles down to 4.5X versus the 5.2X for CU. All in, ATCO makes a lot of sense. You do get a slightly smaller dividend.

You also get a slightly less lengthy dividend streak.

{kind=link}

But the total package is way superior. We rate ATCO a Strong Buy at the current price.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

ATCO: Go For The Dividend Aristocrat, Not The Dividend King