SAP - Automatic Data Processing: Limited Upside From Here

Summary

- Automatic Data Processing reported a top-/bottom-line beat in fiscal Q2, with strength in ES offset by softer PEO results.

- The company faces intense competition from peers that may limit market share gains in the future.

- ADP's shares trade at a discount to its peers in the human capital software group.

- I value ADP at 30x my 2024E EPS of $8.9, implying a price target of $267 at the end of fiscal year 2024.

Thesis

Automatic Data Processing, Inc.'s ( ADP ) robust fiscal Q2 result was driven by healthy demand for payroll and human capital management ((HCM)), coupled with a bounce back in international markets. However, softening professional employer organization ((PEO)) services due to a deceleration in worksite employees growth emerged in the quarter.

While I like ADP's execution, defensive growth, and dependable dividend, I remain a bit cautious on the stock given that the company faces digital competition that could intensify and pressure record high retention rates as companies refocus on their vendor strategies after being consumed by surviving the pandemic. However, I still see ADP as a defensive name with little risk to its dividend and limited valuation upside until visibility on a macro recovery is clearer. I value ADP at 30x my 2024E EPS of $8.9, implying a price target of $267 at the end of the fiscal year 2024.

ADP stock price movement (Seeking Alpha)

{kind=link}

Company Outlook

ADP is extending its reach in human capital management on the back of payroll and HR outsourcing ((HRO)) services leadership. Though its next-generation cloud platform provides a more competitive approach to HCM , stronger competition from new entrants in payroll like Paycom Software, Inc. ( PAYC ) and Paylocity Holding Corporation ( PCTY ), cloud-platform companies like Intuit Inc. ( INTU ) and Workday, Inc. ( WDAY ), and enterprise resource planning incumbents like Oracle Corporation ( ORCL ) and SAP SE ( SAP ) limit significant revenue upside. However, steady cash flow, a consistent dividend payout, and high-quality earnings provide support ahead of a potentially softer labor environment.

Q2 2023 Results

ADP Q2-2023 results were largely in line with estimates. The management reiterated their high-level outlook for FY23, but there was an unexpected downward revision for the PEO segment outlook. This is the first negative revision since the pandemic began.

The PEO segment underperformed expectations due to the underestimation of the impact of inflation on WSE volume. As a result, ADP's FY24 total revenue growth has been lowered by 80bps to 6.5%. However, the core ES segment performed better than expected due to strong retention, same-store hiring, and solid bookings, resulting in a raised ES guidance. Management remains optimistic about hitting 2H bookings targets due to the increased demand for HR services, and they have room to invest in GTM, driving significant margin expansion in 2H. While I still believe in ADP's ability to navigate cyclicality under new leadership, I remain cautious due to PEO outlook.

PEO Disappoints, Core ES Business Remains Strong

ADP lowered its full-year PEO revenue growth guidance from 10-12% to 8-9%. I believe that medical benefit renewal trends are the likely culprit for the slowdown.

For perspective, ADP's PEO business offers medical benefits to clients' employees. Upon annual renewal, carriers (e.g., insurance companies) notify ADP of price increases that ADP ultimately passes through to clients. This year, carriers are raising prices by more than the typical rates. This inflation is driven by a return of demand for doctor visits and special procedures like elective surgeries, both of which were often postponed during the pandemic. As a result, some clients are opting to shop for cheaper medical plans vs. the prices that ADP is passing through, which can drive lower retention.

Additionally, it is to be noted that PAYX also saw a significant slowdown in PEO growth (+4% in November quarter vs. +8% in the August quarter). Their management said that the growth rate was "tempered by the impact of... lower medical plan attachment and participant's volumes along with a mix-shift to administrative services organization ((ASO))."

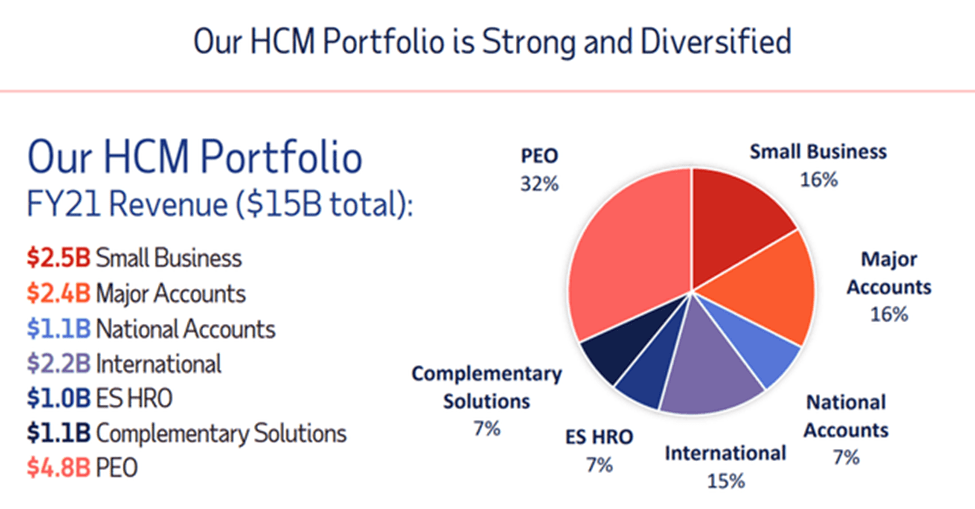

HCM Portfolio of ADP (Company Presentation)

{kind=link}

Valuation

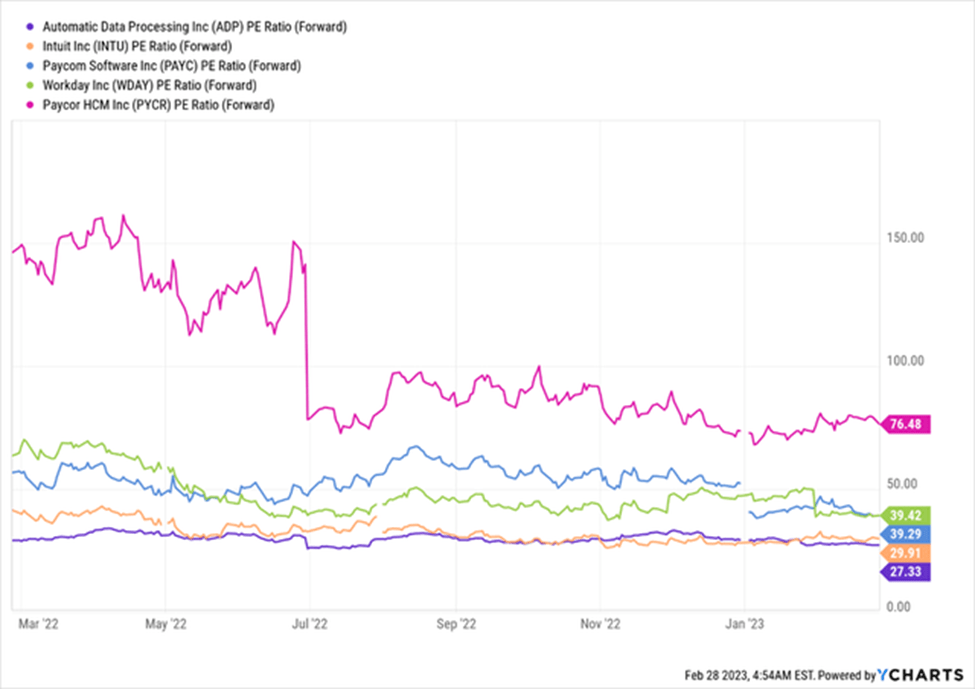

ADP's shares trade at a discount to its peers in the human capital software group, justified by its slower revenue growth of 7.3x, a higher mix of service-related business, and lower operating margins. However, I believe that improved Enterprise execution, a closing organic growth gap vs. high-flying peers. I value ADP at 30x my 2024E EPS of $8.9, implying a price target of $267 at the end of the fiscal year 2024.

ADP valuation metric vs peers (YCharts)

{kind=link}

Final Thoughts

Automatic Data Processing, Inc. has revised down a portion of its outlook for the first time since the pandemic began. I believe this is because they underestimated the impact of inflation when they reiterated their WSE growth guidance last quarter. This may be due to cost-conscious SMBs (small and medium-sized businesses) delaying their purchasing decisions and higher healthcare prices pushing up attrition. This does not seem to be a competitive issue but rather a combination of tough comparisons and uncertainty in the macro environment. The outlook implies F2H WSE growth of 3-5%, which is below the high-single-digit mid-term target, but management remains confident in repositioning for growth beyond FY23.

Although Automatic Data Processing, Inc.'s payroll services are a critical differentiator that could lead to cross-selling opportunities for HCM modules, share gains will be strongly challenged by Workday, Paycom, Paylocity, and other cloud-software app providers. However, ADP's predictable cash-flow generation, dividend yield, high earnings quality, and targeted shareholder return create a defensive stock position. ADP stock is currently trading at a discount to peers, and I maintain a hold rating on Automatic Data Processing, Inc. stock with a price target of $267 for next year.

For further details see:

Automatic Data Processing: Limited Upside From Here