CA - Automotive Properties: A REIT We Can Get Behind At The Right Price

Summary

- This REIT started in 2015 and has done a good job in diversifying its tenant base.

- Its books are in order and its lease maturity schedule is reassuring.

- We review this one for the first time on this platform and provide our thoughts (for more than a penny).

All values are in CAD unless noted otherwise.

Automotive Properties REIT ( APR.UN:CA ) owns and manages income producing automotive properties comprising retail dealerships, service and repair centres, and vehicle service compound facilities. The 2.7 million square feet of gross leasable area [GLA] is located in metropolitan areas across a host of provinces.

The REIT will be nicknamed "Auto REIT" for the remainder of the article.

Automotive Properties

The REIT started in 2015 with 26 properties and has been on a growth spree making 46 acquisitions along the way. It buys properties from automotive dealers enabling them to redeploy the liquidity to enhance their business operations, which they retain ownership and control of. It also meets the needs of dealerships wanting to crystallize the value of their properties for matters such as succession planning. Based on Auto REIT's estimates, there is a lot of untapped market in this regard, with the top-10 automotive dealership groups owning only around 12% of the approximate 3,500 dealerships in Canada.

2022 Investor Presentation

Auto REIT has triple-net leases with its tenants which means that the tenants are responsible for all costs associated with running the property except for structural capital improvements. It also has annual contractual rent increases built in across its portfolio. While not all the increases will keep up with inflation (some actually do track CPI), they do provide some protection from it.

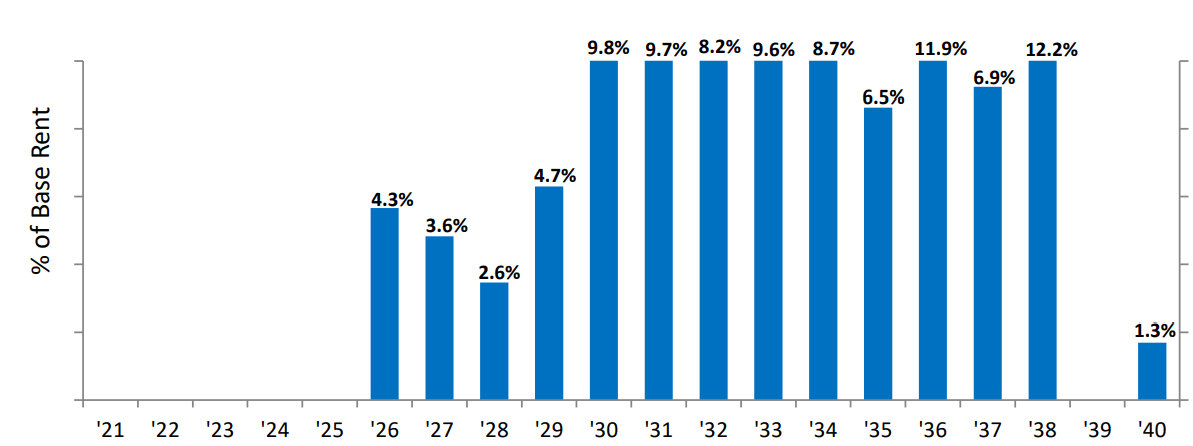

With a weighted average lease term of 11.1 years, the first of Auto REIT's maturities come up in 2026.

{kind=link}

Q2-2022 MD&A

Related Party, Also Primary Tenant

Auto REIT started off with only one tenant, The Dilawri Group, Canada's largest automotive dealership. It purchased the aforementioned 26 properties from this group and leased those back to them. While it has added more tenants along the way, it still receives around 59% of its base rent from Dilawri. We mentioned annual contractual rent increases earlier in this piece, which in this tenant's case is 1.5%. A few things work in the REIT's favor despite the tenant concentration.

1) Dilawri has skin in the game as it owns a 30% interest in the REIT via partnership units in a subsidiary, along with the trust units. The partnership units are economically equivalent to the trust units and are exchangeable on a one-for-one basis.

2) As long as Dilawri continues to have at least a 10% interest in the Auto REIT, the REIT has the first right to purchase any property acquired, developed, redeveloped, refurbished, repositioned or held for sale by Dilawri in Canada or in the US. Point to note, the property should be suitable for use as an automotive dealership for this to apply.

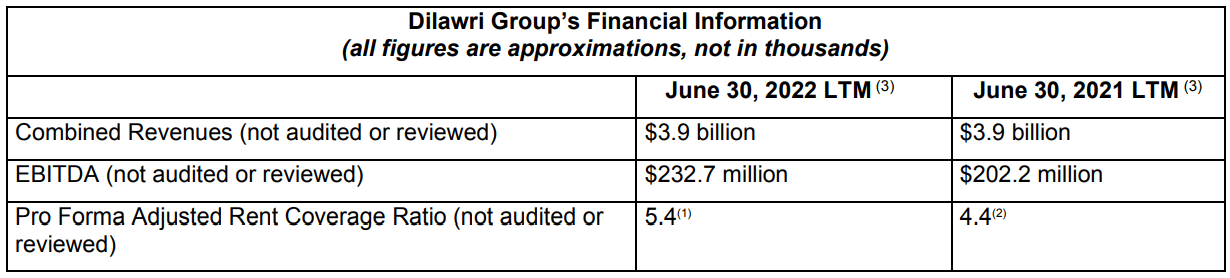

Dilawri, in conjunction with an increase in EBITDA, also had a comfortable 5.4X rent coverage ratio for the annual period ended June 30, 2022.

{kind=link}

Q2-2022 MD&A

Still Dilawri occupies more than 50% of its properties (36 exclusively and two jointly occupied with a third party out of the 72 total) and Auto REIT must be looking to get a crack at the 3100 odd properties that are outside the purview of the top 10 automotive dealerships.

Debt

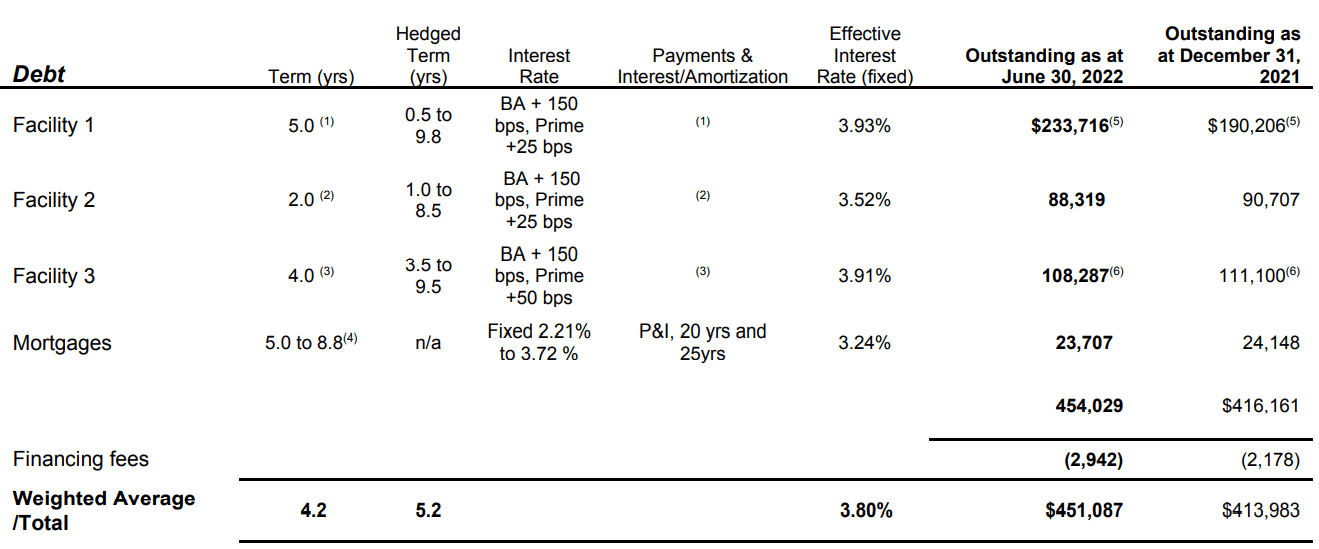

In terms of debt, Auto REIT has credit facilities and mortgages on the books, all of it secured by 62 out of its 72 properties.

{kind=link}

Q2-2022 MD&A

The increase from 2021 is as a result of property acquisitions this year. We can also see the impact of the new borrowings in the higher effective interest rate which was 3.72% for 2021. Predictably, both their interest (3.7X vs 3.8X) and debt service (1.7X vs 1.9X) coverage ratios were lower, albeit minorly, compared to the prior period.

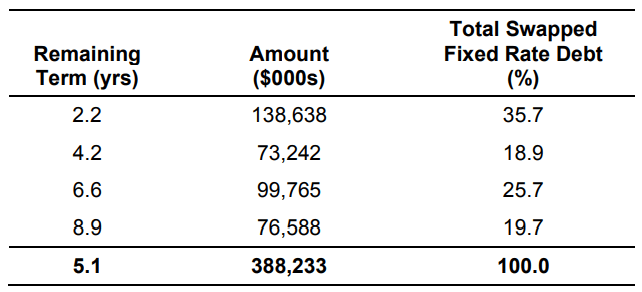

The majority of its debt is from variable rate credit facilities, however, most of the drawn amount is hedged via interest rate swaps. Out of the $430 million drawn from the credit facilities, $388 million is effectively fixed.

{kind=link}

Q2-2022 MD&A

91% of their total debt had a fixed rate (including swaps) as at the end of Q2 2022.

Liquidity

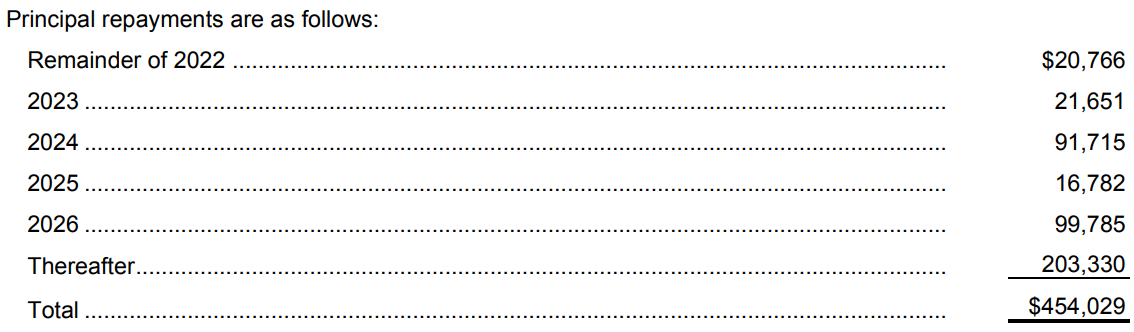

As of June 30, Auto REIT had about 10% of its debt, or $43 million, due by the end of 2023.

{kind=link}

Q2-2022 MD&A

It had about $75 million undrawn capacity under its credit facilities, 10 unencumbered properties valued at approximately $122 million, and $175 thousand cash at the end of Q2. They have ample resources to take care of their obligations for the next couple of years. While Auto REIT is cognizant of the importance of liquidity in the current environment, management did note that they would go in for additional borrowings or equity issuances as growth and development opportunities arise.

Their debt to gross book value ratio was 41% at the end of Q2 and they do have covenants in place which prevent further borrowings if this ratio exceeds 65% (including convertible debentures).

Distributions

The REIT distributes $0.067/month and currently yields 6.4% ($12.53 price at the time of writing this article). With an adjusted funds from operations or AFFO payout ratio of 88%, the distributions are well covered and safe in our opinion. The AFFO payout is subject to covenants with respect to the credit facilities.

{kind=link}

2022 MD&A

The AFFO payout ratio for the rolling four quarters was 89.7%, so well in compliance with the applicable covenants.

Q2-2022 Results

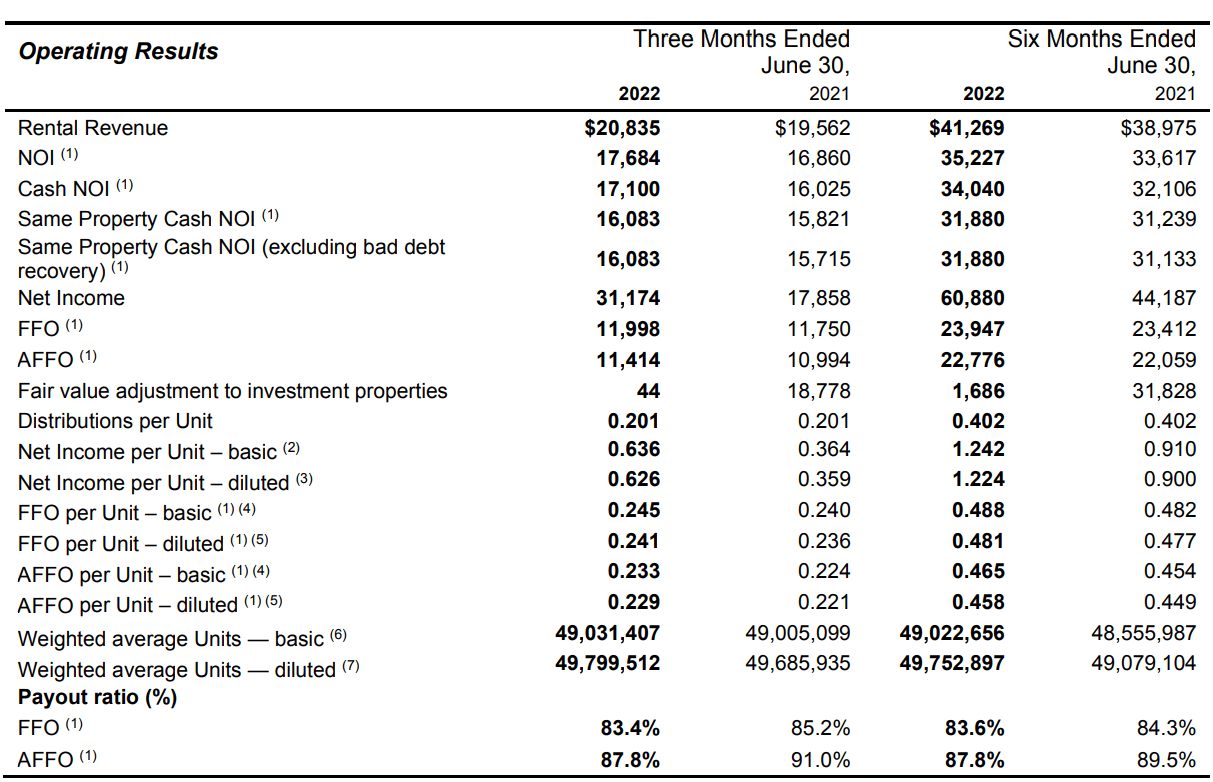

Buoyed by the properties acquired this year and the annual contractual rent increases for pre-existing ones, the funds from operation or FFO was higher than the comparative periods.

{kind=link}

Q2-2022 MD&A

There was a slowdown of the fair value increases to the properties in 2022 with the Q2's minor increase pretty much being the difference between an increase due to the contractual rent and write down of the fair value of the properties. The overall capitalization rate went up from 6.25% in Q1 to 6.30% in Q2.

Verdict

Auto REIT is one of the steadiest REITs we cover. The large dealerships are not fungible with other retail locations and the tenants are there for the long haul. The key challenges for the entire sector come from a move to electric vehicles and whether that can be done smoothly while maintaining profit margins. Currently, auto inventories across North America are very low and dealerships are swimming in cash. So, the challenge we describe above, is a bit far away. One other fact about these dealerships is that they are often located in prime areas and have a lot of valuable land underneath them. Of course, all retail locations are built on land (none float in the sky), but our point is that in the rare chance a tenant goes under, the value of that land is a rather huge buffer for Auto REIT. Concentration in one major partner is a risk, we saw that with another REIT we have previously covered, Granite REIT ( GRP.U ). But just like with GRP.U, the partner has a solid foundation, and we think of it as a positive. We own the stock currently and rate it as a Hold. We would buy under $12.00.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Automotive Properties: A REIT We Can Get Behind At The Right Price