CURLF - Avoid Verano For Now

2023-11-26 22:59:25 ET

Summary

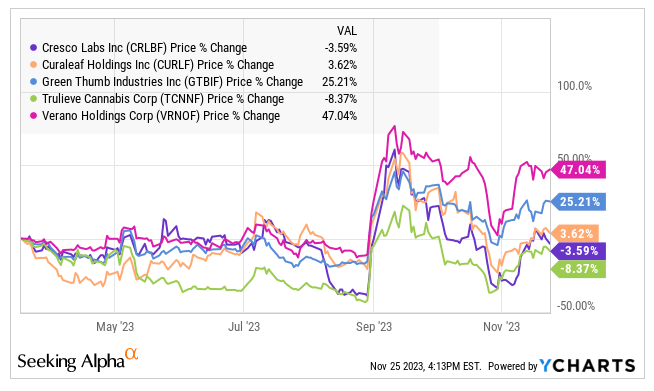

- Verano Holdings has outperformed its peers with a 47% rally since mid-March, leaving the stock up 40.7% year-to-date.

- The company reported Q3 revenue slightly below expectations but adjusted EBITDA was better than expected.

- Analysts project lower revenue and adjusted EBITDA for 2023 and 2024, but the stock's potential depends on the elimination of 280E taxation.

- There are superior choices among MSOs and better risk-reward opportunities outside of MSOs.

Verano Holdings ( VRNOF ) has done much better since I warned about it in mid-March. In fact, it has done substantially better than its four large peers too:

{kind=link}

The 47% rally leaves the stock up 40.7% year-to-date. 3 of the 5 are down in 2023, and Verano has rallied more than twice as much as Green Thumb Industries ( GTBIF ), which is up 18%.

In this follow-up eight months later, I review the fundamental performance, share the analyst outlook, look at the chart, and assess the valuation.

2023 So Far

The company reported its Q3 on November 5th. Analysts, according to Sentieo, were expecting revenue of $241 million with adjusted EBITDA of $75 million. Verano reported overall revenue of $240.1 million, up 5% from a year ago and slightly below expectations. Adjusted EBITDA, on the other hand, was a lot better than expected at $89.3 million, up 9% from a year ago.

For the year, revenue for the first three quarters of $701.3 million has grown 7% from 2022's first three quarters. Wholesale revenue (after intersegment eliminations) has been $145.0 million, up 21%, while retail has been $556.3 million, up 4%. Analysts applauded, and I really appreciated, the company for providing a state-by-state summary of the financials in the press release. Wholesale sales are at least 10% of overall wholesale revenue in three states, including New Jersey, Illinois, and Connecticut. On the retail sales front, Florida, at $162.3 million, is the biggest state, while New Jersey and Illinois are quite large too.

Operating cash flow for the quarter expanded by $36.6 million as the company's income tax payable expanded. Capital spending increased by just $10 million. So far in 2023, operating cash flow has been $77.4 million. Free cash flow is positive, since capital spending has been $26.5 million, down substantially from the first three quarters of 2022. The operating cash flow has been helped by falling inventory.

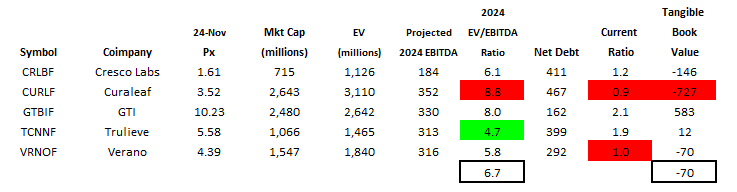

The balance sheet is concerning. The company reported tangible equity at -$70.0 million. It has net debt of $292.3 million, a bit better than at year-end. This does not include the income tax payable of $251 million or the deferred income taxes of $183.3 million. The ratio of current assets to current liabilities is a low 1.0X.

The Outlook

Ahead of the Q3 report, analysts were expecting 2023 revenue of $948 million with adjusted EBITDA of $294 million. Now, the projected revenue will increase by 7% to $937 million, a bit lower. They expect adjusted EBITDA to fall for the year by 6% to $305 million, a bit higher than before. In that piece I wrote in March, analysts at the time were expecting 2023 revenue of $1.01 billion with adjusted EBITDA of $348 million. So, the estimates have been significantly lower since then.

For 2024, analysts were projecting revenue of $1.041 billion with adjusted EBITDA of $334 million, a margin of 32.9%, in early November. Now, they expect revenue to grow 5% to $985 million with adjusted EBITDA of $316 million. These are both lower than the prior estimates ahead of Q3.

For valuation purposes, I rely upon the 2025 estimates, as a year from now, this will be the one-year forward numbers. Ahead of the Q3 report, 3 of the 10 analysts that covered the stock were expecting revenue of $1.098 billion with adjusted EBITDA of $357 million, a 32.5% margin. Now, 5 analysts project that revenue will increase 7% to $1.049 billion, a bit lower than previously. They expect adjusted EBITDA will rise 9% to $344 million, a margin of 32.8%. This seems too high to me, and I am assuming that the company will be at 31.0%, or $325 million. The analyst consensus, if achieved, or even my lower assumption would be a record for the company, exceeding the $324 million from 2022.

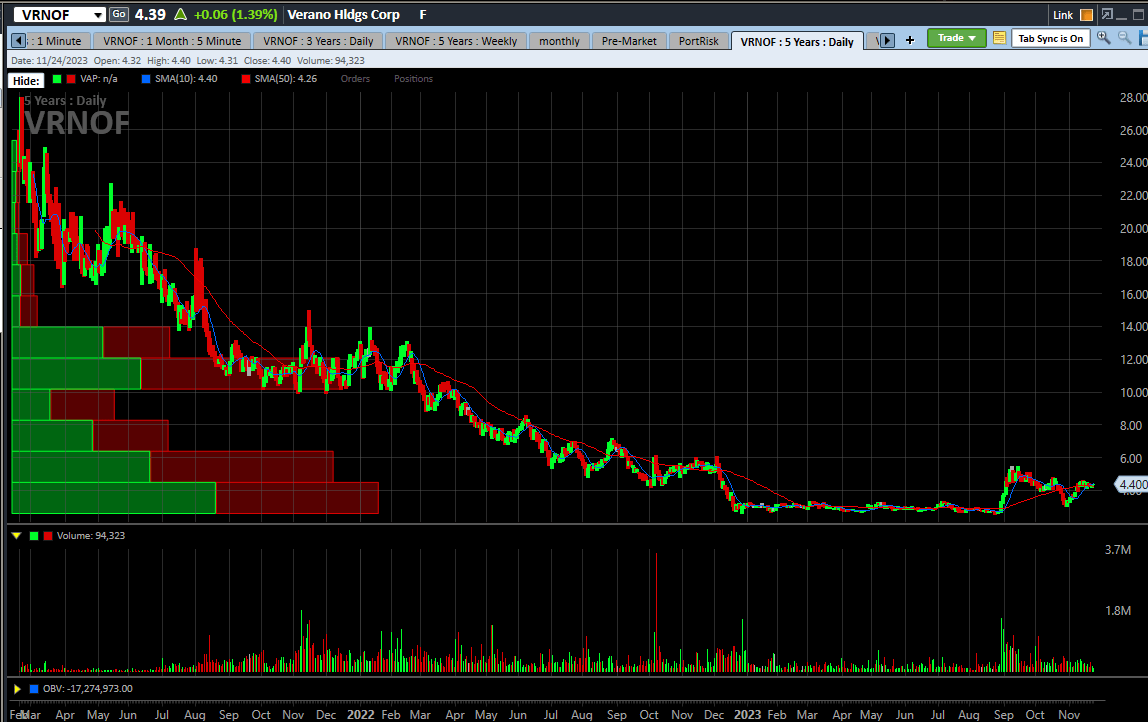

The Chart

Verano has pulled back a lot from its early 2021 levels, as have cannabis stocks in general. The stock created a big bottoming base from late December into the end of August, riding the potential rescheduling news much higher and then pulling back to the base:

{kind=link}

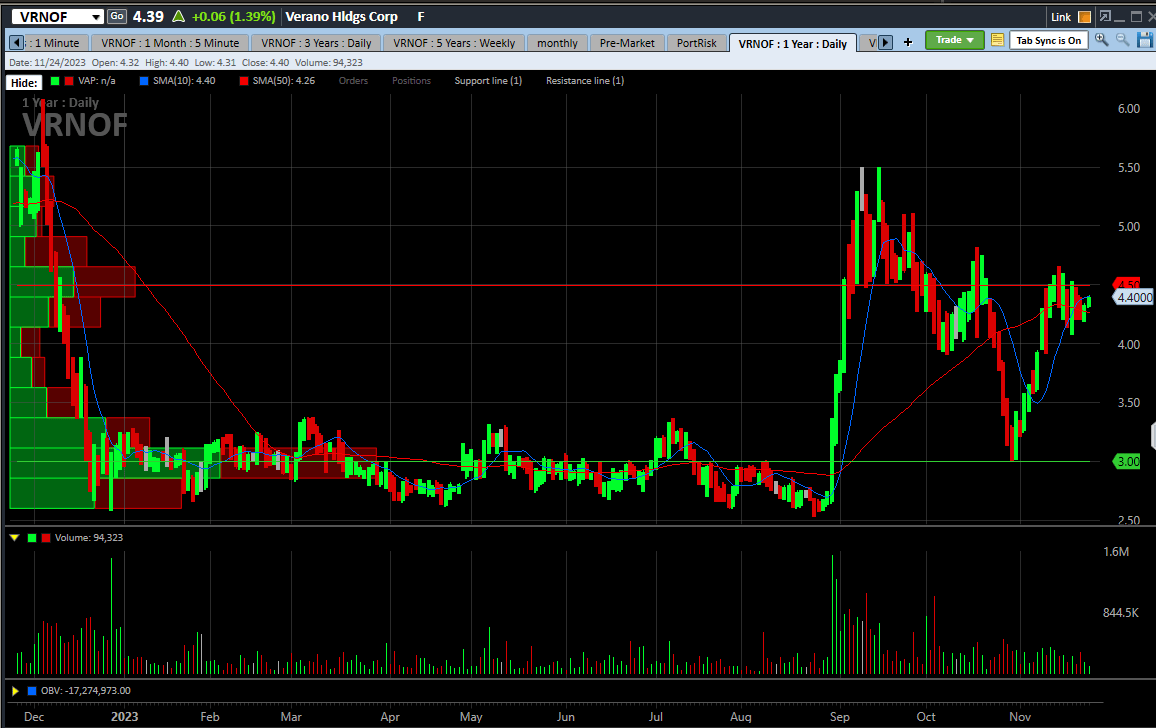

Taking a look at the past year, the sharp sell-off last December and the big move up in late August and early September are evident:

{kind=link}

While the stock has traded higher recently than the resistance I see at $4.50 and below the support I see at $3.00, I think these high-volume trading areas are important to watch.

Valuation

Verano is not the most expensive large MSO, as that is Curaleaf ( CURLF ). It's also not the cheapest, as that is Trulieve ( TCNNF ). Here is the enterprise value to projected adjusted EBITDA for 2024 for these three as well as Cresco Labs ( CRLBF ) and GTI:

{kind=link}

Verano has a low current ratio and negative tangible book value, but its valuation is below average for the group.

The target that I shared with my Investing Group subscribers ahead of the report was based on an either-or scenario. I shared that if 280E goes away due to rescheduling to Schedule 3 from Schedule 1, then my target at year-end 2024 would be $6.86. If it doesn't go away, then my target would be $2.04 as the company struggles with its debt. Updating those for the capital structure and the estimates changes, my bullish target, based on achieving an enterprise value to adjusted EBITDA for 2025 of 8X, is now $6.53, up 49%. I think that this target is likely conservative and the returns could be higher. My bearish target, based on 3X, is now $1.93, down 56%. My targets for Trulieve that I shared last week are based on similar metrics but show more upside and similar downside.

Conclusion

I have been wrong about the price action of this stock, as it has rallied a lot despite lower forward estimates. The rally has been due to the potential rescheduling of cannabis, which could wipe out the onerous 280E taxation.

I don't include Verano in either of my model portfolios. I think that there are better choices among the MSOs, and there are much better deals in other sub-sectors, like ancillaries or Canadian LPs. Still, though, I recognize that Verano will likely go up a lot if 280E gets eliminated. My view, though, is that there are better MSOs to own in that scenario, like Trulieve.

For further details see:

Avoid Verano For Now