CA - Aya Gold & Silver: Industry-Leading Growth At An Attractive Price

2023-09-14 13:00:26 ET

Summary

- Aya Gold & Silver Inc. is a small-cap silver producer that is on track to complete a major expansion next year.

- The company owns the Zgounder Mine in Morocco, has an impressive development asset in Boumadine, and has several other exploration projects.

- In this update, we'll dig into Aya's investment thesis and whether the stock is offering a margin of safety after its ~40% correction.

It's been a rough three years for most precious metals stocks, with the Silver Miners Index ( SIL ) having a negative 50% 3-year return and even some of the larger producers sitting over 40% below their 2020/2021 highs. However, one name that has bucked this trend is Aya Gold & Silver Inc. ( AYASF ), a small-cap pure-play silver producer based out of Morocco that boasts one of the highest growth profiles sector-wide. Benoit La Salle (former founder of Semafo, which was built into a billion-dollar dual-asset gold producer in West Africa and eventually sold in 2020) leads the company, and while it screens as expensive on cash flow and revenue, Aya plans to quadruple production once its Zgounder Mine Expansion is complete, growing into an ~8.0 million ounce silver producer by 2025. Let's dig into the company a little more below:

Zgounder Mineralization - Company Report

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Zgounder Mine & Assets

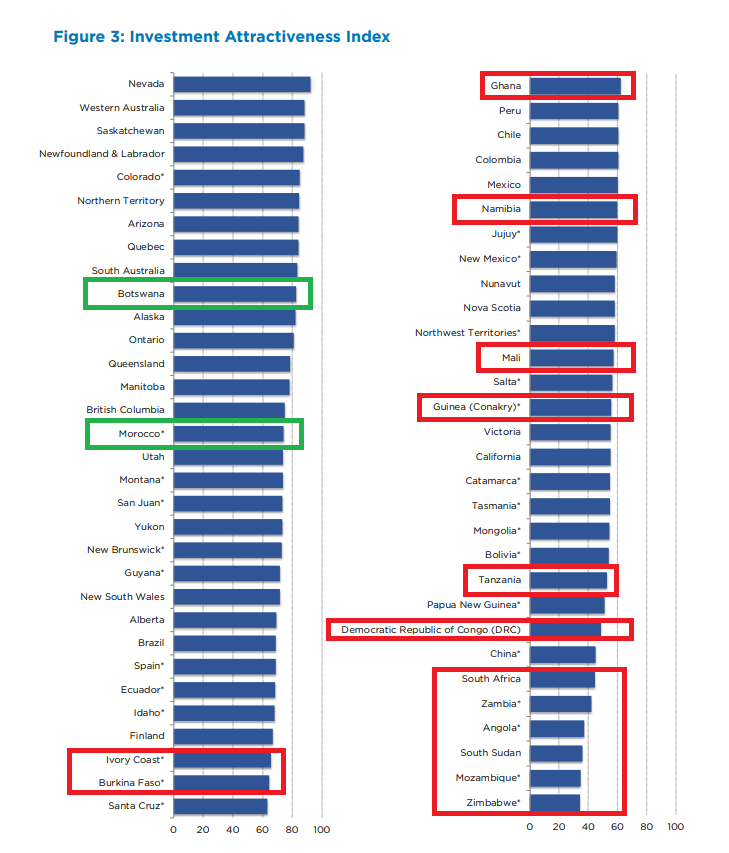

Aya Gold & Silver ("Aya") owns the Zgounder Mine in Morocco, multiple other exploration/early-stage development projects, and the small but high-grade Tijirit Project in Mauritania (25 kilometers southeast of Kinross' massive Tasiast Mine). This jurisdictional positioning may turn away many investors, but it's important to note that Morocco is one of the highest-ranked jurisdictions from an investment attractiveness standpoint within Africa and Mauritania also stacks up relatively well, coming in well ahead of Burkina Faso, Cote d'Ivoire, Mali, Namibia, Guinea, Tanzania, Sudan, and several other jurisdictions according to the Fraser Mining Institute. Morocco's attractiveness stems from:

- significant silver endowment (Africa's #1 silver producer) with major untested potential given limited drilling done along the ~600 kilometer Anti-Atlas Fault

- low discovery costs relative to more prolific jurisdictions (~$120/meter drilled vs. $250/meter in most Tier-1 jurisdictions and ~$400/meter drilled for more remote locations)

- favorable permitting timelines with Zgounder Mine Expansion permitted quickly in Q1-22 and politically stable with a constitutional monarchy

- availability of skilled labor with Morocco being a major phosphate producer, in addition to access to grid power

- a mining code that encourages investment, with new mining code proposing a 15% free-carried interest and a 3% NSR royalty, with the government being open to a buyback of the 15% interest

- a 5-year tax exemption on new mining projects, and 20% tax rate thereafter.

Fraser Investment Attractiveness Index - Fraser Institute Annual Survey 2022

{kind=link}

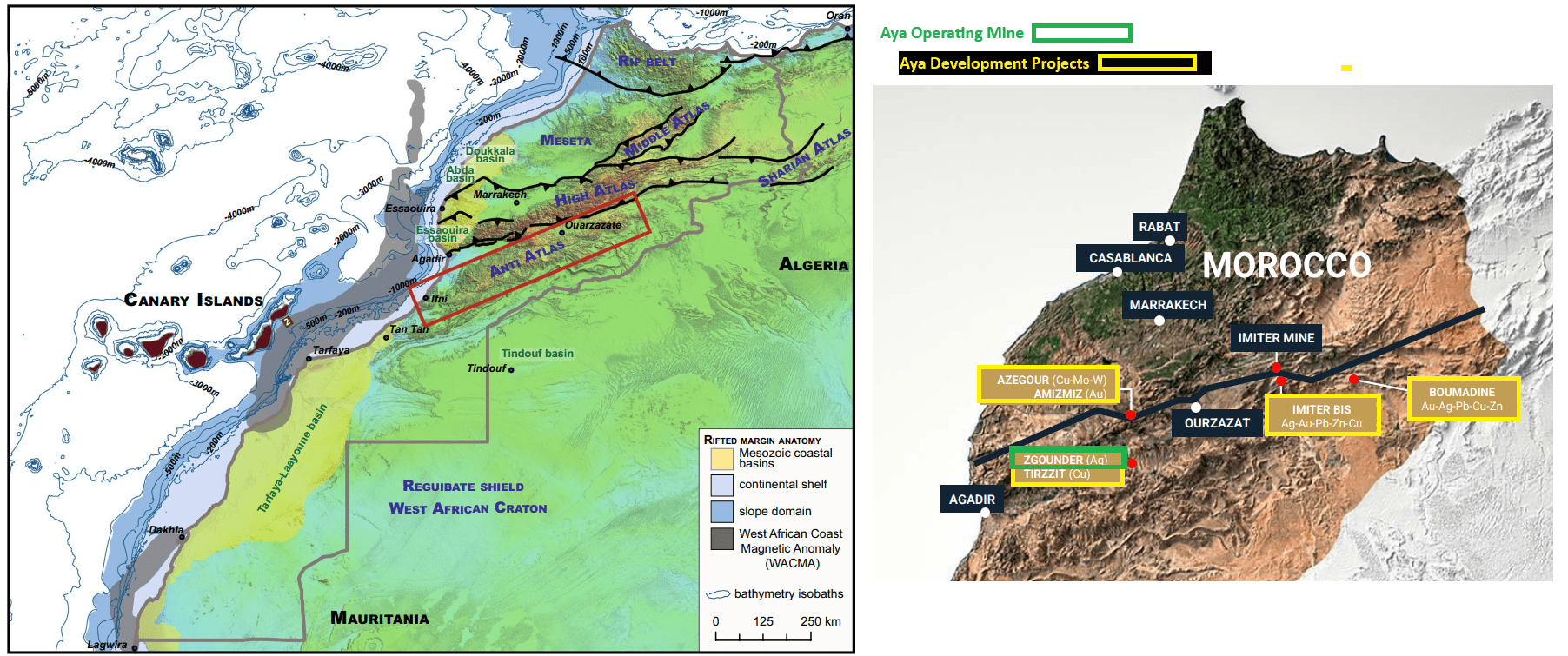

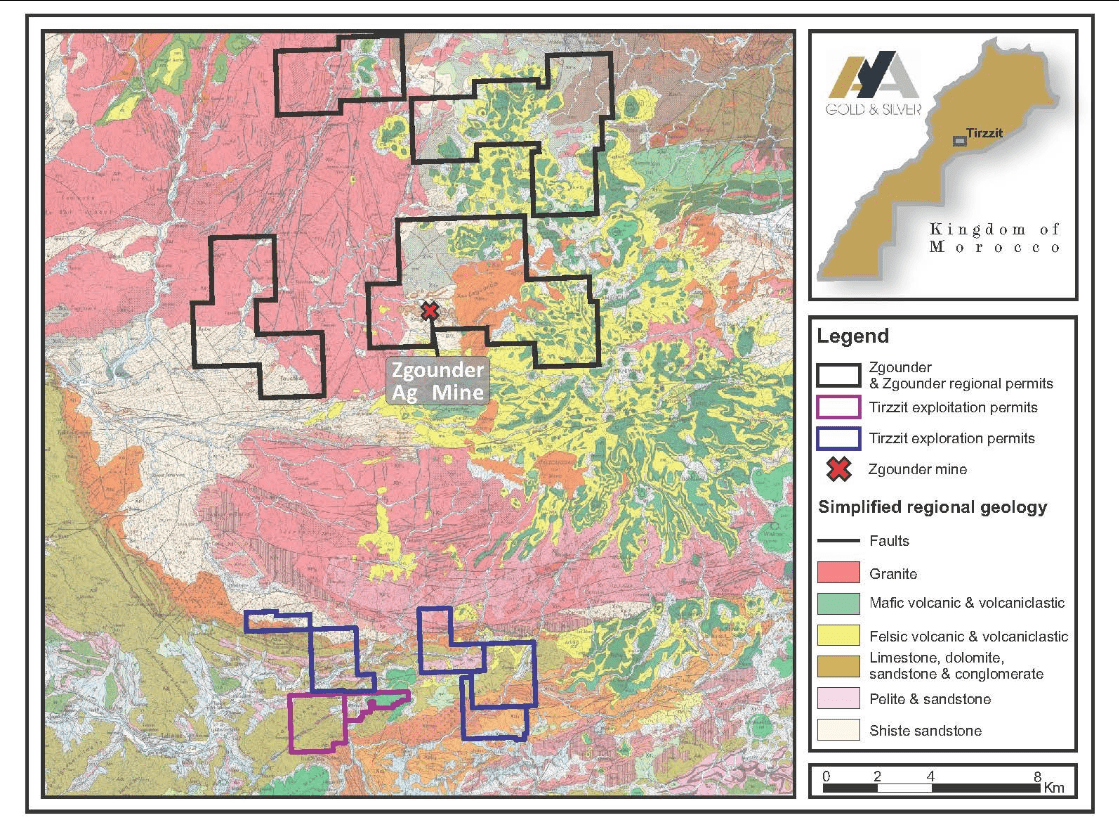

These attributes make Morocco a standout jurisdiction within Africa, and according to the Fraser Institute, Morocco is actually ranked in line with British Columbia and just ahead of the Yukon Territories in terms of investment attractiveness. And within Morocco, Aya has multiple assets, including its operating mine, Zgounder, a permitted development project in Boumadine, and early-stage exploration projects that include Azegour (copper, molybdenum, tungsten), Amizmiz [gold], Tirzzit (copper), Imiter Bis (polymetallic). The flagship asset is Zgounder, which is permitted until October 2027 with a ~16 square kilometer exploitation licence, which lies ~260 kilometers east of Agadir and ~220 kilometers west of Ouarzazate. However, the Greater Zgounder area offers considerable exploration upside, as do Aya's other properties, with the company holding well over 200 square kilometers of land in Morocco, including a newly-acquired property (two mining permits with five exploration permits and ~67 square kilometers) with a past-producing copper mine south of Zgounder (shown below).

Anti-Atlas Fault, Aya Operating Mine & Projects - Post-Variscan Evolution of the Anti-Atlas Belt, Int J Earth Scii (Geol Rundsch - 2017), Aya Presentation Zgounder Mine, Zgounder Greater & Tirzzit Exploitation/Exploration Permits - Company Website

{kind=link}

{kind=link}

Reserves/Resources & Zgounder vs. Peers

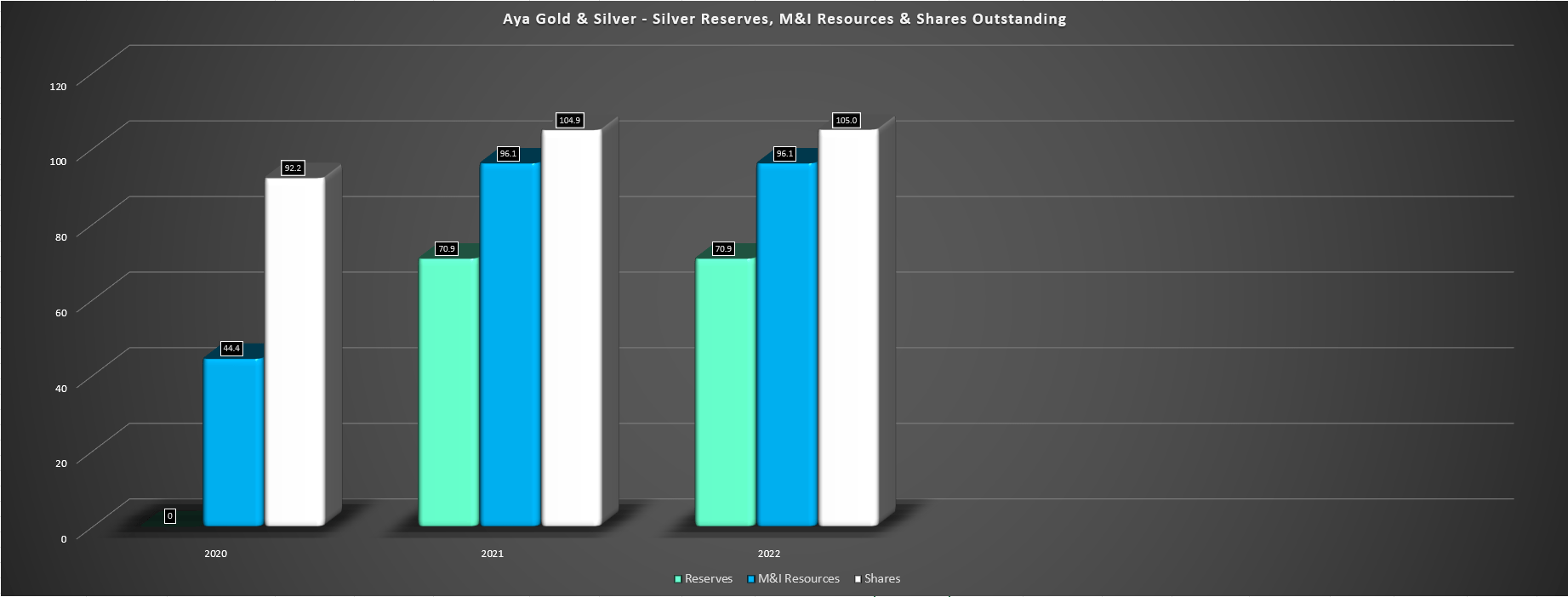

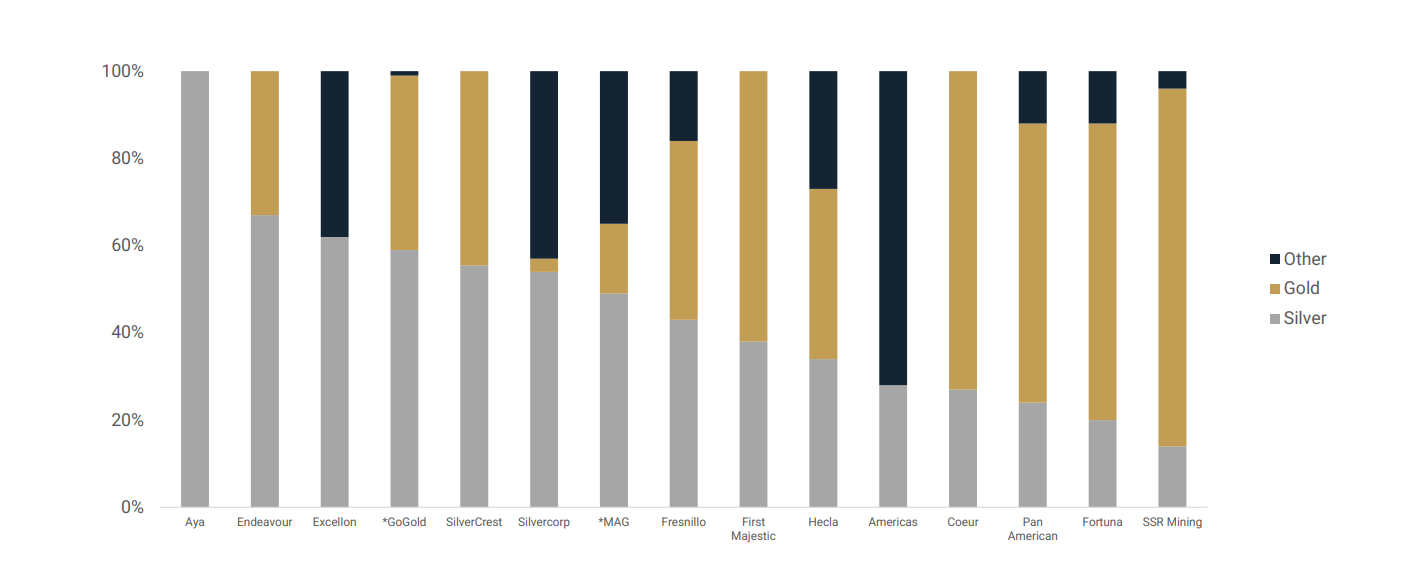

Moving over to reserves and resources, the Zgounder Mine is home to ~2.2 million tonnes of open-pit reserves and ~6.1 million tonnes of underground reserves at 253 and 267 grams per tonne of silver, respectively (~71 million ounces of silver reserves). In addition, Zgounder is unique in that it's solely a silver deposit, not a silver-gold or silver-lead-zinc and or silver-gold-lead-zinc deposit like those owned by many other silver producers (Bolanitos, Topia, Greens Creek, Lucky Friday, San Jose, etc), which should allow Aya to command a higher multiple being a pure-play silver miner in a sector of hybrids. As for the company's resources, they have steadily grown from ~44 million ounces to ~96 million ounces, and there looks to be room to grow this figure to 120+ million ounces even after mining depletion.

And importantly, ounces per share have been growing at a steady clip given that we've seen minimal dilution since CEO Benoit La Salle took over in 2020, with Aya's resources per share more than doubling and set to grow further even after adjusting for minor share dilution after the ~$60 million capital raise at C$8.25 earlier this year.

Aya - Resources, Reserves & Shares Outstanding - Company Filings, Author's Chart

{kind=link}

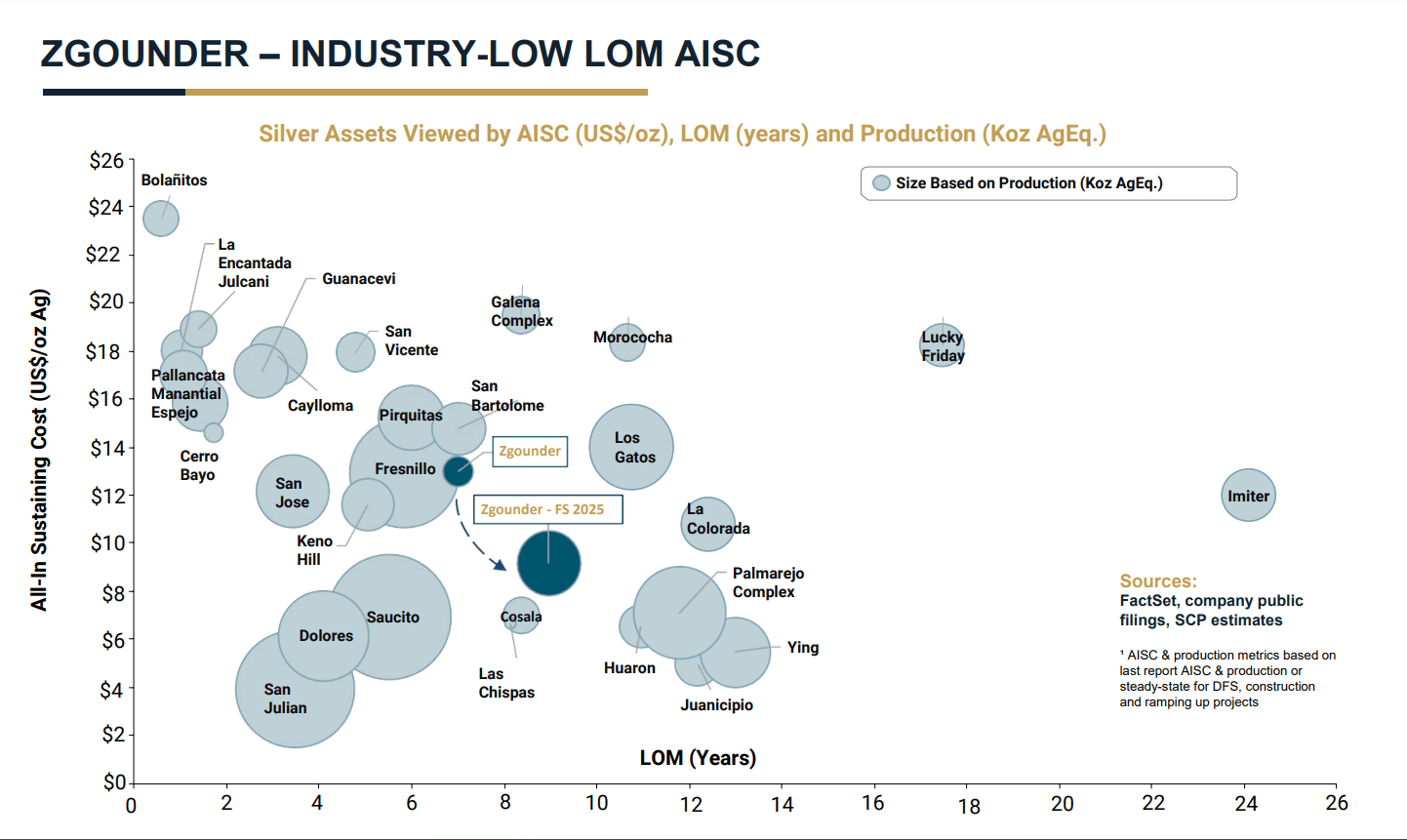

As for how Zgounder stacks up relative to peers, it may not win on mine life, it may not win on grades (~270 grams per tonne) and it may not win on scale, but it stacks up very well from a cost standpoint (~$60/tonne unit costs inflation-adjusted). This is based on the planned Zgounder Expansion, with all-in sustaining costs [AISC] set to dip below $10.00/oz (inflation-adjusted vs. ~$8.50/oz estimates in Q1 2022 study) with the addition of a new 2,000 tonne per day plant that will increase total throughput to just shy of 1.0 million tonnes per annum. And with Aya continuing to have considerable upside from a regional standpoint (possible satellite opportunities) and along strike, there could be room to increase throughput further long-term if the company can continue to build on its resource/reserve base.

Zgounder Mine & Zgounder Expansion - Mine Life, Production & AISC vs Other Assets - Aya Presentation, FactSet, SCP Estimates Aya Gold - Pure-Play Silver vs. Peers - Company Website

{kind=link}

{kind=link}

In fact, from an exploration standpoint, Aya has consistently ranked highly among all silver companies from a grade and thickness standpoint, with a highlight intercept of 21.6 meters of ~3,900 grams per tonne silver released in 2023, the equivalent of ~1,000 gram-meters on a gold-equivalent basis. These results place Zgounder in company with other exceptional assets that include Los Ricos North ( GLGDF ), La Colorada ( PAAS ), Diablillos ( ABBRF ), and Las Chispas ( SILV ) but the difference is that Zgounder is in the best ranked jurisdiction among these assets, is a pure-play silver mine (not a development asset in the case of GoGold and AbraSilver) and the results are over very respectable widths, unlike Las Chispas which is a narrower vein mine and had to reset its expectations recently in its updated Technical Report (some veins more narrow than anticipated, shift from resue to long-hole with difficulty meeting expecting productivity levels and maintaining safety with prior mining method).

So, what's the growth profile look like?

Growth Profile & Financial Results

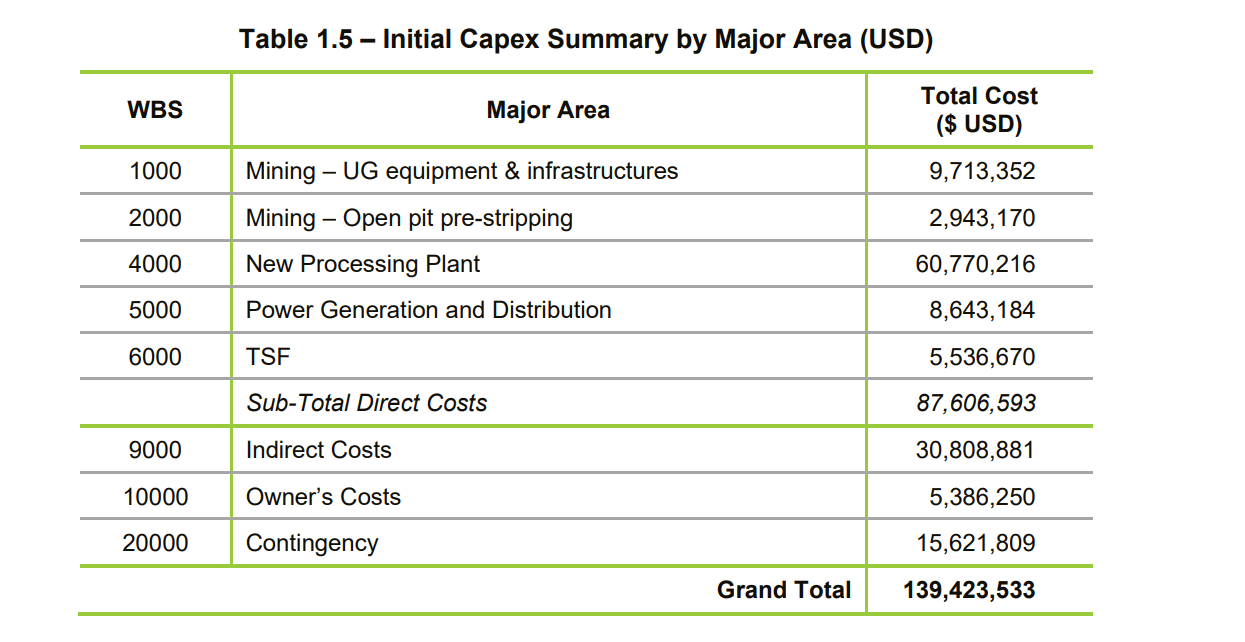

Beginning with the company's growth, Aya is unique in that it has the potential to grow production by ~300% over the next year. This will be achieving by adding a new larger plant at its flagship Zgounder Mine, helping to quadruple its silver production, with annual production set to grow to ~7.0 million ounces per annum (~7.7 million ounces in the first four years). Most importantly, though, this isn't a growth story funded by consistent share dilution like Guanajuato Silver ( GSVRF ), which has succeeded in growing output, but has failed on growing its per share metrics, with continued share dilution at depressed prices and little improve in its margins with its growth, with razor-thin AISC margins. Finally, the other piece of this growth story that makes Aya unique is that this significant growth can be achieved with relatively low capex, with Aya's Zgounder Expansion expected to cost just ~$140 million or ~$154 million if we apply 10% inflation to be more conservative.

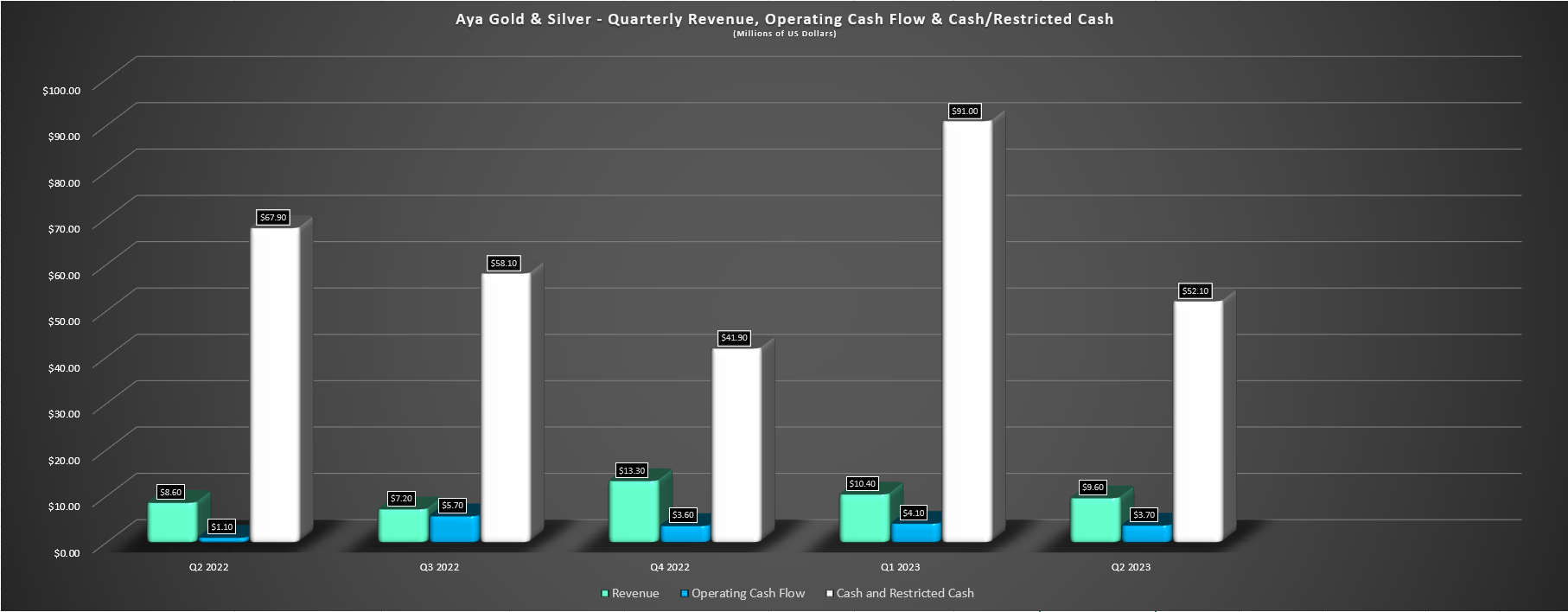

Hence, this growth and aggressive drilling at other properties can be funded without any share dilution, with Aya having access to $92 million in debt from the European Bank for Reconstruction & Development [EBRD] and an additional $8 million tranche from the Climate Investment Funds through its Clean Technology Fund). Coupled with ~$50 million in cash and positive cash flow generation from Zgounder even at the current lower production rate (~$3.7 million in Q2 2023), this will cover the expansion and we should see an increase in free cash flow to $60+ million in 2025 with a full year of commercial production (expansion set to be completed in H1 2024), with the processing plant ~40% complete, overall project completion at ~45%, and the construction of the plant and surface infrastructure tracking in line with budget.

So, in an inflationary environment, low-capex growth and fully-funded growth is a key differentiator vs. other growth stories sector-wide. Plus as we've seen with other high-capex projects in prolific jurisdictions where labor is tight, lots can go wrong and hurt shareholders, with the Magino and Cote builds being clear examples of major disappointments (share dilution, asset divestments and or lower ownership to complete the project successfully).

Zgounder Initial Capex Summary - Company Report Aya - Quarterly Revenue, Cash Flow & Cash/Restricted Cash - Company Filings, Author's Chart

{kind=link}

{kind=link}

As for Aya's financial results, a quick look through the financials and production profile (FY2022: ~1.88 million ounces of silver at $12.63/oz) might make it difficult to wrap one's head around the valuation, with Aya currently trading at over 18x FY2022 revenue (~$38.2 million) at a market cap of ~$710 million, a valuation reserved for a software company, not a single-asset precious metals producer. However, revenue should increase nearly 400% looking out to 2025 to ~$190 million at an ~8.0 million ounce per annum production profile, suggesting that the stock is not nearly as expensive as it appears.

And while a valuation of ~11x FY2025 free cash flow estimates might appear expensive, the major asset in the wings that doesn't appear to be getting nearly enough credit is Boumadine, a polymetallic asset that lies in eastern Morocco that could be twice the size of Zgounder, is already permitted, and should also carry relatively modest upfront capex relative to other expensive builds like Windfall (~$620 million), Eskay Creek (~$500 million), Back River (~$500 million), Fetekro (~$450 million), Skouries (~$900 million), Great Bear (~$1.2 billion).

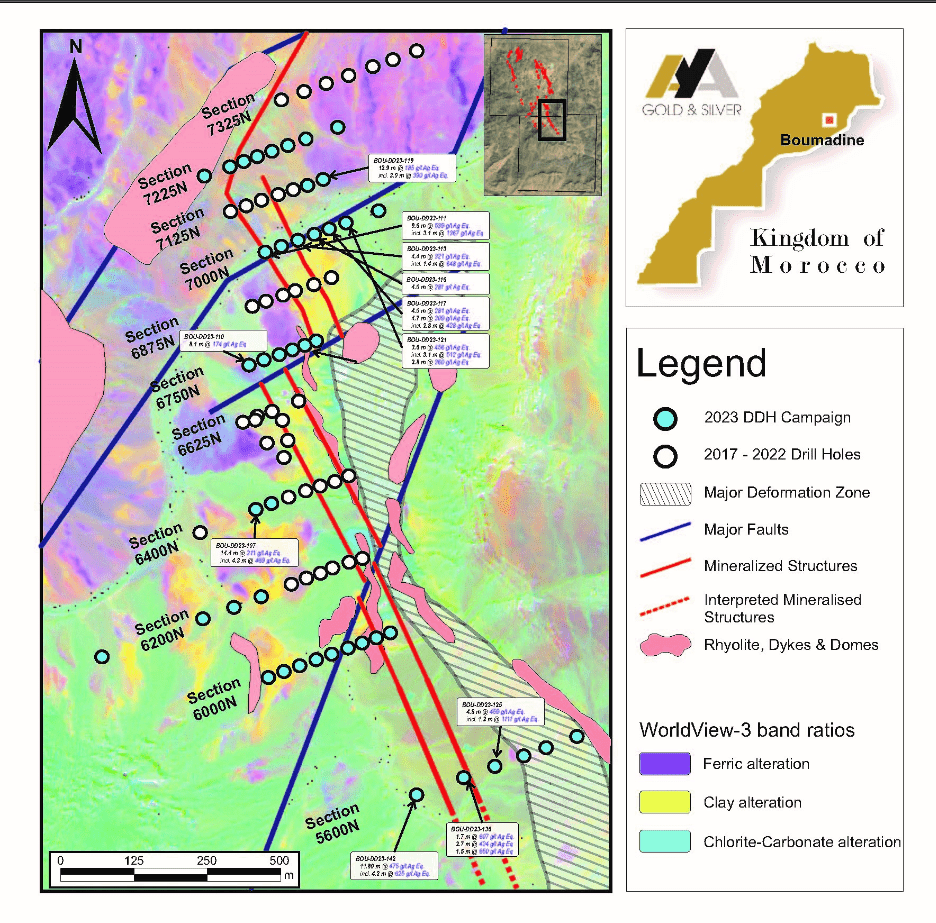

Boumadine Drilling - Company Website

{kind=link}

For those unfamiliar, Boumadine is currently permitted with two exploitation permits covering a 32 square kilometer area (historic resource of ~1.6 million gold-equivalent ounces), and Aya has enjoyed considerable exploration success here since it began drilling this asset last year (~19,000 meters drilled in 2022). Since then, the company has increased the strike at Boumadine to nearly 4 kilometers, increased its drill program by 40,000 meters with a goal of expanding the strike to the south and completing infill drilling to deliver a resource by Q1 2024. Most recently, the company reported highlight intercepts of 11.8 meters at 475 grams per tonne silver-equivalent and 9.6 meters of 539 grams per tonne silver-equivalent, with high-grade intercepts at the north and south end of the deposit.

The plan for this asset appears to be an open-pit and underground operation (similar to Zgounder), but with the growth we've seen in this asset, the company could potentially look at a 4,000 - 5,000 tonne per day operation, and if expedited, this could be in production by 2028 given that permits are already in place.

So, why is Boumadine a potential game-changer?

While Zgounder is an impressive asset with future production of ~7.0 million ounces at industry-leading AISC (~$9.00 - $10.00/oz), Boumadine could dwarf it in size. And while the following numbers are very high-level conceptual estimates, a ~4,600 tonne per day operation at ~500 grams per tonne silver-equivalent and 74% payability would translate to ~20 million silver-equivalent ounces [SEOs] produced per annum, catapulting Aya to mid-tier status with production just shy of 30 million SEOs per annum (Zgounder + Boumadine). In addition, Boumadine's NPV even at an 8% discount rate would nearly cover Aya's current market cap ($600+ million vs. ~$700 million), giving investors Zgounder (its current operating mine), exploration upside, and Tijirit for free. Or looked at another way , investors are paying ~$700 million (Aya's current market cap) for Zgounder (8.0 million ounces at ~$10.00/oz AISC post-expansion) and getting Tijirit, Boumadine and its other exploration assets for free.

So, while it's important to caution that these are very conceptual numbers for Boumadine, this is another relatively modest capex growth opportunity (~$320 million to $360 million) that could contribute over $140 million in free cash flow per annum even at conservative metals price assumptions. Plus, it's hard to put a value on exploration upside when it comes to virgin territory in Morocco that has not received nearly enough attention. And with companies like Endeavour Mining ( EDVMF ) still making massive discoveries like Tanda-Iguela in a jurisdiction that has seen exponentially more drilling than Morocco, Aya certainly offers a huge exploration kicker that isn't present in most other juniors. And as its CEO Benoit La Salle puts it:

"The belt, again, I told you, let's go and discover the Carlin Trend, or the belts in Australia, or the Cadillac-Break in Canada, or the Ashanti Belt in Ghana, let's go it's brand new. This belt (in Morocco) is brand new. It's called the Atlas Fault. It's 1,600 kilometer long. 65% of it has never been walked, forget drilled, forget geophysics, forget satellite imagery, forget spectral imaging, it's never seen that. Our success is not that we are smarter, it's that we came in with money".

- Benoit La Salle, Aya Gold & Silver CEO

Boumadine Camp - Company Website

{kind=link}

Given that we are working with a historic resource and at least two years away from a Feasibility Study, I have chosen to be more conservative on Boumadine and other early-stage assets, valuing all of these assets at $480 million combined ($300 million Boumadine and $180 million combined for Zgounder Regional, Tirzzit, Azegour, Amizmiz, and Imiter Bis.

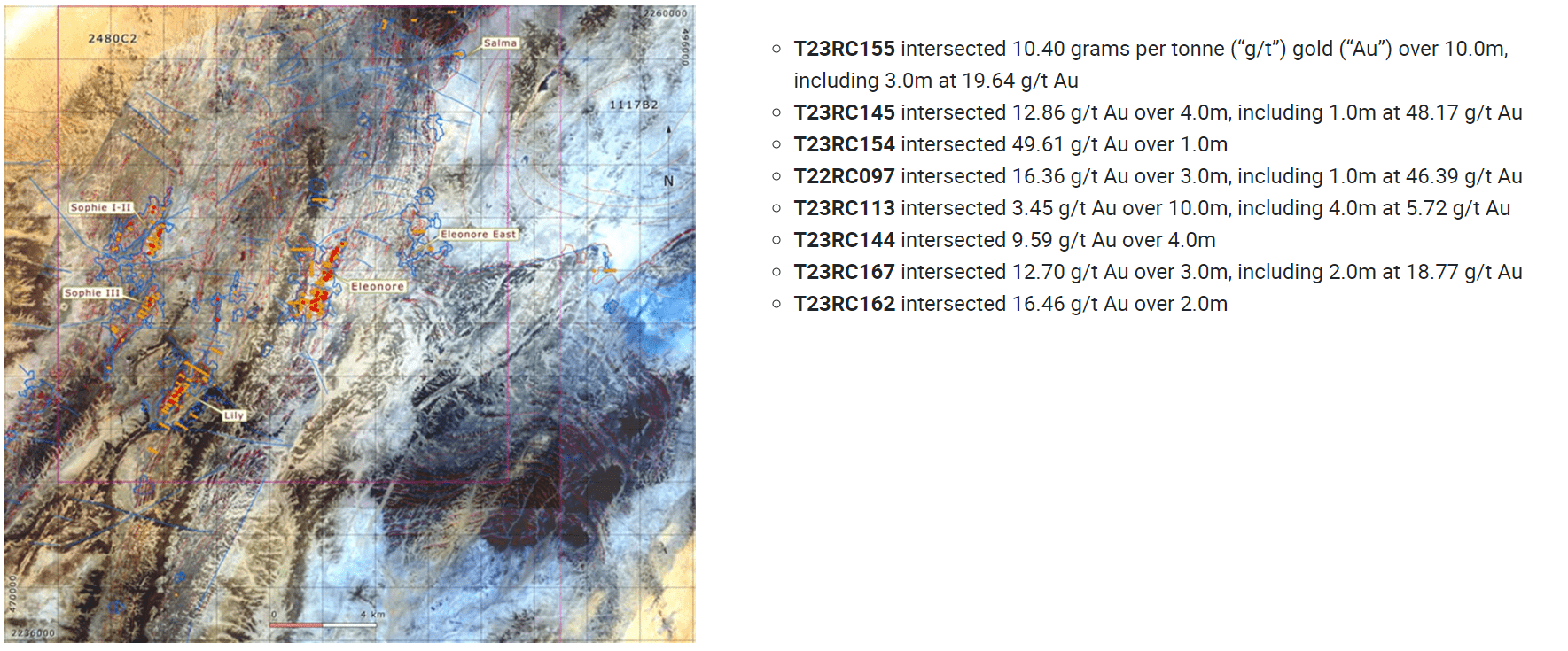

Finally, I'd be remiss not to note that while Aya has considerable upside to its production profile and annual cash flow generation from higher throughput with room for expansions at Zgounder and production at Boumadine, the company also has a smaller opportunity in Tijirit. This asset is 75% owned by Aya and is relatively small (acquired for a song for ~$11 million in 2021) with just ~820,000 ounces of gold (35% M&I). However, there is a high-grade sub-set of this resource at Eleonore, with ~215,000 ounces at 4.2 grams per tonne of gold, with an additional ~280,000 ounces at 3.2 grams per tonne of gold in the inferred category. So, what Tijirit lacks in scale, it makes up for in grade, and these grades would make it one of the highest-grade open-pits globally, with Aya's plan being to start with a small 1,000 tonne per day operation and ramp to 2,000 tonnes per day if Tijirit can support a larger mine life. It's also worth noting that this asset is permitted, like Boumadine, and I would expect that it could be built for less than $60 million, suggesting a quick payback.

Tijirit Highlight Infill Drilling Results & Deposits - Company Website

{kind=link}

Running the numbers on a ~1,000 tonne per day operation with ~95% recoveries and a more conservative 3.3 grams per tonne of gold, this might not seem all that exciting, with Tijirit being a ~37,000 ounce per annum producer under these assumptions. However, recent highlight results have continued to confirm these strong grades, other deposits (albeit lower grade) are present at Tijirit, and the company certainly has the right location. This is because it has Tasiast to the northwest which is home to ~8.6 million ounces of above average grade open-pit resources and reserves, with Tasiast being one of the most impressive gold assets in Africa from a scale standpoint, among other giants like Kibali, Iduapriem, Ahafo, Loulo-Gounkoto, and Fekola. So, while I'm assigning just $45 million here ($50/oz on ~900,000 ounces), I am optimistic this asset is worth much more long-term, and with a low-capex build and feasibility work underway with permits in hand, this could be in production within five years potentially, providing geographical diversification outside of just Morocco.

Valuation

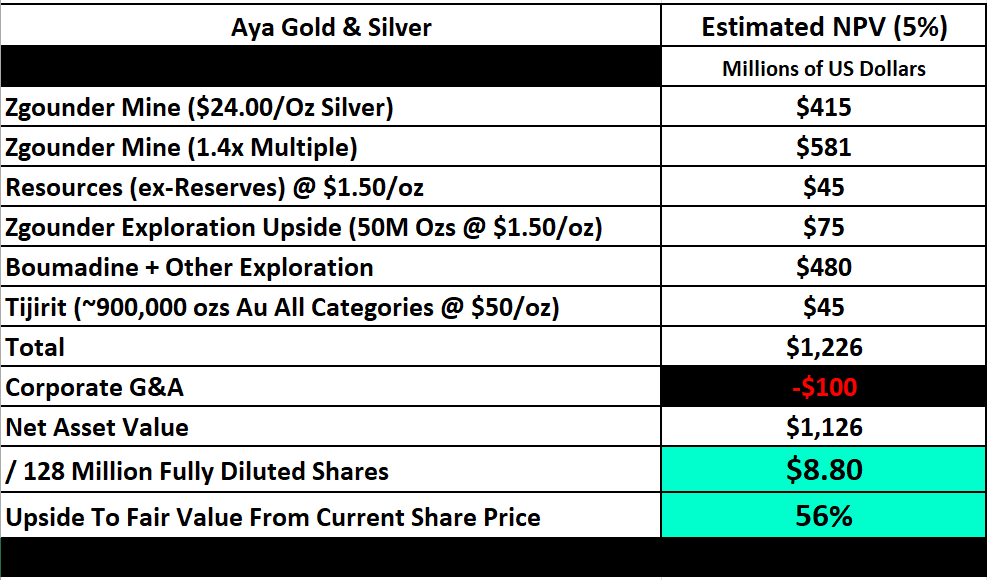

Based on ~128 million fully diluted shares and a share price of US$5.45, Aya trades at a market cap of ~$700 million. This places it ahead of companies like Endeavour Silver ( EXK ) in the silver space and just behind companies like MAG Silver ( MAG ), Coeur Mining ( CDE ), and Fortuna ( FSM ). Given that Aya is a much smaller producer than these companies, it's understandable that the stock might look overvalued at first glance. However, as noted, the company's financial results reflect an asset operating at one-fourth of its potential with no upside from two other permitted projects and potential satellite discoveries at Zgounder that could prompt a further increase in throughput longer-term. In addition, the estimated fair value of Zgounder assumes no upside in the silver price above $24.00/oz from 2024-2034, which I would argue to be a very conservative assumption.

Aya Gold & Silver Estimated Fair Value, Author's Estimates, Company Filings

{kind=link}

Based on the above table (1.4x multiple for Zgounder in line with other silver-producing assets), $120 million for exploration upside near-mine, and $480 million for all of its other exploration upside across Morocco plus Boumadine and subtracting $100 million in corporate G&A, I see a fair value for Aya of ~$1.13 billion or US$8.80 per share. This points to over a 56% upside from current levels, and makes Aya stand out as being very attractively valued among silver producers. Plus, it has the rare distinction of being a fully-funded growth story that's set to see steady growth in reserves, cash flow, and NAV per share, with the potential for a re-rating once investors start to see the real potential at Boumadine, which could be an 18+ million ounce per annum producer on a silver-equivalent basis.

And given that many silver producers in the junior/mid-tier space are serial diluters that have struggled to grow per share metrics with many having weaker balance sheets (carrying high levels of debt), I think Aya should trade at a premium and be a go-to name in the silver space, which is why I have recently started a small position.

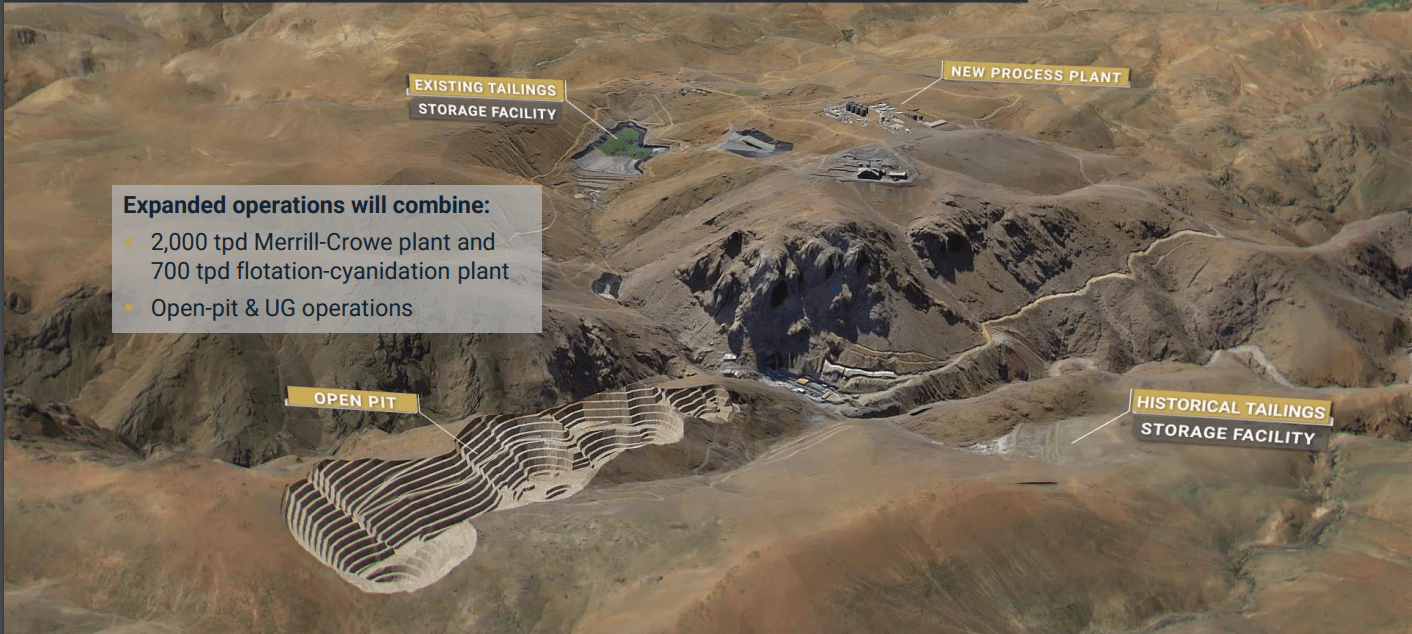

Zgounder Mine Expansion - Planned Layout - Company Website

{kind=link}

Summary

Aya Gold & Silver is not the cheapest name in the sector, but silver producers rarely trade at cheap valuations, and that applies to those executing successfully and those that aren't. In fact, First Majestic regularly traded at over 3.0x P/NAV from 2021 to Q1 2023 before coming back to reality and it was one name that has continued to see declines in its per share metrics . And among silver producers, Aya Gold & Silver does stand out with considerable upside and a valuation that's back-stopped by one of the highest-margin mines sector-wide in one of the more attractive jurisdictions.

More importantly, Aya Gold & Silver is led by a Benoit La Salle, which has done it before in Africa at Semafo, doing a solid job of acquiring assets counter-cyclically and maximizing their value and the company would have sold out at a much higher price if not for the tragic security incident at its Boungou Mine in 2019 that took production offline.

Given this solid track record and the consistent delivery on its goals to date, I see Aya as one of the more interesting names in the silver space, and the ~40% correction has finally left the stock back at a much more reasonable valuation. And while realizing value from Boumadine won't be instant, I would expect more value to be ascribed to Tijirit and Boumadine as these assets become talked about more often and progress through the development cycle, with a major benefit being that both are permitted and low-capex opportunities, reducing the risk around ultimately realizing production from these assets. Plus, both assets carry above average grades, reducing payback and making them both quite economic even at conservative metals price assumptions.

So, with a path to per share growth, high insider ownership (~15%) that makes management aligned with shareholders, the ability to grow into a multi-asset producer long-term, and Aya being one of the best exploration stories sector-wide, I see Aya Gold & Silver Inc. stock as a Buy.

For further details see:

Aya Gold & Silver: Industry-Leading Growth At An Attractive Price