CA - Aya Gold & Silver: Milestones To Be Achieved In 2023 But Beware Of Rate Hikes

2023-03-07 15:26:41 ET

Summary

- AYA expects a significant ramp-up in YoY production from 2024 onward for the Zgounder mine.

- During 2023, AYA expects to achieve significant operational milestones for its key projects, particularly exploration activities.

- I believe the company is largely free from any permitting, or project financing risk.

- However, the Fed's current hawkish policy will maintain pressure on silver prices.

Thesis

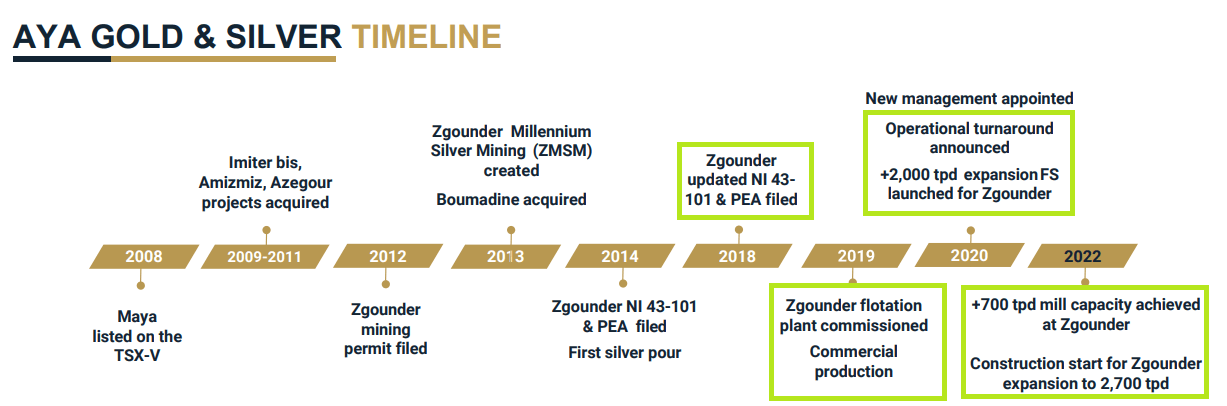

Aya Gold & Silver ( AYASF ) delivered solid operational performance during Q4 and FY 2022, in terms of production and exploration results. AYA is a Canadian-based precious metals mining corporation engaged in the exploration, development, production, and acquisition of precious metals mining projects. The company's focus is on producing silver, and its flagship asset is the Zgounder silver mine in Morocco. The company has a couple of other promising exploration and evaluation projects in its portfolio including Boumadine, Tijirit, Amizmiz, Azegour, Imiter Bis, etc. Apart from the Zgounder mine, all other projects are exploration/evaluation stage projects.

In this article, we look at the following areas to help us consider an investment case in the company:

- Impact of the FED funds rate on the prevailing silver prices, which in turn affects the share price of silver miners like AYASF.

- Mining attraction of the Zgounder project.

- Progress of exploration on other key projects.

Let's get into the details.

FED funds rate and its impact on the silver price

Last week, markets reeled in anticipation of a 50 basis point hike in the FED funds rate. The 2-year yield reached a decade high of 4.889%, with 10-year yields up by 7 basis points to 4.066%. Later, the markets saw some recovery amid renewed hopes of a 25 basis point hike. Meanwhile, weekly jobless claims in the US declined by 2,000 to 190,000, whereas market expectation was ~195,000 claims. This points toward a robust US jobs market which could trigger another rate hike by the FED in its upcoming meeting.

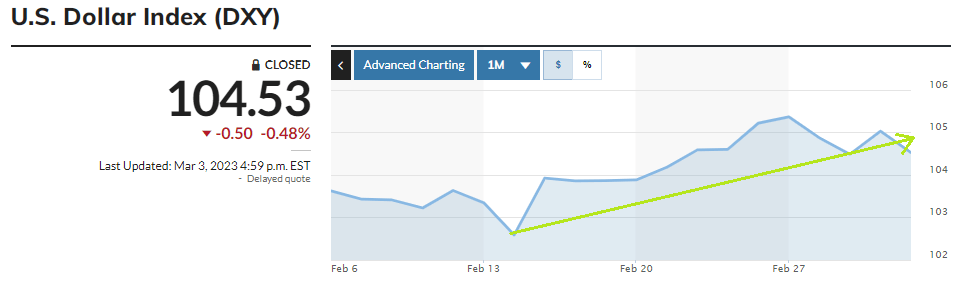

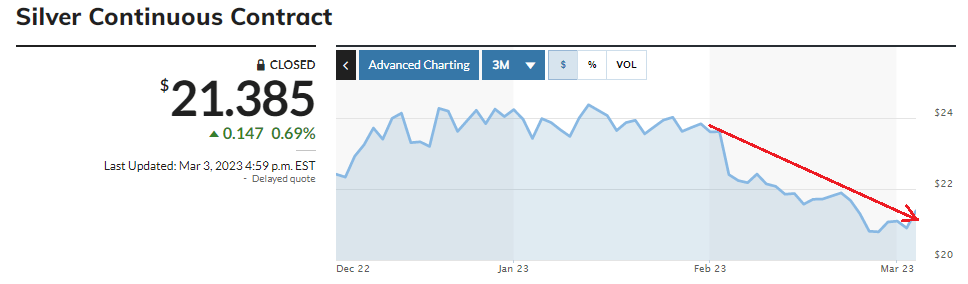

The point is, an increase in the FED funds rate strengthens the USD as it increases the demand for the greenback. Consequently, more money flows from traditional stock markets and PM (read: precious metals) markets into money market products. Generally, there is an inverse relationship between the USD index and the prices of PMs such as silver and gold. This can be seen in the following two charts which show that an increase in the USD index ( DXY ) since February 2023 (refer to Figure-1) is matched by a decline in silver prices (refer to Figure-2) during the same period.

{kind=link}

{kind=link}

My views: Given the expectation that the FED will consider another rate hike in its upcoming meeting, I believe silver prices are likely to witness further downside and could eventually find support within the range of $20/oz to $20.5/oz. For silver mining companies like AYASF, this situation implies the risk of a possible decline in the share price at least in the near term.

Mining Attraction of the Zgounder project

1) Morocco is a mining-friendly location: AYA claims that Morocco is the first pure silver producer in Africa, and that sounds like an advantage to me. A sizeable proportion of large-scale silver projects are located in Latin American countries like Mexico, Peru, Chile, etc. However, the mining environment of these countries generally impacts the mining attraction of their respective projects in terms of permitting issues, tax legislation, etc. In contrast, AYA's Zgounder mine appears to be largely free from such risks; it already has a mining permit for 10 years (renewable thereafter) and the asset is in production.

From another perspective, Morocco can be termed an attractive mining location. The Fraser Institute issues an annual report titled "Annual Survey of Mining Companies" to gauge the mining attraction of different geographical locations in terms of regulatory policy, and the mineral potential of those locations. The 2021 report highlighted that Morocco ranked 2nd on the PPI (read: Policy Perception Index) with a score of 98.06 points. Note that this PPI score not only tops the list of African countries but is also significantly greater than the scores of well-known mining locations like Saskatchewan (91.25 points), Quebec (92.69 points), Yukon (79.77 points), Nevada (91.77 points), Alaska (85.25 points), Western Australia (92.83 points), etc.

My views: I believe the Moroccan regulatory environment favors mining companies and this fact lowers the risk of potential government intervention (permitting, taxation, etc.) in the smooth running of AYA's Zgounder operations.

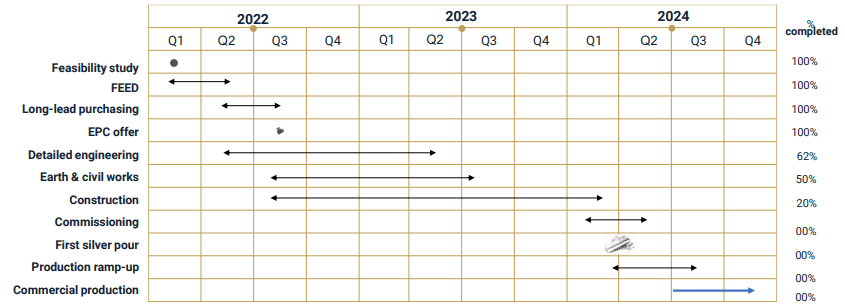

2) Expansion of production is on the cards: The processing plant at Zgounder has an existing capacity of ~700 tpd (read: tons per day) and AYA is working to expand this capacity to ~2,700 tpd (also called the Zgounder expansion).

{kind=link}

Similarly, a ~4x increase in annual silver production is expected in FY 2024 (~7.9 Moz) compared with annual production guidance for 2023 (within the range of ~1.7-1.9 Moz). This will be made possible through the Zgounder mill expansion mentioned earlier.

My views: The ongoing 2 years (2023-2024) are important from a project development perspective since major development milestones are expected to be achieved by the end of FY 2024.

{kind=link}

3) Mineral Reserves surpass Mineral Resources: AYA released the updated FS (read: Feasibility Study) on the Zgounder project in January 2022, whereas the FS on the 'Zgounder expansion' project was released in June 2022. Both studies revealed robust mining prospects for the project.

For instance, the project is expected to contain an underlying total mineral resource of ~96.1 Moz (read: a million ounces) silver of which ~70.9 Moz are estimated to be P&P (read: Proven & Probable) reserves while the remaining 25.2 Moz are estimated to be M&I (read: Measured and Indicated) resources . I see that the P&P reserves far exceed the M&I resources, and that's a good thing because 'reserves' have a greater chance of actually being converted into mining output than 'resources'.

Note that the Zgounder mine comprises both open pit and underground operations; a quality observed in very few mines. Typically, open pit operations have a lower initial development CAPEX than underground mining operations. It's interesting to note that ~29% of the 70.1 Moz reserves are located in the open pit ore.

4) Cut-off grades: Another interesting aspect is the cut-off grades and estimated LoM (read: Life of Mine) prices used in the feasibility studies. The mineral reserves were estimated using LoM silver prices of ~$20/oz with average cut-off grades of ~47 g/t silver in the open pit, ~85 g/t silver in the underground, and ~44 g/t silver in the historical tailings portion.

My views: The underlying mineral reserves at Zgounder can potentially increase because the ~$20/oz price is a conservative estimate of long-term silver prices (spot silver trades at ~$21.3/oz; refer to Figure-2). Silver prices higher than those at which cut-off grades are estimated (in this case $20/oz) enable a company to mine even lower-grade ore in a bullish silver price environment, and hence the potential to have mineral reserves greater than initially estimated in the FS.

5) Strong YoY operational performance: AYA's 2022 silver production clocked in at 1.88 Moz, recording an impressive YoY increase of 17.5%. The company processed 254,976 tons of ore during 2022, up 13.6% YoY. Meanwhile, the FY 2022 combined silver recovery ratio of 86.6% also increased by 4.6% YoY. These numbers indicate the YoY improvement in AYA's operational performance at its Zgounder mine.

My views: We can expect these numbers to further witness a significant increase in FY 2024 for two reasons; (1) the expected increase in processing capacity when the additional ~2,000 tpd plant becomes operational (thus increasing total processing capacity to ~2,700 tpd), and (2) an improvement in recovery ratio stemming from identification of high-grade zones in the ongoing exploration activities. Another reason to believe that production numbers are likely to improve, going forward, is the fact that Q4 2022 production numbers represent ~1/3rd of the 2022 total value on multiple production-related performance metrics, as noted in the table below.

Q4 2022 versus Full Year 2022 - Key production-related metrics (Figure-5)

6) Exploration Activities Reveal Potential High-Grade Zones: AYA's P&P reserves at the Zgounder mine are estimated to be ~70.9 Moz at an average grade of ~257 g/t. Interestingly, AYA's ongoing drill exploration program helps identify and add high-grade zones to expand the mineral resource. A few key high-grade silver intersections reported during the 2020-2022 drill exploration program include the following:

- 3,043 g/t Ag over 14.4 meters;

- 3,956 g/t Ag over 21.6 meters;

- 4,101 g/t Ag over 14.4 meters;

- 6,437 g/t Ag over 6.5 meters; and

- 9,346 g/t Ag over 4.0 meters.

My views: High-grade zones enable a mining company to maintain suitable operating margins even when the prevailing silver prices are low, and vice versa. For this reason, I believe AYA's impressive high-grade silver discoveries at the Zgounder mine will help the company maintain its operating margins (in the future) in both bullish and bearish silver price environments. It's worth noting here that during 2023, AYA has budgeted a 26,000-meter DDH (read: Diamond Drill Holes) exploration program at Zgounder to expand the mineral resource at depth through near-mine drill targets. This is in addition to the ~6,700 meters program planned for 2023 at the Zgounder Regional exploration project.

High-Grade Zones identified at the Zgounder mine (Figure-6)

7) Robust liquidity to support Zgounder's growth CAPEX: Estimated CAPEX to expand Zgounder's processing capacity from 700 tpd to 2,700 tpd is ~$139.4 MM. As of September 2022, AYA had cash worth ~$124 MM. If needed, AYA could utilize the ~$100 MM undrawn credit facility to support Zgounder's growth CAPEX. Hence, investors need not worry about possible dilution in shareholder value emanating from a potential equity issuance in the future in my opinion.

Impressive progress on other pipeline projects

Apart from Zgounder, AYA has a couple of other promising mining projects in its portfolio including Imiter bis, Boumadine, Amizmiz, Azegour, and Tijirit. The company is fast ramping up these projects on the drilling/exploration front and I see major milestones to be achieved on some of these projects over the 2-year period between 2023-2024.

1) Boumadine: Acquired in 2013, the Boumadine project is currently undergoing extensive exploration studies and is classified as a primarily gold-silver project. Like Zgounder, the proportion of AYA's interest in this project is 85%, with the remaining 15% owned by a government agency. In 2022, AYA conducted a drill exploration program on 18,335 meters. Some of the interesting high-grade discoveries from the 2022 drill program are mentioned below.

Boumadine 2022 exploration - Notable Discoveries (Figure-7)

I think 2023 will be an important year for the Boumadine project for the following reasons:

- AYA plans to double the exploration activities in 2023; from 18,335 meters (in 2022) to ~36,000 meters. Out of those 36,000 meters, ~21,000 meters will be focused on the main trend, while ~15,000 meters will aim to extend mineralization along strike and at depth.

- AYA's 2023 ~36,000 meters exploration program for Boumadine is even greater than the exploration program for the company's flagship asset, Zgounder (2023 planned exploration =~26,000 meters). That's why I believe that after Zgounder, Boumadine is the next best thing for AYA.

- AYA's exploration results for the 2023 program will help the company to issue a mineral resource estimate in 2024. The mineral resource will incorporate the exploration results from the 2018-2023 period, and will better define the mining attraction of the Boumadine project.

2) Tijirit - Mauritania: Tijirit is a relatively smaller project in AYA's portfolio (AYA's project ownership=75%). Here's what I like about this project:

- Although Tijirit is primarily a gold mining project, the 2018 PEA assumes a discount rate of 8% to calculate the project's after-tax NPV of $69 MM. I believe that PM projects should be discounted using a rate between 6-8% compared with 'base metals' projects which typically attract a discount rate between 8-10% because PMs (such as gold/silver) have low barriers to selling compared with base metals. In contrast, mining companies often use a low discount rate that's not commensurate with the overall risk profile of their respective projects, thereby portraying a high after-tax NPV. For instance, PolyMet Mining uses a discount rate of 7% for its NorthMet project which primarily comprises base metals, and is also not fully permitted. Having said that, I believe an 8% discount rate is fair enough for Tijirit, which represents a gold mining project and the rate is also on the higher end of the suggested range for PM miners (that is, 6-8%) .

- The project is expected to produce ~580,000 gold ounces over a period of 7 years at an average LoM AISC (read: All-In-Sustaining-Cost) of $726/oz. Given gold's prevailing prices within the range of ~$1,800-1,850/oz, I believe Tijirit's LoM AISC will provide room for healthy operating margins in the future (~$1,000+/oz).

- The project has a payback period of only 1.8 years.

- AYA's 2022 drill program on the Tijirit project encompasses an area of 25,000 meters, and the project's FS is ~85% complete. AYA expects the exploration program to conclude in Q1 2023, after which the FS will be issued to better define the project's economics.

Investor Takeaway

AYA can be classified as a long-term growth company. However, that growth extends into the mid-to-long term, especially in terms of YoY production growth. I like the company for its Moroccan operational presence (as Morocco is considered a mining-friendly jurisdiction), as well as the attractive mining dynamics of its key projects. Moreover, I don't see any major permitting or financing risk for AYA's mining projects that are currently being focused on by the company (especially Zgounder, and Boumadine).

Notably, 2023 is an important year for the company when we talk about its ongoing aggressive exploration programs which are likely to improve resource definition of the mineral orebodies underlying AYA's key mining projects. Nonetheless, 2023 silver production (from the Zgounder mine) is expected to remain in line with the last year.

That said, I believe AYA to deliver slow but steady share price growth over the medium to long term as its projects progress on the key milestones identified in our analysis. Nonetheless, AYA's near-term share price will be largely impacted by the prevailing metal prices (especially silver, and gold). In my view, the FED's continued rate hikes are a key headwind that could keep silver prices under pressure at least over the near term (say, 3-6 months), therefore, one should look for a suitable entry point in AYA when silver prices move to the 'support' range of ~$20/oz to $20.5/oz (spot silver=$21.14/oz, at the time of writing).

For further details see:

Aya Gold & Silver: Milestones To Be Achieved In 2023, But Beware Of Rate Hikes