CA - B2Gold: A Free Cash Flow Machine Post-2024

2024-01-11 12:59:31 ET

Summary

- B2Gold Corp. was one of the worst share-price performers in 2023, significantly underperforming its peer group with a 12% annual decline.

- This can partially be attributed to relatively low free cash flow generation, which is expected to continue into 2024 with a major construction project underway at Goose in Nunavut.

- In this update, we'll look at why this deal is transformative for B2Gold, the company's 2024/2025 outlook, and whether the stock is worthy of investment after its recent share-price underperformance.

It's been a tough year for the Gold Miners Index ( GDX ), with the disappointing results of a few souring sentiment for the group, and continued share-price underperformance vs. the gold price. Some of the detractors with pitiful results and/or per share metrics (due to continued share dilution) have been Coeur Mining ( CDE ), First Majestic ( AG ), and Iamgold ( IAG ). While Evolution Mining's ( CAHPF ) margins have been solid, we've seen significant additional share dilution with more aggressive growth by M&A, with this being the third major deal in just three years (Battle North, Ernest Henry, Northparkes).

Fortunately, the metals prices are finally at favorable levels where the usual (share dilution) suspects might be able to avoid leaning on their ATM or issuing equity, and the sector leaders have some of the strongest balance sheets in years on balance, and the average million-ounce producer is paying a dividend yield double that of the S&P-500 (SP500). In addition, we've seen far more disciplined growth from most miners (unlike past cycles), with one example being the recent B2Gold Corp. ( BTG ) acquisition of Sabina Gold & Silver . In this update, we'll look at why this deal is transformative for B2Gold, the company's 2024/2025 outlook, and whether the stock is worthy of investment after its recent share-price underperformance.

Goose Project Construction - Company Website

{kind=link}

A Transformative Acquisition

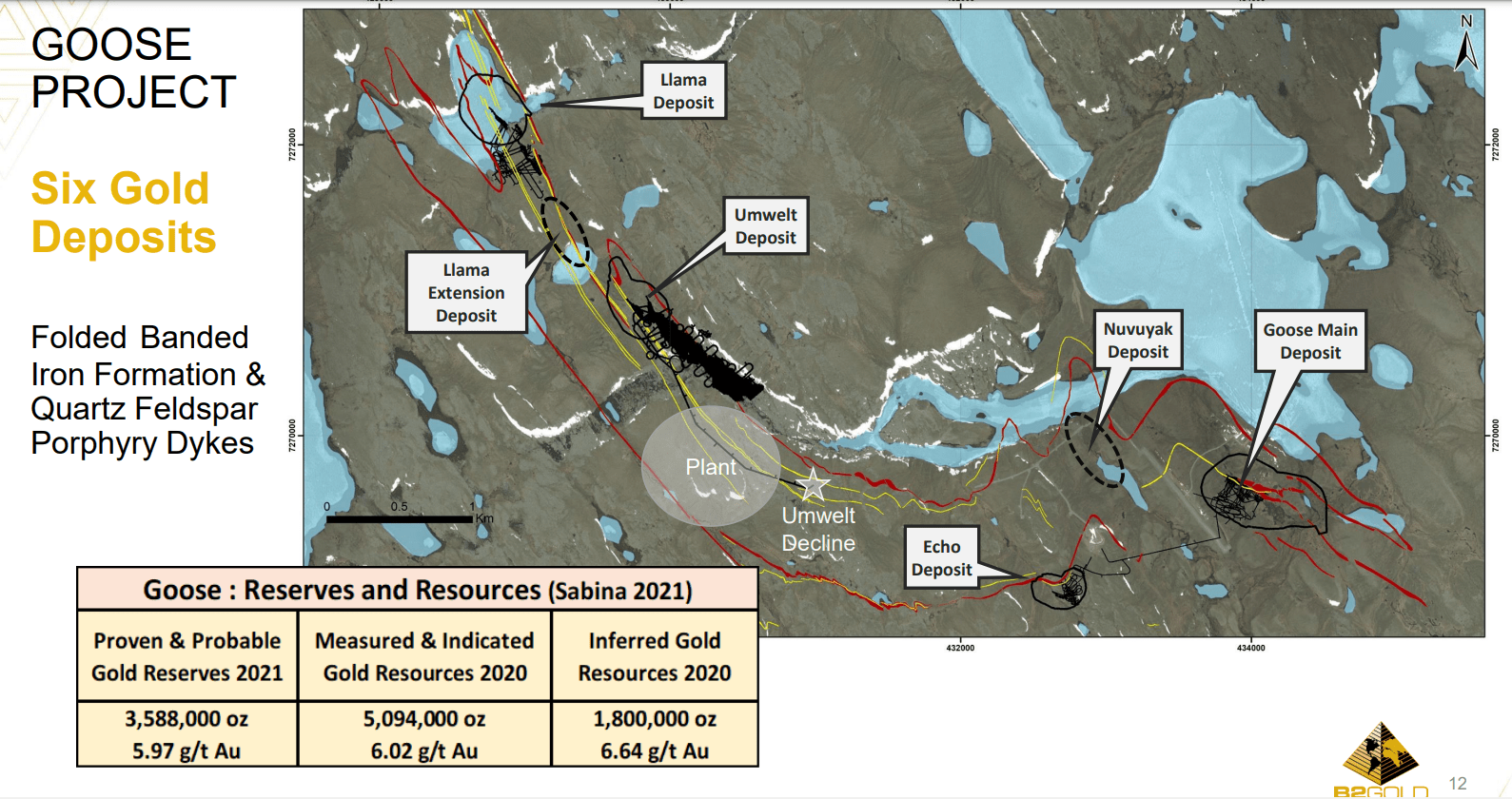

B2Gold closed its acquisition of Sabina Gold & Silver in April 2023 for ~$940 million in one of the most transformative deals in the company's history next to Papillon (Fekola) in 2014. This is because the acquisition has not only given B2Gold a new Tier-1 ranked mining jurisdiction in Nunavut, Canada, but the asset itself is phenomenal, with a high-grade reserve base of ~3.59 million ounces at ~6.0 grams per tonne of gold within a larger resource base of ~9.18 million ounces between Goose (main project area) and George.

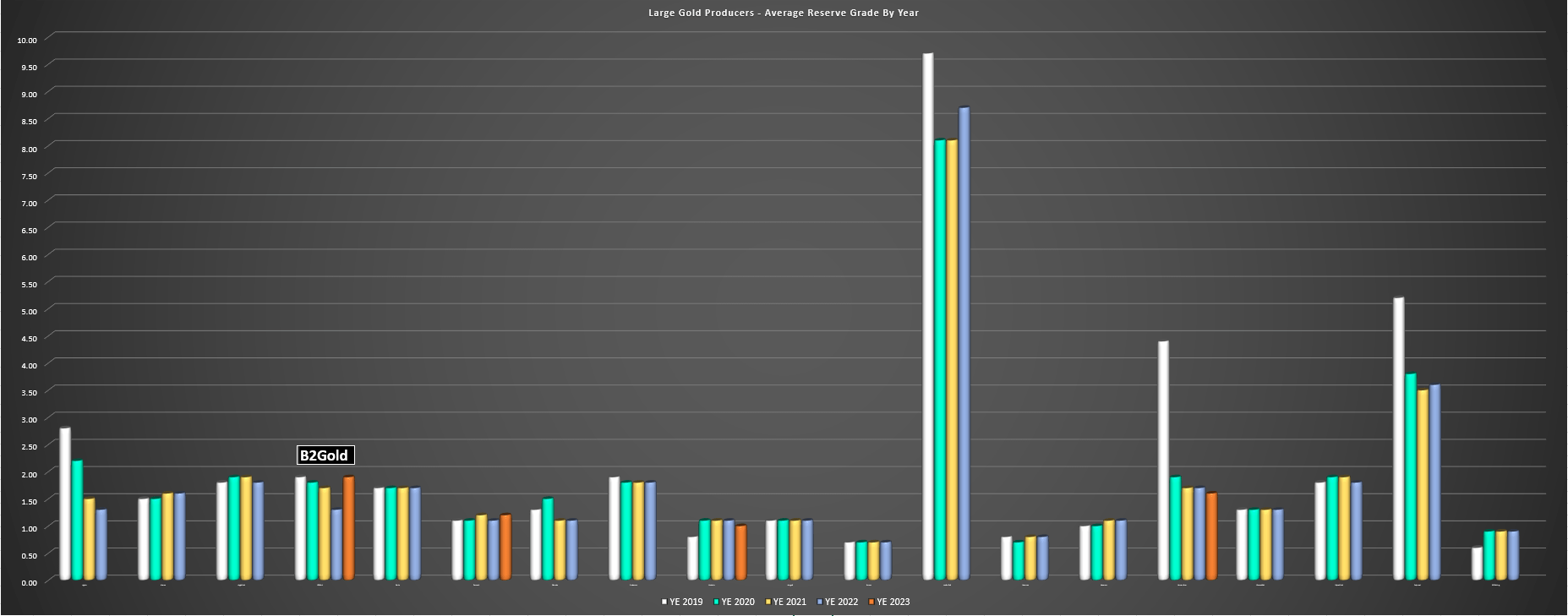

As shown below, this acquisition has increased B2Gold's average reserve to ~1.90 grams per tonne of gold (2022: ~1.30 grams per tonne of gold), and with significant progress made to date at Goose (open-pit mining at Umwelt set to begin in Q1 2024 with underground development at over 150 meters, and open pit mining already underway at Echo), investors can look forward to first gold pour within 15 months at this high-margin asset.

Large Gold Producers - Average Reserve Grade By Year

{kind=link}

For those unfamiliar with Back River, it is one of the highest-margin undeveloped gold projects globally, and is expected to produce ~230,000 ounces over its 15-year mine life. However, first five-year production is expected to be above 300,000 ounces with the 4,000 tonne per day expansion pulled forward at sub $850/oz all-in sustaining costs (even accounting for inflationary pressures). To put these costs in perspective, Goose's annual all-in sustaining costs from 2025/2026 are likely to be over 40% below industry average estimates of ~$1,430/oz, and significantly below the average cost profile of B2Gold's current operations from Fekola, Masbate, and Otjikoto.

Plus, it's important to note that this is an asset that is permitted for 6,000 tonnes per day and there's the possibility that it could operate at above nameplate capacity even without an expansion (~4,300 tonnes per day vs. 4,000 tonnes per day), suggesting peak production that could come in closer to 330,000 ounces.

"So we're actually permitted at Goose for 6,000 tonnes per day versus what our feasibility shows at 3,000 tonnes per day for expansion to 4,000. You'll see that we made the decision that rather than building at 3,000 tonnes a day and expanding before the end of the second year, we made that decision to build it at 4,000 tonnes a day. What's not in our feasibility study is the effects of that extra 1,000 tonnes a day for the first 2 years. One thing I would just add to the one of the opportunities that Bruce touched on obviously the ability actually to start this mine and produce in excess of 300,000 ounces a year for the first several years. And obviously, the goal would be to continue that we'll even expand that going forward."

- B2Gold Sabina Acquisition Call, Bruce Mcleod (Sabina CEO), Clive Johnson (B2Gold CEO).

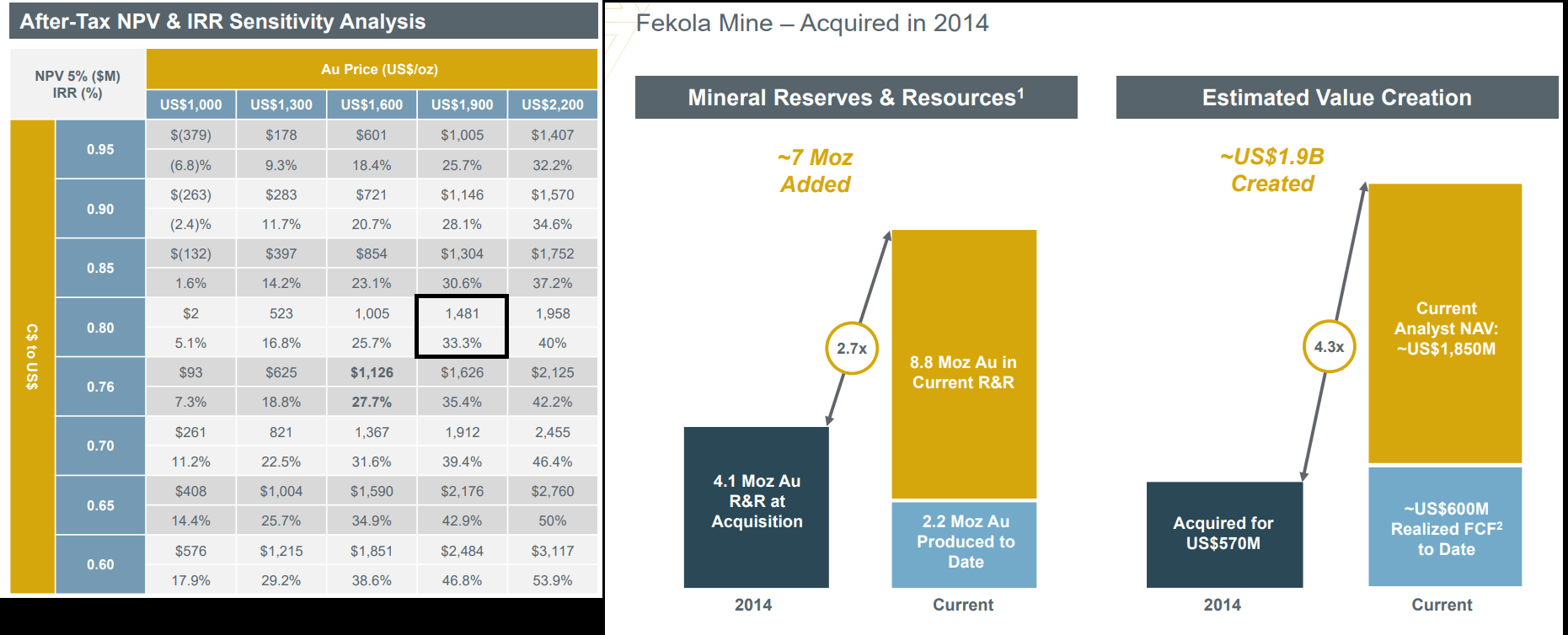

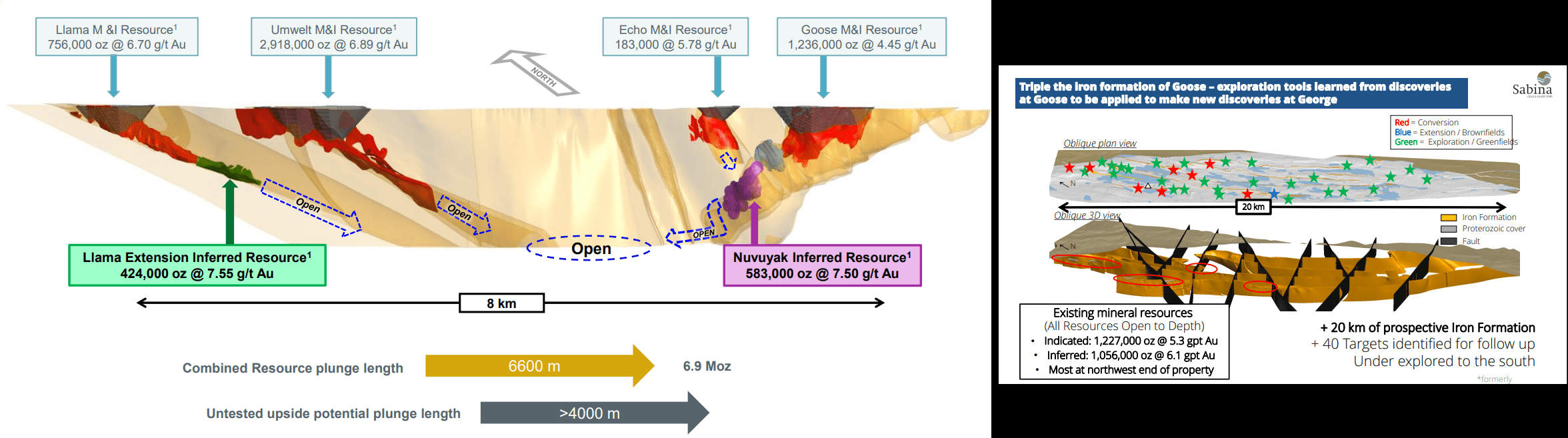

Looking at project economics (left hand side of chart below), we can see that even without the positive impact of 4,000 tonnes per day upfront and based on just a fraction of the total resources across the 80 kilometer belt, Goose's NPV (5%) sits at ~$1.25 billion at $1,950/oz gold or closer to ~$1.10 billion baking in some conservatism from inflationary pressures. However, this mine plan is based on just four deposits (Llama, Umelt, Echo, Goose Main), and does not include a significant high-grade resource at Nuvuyak (583,000 ounces at 7.50 grams per tonne of gold), nor does it include the high-grade Llama Extension with 424,000 ounces at 7.55 grams per tonne of gold. Plus, with average banded iron formation potential of ~1.5 million ounces per 1,000 meters and significant untested potential down-plunge and new recent discoveries in Hook and Wing, this could ultimately be a 22+ year mine life at ~245,000 ounces per annum (life-of-mine average) or ~5.1 million ounces of recoverable gold (~5.5 million ounces of reserves at ~93% recoveries) vs. the ~3.6 million ounces of reserves in inventory today.

The average conversion rate of inferred resources to date is 73%, and even at a more conservative conversion rate of 65% on current inferred resources this would translate to ~650,000 ounces from Llama Extension and Nuvuyak alone. Plus, as B2Gold has demonstrated at Fekola, it has a strong track record of increasing resources/reserves and adding value to its flagship assets.

Goose Project Sensitivity Analysis + Value Creation Fekola - B2Gold Presentation Goose Project Pits & Upside - B2Gold Presentation

{kind=link}

{kind=link}

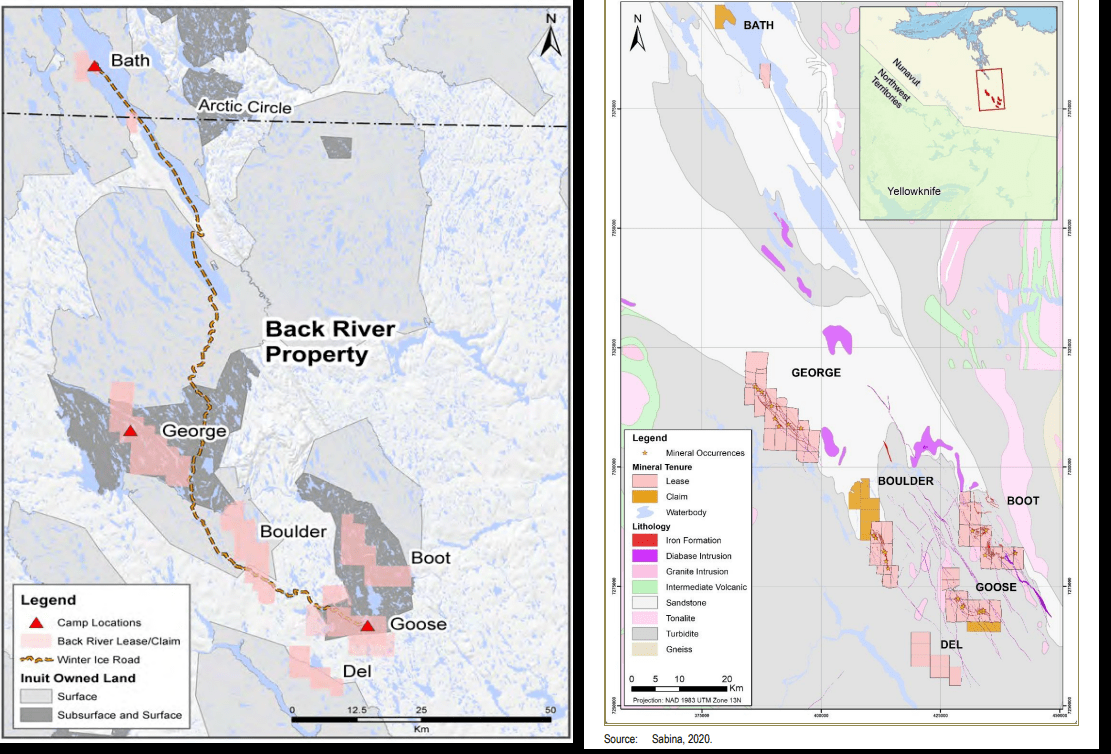

Looking at the bigger picture potential outside of opportunities to grow reserves at Goose, we can see an image of George (right image) which is home to ~2.28 million ounces of gold at ~5.6 grams per tonne of gold and has triple the iron formation of goose with over a dozen targets. This represents significant upside and could ultimately be a satellite opportunity ~50 kilometers northwest of Goose, similar to Amaruq, which has been a key contributor that also lies ~50 kilometers northwest of Agnico Eagle's ( AEM ) Meadowbank Mine in Nunavut. And while it's still early days at Goose, the fact that there's an iron formation triple the size of a project that's already home to 7.0 million ounces and other targets with iron formations (Boulder - possible extension of George, and Boot).

Plus, these relatively untested targets (Boulder, Boot, Del) sit on a combined ~270 square kilometers of land and haven't received nearly as much drilling with less than 50,000 meters of combined drilling vs. ~370,000 meters at Goose and ~190,000 meters drilled at George that has delineated a resource of ~6.9 and ~2.3 million ounces of gold to date, respectively.

Current Goose Resource Base, Exploration Upside & Geroge Project - Company Presentation

{kind=link}

Back River Gold Belt & Land Package - Company Presentation, 2021 TR

{kind=link}

Finally, as for recent developments, B2Gold recently hit 22.0 meters at 7.79 grams per tonne of gold over 100 meters down plunge from existing resources at Llama. In addition, intercepts like 17.05 meters at 17.14 grams per tonne of gold and 16 meters of 14.28 grams per tonne of gold have confirmed the continuity of high-grade mineralization at the Umwelt deposit, with B2Gold stating that "several drill holes have returned intercepts with higher gold grades and widths than predicted by the resource model." Plus, the company saw encouraging intercepts from George (possible satellite potential later in mine life), with the best intercept hitting 7.50 meters at 19.17 grams per tonne of gold.

Finally, B2Gold noted that it is changing the mining method to long-hole stoping from cut and fill/drift and fill previously to lower underground mining costs and improve productivity, while open-pit mining is being optimized to increase mining rates while utilizing the same equipment.

Underground mining costs were previously estimated at ~$66/tonne (~$92/tonne with sustaining capital) which already looked very ambitious compared to other Nunavut operations but the change in the mining method if implemented successfully may help to partially offset some inflation and what looked to be low estimates from the dated 2021 study.

2024/2025 Outlook

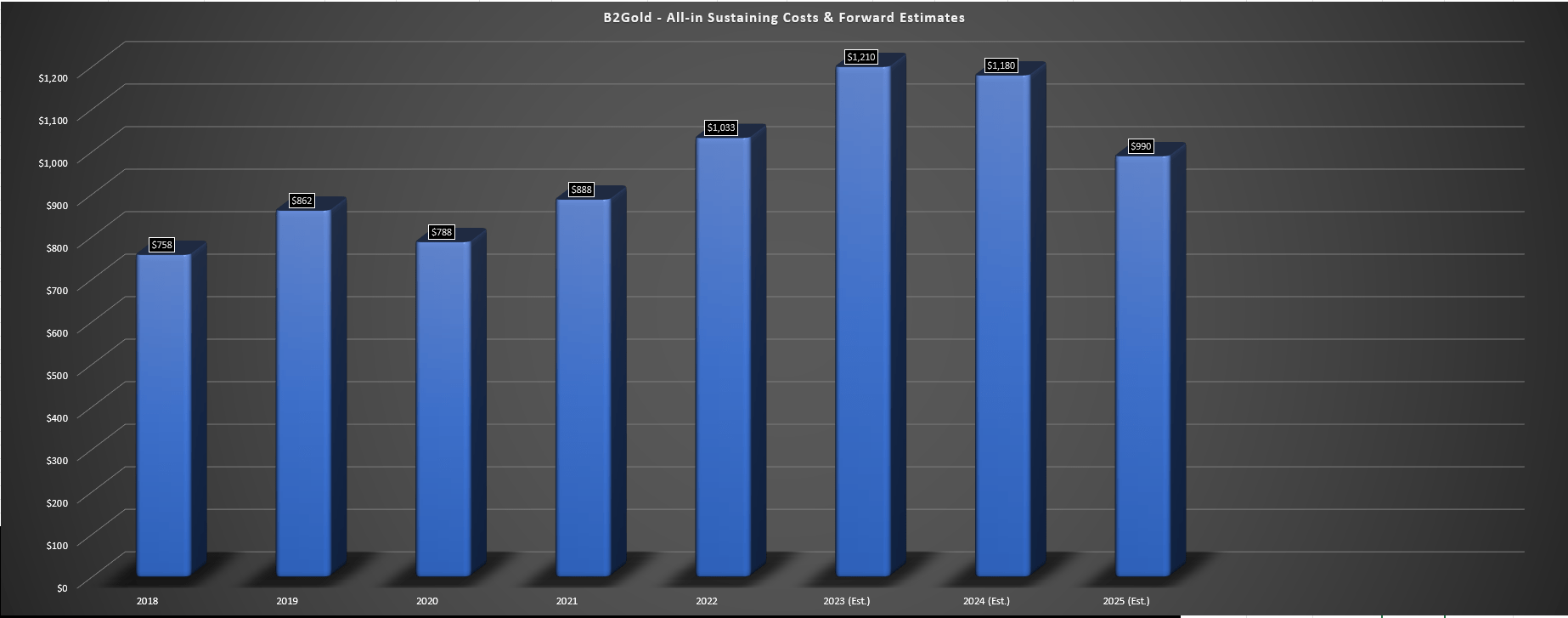

While the addition of the Back River Project to B2Gold's portfolio is certainly positive, the stock has been under pressure due to a significant decline in free cash flow generation (understandably as it builds a major project in the Arctic), and significantly higher all-in sustaining costs [AISC]. In fact, all-in sustaining costs have increased to $1,182/oz year-to-date (~$1,210/oz estimates in 2023) compared to three-year average AISC (2020-2022) of ~$890/oz. However, as noted in past updates , 2022 has been a year of significant sustaining capital spend (new TSF construction, new/replaced mining equipment, solar plant expansion costs, and ~$100 million in capitalized stripping at Fekola), and we should see more normalized sustaining capital next year to bring B2Gold's costs more in line with what investors have been accustomed to with margins typically being above that of its peers.

B2Gold Annual AISC & Forward Estimates - Company Filings, Author's Chart & Estimates

{kind=link}

Unfortunately, while all-in sustaining costs should improve slightly year-over-year, 2024 will be a less ebullient year given that we will likely see lower production due to the delay in receiving exploitation permits for Bantako North and lower grades at Fekola, pointing to lower production from its flagship asset. This means that without a further rise in the gold price we'll see lower operating cash flow year-over-year, and when combined with significant growth capital at Goose, free cash flow will come in below $120 million, a significant decline from the ~$600 million generated in 2020 when the stock briefly headed above US$7.00 per share. However, while this near-term outlook of lower free cash flow generation may be keeping a lid on the stock relative to peers like Lundin Gold ( LUGDF ) with ~28% free cash flow margins, we should see a massive turnaround in 2025 for B2Gold from a financial standpoint.

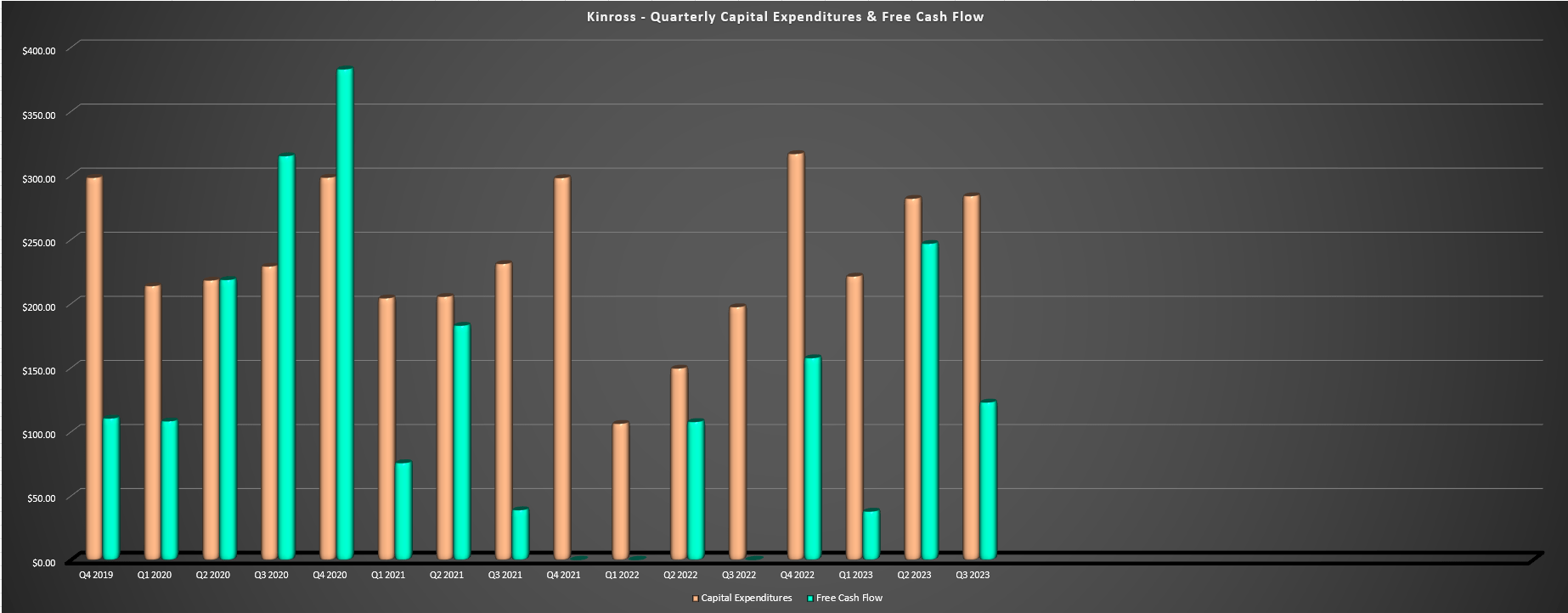

Outside of the benefit of bringing one of the highest-margin mines globally online in Q1 2025 (~290,000 ounces at sub $825/oz AISC in its first year), B2Gold will see a significant drop in capital expenditures, with capex likely to come in below $440 million in 2025. This suggests the potential to generate up to $750 million in free cash flow in 2025 (~600% growth from 2024 levels) with higher margins and a 1.2+ million ounce production profile. If achieved, this free cash flow figure would amount to more free cash flow than Kinross ( KGC ) expects to generate this year, and it trades at twice B2Gold's valuation (~$9.0 billion enterprise value vs. ~$3.8 billion for B2Gold) with a weaker balance sheet and lower margins.

Kinross - Quarterly Capex & Free Cash Flow - Company Filings, Author's Chart

{kind=link}

Some of this premium can be attributed to Kinross' superior jurisdictional profile on balance (Nevada, Alaska, Ontario (development), Chile, Mauritania, Brazil), greater diversification and scale (six mines) and higher NAV. Still, B2Gold should be able to play catch-up to some of its peers that have outperformed this year with this level of free cash flow in 2025, suggesting it's one of the better turnaround plays in the sector for patient investors.

Valuation

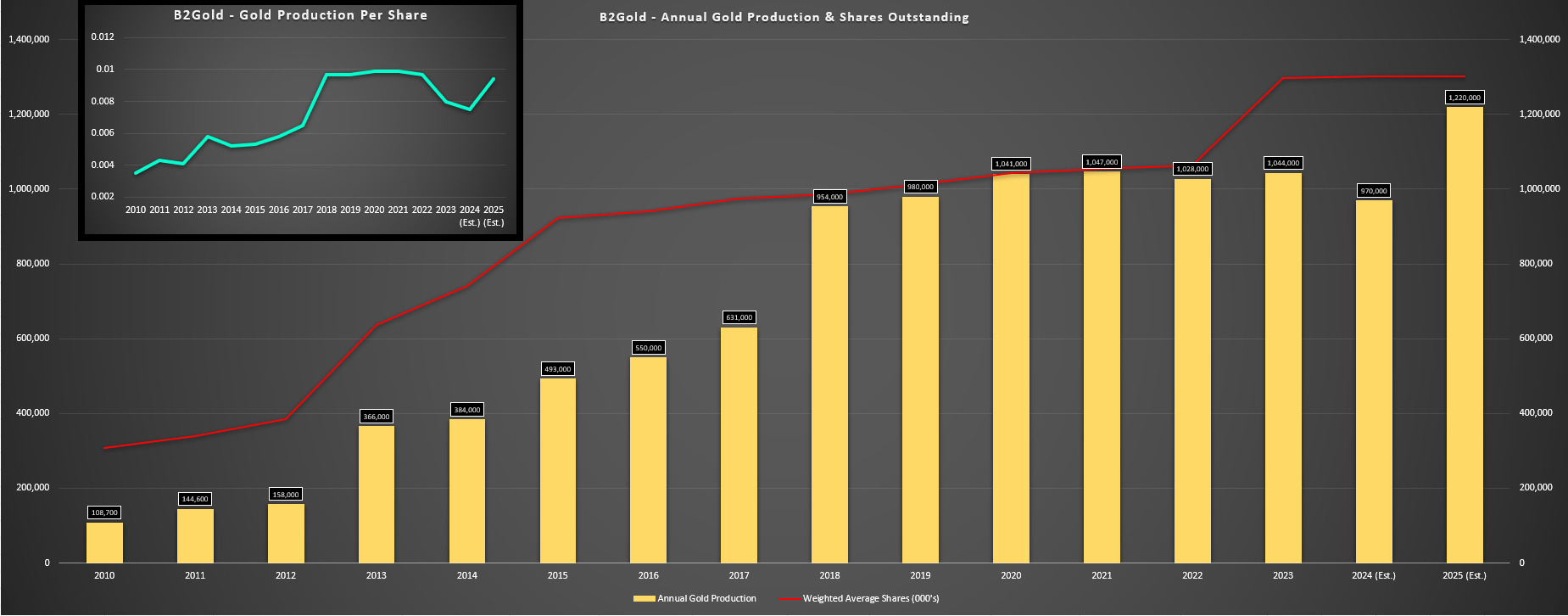

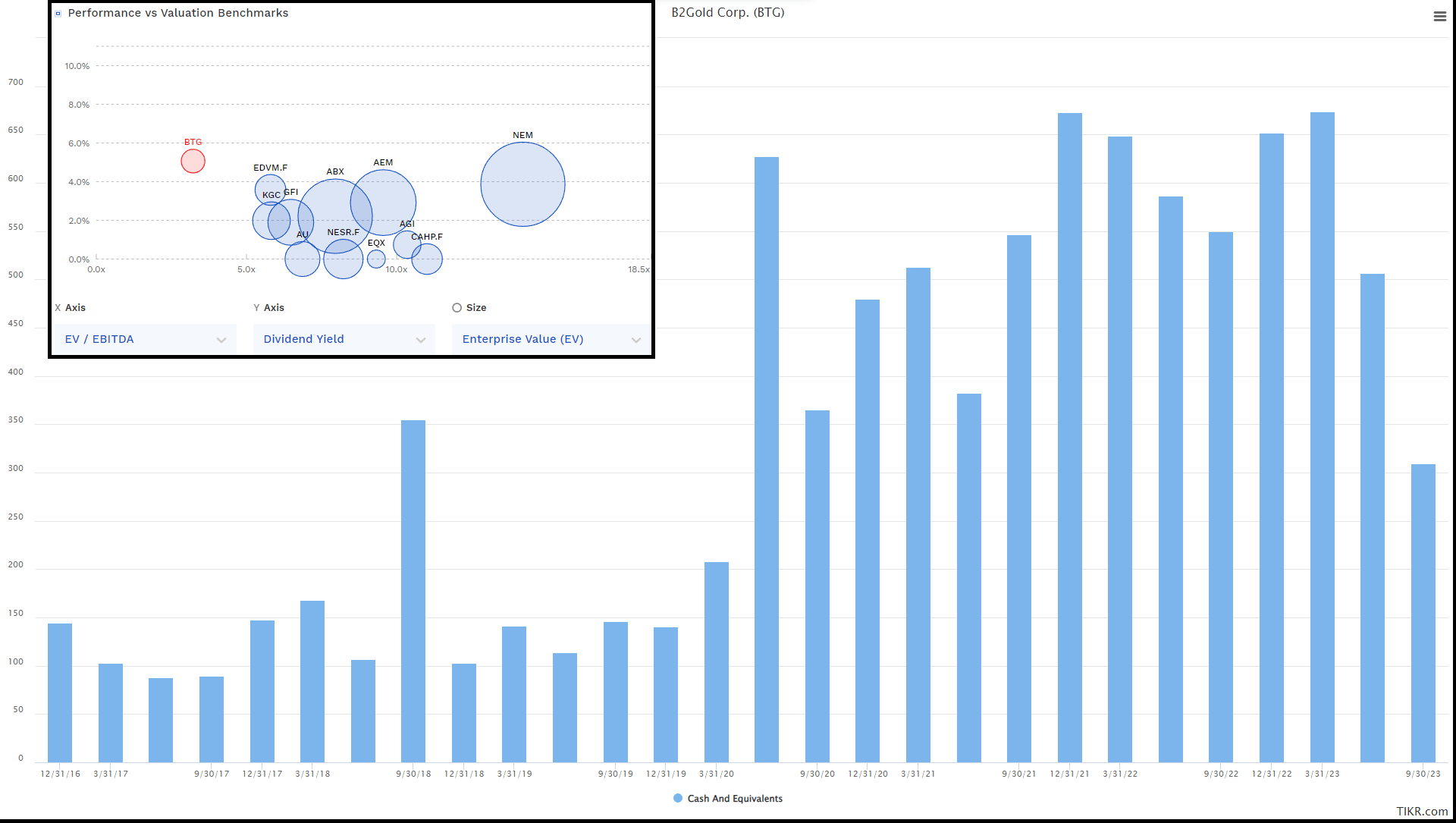

Based on ~1.30 billion shares and a share price of US$3.06, B2Gold trades at a market cap of ~$4.0 billion, and an enterprise value of ~$3.8 billion. This makes B2Gold one of the lowest capitalization intermediate/senior producers in the sector today and one of the highest yield names in the sector, with a dividend yield of ~5.2%. Notably, this is despite B2Gold having a glowing track record of per share growth , boasting one of the best production growth per share track records among its peers.

In addition, the company managed to finally add a Tier-1 ranked jurisdiction to its portfolio with minimal hit to its production growth per share (2025 estimates) due to acquiring counter-cyclically like it did with Papillon in 2014, and with it paying just ~0.80x P/NAV for Sabina to lock up its Goose Project and a massive 80 kilometer belt with multiple early-stage and advanced exploration targets.

To illustrate the benefit of acquiring counter-cyclically vs. at a cyclical high for the gold developers, B2Gold's purchase price for Sabina of ~$940 million was far less than Kinross' Great Bear acquisition for ~$1.46 billion and at a multiple of 0.80x P/NAV vs. consensus NAV of ~1.0x P/NAV for Great Bear, although Great Bear was over eight years from commercial production at Dixie (2030? vs. 2022) vs. just two years at the time of the acquisition closing for B2Gold/Sabina.

B2Gold - Annual Gold Production, Shares Outstanding & Gold Production Per Share + Forward Estimates - Company Filings, Author's Chart & Estimates B2Gold Cash & Cash Equivalents, Valuation, Dividend Yield & EV/EBITDA Multiple vs. Peers - TIKR, Finbox

{kind=link}

{kind=link}

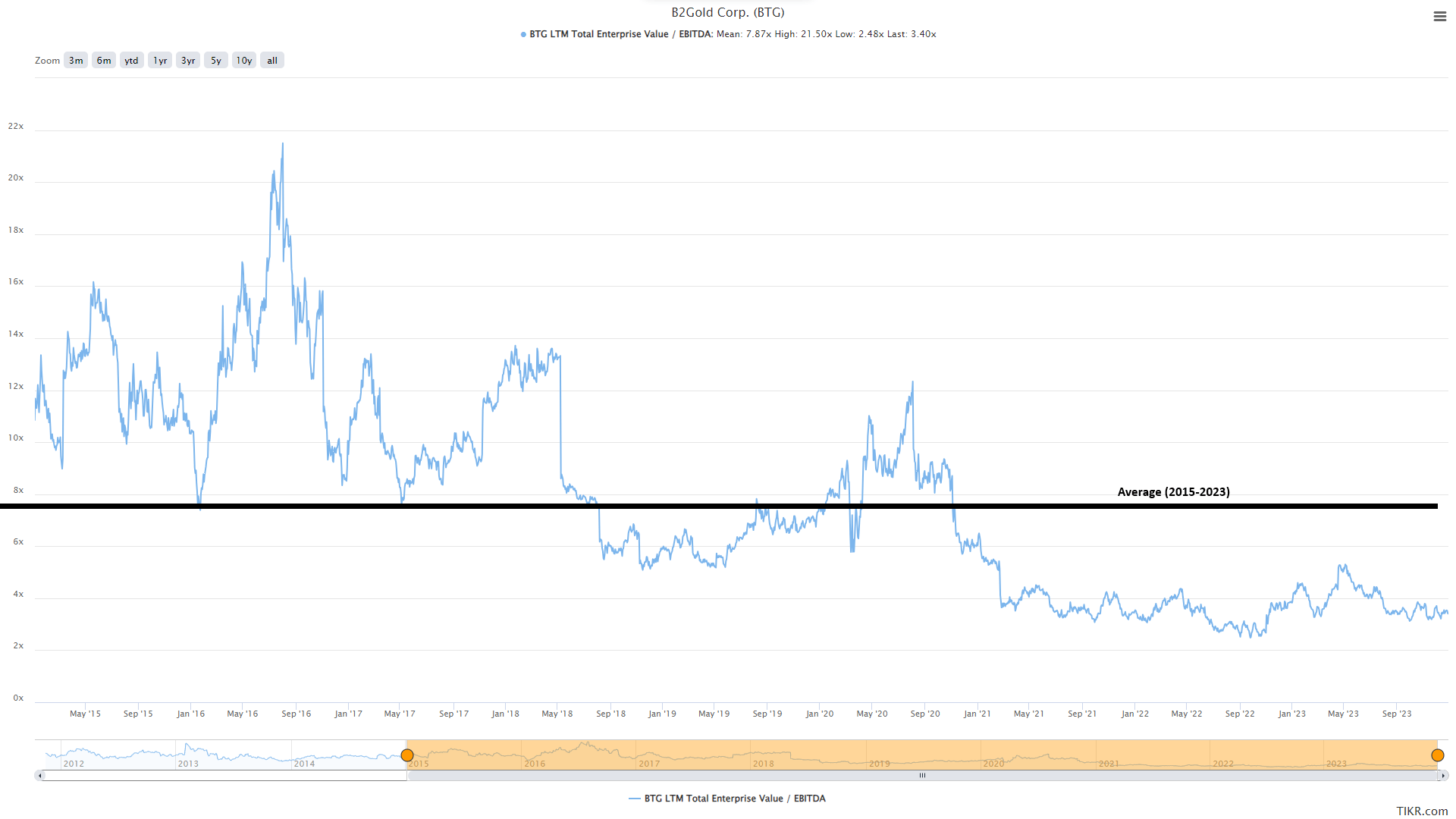

Looking at B2Gold's historical multiples, the stock has traded at an average multiple of ~9.9x cash flow since 2010, and it currently trades at just ~5.2x FY2023 cash flow per share estimates. Using what I believe to be a more conservative multiple of 8.5x cash flow and 1.0x P/NAV (and a 65/35 weighting to P/NAV vs. P/CF) based on its increased diversification/addition of a Tier-1 jurisdiction offset by its lower growth rate as it's become more mature and using FY2025 cash flow per share estimates of $0.92, I see a fair value for the stock of US$4.70. This points to a 51% upside from current levels, but closer to 56% on a total return basis given B2Gold's ~5.1% dividend yield.

B2Gold - Historical EV/EBITDA Multiple - TIKR

{kind=link}

That said, we could certainly see some upside to this figure as FY2025 cash flow per share would come in closer to US$1.00 at spot levels, and the company can generate ~$750 million in free cash flow in FY2025 (assuming Goose remains on schedule with a smooth first year of production). Plus, even if we use a more conservative multiple of 10.0x free cash flow (B2Gold peaked at ~13.0x free cash flow at its 2020 highs), we could see B2Gold trade as high as US$5.70 per share.

In summary, I would argue that B2Gold's fair value estimate of US$4.70 by year-end 2025 could end up being conservative, and I would not be surprised to see the stock trade back above US$5.50 in the next two years given that it's more desirable as an investment than it ever has been with less of its cash flow/NAV tied to Mali and another high-margin asset with scale in its portfolio on top of Fekola.

Summary

B2Gold trounced the performance of the Gold Miners Index from 2016 through 2020, but has since suffered a 60% plus drawdown, significantly underperforming sector leaders like Alamos Gold ( AGI ). However, unlike other sector laggards, B2Gold has a strong track record of creating shareholder value, continues to return capital to shareholders in a disciplined manner, and it is now the best positioned it's ever been with four mines in four countries and early/advanced stage development opportunities in other countries that could fuel its next leg of growth (Finland, Colombia, Mali [Fekola Regional].

Plus, as noted earlier, Goose could end up being just the tip of the iceberg in an upside-case scenario, with the potential for a ~400,000 ounce production profile at the end of this decade in Nunavut alone if it can scale up to ~6,000 tonnes per day at an average grade of 6.0 grams per tonne of gold.

To put this opportunity in perspective, B2Gold could see annual gold production of ~1.1 million ounces from Fekola and Back River combined with Fekola Main + Fekola Regional and an expansion at Back River, with these being high-margin ounces. Hence, this would more than offset Otjikoto heading offline later this decade when combined with Masbate and Calibre attributable ounces. Finally, this doesn't contemplate further production from Gramalote (if pursued) which could be a ~200,000 ounce per annum opportunity.

To summarize, B2Gold's pipeline is stronger than ever, production will hit new all-time highs in 2025, all at the same time as margins and reserve grades sit above the sector average. So, with significant free cash flow growth on deck post-2024, I would view any sharp pullbacks in the stock as buying opportunities.

For further details see:

B2Gold: A Free Cash Flow Machine Post-2024