CA - B2Gold: Ignore The Weak Q3 Results

2023-11-27 16:22:54 ET

Summary

- B2Gold's Q3 production was below plan due to an intense precipitation event at Fekola that impeded access to high-grade P6 ore.

- The result, when combined with elevated sustaining capital, was that AISC was higher year-over-year despite the benefit of lower fuel costs, but will still meet FY2023 guidance.

- In this update, we'll dig into the Q3 results, recent developments, and where the stock's updated low-risk buy zone lies.

The Q3 Earnings Season for the VanEck Gold Miners ETF ( GDX ) is finally over, and while quite a few miners have traded higher since their reports, B2Gold Corp. ( BTG ) is an exception. This may be attributed to the fact that we still have some uncertainty related to decrees which have yet to be announced (that should not affect the existing mining code and its current Fekola Main operations but only future potential mining areas like Fekola Regional) and that permits are still outstanding for Bantako North (a planned source of saprolite feed this year). Unfortunately, this means that no gold production is expected from Bantako North this year, resulting in Fekola being expected to deliver at the low end of guidance. In this update, we'll dig into the Q3 results, recent developments, and where the stock's updated low-risk buy zone lies.

{kind=link}

Q3 Production & Sales

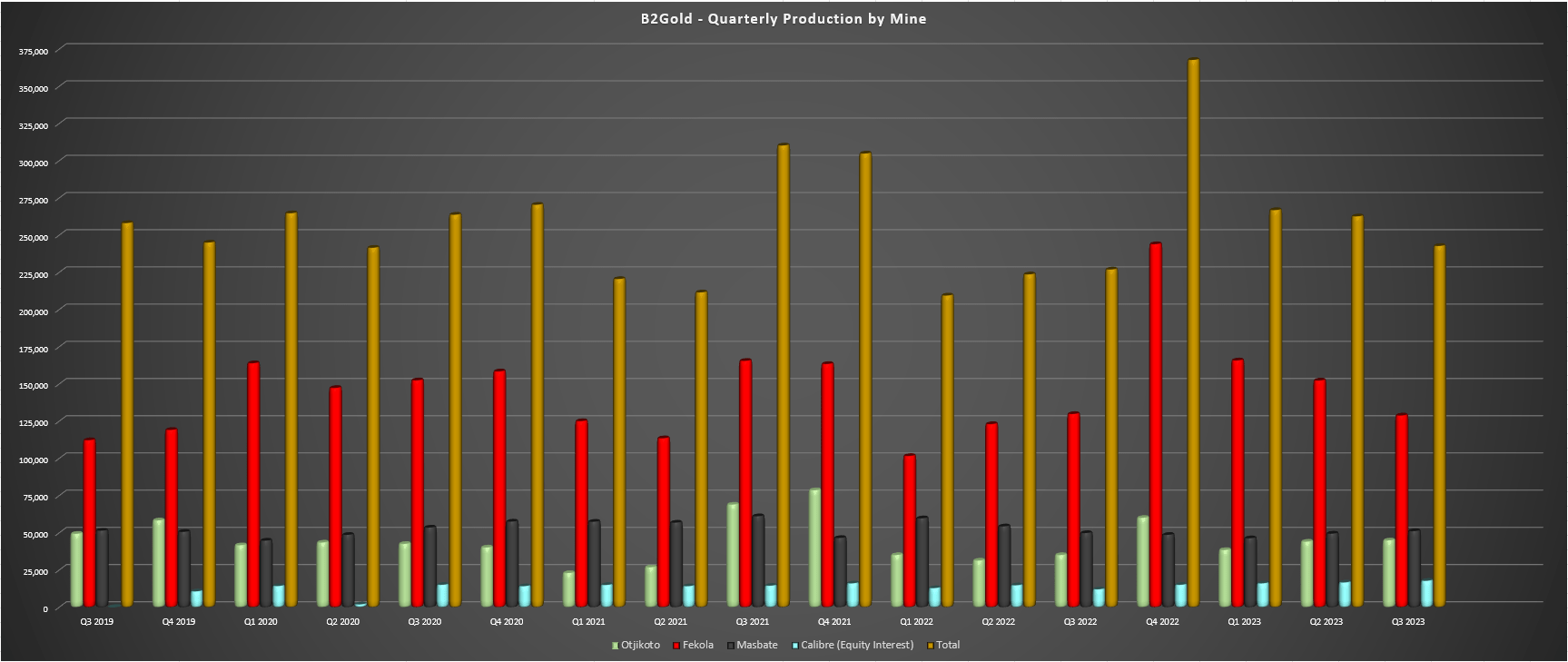

B2Gold released its Q3 results earlier this month, reporting quarterly production of ~225,100 ounces of gold (~242,800 ounces when including its equity investment) in Calibre Mining Corp. ( OTCQX:CXBMF ), a 7% improvement from the year-ago period. The increased gold production was related to a higher contribution from Calibre and a better than planned quarter at Masbate (10% above budget) on the back of higher throughput which more than offset lower grades processed in the period. Unfortunately, this was offset by a weaker than expected quarter at its Fekola Mine with production of ~128,900 ounces, down marginally year-over-year despite lapping relatively easy comparisons after a softer Q3 2022 due to the rainy season last year. The company noted that this was related to an intense precipitation event, impeding access to the higher grade Phase 6 ore.

B2Gold Quarterly Production by Mine - Company Filings, Author's Chart

{kind=link}

Digging into the results a little closer, Fekola processed ~2.39 million tonnes at 1.82 grams per tonne of gold (Q3 2022: ~2.29 million tonnes at 1.90 grams per tonne of gold) with lower grades related to having to rely on some stockpile material, in addition to slightly lower production from lower recovery rates (92.1% vs. 93.1%). And even with the benefit of higher ounces sold from inventory, we saw a significant increase in all-in sustaining costs to $1,261/oz (Q3 2022: $978/oz) given the sharp increase in sustaining capital $72.5 million vs. $18.7 million) in the period and an increase in sustaining capital vs. the prior 2023 budget. That said, total cash costs were lower, guidance is still on track for the mid-point of the year when adjusting for no production from Bantako North in 2023, and we should see a better Q4 vs. Q3 with production of ~134,000 to 141,000 ounces assuming delivery into the lower end of guidance (580,000 to 610,000 ounces), with mining of Phase 6 ore resuming in October.

Moving over to Masbate, it was a solid quarter for the mine, with production of ~51,200 ounces vs. ~49,900 ounces in the year-ago period. During Q3, the mine processed ~2.16 million tonnes at 1.01 grams per tonne of gold at all-in sustaining costs of $1,124/oz on the back of better than planned grades and throughput rates. This has left the mine on track to deliver toward or above the high end of annual guidance, and below its expected cost guidance with the benefit of lower fuel costs and higher production. As for Otjikoto in Namibia, production also improved year-over-year with higher grades from Wolfshag Underground (1,259 tonnes per day at 5.55 grams per tonne of gold), lifting overall grades to 1.66 grams per tonne of gold in Q3. Meanwhile, all-in sustaining costs were also lower year-over-year, benefiting from easier comparisons (Q3 2022: $1,625/oz), a weaker Namibian Dollar, and lower than planned sustaining capital (underground development and deferred stripping).

{kind=link}

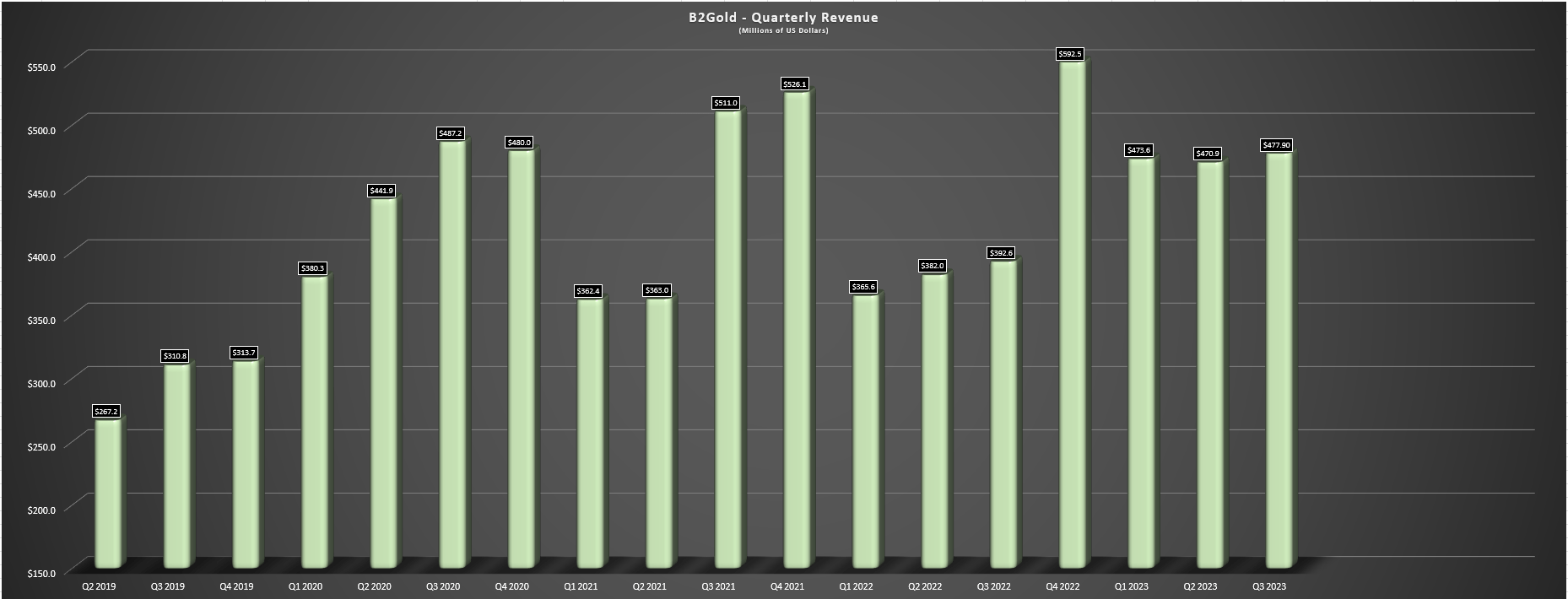

Given that Otjikoto and Masbate were able to pick up some of Fekola's slack (13,300 ounces below Q3 budget) and with the benefit of a higher average realized gold price and more ounces sold than produced, B2Gold's revenue increased 22% year-over-year to $477.9 million, working capital increased to $110.2 million ($191 million before working capital changes), and adjusted earnings came in at $64.8 million (Q3 2022: $32.0 million). That said, the company ended the quarter with a lower cash position of $310 million given the significant increase in capital expenditures at Fekola (~$83 million) and Goose construction (~$88 million), with total capital expenditures up sharply year-over-year to $225.6 million. On a positive note, although capex will remain elevated next year in the final year of construction for Goose in Nunavut, we should see more normalized capital expenditure at Fekola in 2024, with the company likely to generate positive free cash flow even during major construction if gold prices remain at current levels.

Costs & Margins

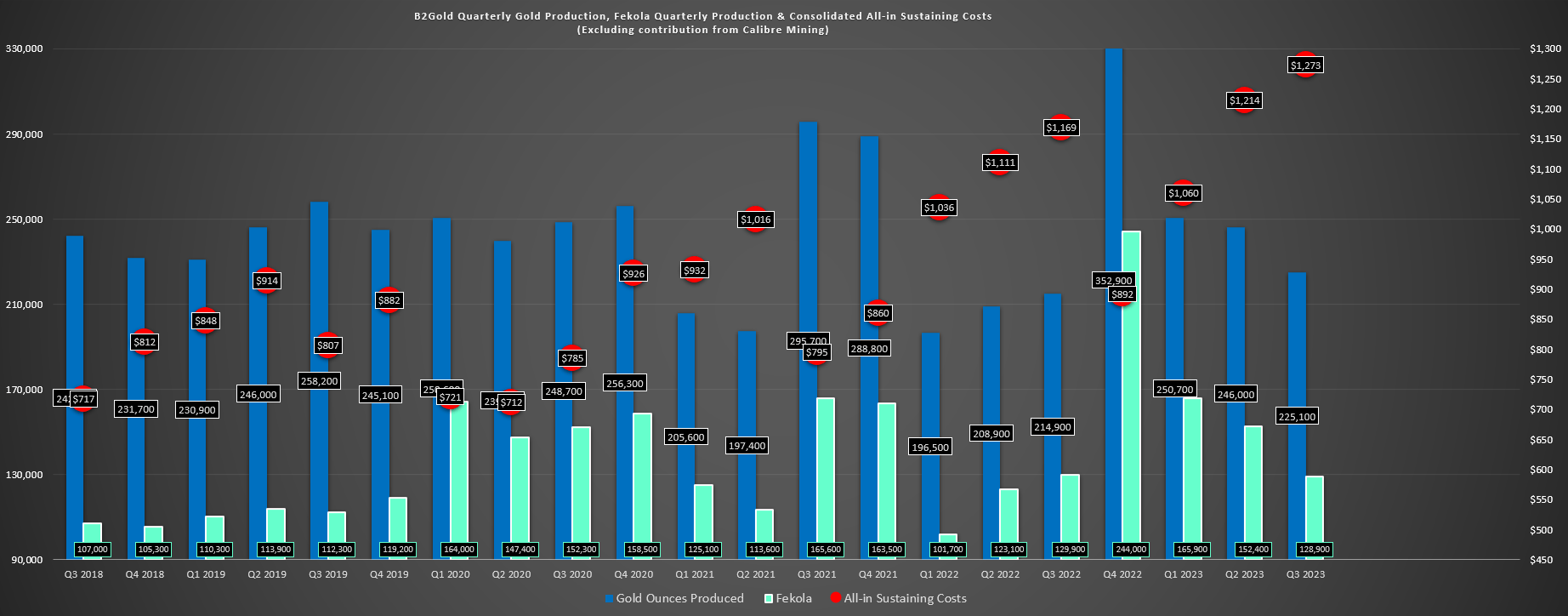

Moving over to costs and margins, B2Gold's total cash costs came in at $840/oz or $827/oz excluding its equity investment in Calibre vs. $939/oz and $926/oz in the year-ago period, respectively. The lower costs were related to much lower costs at Otjikoto after a weaker production quarter in Q3 2022 (delay bringing Wolfshag UG into production), lower than planned fuel costs and a weaker Namibian Dollar, and lower costs at Fekola (lapping easier comparisons) with fewer ounces sold in the year-ago period and elevated fuel and explosive prices. Meanwhile, from an all-in sustaining cost standpoint [AISC], consolidated AISC came in at $1,272/oz ($1,182/oz year-to-date) up nearly 9% from $1,169/oz in the year-ago period. However, it's important to note that this was largely because of a significant increase in sustaining capital at Fekola, which was expected given the meaningful sustaining capital spend this year (offset by higher ounces sold vs. produced).

B2Gold - Quarterly Production & AISC (Operating Mines) + Fekola Production - Company Filings, Author's Chart

{kind=link}

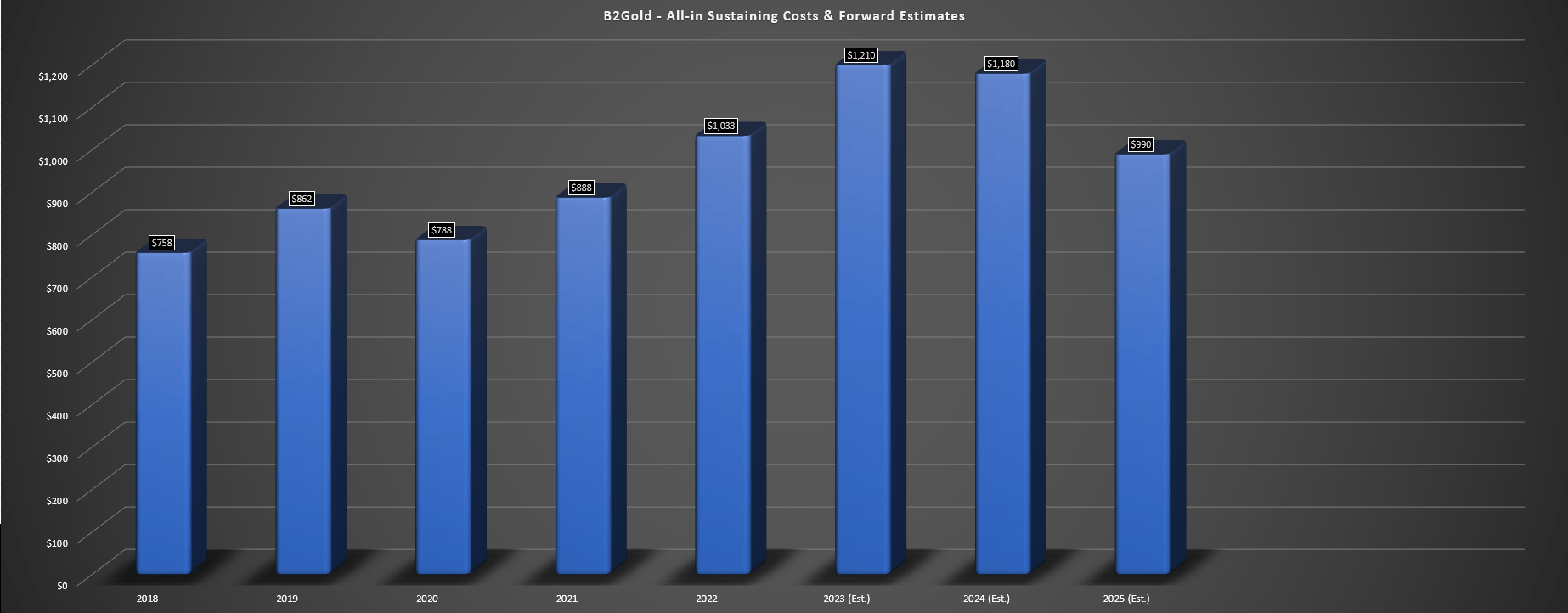

Digging into all-in sustaining costs a little closer, sustaining capital came in at ~$94.7 million (+127% year-over-year), with this mostly at Fekola where sustaining capital came in at $72.5 million. The company noted that sustaining capital will be $50 million above its initial budget laid out at year-end 2022, which will include $11 million for solar plant expansion costs and $35 million for new mobile fleet and capital rebuild costs at Fekola. That said, B2Gold noted that all-in sustaining costs are tracking to the "low end" of its $1,195/oz to $1,235/oz range with a strong Q4 on deck at its flagship asset and AISC at $1,182/oz year-to-date vs. budget of $1,235/oz. Hence, the sharp rise in AISC should not alarm investors and while costs were elevated compared to what investors have become accustomed to from this high-margin producer, this is largely because of a much busier year for spending at Fekola (new TSF construction, new/replaced Fekola mining equipment, and ~$100 million in capitalized stripping).

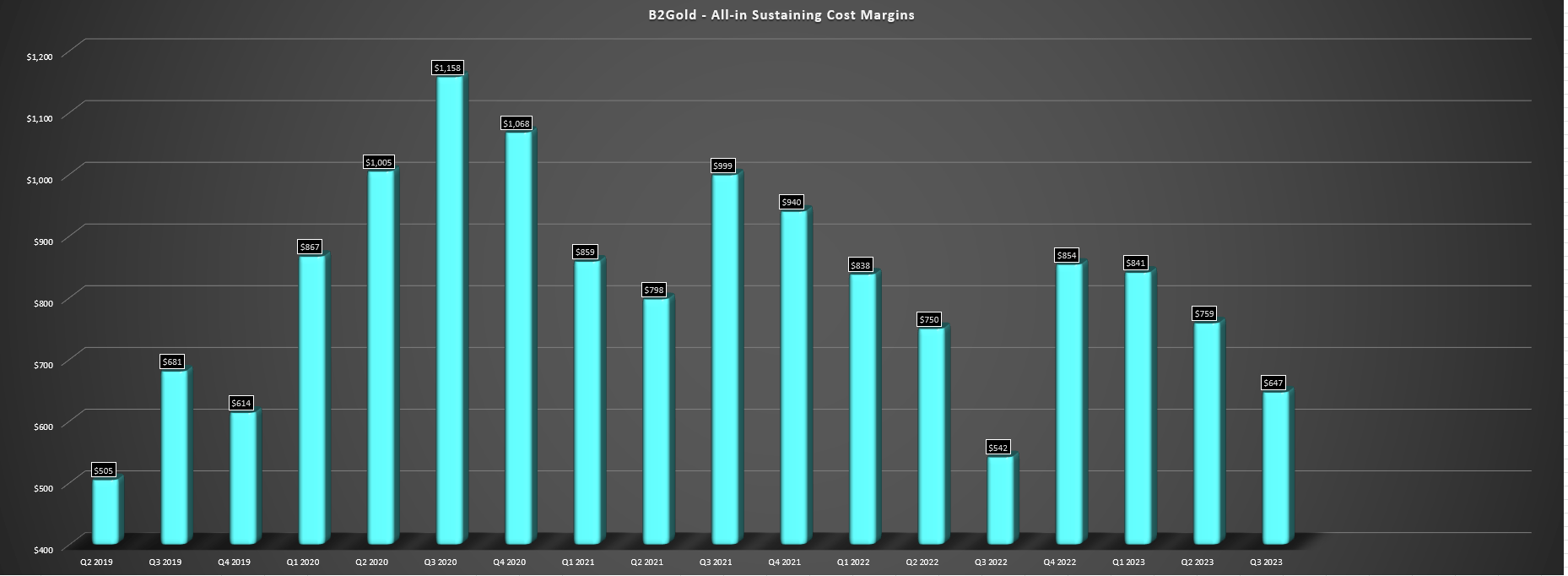

Fortunately, AISC margins improved year-over-year despite the higher AISC because of the strength in the gold price ($647/oz vs. $557/oz), and this year should mark peak costs for B2Gold. This is because sustaining capital expenditures should normalize next year at Fekola after a capital intensive year in 2023 and the company will benefit from two high margin assets in 2025. For starters, the Goose Project in Nunavut is expected to have industry-leading AISC (sub $900/oz when adjusting for inflationary pressures) and B2Gold will benefit from three quarters of production based on the Q1 2025 start date. Second, B2Gold will benefit from Calibre adding a high-margin asset at Valentine (sub $950/oz AISC in early years) if the recently proposed acquisition of Marathon Gold Corporation ( OTCQX:MGDPF ) goes through, offering a slight tailwind from a consolidated cost standpoint and pushing B2Gold's AISC back to industry-leading levels below $1,000/oz in 2025 and 2026. Third, Fekola will be back to its usual industry-leading costs, especially if it can flex production with more material north of the mine (Bantako North, pending permits).

B2Gold Quarterly AISC Margins - Company Filings, Author's Chart B2Gold Annual AISC & Forward Estimates - Company Filings, Author's Chart

{kind=link}

{kind=link}

To summarize, I don't see any reason to get hung up on the higher costs in Q3, with a very high-margin asset on budget to start production in Q1 2025 and a tough quarter for Fekola because of another difficult rainy season combined with elevated sustaining capital spending. In fact, assuming all goes to plan, B2Gold should be one of the top-10 lowest-cost gold producers in 2025/2026 next to other larger producers like Agnico Eagle Mines Limited ( AEM ), Lundin Gold Inc. ( OTCQX:LUGDF ), Evolution Mining Limited ( OTCPK:CAHPF ) and Endeavour Mining plc ( OTCQX:EDVMF ).

Recent Developments

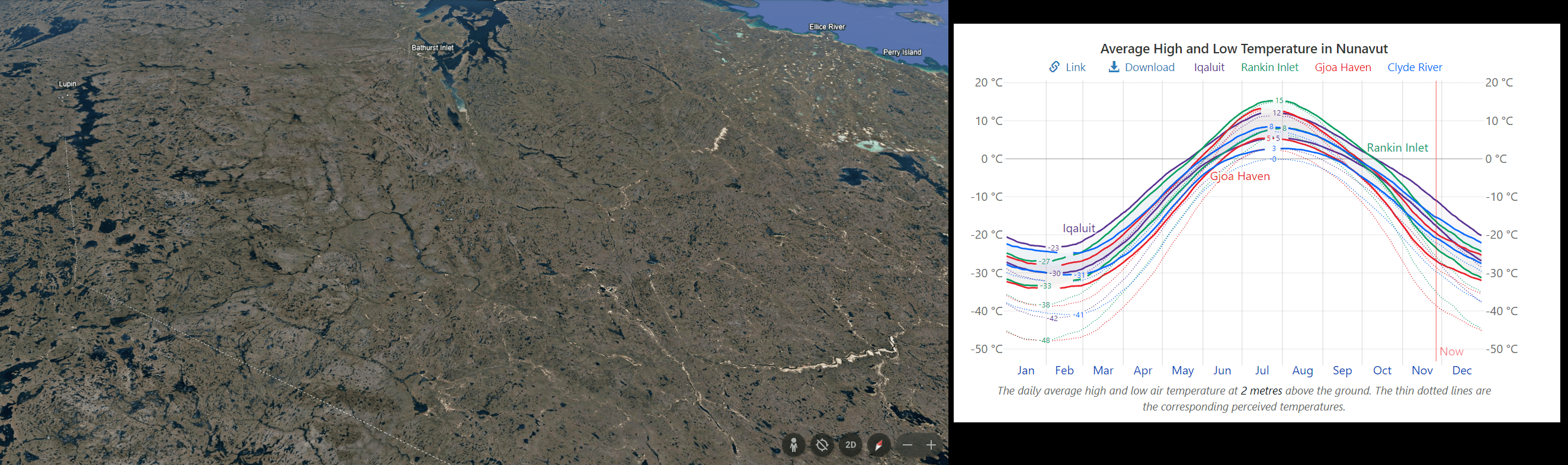

As for recent developments, investors will be pleased to know that B2Gold and Sabina (while it owned the asset) have put a meaningful dent in planned/revised upfront capex for Goose (~$670 million) with ~$300 million left to spend as of the end of Q3. From a funding standpoint, B2Gold can easily cover this capex from cash flow from its operations, ~$255 million in net cash and $700 million available ($50 million since drawn) on its RCF, giving it total immediately available liquidity of ~$950 million. As for construction progress, B2Gold noted that production remains on track for Q1 2025 and that the first concrete pour was completed in July 2023, with concrete/steel work in the mill area tracking ahead of schedule. Importantly, the erection of structural steel for the mill building, power house and truck shop has already begun and cladding on the mill building is over 50% completed while cladding of the powerhouse and truck shop has begun. This will allow B2Gold to work through the coldest months and has helped to de-risk delivering the mine on schedule.

Nunavut Weather, Project Location - Google Earth, WeatherSpark.com

{kind=link}

As for developments elsewhere in the portfolio, the company noted that its acquisition of the other half of the Gramalote Project is based on the potential to look at a smaller and higher-return project vs. the ~11.0 million tonnes per annum project previously envisioned (10.0+ million tonnes per annum throughput rate required to make it worthwhile for two million ounce producers to share). While we haven't gotten details on what this could look like yet, this would certainly reduce the likely upfront capex of $1.2+ billion on an inflation-adjusted basis, (Q1 2020 estimate: ~$900 million) but still be a project that would move the needle for B2Gold if approved with potential production of 200,000+ ounces per annum (similar size to Masbate and Otjikoto).

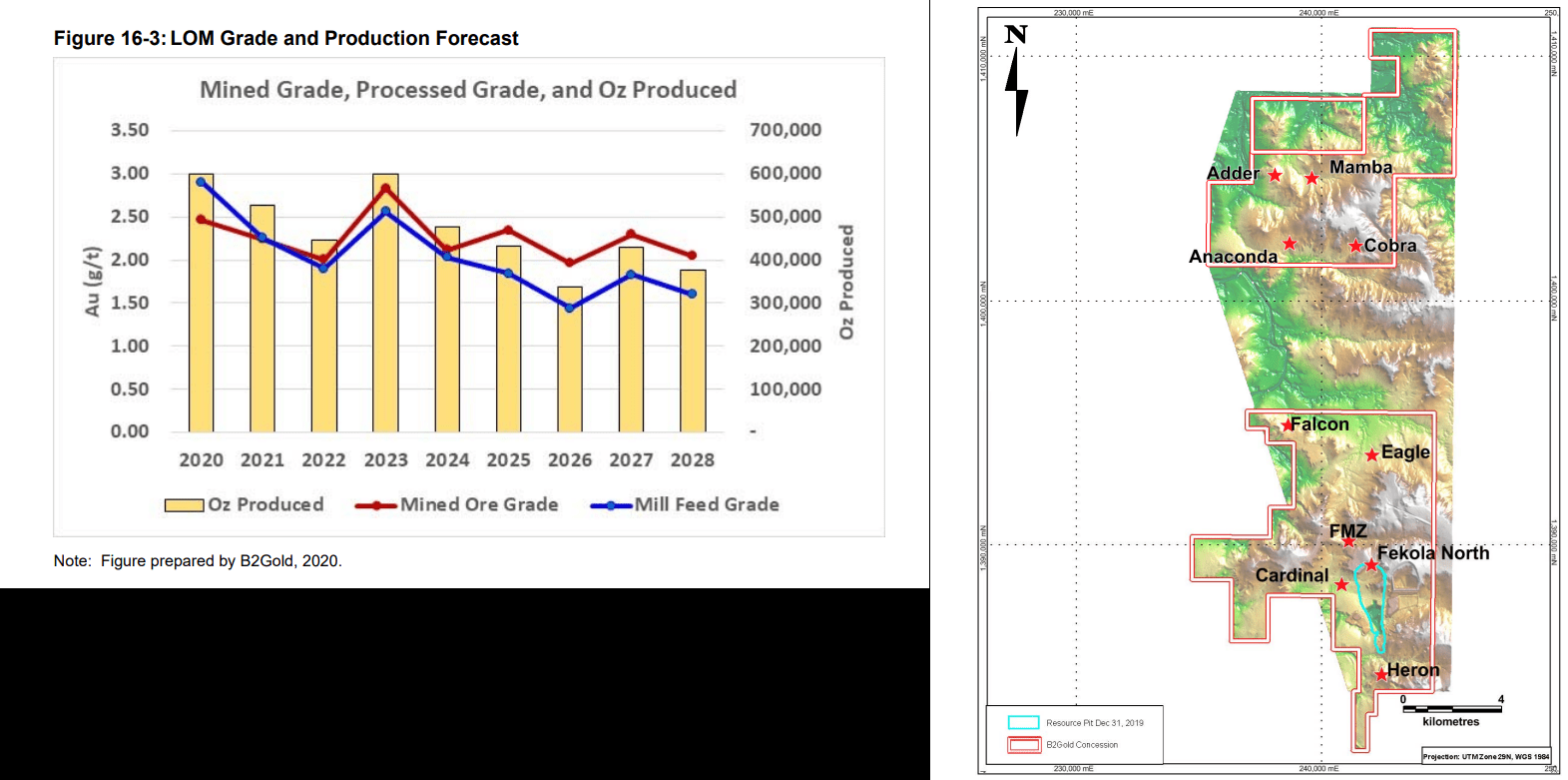

Fekola Mined Grade (2020 TR) & Regional Targets + Current Mine - 2020 Fekola TR

{kind=link}

Finally, the company noted that exploitation permits are still outstanding for Bantako North, which will allow for the trucking of ore from Anaconda to the Fekola Plant. This is expected to result in no production from Fekola Regional in 2023 (18,000 ounces previously budgeted), and depending on the timing of permit approvals could also result in lower production than previously hoped in 2024 at Fekola. That said, the company has got a head start with the haul road from Bantako North operational, and construction of haul roads, warehouse, workshop, fuel depot and offices on schedule for completion by year-end. In addition, the company noted that it continues to see support from the Malian government, who encouraged them to build the infrastructure for trucking ahead of the permit being granted. Plus, if contribution from Anaconda is light in what will be a lower production year for Fekola in 2024, B2Gold noted that it may be able to increase contribution from Cardinal (which is on its current Medinandi mining permit good until 2044) in the interim.

Summary

B2Gold's Q3 results were weaker than its peer group with AISC up sharply year-over-year, but it's important to note that cash costs were down year-over-year despite a softer quarter for its breadwinner (Fekola) and AISC remained below the industry average on a year-to-date basis ($1,182/oz vs. ~$1,360/oz). Plus, as discussed earlier, the higher AISC is largely a function of the elevated sustaining capital spend at Fekola this year ($267 million year-to-date including exploration and lease expenditures), which is up ~110% year-over-year and weighing on costs at the mine short-term. However, with a high-margin asset in the wings, a return to higher margins at Fekola and material production growth to 1.25+ million ounces in 2025, 2023 will likely mark the low for free cash flow generation and the trough for margins ahead of a much more profitable several years ahead. Hence, for investors looking for exposure to a gold producer with a solid track record and an attractive yield, I would view any pullbacks below US$2.90 as buying opportunities.

For further details see:

B2Gold: Ignore The Weak Q3 Results