CA - B2Gold: Tracking Well Against FY2023 Guidance

2023-05-10 10:39:11 ET

Summary

- B2Gold released its Q1 results this week, reporting quarterly production of ~266,900 ounces at total cash costs of $678/oz and all-in sustaining costs of $1,060/oz.

- This represented a significant improvement from the year-ago period, with B2Gold up against easy year-over-year comps due to lower grades at Fekola in Q1 2022.

- From a big-picture standpoint, B2Gold is tracking well against its 2023 guidance and has meaningful growth on deck with its new Goose Project and Fekola Complex plans.

- Given the upgrade to B2Gold's jurisdictional profile, the ability to maintain industry-leading margins with Goose and its reasonable valuation, I continue to see B2Gold as one of the more attractive names sector-wide.

We're nearly halfway through the Q1 Earnings Season for the Gold Miners Index ( GDX ) and one of the most recent companies to report its results is B2Gold ( BTG ). Like Agnico Eagle ( AEM ) and Alamos Gold ( AGI ), B2Gold put together a very solid start to the year, helped by improved grades at Otjikoto with a ramp-up in underground production from Wolfshag and high-grade Fekola P6 ore. The increase in grades and easy year-over-year comps helped the company to report a significant increase in output, and revenue and cash flow benefited from a higher average realized gold price. Let's take a closer look at the results below:

B2Gold Operations (Company Website)

{kind=link}

Q1 Production & Sales

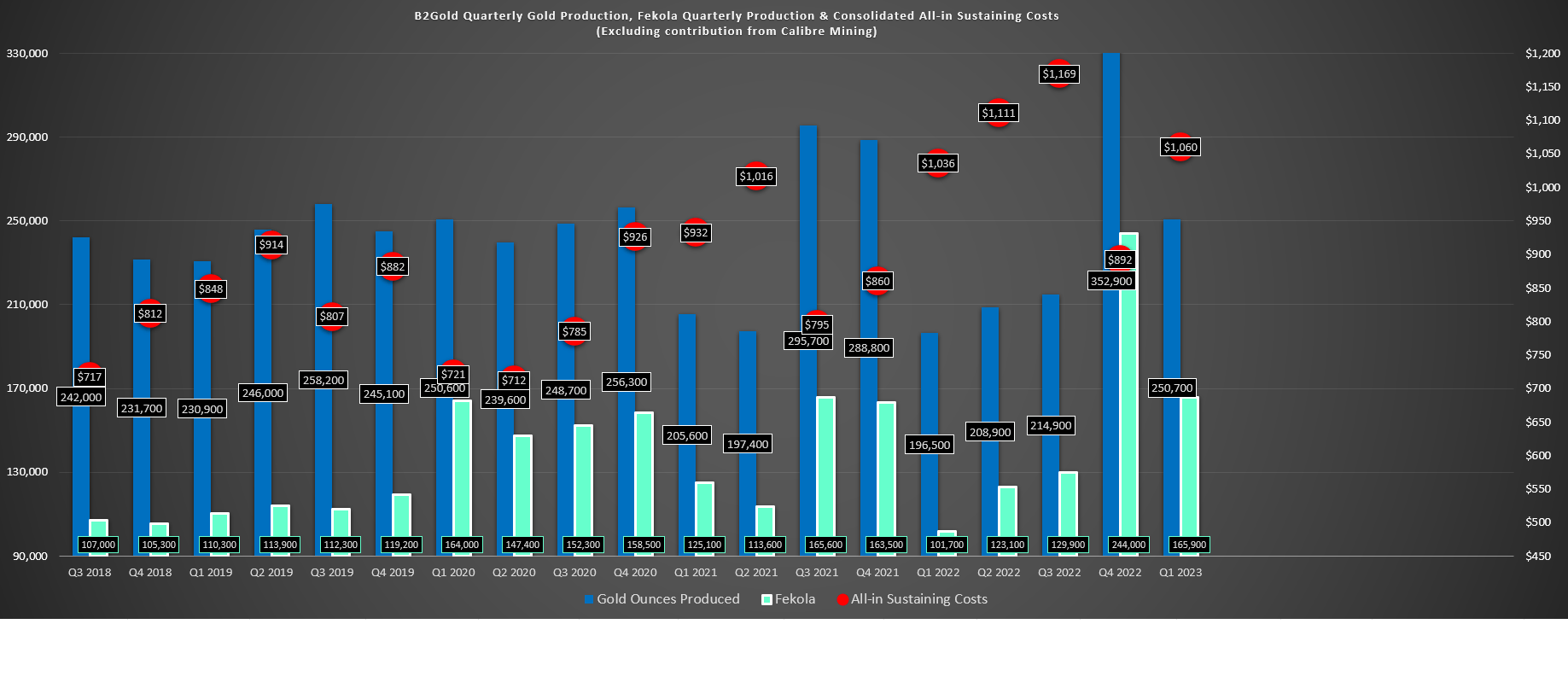

B2Gold released its Q1 results this week, reporting quarterly production of ~266,900 ounces of gold which was ahead of plan and included ~16,100 ounces of attributable production from its 25% stake in Calibre Mining ( CXBMF ). As noted, the solid performance was driven by another strong quarter from Fekola, which just came off a quarterly record in Q4, with Q1 production of ~165,900 ounces at all-in sustaining costs [AISC] of $964/oz. The mine processed ~2.27 million tonnes of ore in the period at an average grade of 2.47 grams per tonne of gold, and while the growth was significant, the mine was up against easy comps with lower throughput and much lower grades in Q1 2022 during a period of higher waste stripping as B2Gold worked to develop Phase 6 of the Fekola Pit.

B2Gold - Quarterly Production (Ex-Calibre), Fekola Production, All-in Sustaining Costs (Company Filings, Author's Chart)

{kind=link}

While all-in sustaining costs may have come in higher than some hoped at Fekola in Q1 given the strong production results, it's worth noting that this is a very capital-intensive year at Fekola with sustaining capital expected to come in above $210 million. And while the mine benefited from lower than budgeted diesel costs in Q1 and much higher volumes, sustaining capital doubled year-over-year to ~$51.5 million (Q1 2022: $25.5 million), affecting AISC in the period. I expect these higher costs to persist throughout the year given the significant capitalized stripping (Phase 7 Pit pushback at Fekola), but we should see a lower cost profile in 2024 for this world-class asset.

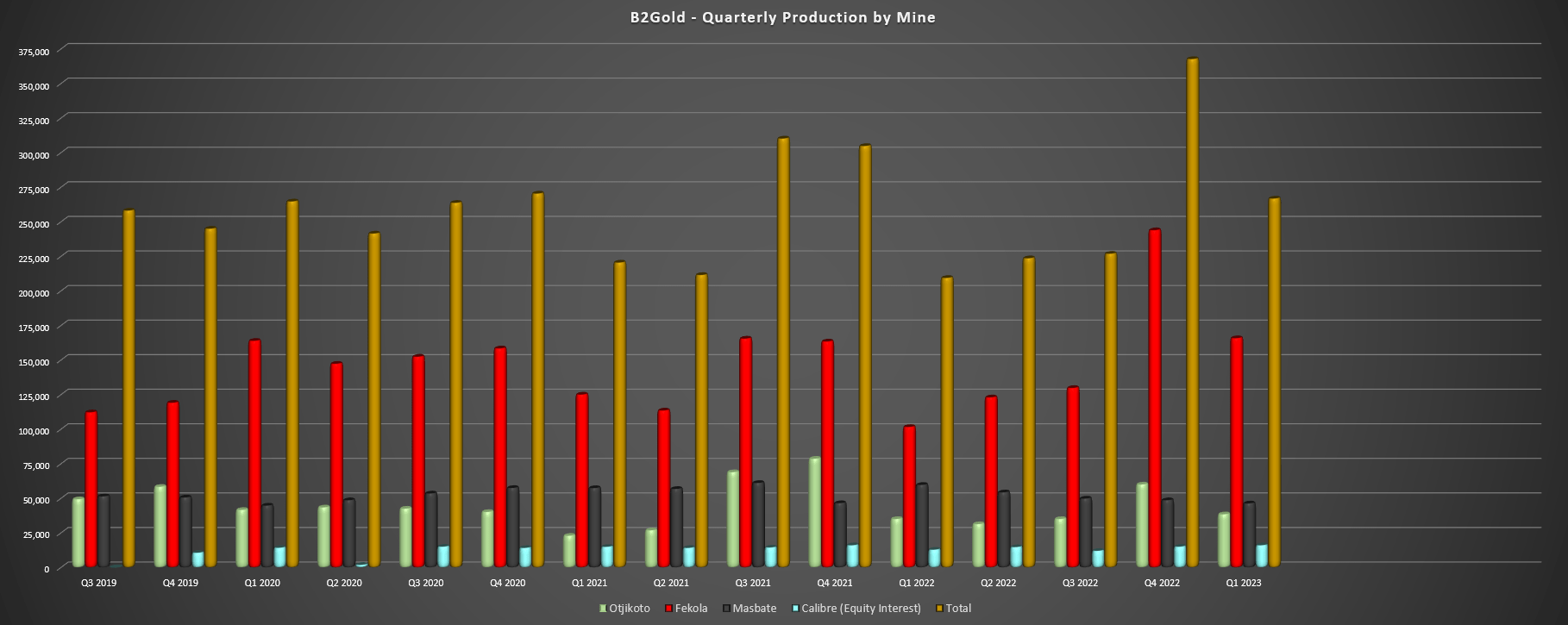

B2Gold - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

Looking out across the rest of the portfolio, Otjikoto saw an increase in production, with 38,500 ounces produced at all-in sustaining costs of $905/oz. The increase in production was driven by higher grades and recoveries, with the asset benefiting from higher-grade ore from WSUG which began production in Q4 and averaged over 1,000 tonnes per day of contribution in Q1. At Masbate, output fell sharply year-over-year to ~46,400 ounces (Q1 2022: ~59,800 ounces) due to lower grades and recoveries. This was not surprising, given that Q1 2022 was a massive quarter, with its best quarterly production in years. As for costs, they increased materially to $1,320/oz, related to much higher sustaining capital and lower sales volumes.

B2Gold - Quarterly Revenue (Company Filings, Author's Chart)

{kind=link}

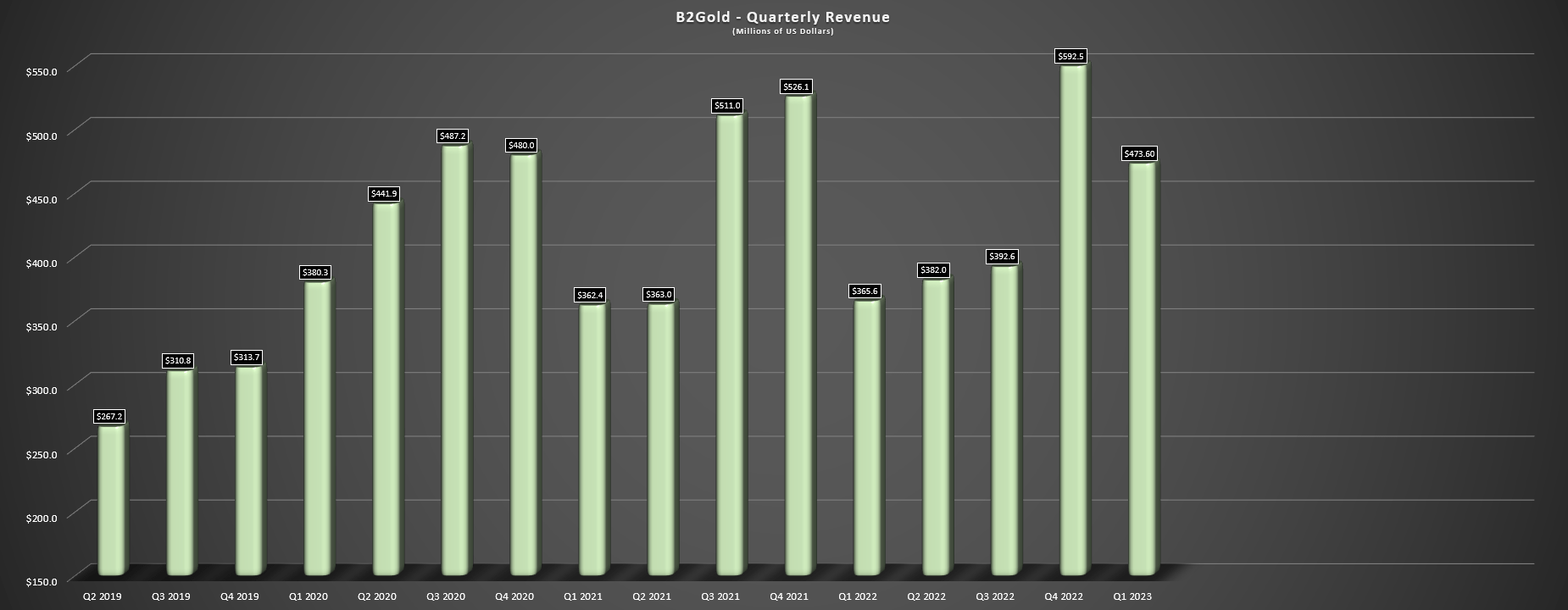

Finally, if we look at revenue, B2Gold's sales increased 29% year-over-year to $473.6 million, benefiting from higher gold sales and a higher average realized gold price of $1,901/oz (Q1 2022: $1,874/oz). Meanwhile, operating cash flow came in at $203.8 million, a 90% increase from the year-ago period. This was related to increased sales volume and improved margins, and the company finished the quarter with ~$670 million in cash, giving it a strong balance to support Goose Project construction (Sabina acquisition) and its plans for a stand-alone oxide mill at Anaconda north of Fekola which would likely be constructed in H2-2025 if green-lighted, shortly after Goose construction is complete.

Costs & Margins

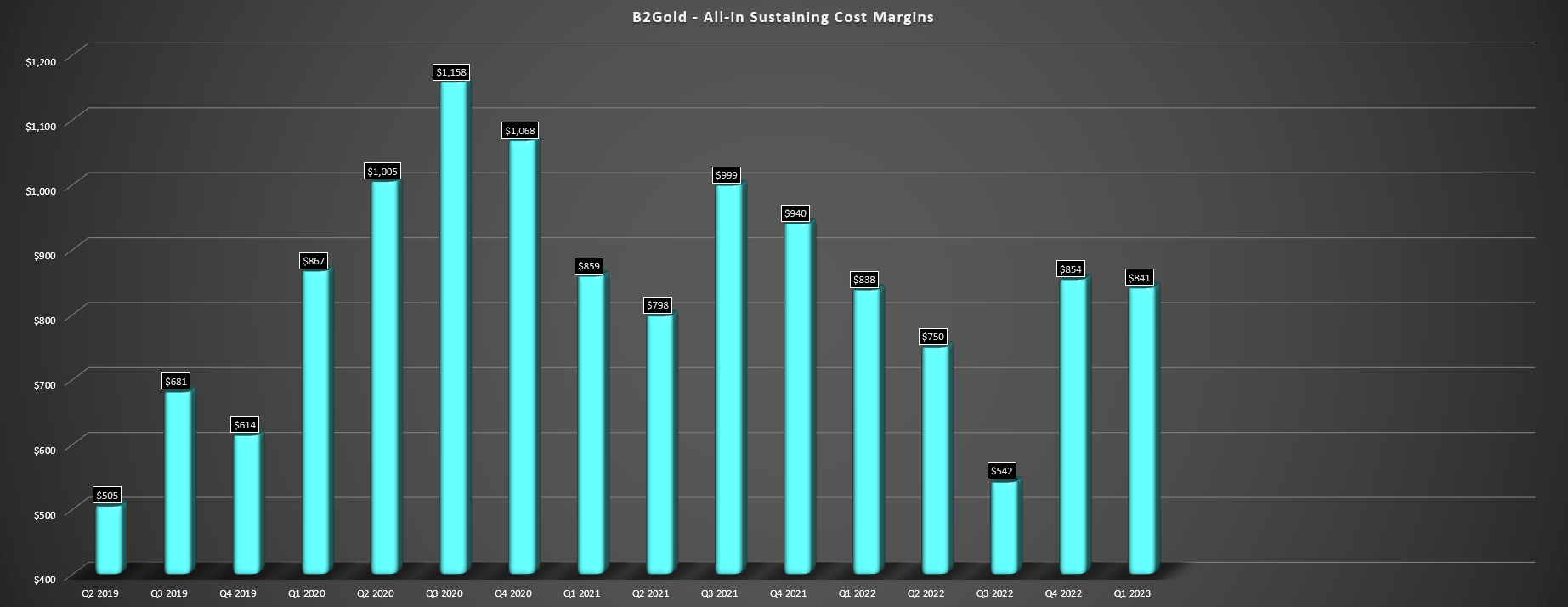

Moving over to costs and margins, B2Gold saw a meaningful improvement in costs, benefiting from higher sales volumes which offset the significantly higher sustaining capital expenditures in the period from a ~$180 million capitalized stripping program across its operating portfolio. During Q1, all-in sustaining costs came in at $964/oz (Q1 2022: $987/oz), and are tracking below the guidance midpoint of $1,195/oz to $1,255/oz. Given that production is tracking slightly ahead of budget and sustaining capital is slightly behind budget, I still expect AISC to come in at or above $1,200/oz for the year, but we could see a beat if fuel prices remain favorable. Plus, any margin compression from temporarily higher costs is being offset by the gold price increase.

B2Gold - AISC Margins (Company Filings, Author's Chart)

{kind=link}

As shown in the chart above, B2Gold's AISC margins improved to $841/oz in Q1 2023, up marginally year-over-year despite the higher sustaining capital expenditures and impact of inflationary pressures on some consumables since Q1 2022. And while I didn't expect to see any margin expansion this year under a more conservative gold price outlook, the company has a better chance of holding the line or even seeing improving margins if the gold price can remain above $1,950/oz. Plus, it's important to note that any margin compression is temporary if it occurs, with significantly lower capitalized stripping in 2024 likely to translate to sub $1,100/oz costs in FY2024.

Recent Developments

Finally, if we look at recent developments, B2Gold noted it will benefit from high-grade saprolite material being trucked south to Fekola from Bantako starting in Q3 2023, with ~18,000 ounces of contribution this year, but up to 80,000 ounces longer-term. In addition, the company continues to drill aggressively at Anaconda, plans to release a resource estimate by mid-year and a study related to a 4.0 million tonne per annum stand-alone mill and oxide processing facilities at Anaconda that could come into production by 2027. When combined with the potential to head underground at Fekola, investors can remain optimistic that this asset could grow to 800,000+ ounces per annum, offsetting declining production from Otjikoto later this decade.

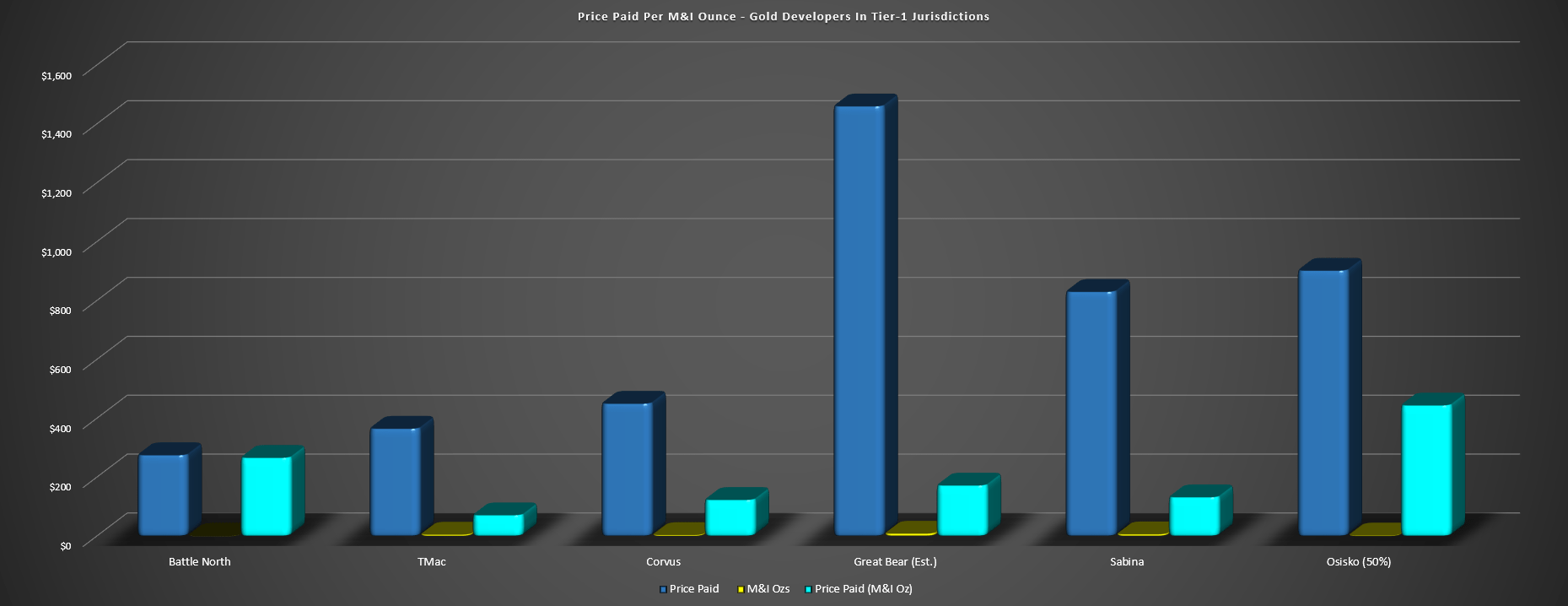

Meanwhile, in Nunavut, B2Gold closed its acquisition of Sabina Gold in April, at a cost of just ~20% share dilution or ~216 million shares. B2Gold noted that it has a $20 million budget at Back River for 2023 for near-mine exploration and testing regional targets like George, Boulder, Boot, and Del, and it also repurchased the gold metal offtake agreement for $62 million from Orion Mine Finance and one-third of the gold stream with Wheaton Precious Metals ( WPM ) for $46 million, increasing its exposure to the asset. As we can see in the above chart, B2Gold paid a very reasonable price for Sabina with a cost per M&I ounce of $132/oz (~$113/oz on total ounces), below the 3-year average of ~$215/oz for ounces in Tier-1 jurisdictions.

Price Paid Per M&I Ounce - Tier-1 Jurisdiction Gold Projects (Company Filings, Author's Chart)

{kind=link}

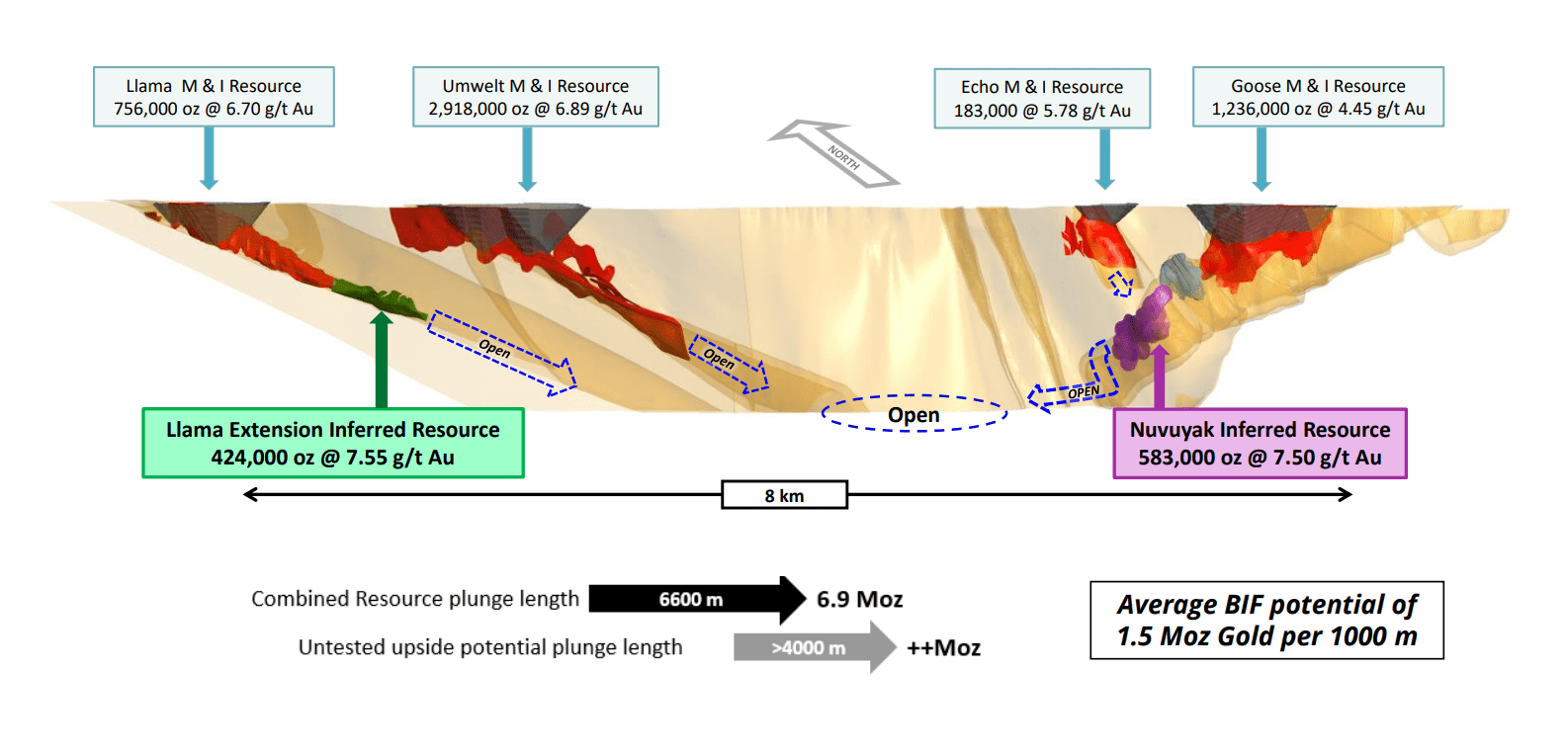

Plus, while this was well below the average, this is an asset which could ultimately prove up over 9.0 million ounces in the measured and indicated categories long term, given that it's a ~58,000-hectare land package that's already home to ~6.3 million M&I ounces, but with limited regional drilling to date. In fact, the George deposit 50 kilometers to the northwest has an iron formation that's 2.5x the size of Goose's iron formation, and Goose is permitted for 6,000 tonnes per day with a planned production rate of 4,000 tonnes per day. This means that B2Gold could ultimately look at leveraging off existing infrastructure at Goose to process additional material either from new discoveries at Goose or satellite opportunities like George.

Exploration Upside at Goose (Sabina Presentation)

{kind=link}

In addition, there appears to be meaningful exploration upside at Goose, with a significant resource base outside of its reserves (~3.6 million ounces of gold), discoveries made over the past few years at Hook and Wing, and its high-grade underground deposits being open at depth (Umwelt, Llama Extension, Nuvuyak). Highlight intercepts drilled at Umwelt include 20.35 grams at 12.64 grams per tonne of gold, 31.9 meters at 13.68 grams per tonne of gold, 32.80 meters at 10.85 grams per tonne of gold, and 15.10 meters at 21.87 grams per tonne of gold. These intercepts are all in the V2 high-grade corridor just beneath the Umwelt Pit, suggesting the potential to bring higher-grade ounces into the mine plan.

Umwelt Drilling (Sabina Presentation)

{kind=link}

As it stands, the project is expected to produce over 280,000 ounces per annum in its first five years at sub $750/oz costs, but B2Gold appears confident that it may be able to increase production to closer to 300,000 ounces per annum. While this would generate additional free cash flow, with this expected to be a cash cow over its first five years and one of the lowest-cost mines globally, I think it's the long-term potential that is the most exciting, with this being an 80-kilometer gold belt that could ultimately support two mines feeding a single processing facility. Assuming a throughput rate closer to 6,000 tonnes per day, this asset has the potential for 400,000 ounces per annum once optimized.

Valuation & Technical Picture

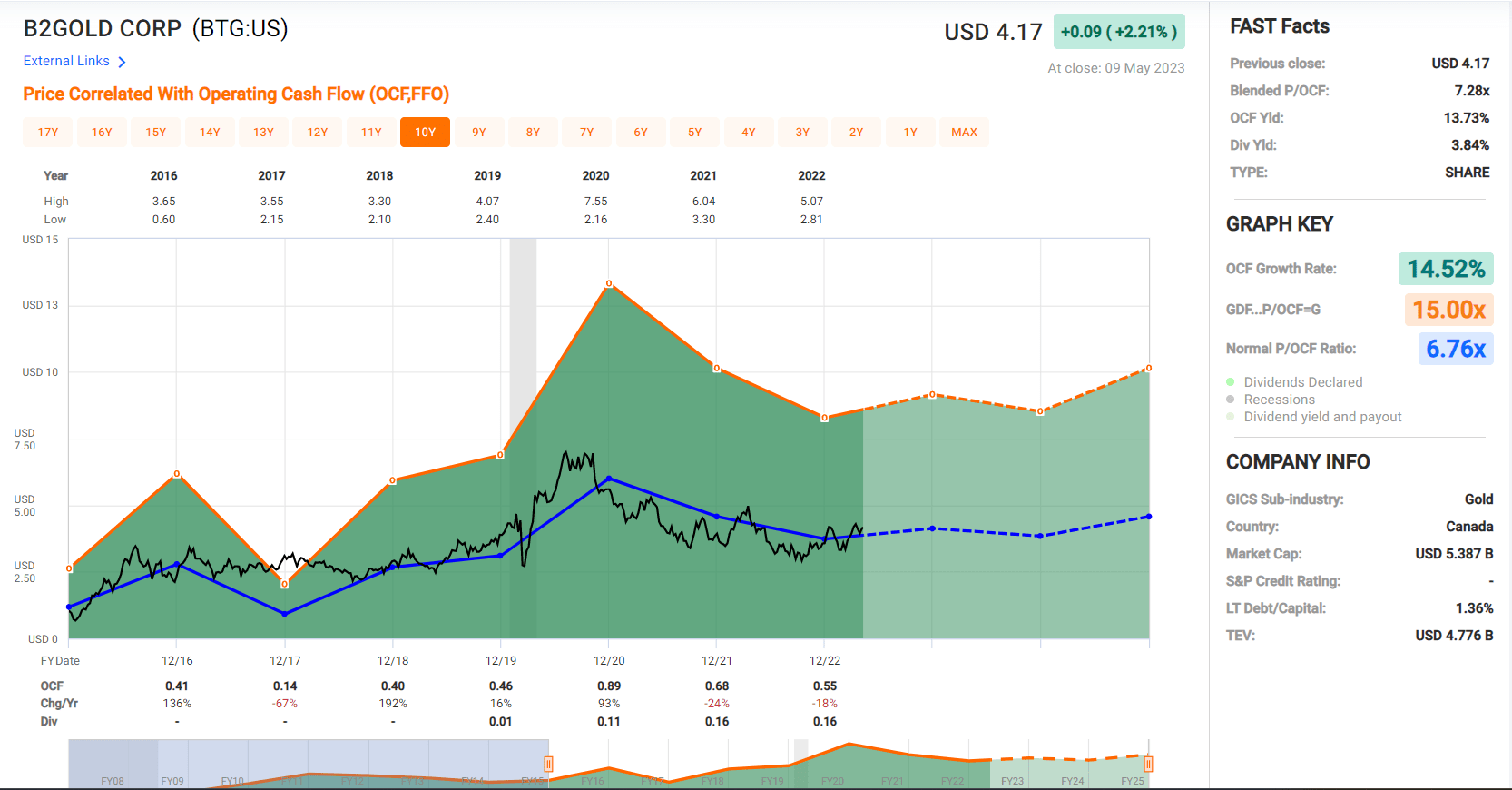

Based on ~1.33 billion fully diluted shares and a share price of US$4.20, B2Gold trades at a market cap of ~$5.58 billion and an enterprise value of ~$4.91 billion. This has left B2Gold trading at a premium to its estimated net asset value of ~$4.90 billion, which isn't unreasonable given that the company has upgraded its reserves and jurisdictional profile with its recent acquisition of Sabina and continues to see material exploration success in Mali. Meanwhile, from a cash flow standpoint, B2Gold is back to trading roughly in line with its historical average, currently sitting at ~6.6x FY2023 cash flow per share estimates ($0.64) vs. a historical multiple of ~6.7x cash flow.

B2Gold - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

Given B2Gold's added diversification, margin benefit from Sabina, and lower-risk jurisdictional profile (given that over 20% of annual production post-2025 will come from a Tier-1 ranked jurisdiction post-2025), I believe B2Gold can easily command a premium to its historical cash flow multiple, with a fair multiple being 8.25x cash flow. Using this multiple and FY2023 cash flow per share estimates of $0.64, I see a fair value for the stock of US$5.30. This points to a 26% upside from current levels, or a ~30% upside from a total return basis when including the company's industry-leading dividend.

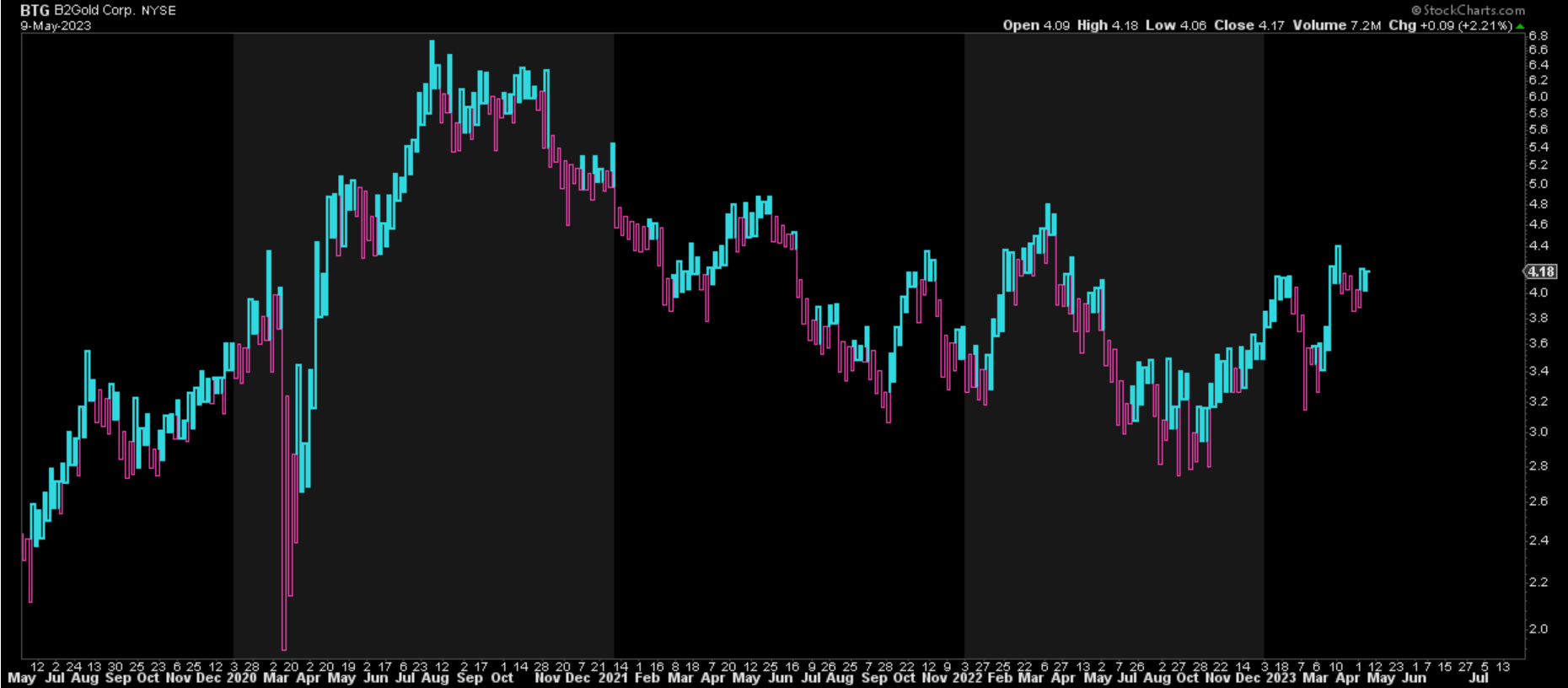

While this fair value estimate points to a meaningful upside, I prefer a minimum 35% discount to fair value in place to justify starting new positions in mid-cap producers to ensure an adequate margin of safety. If we apply this discount to BTG, its ideal buy zone would come in below US$3.45 per share. Obviously, there's no guarantee that the stock will pull back to this level, but this is where the stock would become more interesting from an investment standpoint. Meanwhile, from a technical standpoint, the reward/risk is less favorable than it was coming into 2023, with the stock trading in the upper portion of its range. So, while I see BTG as one of the better-run producers sector-wide, I don't see this as a low-risk buying opportunity.

BTG 4-Year Chart (StockCharts.com)

{kind=link}

Summary

B2Gold put together a solid Q1 report and is tracking well against its FY2023 guidance and the gold price has certainly helped, allowing the company to evade material margin compression in this capex-heavy year. Meanwhile, its development pipeline has never looked better with two significant projects in the pipeline (Goose in construction, Anaconda stand-alone being studied), and continued drilling success in Finland. Overall, I believe B2Gold's bold move to acquire Sabina has upgraded the investment thesis and also provided a solid boost to reserves in an attractive jurisdiction. Given its position as one of the better-run producers, I would view sharp pullbacks as buying opportunities.

For further details see:

B2Gold: Tracking Well Against FY2023 Guidance