PLTR - Back To The Future 4.0 - Reviewing Our Calls For Q2

2023-07-12 14:31:05 ET

Summary

- We end each quarter by reviewing our work within the semi and software/hardware spaces, analyzing our best calls and where we could’ve done better.

- This quarter was exceptional; we launched our Investing Group, Nvidia Corporation triggered the A.I. rally carrying Advanced Micro Devices, Inc., Marvell Technology, Inc., Broadcom Inc., and others higher on A.I. fumes.

- The market is in a deadlock, with the Fed expecting interest rates to move higher.

- We operate in a forward-looking market and hence lay out our predictions of what 2H23 will bring, what names to look out for, and which to look into.

The S&P 500 reached 14-month highs this quarter, and the Direxion Daily Semiconductor Bull 3X Shares ETF ( SOXL ) hit 12-month highs of over $24 per share. The second quarter kicked off with markets still recovering from the regional bank crisis after the failures of Silicon Valley Bank (SIVBQ) and Signature Bank (SBNY) in March. Investors shifted focus to better-than-feared earnings for the quarter, with Nvidia Corporation ( NVDA ) taking central stage as it guided revenues 50% above consensus for the next quarter - safe to say, we've never seen such a revision for a mega-cap company.

A.I. became the next greatest thing for investors to chase, and the A.I. rally pushed several names higher on expectations of higher A.I. revenues. Our concern for the next quarter is investor confidence in the A.I. rally as being the Hail Mary out of the post-pandemic slump; looking ahead, we think that the next wave of earrings will see higher A.I. revenues but lower revenues in other segments that could drag markets down.

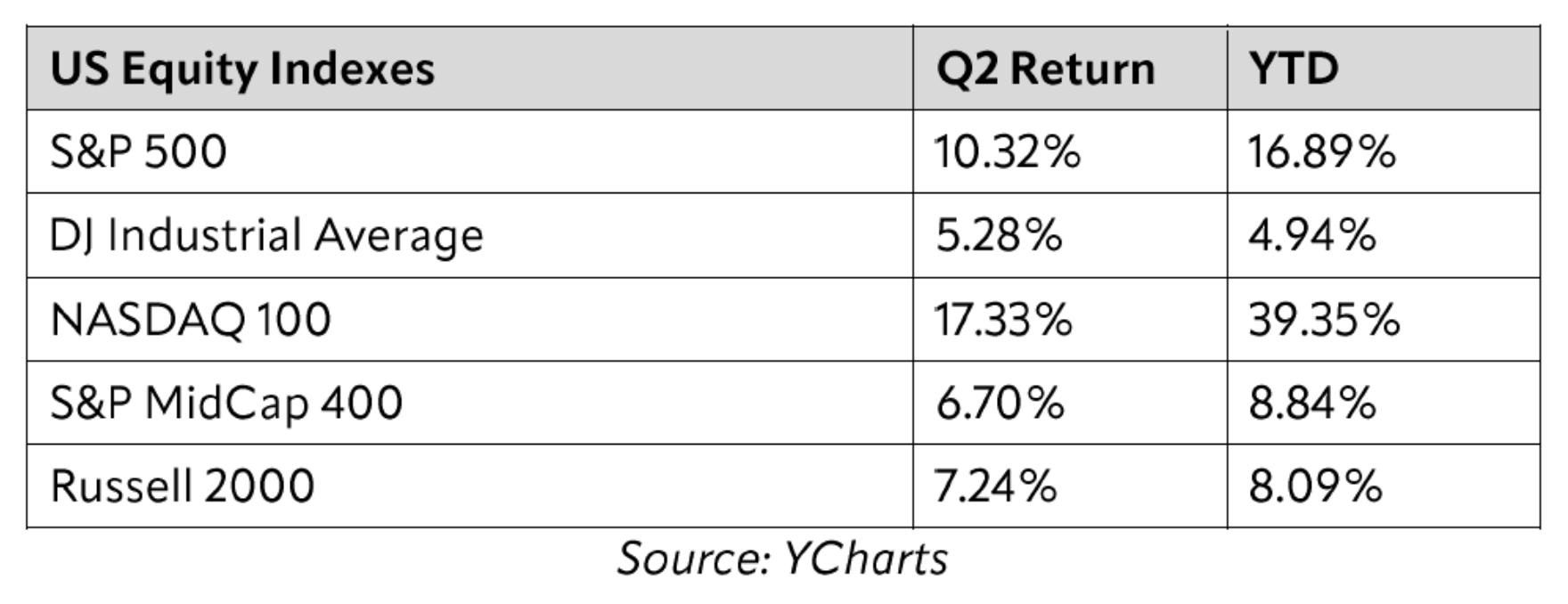

The following chart outlines U.S. Equity Indexes as of the end of Q2.

{kind=link}

Special Takeaways From 2Q23

This past quarter, we saw retail investor trading of semis reach all-time highs driven by the A.I. boom; the A.I. frenzy is not surprising, but the fact that Advanced Micro Devices, Inc. (AMD), Marvell Technology, Inc. (MRVL), Broadcom Inc. (AVGO), among other names, rode the bullish sentiment higher despite less than great A.I. exposure and with fundamental headwinds in their core businesses is concerning. We're seeing a trend of stock rallies not driven by fundamentals, that impacted our coverage portfolio to some extent; the market, in turn, is not only driven by real-growth recovery, but also by expectations of it.

Another notable takeaway this quarter is the intensifying chip wars between the U.S. and China. Last week, The Wall Street Journal reported the U.S. is considering tightening export control rules to limit China's access to A.I. chips. Matters began to heat up last October when the Biden administration issued a set of regulations around the export of semiconductors to China in an attempt to halt the county's technological advancements. The most recent developments of potential U.S. export controls on A.I. chips to China will negatively impact the semi-industry, namely NVDA, MRVL, AVGO, and AMD.

Our main concern is for the A.I. leader, NVDA, as the controls can impact up to 20-25% of the company's data center sales, specifically, the sale of A800 & H800. NVDA warned that the U.S. restrictions would result in a "permanent loss of opportunities" for the U.S. industry. Still, the company stated on a call that if adopted, the controls will not have an immediate material impact on financial results due to the strength of demand for NVDA products amid the A.I. boom, but may have a longer-term effect if indeed assumed.

The CAC (Cyberspace Administration of China) retaliated with an investigation into Micron Technology, Inc. ( MU ) that determined that the company failed its cybersecurity review as it was founded to pose significant security risks to China's critical information infrastructure supply chain. From the company's 8k filling, we expect the CAC ban will impact up to 50% of China-based sales, which accounts for 25% of total sales. This will likely be a continued headwind for the company slowing its recovery. Still, we maintain our buy rating on MU for the longer term investor as we expect memory demand and pricing to improve into 2024 after inventory correction cycles have been completed.

Best Calls - Review & Preview

While A.I. is an exciting dose of bullish sentiment in an otherwise worsening macro backdrop, the boom is not all rainbows and butterflies. Some of our best calls this quarter have resulted from filtering through market noise around promises of A.I. growth exposure rather than feeding into it.

1. NVDA & AMD

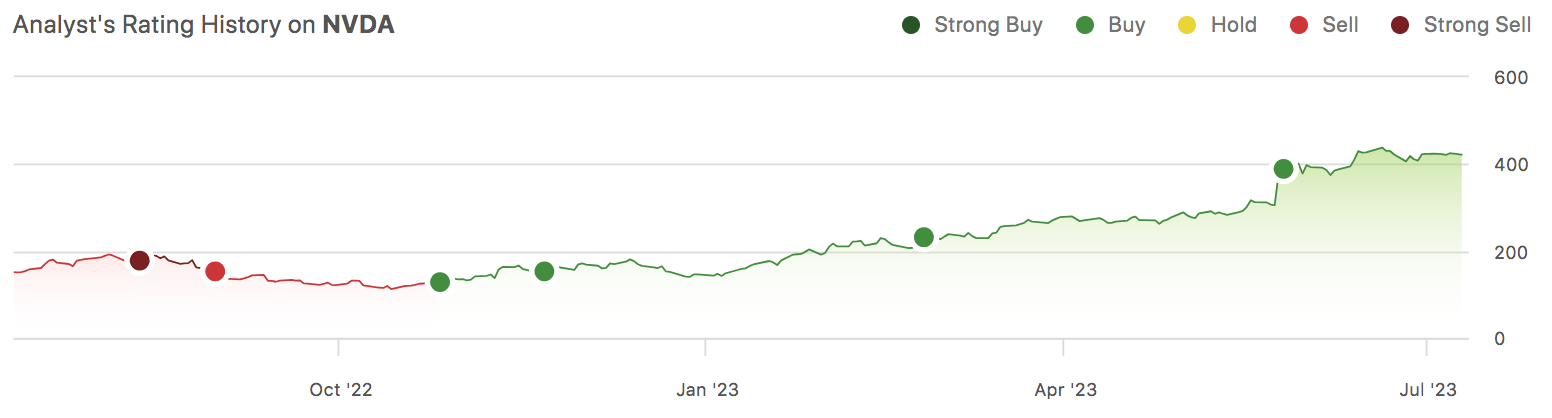

NVDA has been among our favorite semi-names; we upgraded the stock back in late October since the stock is up 227%, outperforming the S&P 500 by around 212%. YTD, the stock is up 195%. NVDA's valuation expanded significantly as the company is on track to reach a market cap of 2T by 2030. We don't think the stock is overvalued only because the company is the winner of the design cycle for 2023 and 1H24. The following chart outlines our rating history on NVDA.

{kind=link}

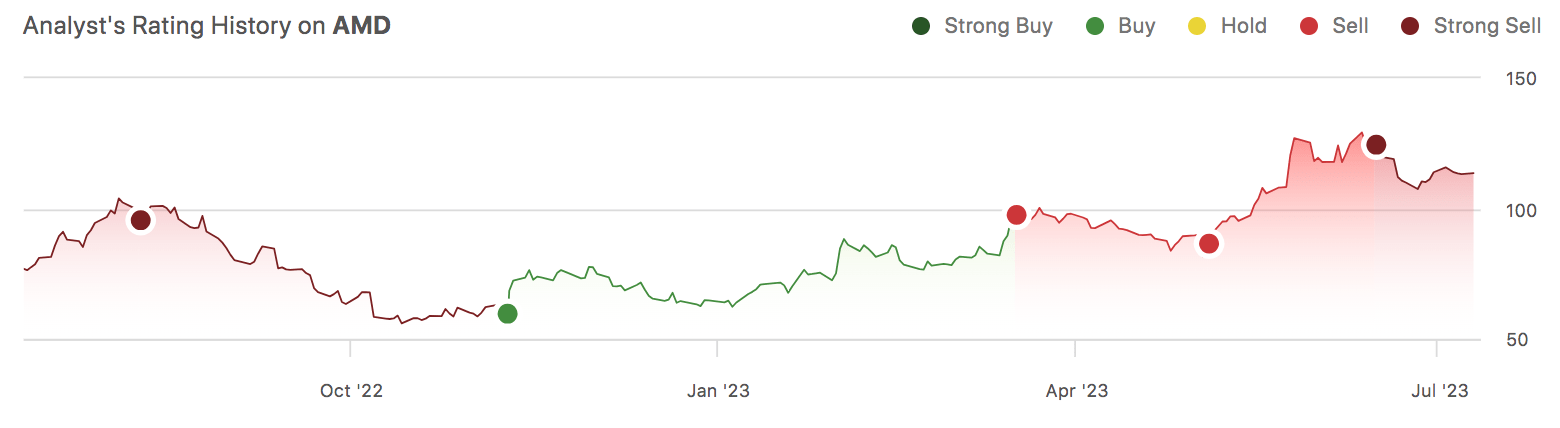

AMD remains a distant second in the A.I. race despite investor confidence in CEO Lisa Su and the upcoming MI300 series announced in the company's Data Center and A.I. Technology presentation. To contrast the two, AMD experienced a rally on A.I. hype, but the rally failed to hold as the company was late to the design cycle. We were early in our downgrade of AMD, but not wrong. This quarter, we predicted the company's outperformance would moderate due to share loss to Intel ( INTC ) in PC and Data Center markets and, more recently, failure to compete meaningfully with NVDA in 2H23 for surging demand for A.I. servers.

We received a lot of backlash for our sell rating on AMD; however, the stock is coming down since our latest note in mid-June, down 9%, underperforming the S&P 500 (SP500) by a little over 8%. The following graph outlines our rating history on AMD.

{kind=link}

Looking ahead, we expect NVDA demand tailwinds to stretch for three more quarters; hence, despite the higher valuation, we would urge investors to look into entry points into the stock on pullbacks. The recent Wall Street Journal report that the U.S. is considering further regulations around A.I. chips export to China caused NVDA to drop, providing opportunities to pile up. Regarding AMD, we expect the company to continue to see lower highs into Q3 as we expect earnings to be lackluster, given the exaggerated expectation of A.I. growth exposure.

2. PLTR

We've been bullish on Palantir Technologies Inc. ( PLTR ) since the company was trading at around $9 per share in 2020; the stock is up an impressive 77% over the past five years, up 155% YTD, and up 94% since we started publishing on the stock in February. PLTR's rival C3.ai, Inc. ( AI ) also rallied on A.I. sentiment by around 265%, but PLTR remains the better pick in the business of data analytics and A.I., in our opinion. The following chart outlines PLTR, AI, and the S&P 500 stock performance YTD.

YCharts

3. META

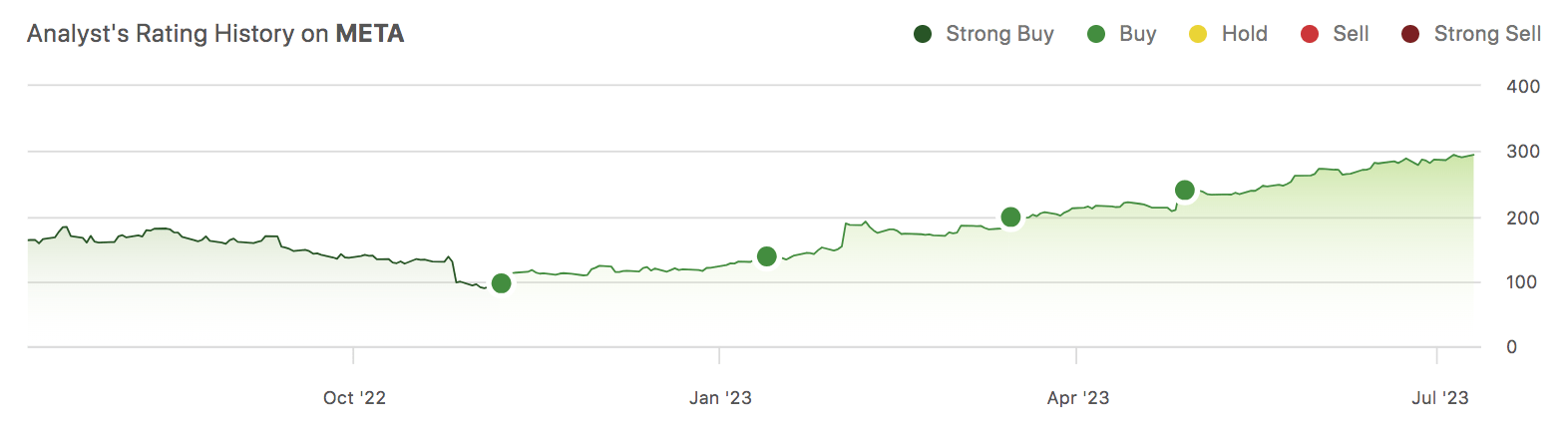

Meta Platforms, Inc. ( META ) got a bad rep after the overspending issue in the Reality Labs last year; Meta dropped roughly 59% in 2022, and now the company is making a steady recovery reeling in spending. YTD, the stock is up 136%, and since our buy-rating in early November, the stock is up 204%, outperforming the S&P 500 by around 188%. META is also largely undervalued, trading below the peer group on the P/E ratio and EV/Sales. The following chart outlines our rating history on META.

{kind=link}

Meta introduced Thread, a new app built by the Instagram team that is more or less Twitter; the app allows users to share text updates of up to 500 characters, including photos, links, and videos up to 5-minutes in length, and join in on public conversations. Thread became the fastest downloaded app in history, racking up to 100M users since its launch debut last week, beating OpenAI's ChatGPT sign-up of 100M monthly users in two months; the genius of the app, in our opinion, is that as part of Meta's FoA, it leverages Instagram users and allows Thread users to track those they follow on Instagram creating an Instagram-based Twitter. It's still to be determined if users will use Thread on a long-term basis, but the signups are a notable accomplishment.

Our bullish sentiment on Meta is the company's increased focus on profitability and cost reductions in CEO Mark Zuckerberg's "year of efficiency"; if Thread successfully cements itself as the new Twitter, the company is looking at 2018-2019 Twitter-like profitability. We expect Meta to continue outperforming in 2H23 and beat consensus next quarter.

Timing Is Everything; Where We Could've Gone Better

We've had a cluster of software/hardware names that rallied on an A.I. frenzy and the expectation of recovery rather than fundamentals that's negatively impacted our calls on Microsoft Corporation ( MSFT ) and Amazon.com, Inc. (AMZN). The following chart outlines MSFT, AMZN, and the S&P 500 stock performance YTD.

YCharts

MSFT skyrocketed with the launch of ChatGPT on its early investment in OpenAI in 2019 and its further multi-year, multi-billion dollar investment this year. Our bearish sentiment on MSFT was based on our belief the company’s A.I. growth exposure would not be able to offset the weaker macro environment, and earnings confirmed our concerns, as did the recent announcement that the company would cut more jobs after the start of FY24 on top of the previous 10,000 job cuts. We’re exploring favorable entry points to upgrade MSFT into 2024, but believe the stock is currently overvalued.

We maintain our bearish sentiment on AMZN, as we expect the company to see headwinds in 2H23 due to softer cloud/enterprise spending pressuring AMZN’s AWS growth engine. The stock is up 51% YTD; AMZN stock prices are hard to justify at current levels. Also, AMZN Prime Day begins this week, which historically boosts the stock, but it remains unclear if that’ll be the case this year. We believe AMZN's YTD rally might not have legs to support it. We expect inflationary pressures and higher interest rates will weigh on consumer spending, slowing top-line growth in product sales. We continue to recommend investors explore exit points at current What's.

What’s Next In 3Q23?

We see a more volatile 2H23 as the market is stuck in a deadlock between narratives of a bull market and an upcoming correction. We see softer cloud/enterprise spending unfolding in 2H23 and continue to see Y/Y TAM contraction for PCs, smartphones, and servers. We think the real recovery won’t materialize until 2024, but are seeing signs of memory market recovery and PC inventory correction cycles wrapping up.

We believe this quarter, A.I. promises made last quarter will be under investor scrutiny to detect if companies riding the A.I. sentiment will pull through on meaningful profits. We don’t think the bull market has begun, with the Fed warning of higher interest rates and softer cloud/enterprise spending. The market is attempting to wait out the worsening macro backdrop; the bar for earnings is already low, which might help companies beat consensus, but we don’t think it will save the stocks from confronting their A.I. promises and macro headwinds.

For further details see:

Back To The Future 4.0 - Reviewing Our Calls For Q2