SAN - Banco Santander: Another Steady Quarter; Shares Still Attractive

2023-10-26 01:35:26 ET

Summary

- Banco Santander has performed well since my first piece on the bank last year, though as expected it has lagged select peers with greater capital returns potential.

- Q3 was another steady quarter for the bank. The business model here is designed to smooth out long-term earnings volatility, and that was on show last quarter.

- These shares remain cheap below tangible book value, with a decent 10% shareholder yield at the prevailing share price.

Covering Spanish multinational banking giant Banco Santander ( SAN ) early last year, I argued that while the shares were cheap, they may underperform European peers with better capital returns potential like ING (NYSE: ING ) and BBVA (NYSE: BBVA ). That call has worked out nicely, with SAN materially trailing both those tickers albeit still returning a decent 25% in that time (for a roughly 16% CAGR).

Santander's geographical diversity has resulted in lower earnings volatility in the past, but it is a sword that can cut both ways. In times of supportive macro environments for bank profits, more concentrated peers can outperform in terms of earnings. ING, for example, saw an 80% rise in net income between 2Q2022 and 2Q2023, while Santander only saw a circa 14% increase over the same period. On the flip side, the idea is that Santander's profits can hold up better during downturns.

With the above in mind, some of the bank's European peers have already released Q3 results that show modest sequential declines in profit. To be clear, earnings are still very good, but it looks like they may have peaked. Santander, on the other hand, still managed to grow its earnings in Q3. Moreover, the stock still trades at a discount to tangible book value – less so than when I covered it last time, but still a meaningful discount. These shares remain attractively valued based on the bank's ROTE outlook and capital returns potential.

Q3: Another Steady Quarter

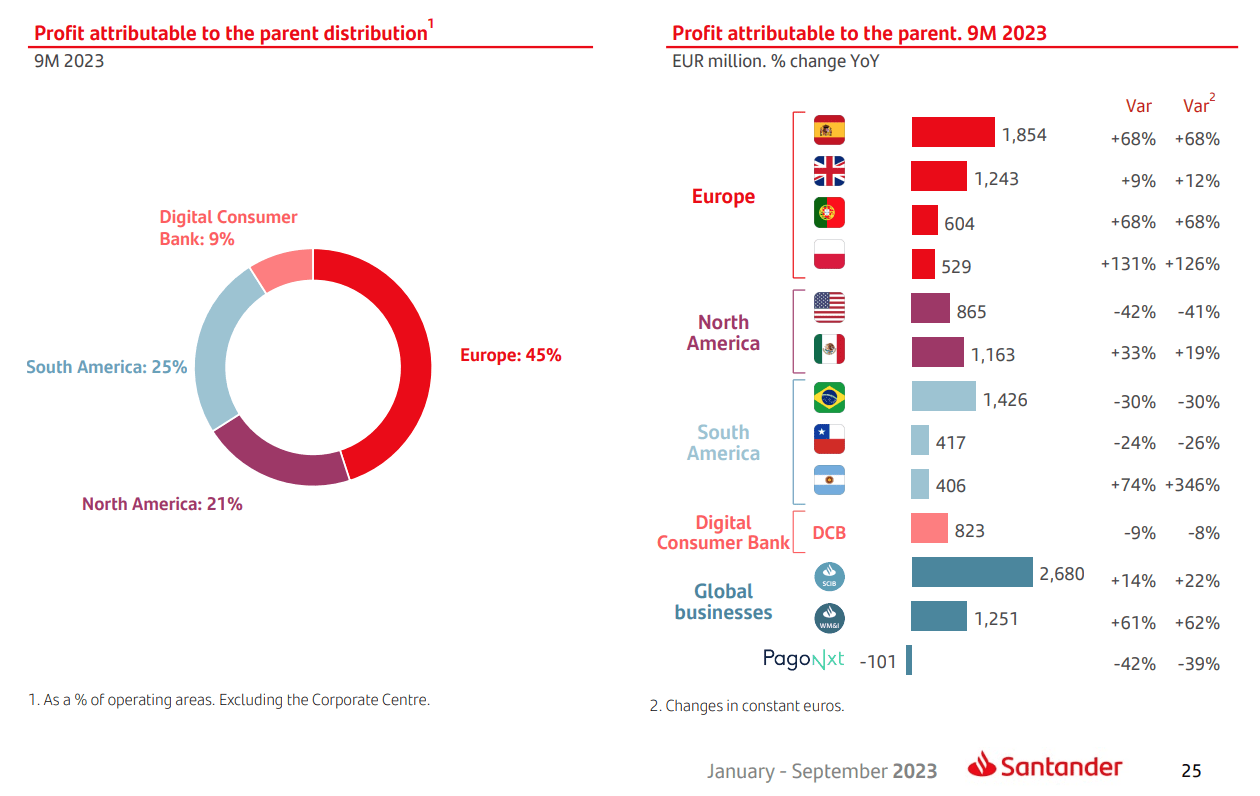

Santander is such a vast business that it is hard to cover it within a circa 1,000 word limit. A key point to appreciate is its geographic split, with Latin America (38% of 9M'23 attributable profit, including Mexico) and Europe, including the auto lending-focused Digital Consumer Bank (54%), its main earnings contributors. It also operates in the US (~9% of 9M'23 attributable profit) with a big skew to consumer auto lending (around 40% of its US loan book).

Source: Banco Santander Q3 Results Release

{kind=link}

As I alluded to above, Santander's markets are often at different points in their respective cycles. Q3 results demonstrate this nicely. Brazil, for instance, was quicker than the U.S. and Europe to increase interest rates in response to the inflation generated by the fiscal and monetary response to COVID. While many US and European banks are still waiting for asset quality to deteriorate and earnings to meaningfully fall, Brazilian banks have already been there for a few quarters. As a result, Santander's YTD earnings are down around 30% in Brazil year-on-year, with ROTE falling to 13.7%.

On the flip side, check out Spain. For years Santander's business there would have been suffering due to the extremely low interest rate environment in the Eurozone. Now that rates have risen sharply, it is reaping the benefits. Deposit beta there was still only around 20% cycle-to-date. It earned a circa 15% ROTE in Spain on a 70% year-on-year increase in 9M'23 earnings.

When viewed holistically, Q3 was another steady quarter for Santander. Pre-provision earnings increased by around 5% sequentially (Fig 1), enough to offset an increase in provision expenses. Profit before tax and net income (Fig 2) were up 5% and 9%, respectively, quarter-on-quarter. ROTE overall was 15%. I think that will prove to be a good performance relative to peers once they have all reported, though the context is that many of its peers had faster growth in the preceding periods. Because of its geographic spread, Santander has been less spectacular while still growing profits overall.

Fig 1. (Data Source: Banco Santander Quarterly Results) Fig 2. (Data Source: Banco Santander Quarterly Results)

Balance Sheet Not A Major Concern

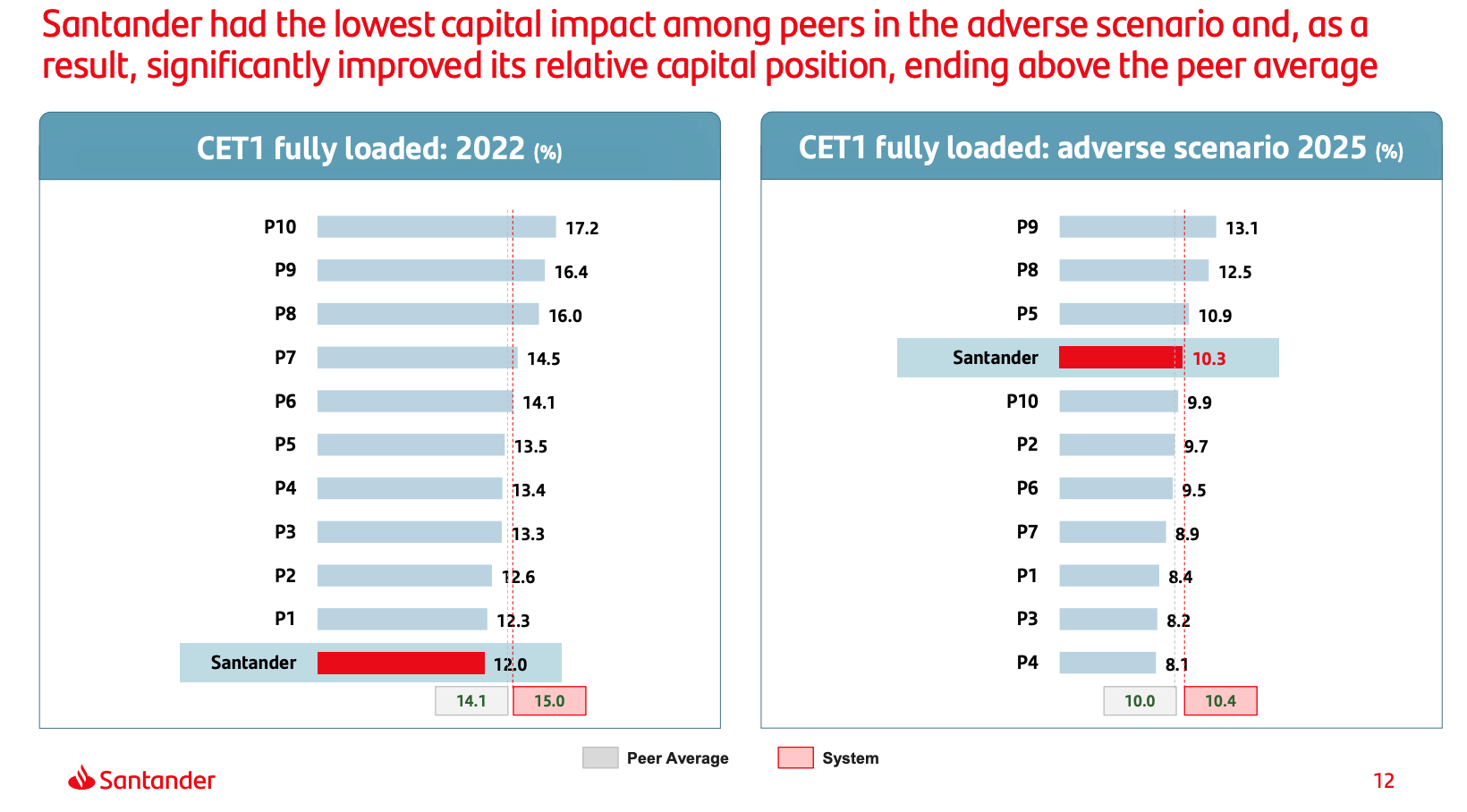

There is another aspect to Santander's earnings profile to consider. Compared to peers, its CET1 ratio has typically been on the low side (12.3% in Q3). This is something that has popped up in the comments section of previous articles on Seeking Alpha as a concern. In fact, Santander lands right at the bottom on that metric compared to its self-selected peer group (Fig 3).

Fig 3. (Source: Banco Santander 1H23 Results Presentation)

{kind=link}

This also needs to be put into the context of its business exposure and historical earnings volatility (at the top-end of its peer group assuming lower is better). For example, in the recent ECB stress test Santander would see a circa 200bps decline in its CET1 ratio under an adverse scenario, and that would pull it back up towards its peer group average.

Valuation Remains More Than Reasonable

Santander shares trade for €3.45 per share at time of writing in Madrid trading ($3.60 for ADSs on the NYSE), putting them at around 0.75x Q3'23 TBVPS (€4.61/share). Multiple expansion was a plank of my Buy rating last time out, but there has only been a modest re-rating in that time (SAN was on a 0.65x TBVPS multiple back then).

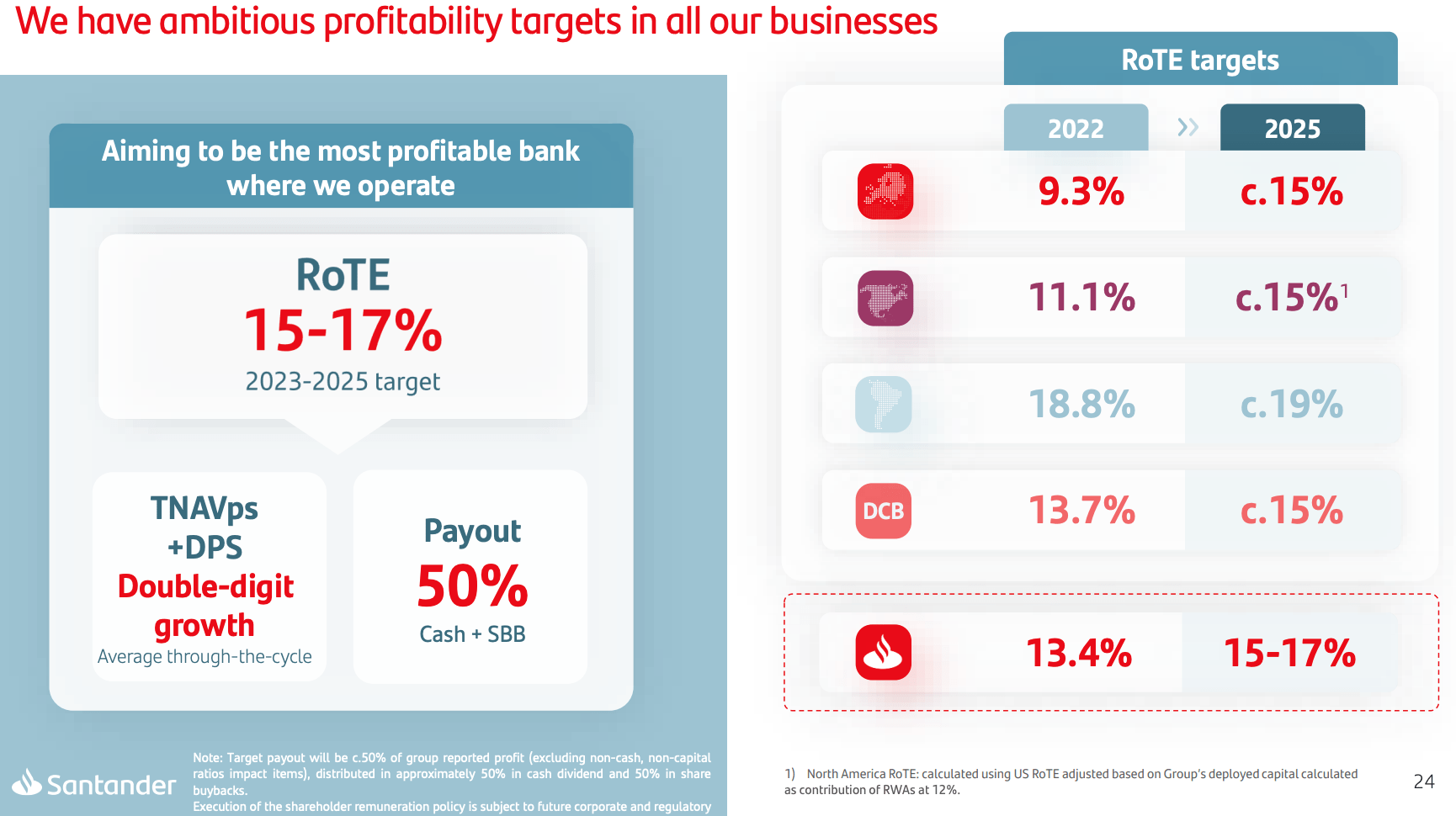

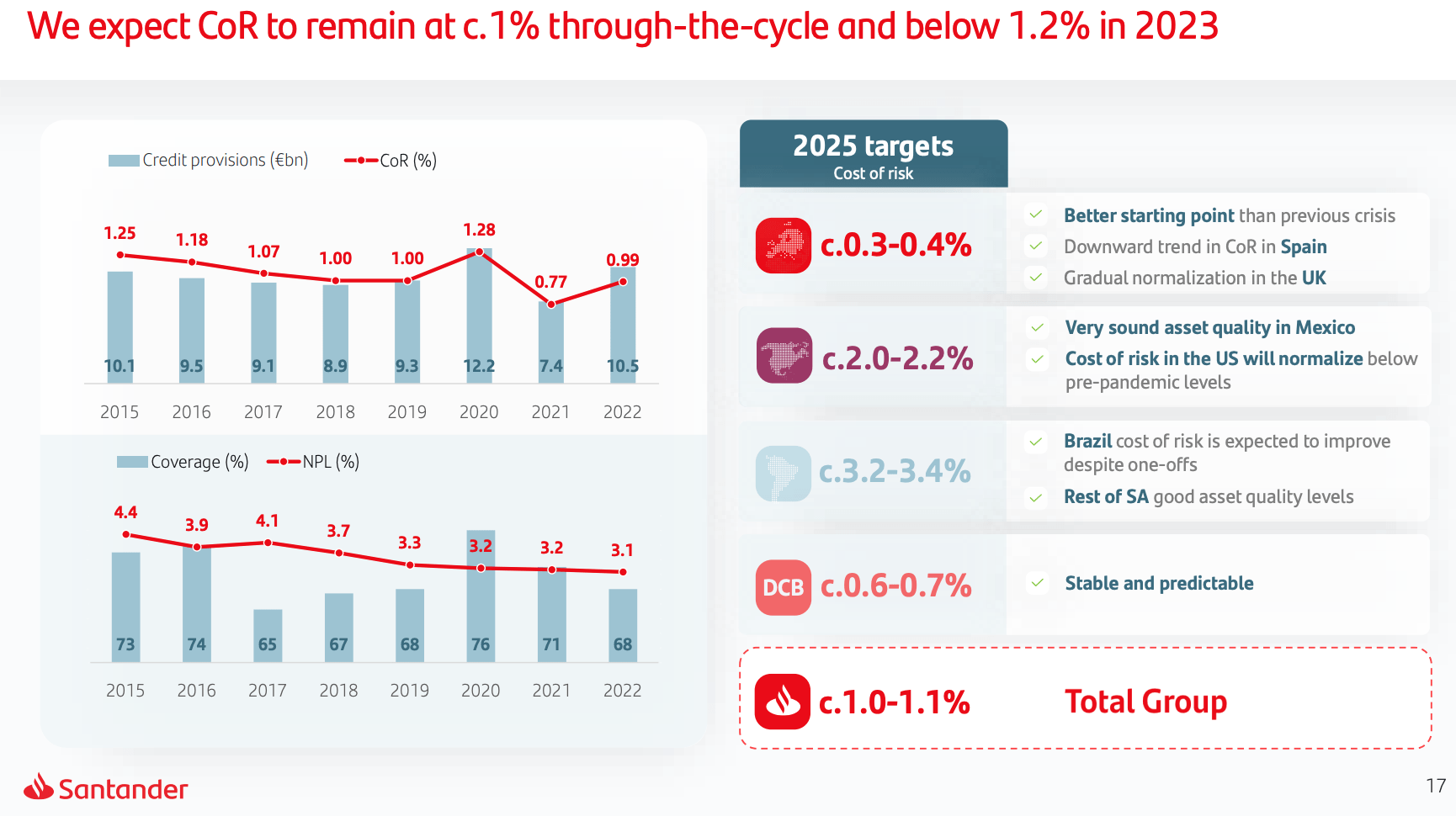

The current multiple still looks too cheap to me. The bank has generated a 14.8% ROTE YTD through Q3. It targets a 15-17% ROTE in the medium-term (Fig 4). Provisioning expenses are about in line with its medium-term target right now (cost of risk was 1.13% in Q3 versus a 1%-1.1% 2025 target)(Fig 5). Even if we prudently build in some margin of safety, I think Santander will be good for a double-digit ROTE through-the-cycle. Below 1x TBVPS therefore looks good value to me.

Fig 4. (Source: Banco Santander Q3 Results Release) Fig 5. (Source: Banco Santander Q3 Results Release)

{kind=link}

{kind=link}

Many European banks are in the same boat. They still trade below TBVPS despite posting good double-digit ROTE right now. Why? Well, many of them are over-earning currently, with higher funding costs, low earning asset growth and credit quality all becoming stronger headwinds going forward. Still, there is more to it than that. My guess is that the market thinks the current interest environment is an aberration and that we will see a return to the pre-2022 situation in Europe. That is to say, ultra-low interest rates and associated single-digit ROTEs. Santander would be less exposed if that does indeed turn out to be the case.

The final point I would make concerns the bank's capital returns policy. Last time out, Santander targeted a 40% payout ratio of net income (split 50/50 between dividends and buybacks). That has since been upped to 50% with the same 50/50 split between dividends and buybacks. Based on a mid-teens ROTE and 0.75x multiple of TBVS, that means a 10% shareholder yield. You can again build in a margin of safety and still come out quite nicely here, with forward returns potential remaining attractive.

For further details see:

Banco Santander: Another Steady Quarter; Shares Still Attractive