SAN - Banco Santander (Brasil) Q3: The Worst Is Behind But Still Pricey

2023-10-27 09:26:07 ET

Summary

- Santander Brasil's Q3 results showed notable improvements in asset quality, credit origination, and a gradual focus on enhancing profitability.

- Despite the positive trends, the bank's ROE of 13.1% remains weaker than historical performance and that of some competitors.

- The credit portfolio exhibited modest growth, with a specific focus on less risky segments, leading to a controlled net interest margin.

- Although the bank's dividend payout remains strong, an overvaluation of approximately 18% relative to the current share price indicates a cautious stance for now.

The investment thesis for Banco Santander (Brasil) ( BSBR ) has predominantly focused on concerns regarding loan defaults and credit availability, significantly impacting the broader Brazilian banking sector and negatively affecting the bank's efficiency and profitability in recent quarters.

However, there have been some positive developments in the thesis following Santander Brasil's Q3 results. These results showed notable improvements in asset quality, credit origination, and a gradual profitability enhancement.

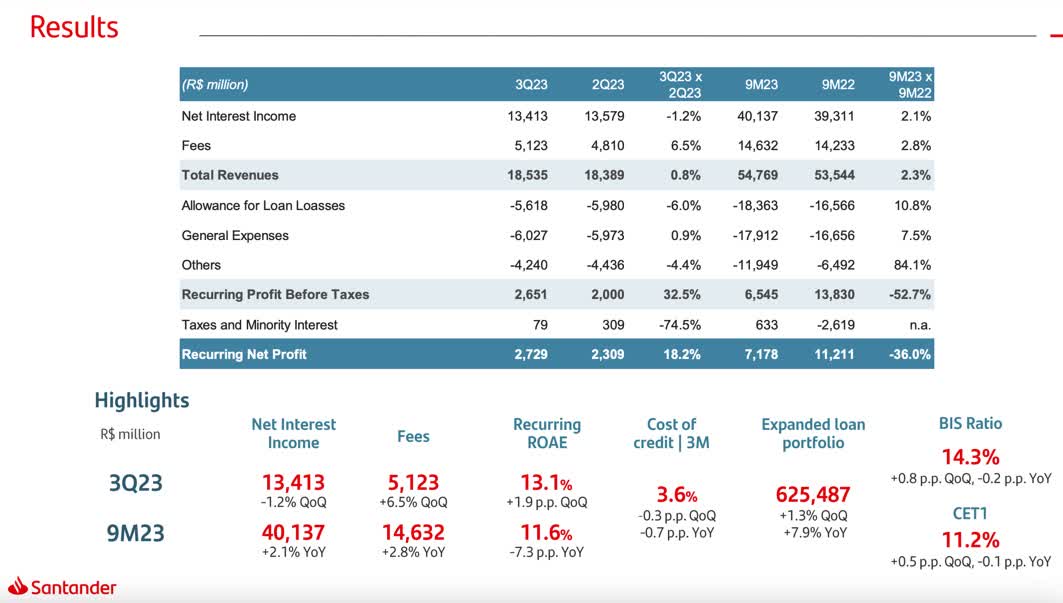

The Brazilian subsidiary of the Spanish Banco Santander ( SAN ) reported a net profit of R$2.7 billion, marking a substantial quarterly improvement of 18.2%. Nevertheless, its profitability, as measured by the Return on Equity ((ROE)), currently stands at 13.1%, which is lower than the bank's historical performance and lags behind some of its competitors.

{kind=link}

In a previous article about the bank about at the beginning of the month, I provided an overview of the main events in Q2, I noted that despite the observable improvements, I had reservations about Santander Brasil's valuation. It traded at a premium compared to its Brazilian peers, even with a lower ROE and no discernible competitive advantage.

Nonetheless, Banco Santander (Brasil) is still a great income stock. It has a track record of higher payouts than its peers and presents better earnings prospects for the next few quarters, translating into a more robust yield.

While my outlook for the bank has improved considerably after the third quarter of 2023, I still believe other domestic peers, such as Itaú Unibanco ( ITUB ) and Banco do Brasil ( BDORY ), have more attractive valuations and more robust ROE. Therefore, I maintain a neutral stance on Santander Brasil.

Credit Portfolio: Quality Over Quantity

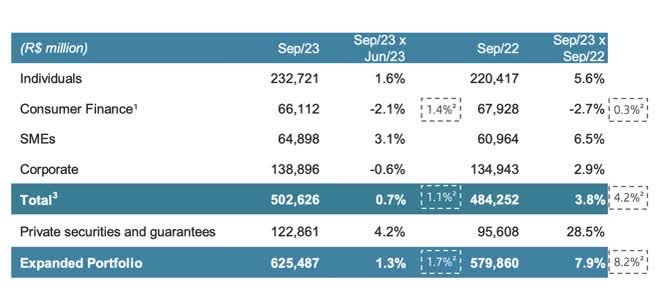

Santander Brasil's credit portfolio in Q3 2023 stood at R$502.8 billion, reflecting modest growth of just 0.7% quarter-over-quarter and 3.8% year-over-year. Excluding the exchange rate effect, the quarterly growth would have been merely 0.2%, with a 4.4% increase yearly.

{kind=link}

In the quarter, the positive highlights include the individual segment, which grew by 1.6% and 5.6%, and small and medium-sized companies, which rose 3.1% and 6.5% in the year. On the negative side, the consumer financing line contracted by 2.1% in the quarter and 2.7% in the year, primarily due to the sale of the stake in Banco PSA.

Santander Brasil's credit portfolio for large companies has contracted for the second consecutive quarter. Between July and September this year, the figure for the large corporate segment was R$138.9 billion, representing a 0.6% decline compared to the second quarter. At the end of April, the volume was R$141.66 billion, marking a 6.7% increase from the end of last year.

This reduction can be attributed to two factors: the recovery of the capital market and the bank's more excellent selectivity, indicating a strategy less focused on the number of clients and more concentrated on maximizing return on equity ((ROE)).

NII has Exhibited a Lower Spread, While Service Income has Shown Expansion

The bank's interest income decreased by 1.2% compared to the previous quarter but increased by 6.5% compared to last year.

Santander Brasil's IR

The margin with clients (NII Clients) declined by 1.3% quarter-over-quarter, influenced by a more selective approach that resulted in a more conservative mix, causing the spread to drop below the levels seen in the second quarter of 2023 (-0.2pp).

Conversely, the margin with the market (NII Markets) remained relatively stable compared to the second quarter of 2023, with a year-over-year improvement of 1.8%. Treasury results negatively impacted this stability despite Brazil's interest rate decrease (Selic).

As a result, as the appetite for products with higher margins rebounds and market margins gradually improve due to the expected interest rate reduction in the coming quarters, there is a tendency for NII to grow again in 2024.

Service income demonstrated significant expansion, with a 6.5% increase quarter-over-quarter and an 8.2% rise year-over-year. This growth in the quarter can be attributed to increased revenues from insurance of 19% year-over-year, credit operations climbing 10.8% year-over-year, and cards 3.2% year-over-year.

Delinquency: The Worst Is Over

After 18 months of deteriorating asset quality, the bank has finally witnessed a drop in delinquency in the quarterly comparison. This positive trend has contributed to reduced expenses related to provisions against defaults. Delinquency over 90 days (NPL 90+) decreased by 0.3 percentage points quarter-over-quarter and remained stable year-over-year at 3.0%.

Santander Brasil's IR

This quarter it marked a significant improvement in the individual segment, which decreased by 0.6 percentage points quarter-over-quarter. There was also a slight moderation of 0.1 percentage point quarter-over-quarter in large companies and small and medium-sized enterprises. This marks the first notable improvement in delinquency rates in this credit cycle since the third quarter of 2020.

Additionally, the new vintages that originated in January 2022 continue to exhibit better quality, with an NPL 90+ rate of 2.9%, 0.3 percentage points lower than the older vintages.

Credit Provision Expenses: First Annual Drop

Net provision expenses ((PDD)) amounted to R$5.6 billion, marking a significant annual decrease of 6% year-over-year and 9.5% quarter-over-quarter. This marks the first yearly drop and could signify a turning point. The positive performance in the quarter was partially attributed to the strengthening of the balance sheet in the first quarter of 2023 and the improved results of the new portfolios.

Santander Brasil's IR

Additionally, the bank divested R$2.3 billion from its portfolio, with R$2.2 billion already off-balance sheet (written off) and only R$0.1 billion remaining active. This divestiture resulted in a gain of approximately R$14 million.

With provision levels surpassing defaults, the coverage ratio now stands at 229.5%, demonstrating an increase of 15.8 percentage points quarter-over-quarter and 3.8 percentage points year-over-year. This indicates that Santander Brasil is in a robust financial position.

Decent Dividends Expected, Yet Overvaluation Persists

Considering its policy of generously distributing dividends to its shareholders as part of its commitment to returning profits to its Spanish controlling shareholders, Banco Santander Brasil has historically maintained a payout ratio ranging from approximately 40% to 50%. During the earnings call, CFO Gustavo Viviani mentioned that they are still evaluating potential changes to the company's payout policies. However, the current projection suggests a payout of 80% for this year.

Banco Santander Brasil's payout (orange line), net profit (green line), and dividends (blue line). (Status Invest)

{kind=link}

Considering the consensus estimates, which in this case are based on one analyst's perspective, it is projected that Santander Brasil will likely see a 26% decline in its Earnings Per Share ((EPS)) in 2023. This would equate to a net profit of roughly $1.99 billion. Personally, I find this estimate to be rather conservative, yet still prudent, given the company's recent performance.

A notably high payout ratio of 80% and dividing this by the bank's 7.46 million outstanding shares would imply a dividend of $0.21 per share. This corresponds to a yield of 4%, which contrasts with the consensus expectations of a yield of 5.5% for this year.

{kind=link}

Given the current share price of $5.37 per share and establishing a conservative ROI (Return on Investment) of 5%, the target price for Santander Brasil's shares would be $4.29. This indicates an overvaluation of 25% relative to the current price.

Company's data, compiled by the author

The Bottom Line

In summary, Santander Brasil's quarter was marked by a customer and product mix shift. The Brazilian arm of Banco Santander is focusing its credit concessions on less risky lines and customers with a better risk profile, resulting in lower net interest margins.

During this quarter, we observed a decrease in defaults to 3% (over 90 days), a positive development. I believe the peak in delinquency is now behind us, and it should gradually return to historical levels over the next few quarters.

Despite improvements in certain areas, Santander Brazil's profitability ((ROE)) is just 13.1%, weaker than the bank's historical performance and some competitors. CEO Mario Leão has indicated that the bank is working towards a recovery in profitability, targeting an ROE range of 15-20%. He believes the worst part of the economic cycle is now in the past.

With the improvement in credit quality, I believe the bank may resume more consistent growth in 2024, and Q3 could mark a turning point in this regard.

However, despite the signs of improvement, I reiterate my neutral recommendation for the bank. I see a fair price for Santander Brasil at $4.52 per share. I might consider adopting a more bullish stance if the share price corrects to this level.

For further details see:

Banco Santander (Brasil) Q3: The Worst Is Behind, But Still Pricey