SAN - Banco Santander: Collateral Damage While Shareholder Payouts Should Increase In 2023

2023-03-14 08:05:22 ET

Summary

- Banco Santander is a Spanish bank but it generates most of its income outside of Spain.

- About 15-20% of the annual net income is generated in the United States.

- The Bank focuses on car loans in the USA. That's not risk-free but at least it is not exposed to the valuation swings in the securities available for sale segment.

- The bank confirmed at a recent Investor Day it will increase the shareholder payout ratio from 40% to 50%.

Introduction

Although Santander ( SAN ) is a Spanish bank, it generates most of its earnings outside of Spain and I consider this financial powerhouse to be an excellent way to gain exposure to South American economies as well as the Mexican economy.

But as Santander is active all over the world, it also means it is also exposed to ‘sector phenomena’ like what we saw in the US market the past few trading days. In this article I will dig a bit deeper into Santander’s exposure to the current issues in the US banking sector.

Looking back at the 2022 results

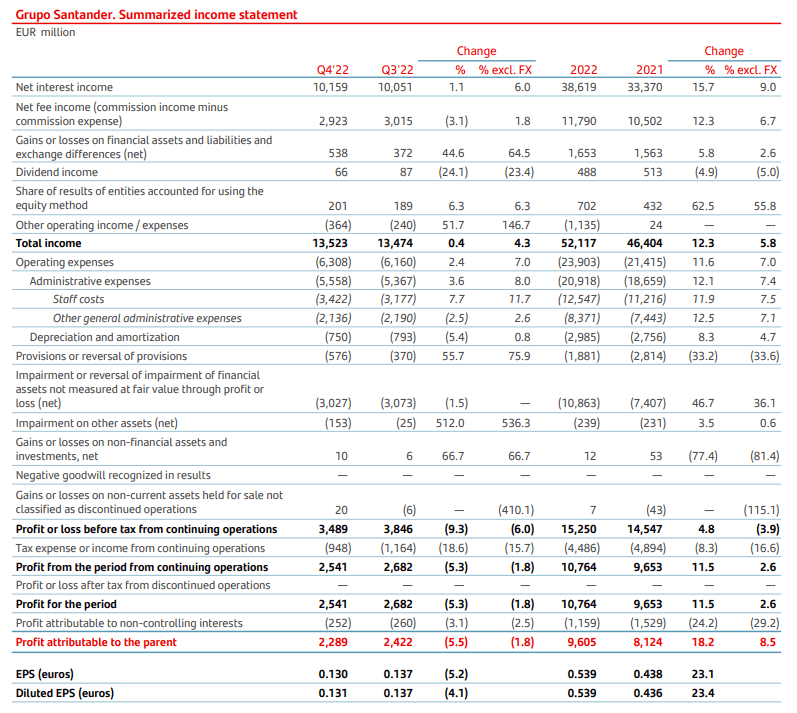

First of all, let’s have a look at the Q4 results, and by extension, Santander’s full-year financial results for 2022.

We see the net interest income increased by approximately 1.1% to 10.16B EUR on a QoQ basis, including the (negative) impact from currency fluctuations. Excluding the impact from those currency fluctuations, the net interest income would have increased by approximately 6%.

{kind=link}

The bank did notice a decrease in the net fee income but posted a higher gain on financial assets which helped to compensate for the lower dividend income and the higher other operating expenses. The total ‘income’ in the fourth quarter increased by 0.4% to 13.5B EUR but unfortunately the operating expenses increased at a relatively fast pace with a 2.4% increase. That was mainly due to higher admin expenses, partially offset by lower depreciation and amortization expenses.

The total amount of impairment charges increased as well, and that’s the main reason why Santander’s pre-tax income fell by in excess of 9% to just under 3.5B EUR. The reported net income was 2.54B EUR of which just over 250M EUR was attributable to non-controlling interests resulting in a net income of approximately 2.29B EUR attributable to the shareholders of Banco Santander. This represented an EPS of 0.13 EUR. Lower than in the third quarter, but FY 2022 was still a success as the full-year EPS came in just under 54 cents compared to the 43.8 cents generated and reported in 2021.

The bank uses a 40% payout ratio for its shareholder distributions which is split evenly between a dividend and a share buyback. The total attributable net income in FY 2022 was 9.605B EUR which means the bank will spend almost 2B EUR on a dividend and the same amount on a share repurchase. Santander already paid an interim dividend of 5.83 cents per share and announced a final dividend of 5.95 cents for a total dividend of 11.78 cents per share (subject to the standard Spanish dividend withholding tax rate of 19%). The 2B EUR earmarked for share repurchases will help to boost the per-share results (and thus the dividend) further down the road.

And during its capital markets day at the end of February, Santander confirmed it will increase its payout ratio from 40% to 50%, again evenly distributed among a dividend and a share repurchase program.

Santander also sounded pretty upbeat for the next few years as the bank is now targeting a Return On Tangible Equity of 15-17% in the 2022-2025 era while maintaining a CET1 ratio of in excess of 12%. The tangible book value per share was 4.26 EUR as of the end of 2022 which means that a 15% ROTE implies an EPS of in excess of 60 cents per share so that’s quite an aggressive target from Santander, knowing the ROTE was less than 13.4% in 2022 and less than 12% in 2021. The momentum is there, but it will be interesting to see if the bank can indeed meet its own 15% ROTE threshold. If Santander is successful, its cash dividend should increase to in excess of 16 cents per share (including the recently announced payout ratio increase to 50%).

Santander appears to be ‘collateral damage’

So why did Santander’s share price move down over the past few trading days? It’s clear the market is taking a step back from all US-based financial institutions until the dust settles. Most of the major financial institutions in Canada have seen their share prices recover, but smaller regional banks are still feeling the pain. Additionally, Monday was a weak day for European banks in general, so Santander was hit twice: it moved down along with other European banks while its US division will be under additional scrutiny from US investors.

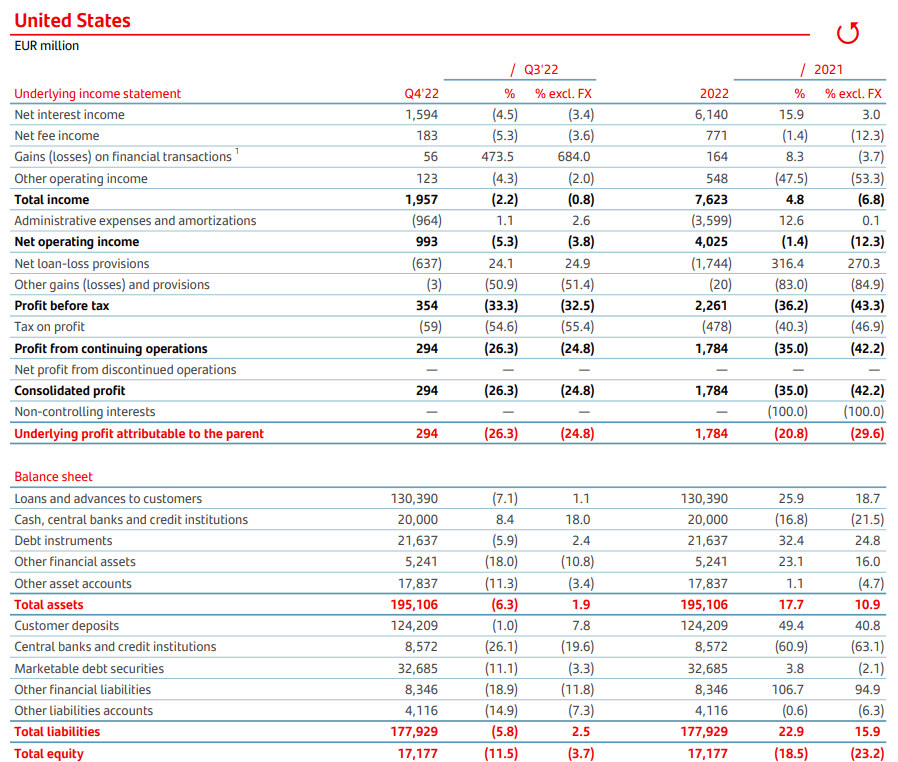

Unfortunately even the annual report does not contain a detailed breakdown of the assets in the US subsidiary so we’ll have to work with the condensed financial statements.

We know the US subsidiary contributed about 294M EUR to the Q4 net income and just under 1.8B EUR to the full-year net income. That’s just over 20% of the consolidated net income.

{kind=link}

But what’s really important is that the 195.1B EUR balance sheet is mainly focusing on consumer loans and cash held at central banks and credit institutions. This means that the total exposure to securities available for sale should be relatively limited (there are 21.6B EUR in debt instruments on the balance sheet which likely consists of a combination of securities AFS and securities held to maturity).

And with about 17.2B EUR in equity, the balance sheet of the US subsidiary actually looks pretty decent. Even if the bank would have to take a haircut on debt securities, the existing equity value should cover that potential loss. So in a normal market, I don’t expect Santander’s US division to run into any problems. The majority of the balance sheet consists of loans which are not subject to mark-to-market requirements.

Investment thesis

It looks like Banco Santander’s share price got caught in the crossfire and Santander may be just ‘collateral damage’. The consolidated financial statements of the bank look fine and the US subsidiary looks well-capitalized with relatively few loans and investments that have to be marked to market and could cause potential issues.

SAN stock is still up about 20% since my most recent article was published about three months ago, and I am definitely keeping my position for now.

For further details see:

Banco Santander: Collateral Damage While Shareholder Payouts Should Increase In 2023