SAN - Banco Santander: Poised To Outperform - Here Is Why

2023-08-07 00:14:54 ET

Summary

- Santander has performed well with a 7-8% RoR since February, just below the S&P Global average.

- The company's 1H23 results show strong performance with a 12% increase in revenues and a 14% YoY increase in profit.

- SAN stock is undervalued with a P/E ratio of 6x and has the potential for significant upside in the future.

Dear readers/followers,

I've been a vocal proponent of some financial investments for a long time. One of those investments has been Banco Santander, S.A. ( SAN ). While I've not yet seen the company "pop" as an investment, I expect this to do so going forward. The company has performed pretty well - a 7-8% RoR since my last article back in February, which is just below the S&P Global average in the same timeframe.

The company is not the most stable or fundamentally safe financial investment out there. That's why my position is smaller compared to my overall investments in other banks and investments. There's no doubt that Banco Santander isn't as safe as, say, Allianz (ALIZY) or other European Financial institutions, but this does not equate to this bank not being investable.

My thesis and my position for the company are in relation to this - and now we'll look at the most recent numbers and forecasts.

Santander - An update going into 2H23

Many investors make the mistake of equating the risk of southern-European finance and banking institutions with how they were, say during the GFC. That is an erroneous assumption. The fiscal and regulatory safety of these banks has vastly improved over the past 10 years - the same as with most banks outside of these areas.

It's understandable to see some hesitation here when going into a company like Santander. A lot of history, a lot of negative history indeed, is still part of the equation. But forward risk does not equate to historical risk.

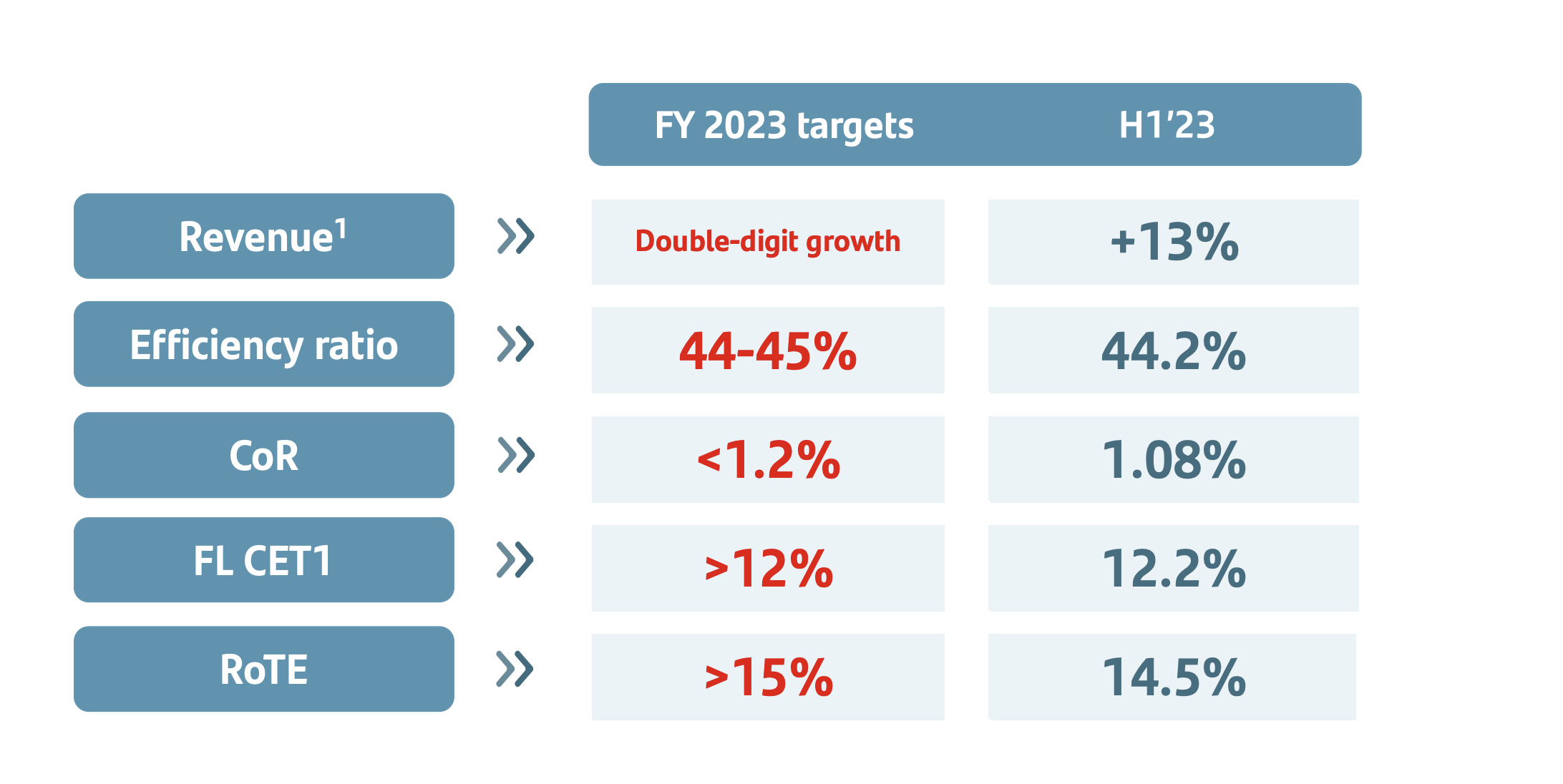

We have 1H23 results, and these are solid. The company managed very strong results, adding over 9M new customers that contributed to a double-digit, 12% increase in company revenues. Profit for the quarter came to €2.7B, which is a 14% YoY increase - and still-growing rates will continue to contribute to an ever-growing NII. EPS was up 13% YoY, the company saw impressive RoTE, and a CET-1 ratio of 12.2%. This is below most other banks that I cover, but it should be seen in the context of what sort of bank we're looking at.

The important thing that I want to see when looking at Santander, is not only to see a growing revenue or earnings. That can come from volume, which is fine (even great), but I'm more about profitability than I am about volume. You can have the best business in the world - and I have had people present business ideas - but unless you can make good margins , then I won't be interested. And while I accept that certain ideas do need scale to work out, I've always been very dubious of the amount of business, particularly tech where the argument has been "We'll make a profit when we get big enough". What's big enough? Look at Spotify ( SPOT ). Pretty big, right?

Spotify, like many businesses that capable investors keep investing in, has never made a single dollar in annual net profit. Billions and billions of dollars in loss.

So, I'm about margins and profitability. And Santander is seeing improved margins, not just volumes. This hails from operating improvements, with an efficiency ratio target of 44-45%. This is still below some of the Scandinavian peers that I cover - check out DNB ( OTCPK:DNBHF ) for class-leading cost efficiency numbers - but it's markedly improving from where the bank was prior.

{kind=link}

Digitization and modernization, leveraging its already impressive global capacities have turned Santander into a growing banking powerhouse, easily able to compete with some of the more efficient players out there. KPIs that I look at include costs per consumer, revenue per consumer, transaction data, and integration. Not because these are more important than earnings, but because these tell me things about the underlying trends, which I consider equally important to a positive thesis, especially to a risk-heavier bank such as this one.

We want to look at global trends because we want Santander to grow. And it does.

{kind=link}

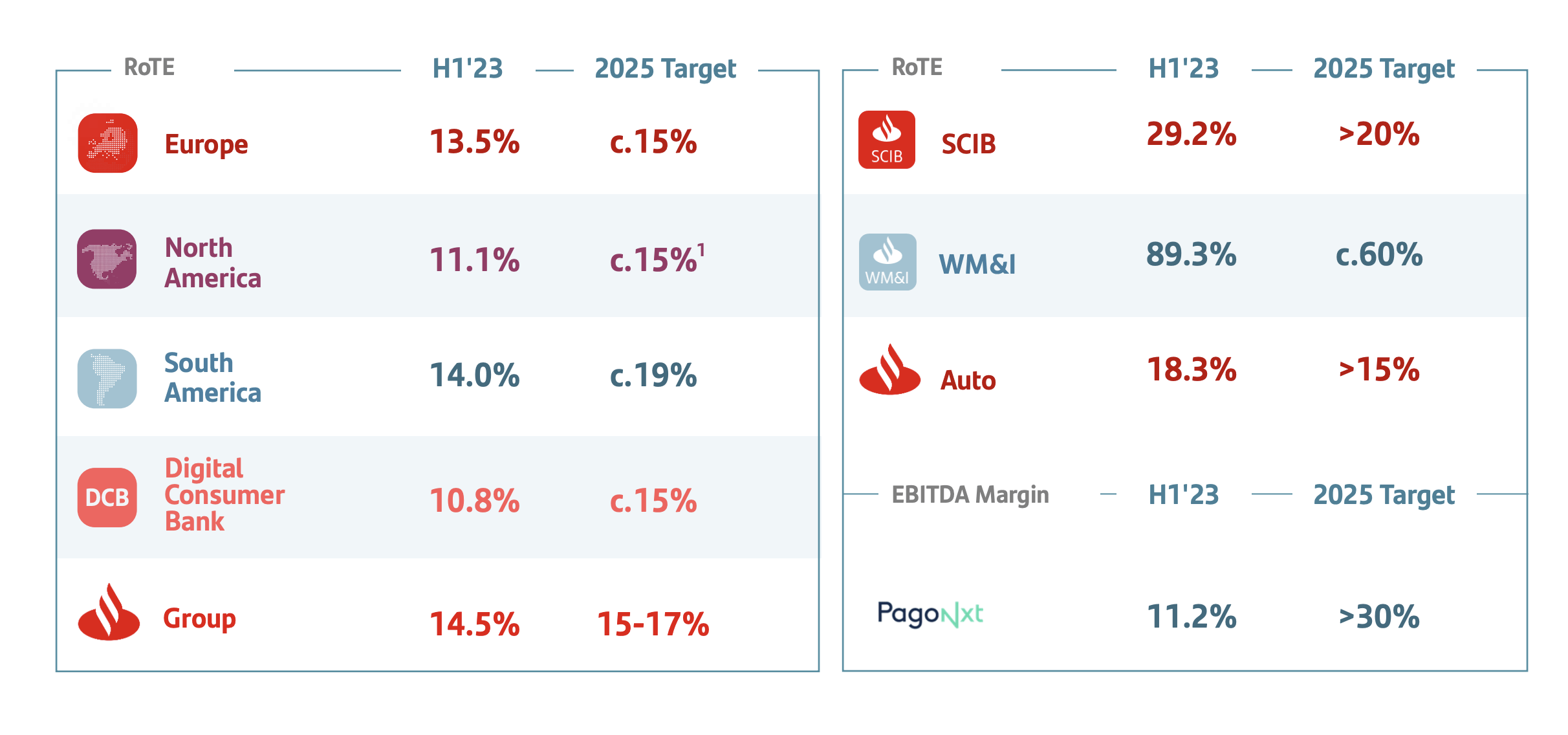

The company is growing in several areas, and profitability targets are slowly being achieved. The keyword here is patience, but that's why you're getting such a gangbuster yield for your risk. Europe is the closest area to profitability targets, short by around 150 bips. Overall, the group is 50 bps shy of its 2025 target range - though the low end.

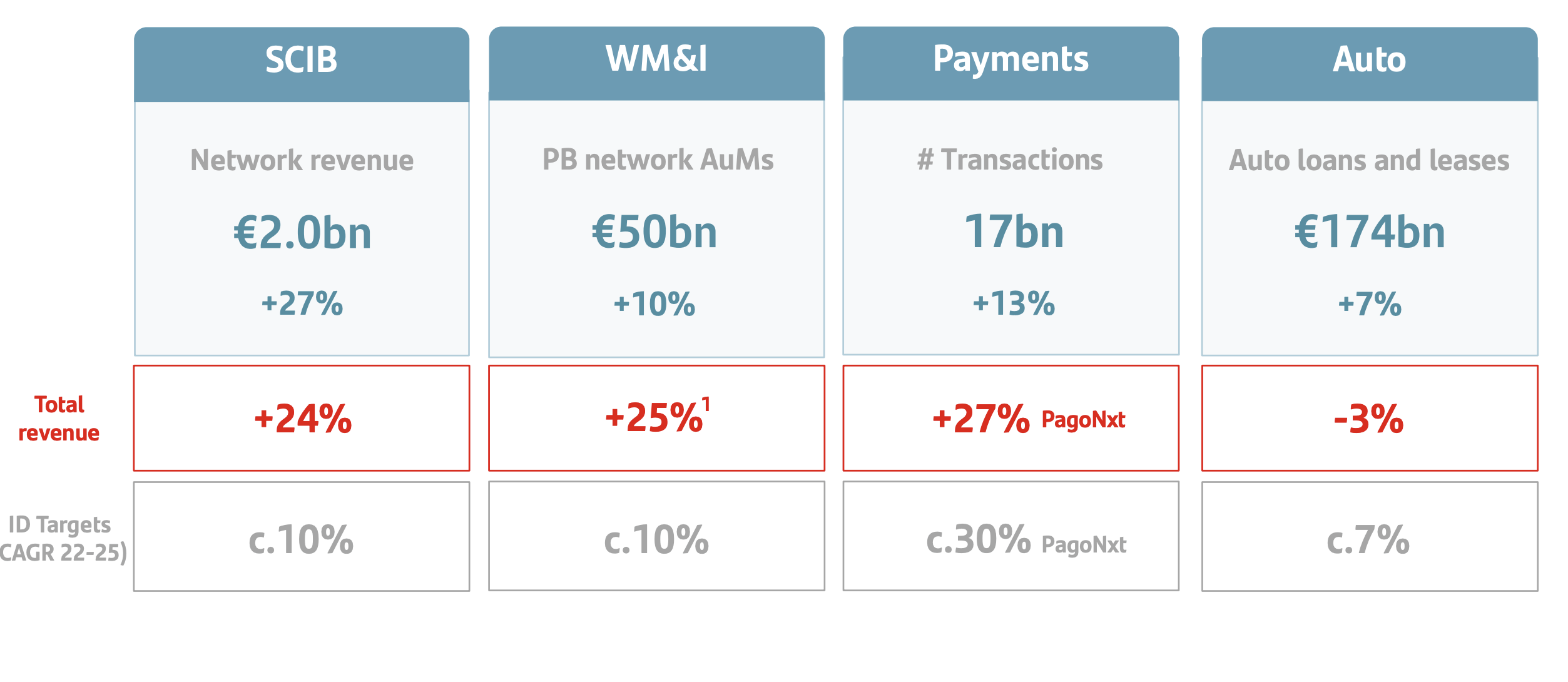

All of the company's "side businesses" are already on track.

{kind=link}

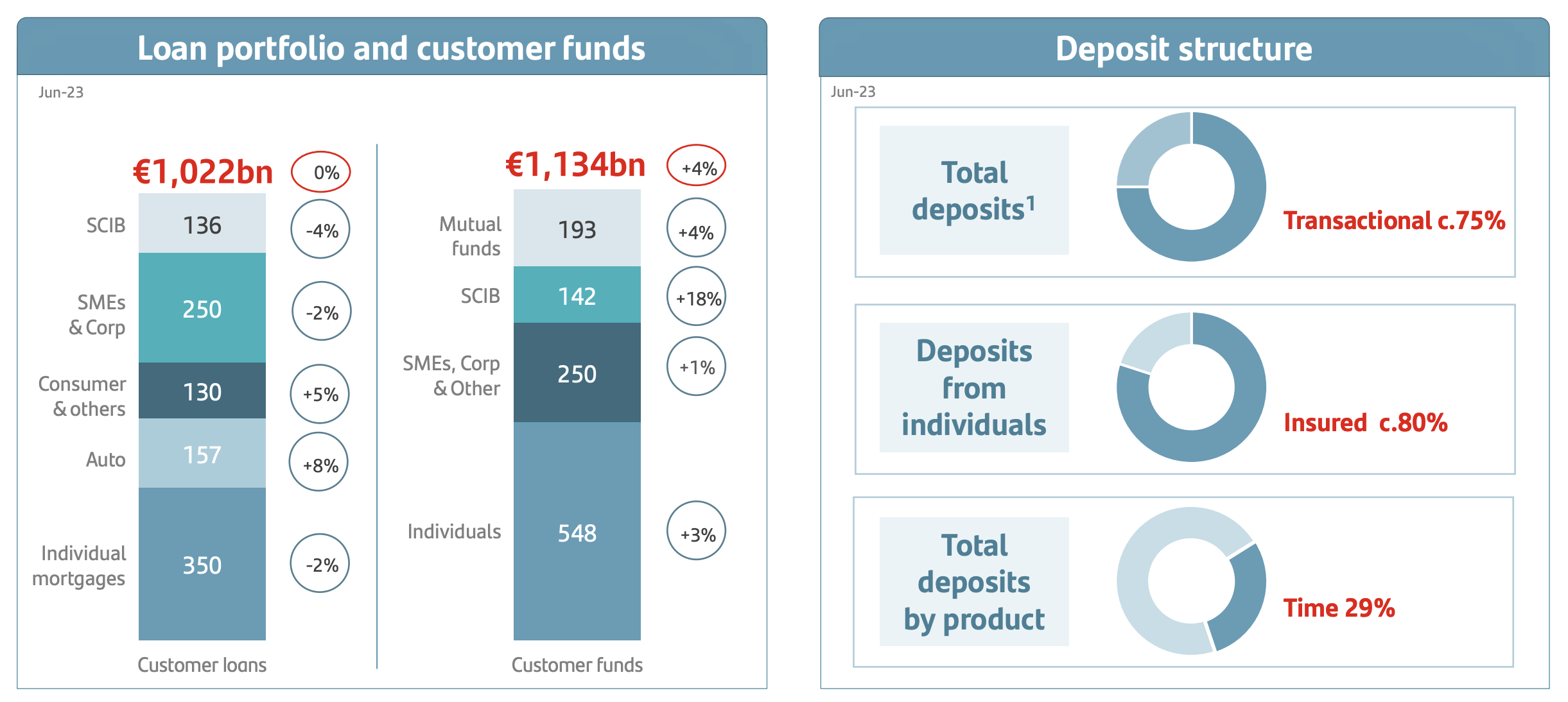

Overall, the positives in the bank were backed not only by tailwinds from NII and interest rates overall, but impressive customer growth added to efficiency improvements and scale advantages. This is exactly what we want to see from Santander. All regions are increasing. Even South America saw solid fee performance, and 95% of the company's revenue is customer related. The one negative, Auto, was mainly due to some poor US results - but the overall interest incomes and margins are absolutely stellar here.

{kind=link}

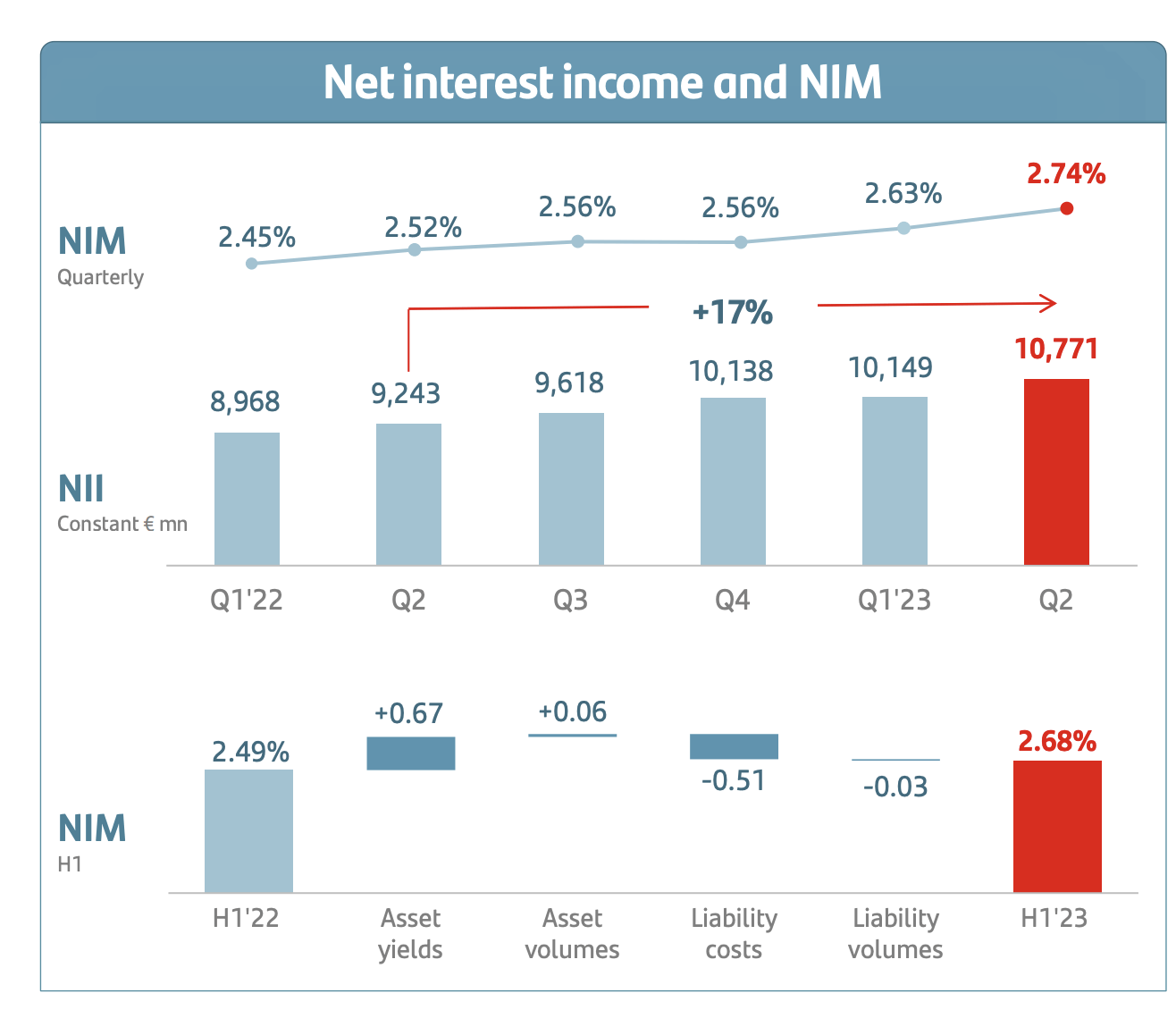

Results here are being driven by consistent asset repricing and positive improvements in the cost of deposits. The bank has reported a positive interest rate sensitivity well in excess of previous targets - nearly half a billion euros more than previously communicated. Europe alone saw a 32% increase in NII due to positive sensitivity, and growth like that is expected to continue in the next few periods.

These are the reasons why I am overweighting banks and finance companies. Next year as well as this year, we're going to see these companies being very cash-heavy due to income increases, which translates into earnings and dividends. I expect the next annual set of European dividends to be very positive.

Cost results are in fact nearly flat. The company has managed a sub-45% C/I for the past 2 quarters, and cost in real terms is down around 1%, and growing below the current rates of inflation in South America, Europe, and DCB.

Safeties and credit qualities?

Very solid. The company's NPL ratio is around 3.07% for June 2023. This is higher than almost every other bank I cover, but here it pays to consider what geographical areas and what risk profile Santander has elected to go into. I never have a problem with risk - I just want to either be paid well for it, or in the case of a company, I want to see the company provisioning well for it.

The increase of 0.02% in NPL's not worth mentioning. The company's credit quality is in fact improving, with CoR dropping on a YoY basis, and the coverage ratio well above 65%. Poland, Brazil, and other higher-risk areas remain foremost here - but again, we need to consider that this is a business that Santander is in.

And overall scores and safeties are very safe.

{kind=link}

The company's CET1 is at 12%+, and ROTE is at good levels.

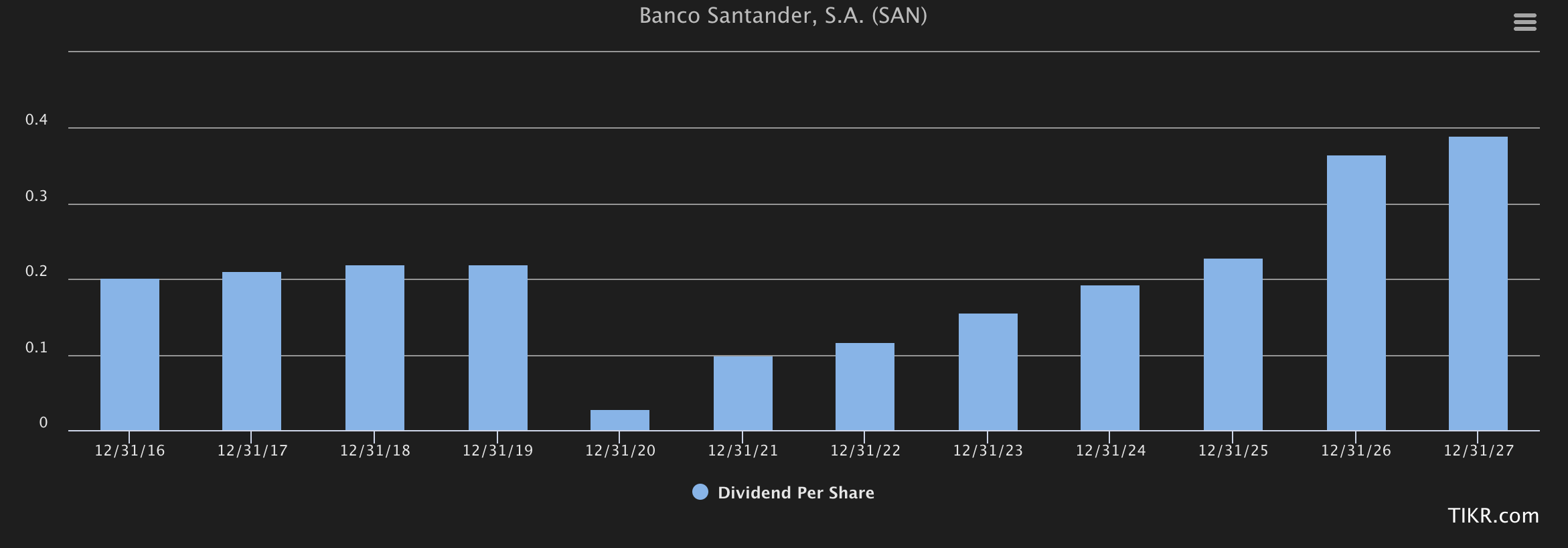

These positive results have the expected consequence of supporting continued, very attractive dividend growth. The company is confident that the shareholders will be enumerated at the target of the 50% dividend policy.

That would mean, in accordance with current expectations, that the yield is somewhere around 5%. But take a look at expectations.

TIKR.com SAN forecast (TIKR.com/S&P Global)

{kind=link}

This dictates the current expectations and a solid fair value for the company as follows.

Santander Valuation - Remains positive

The case for Santander has always been one of recovery. This has been a hard stance to support in the face of a 20-year average growth rate of only 2% per year, and an annualized RoR close to 1-2% due to many declines in EPS - especially during the GFC.

However, since around 2017-2018, I've viewed this bank as one that could really deliver solid returns, if the company continued and executed on its planned turnaround.

Well, I'm now ready to clearly state that Santander is executing upon it.

And if we assume that this is the case, then Santander is now one of the most undervalued A+-rated banks in the world.

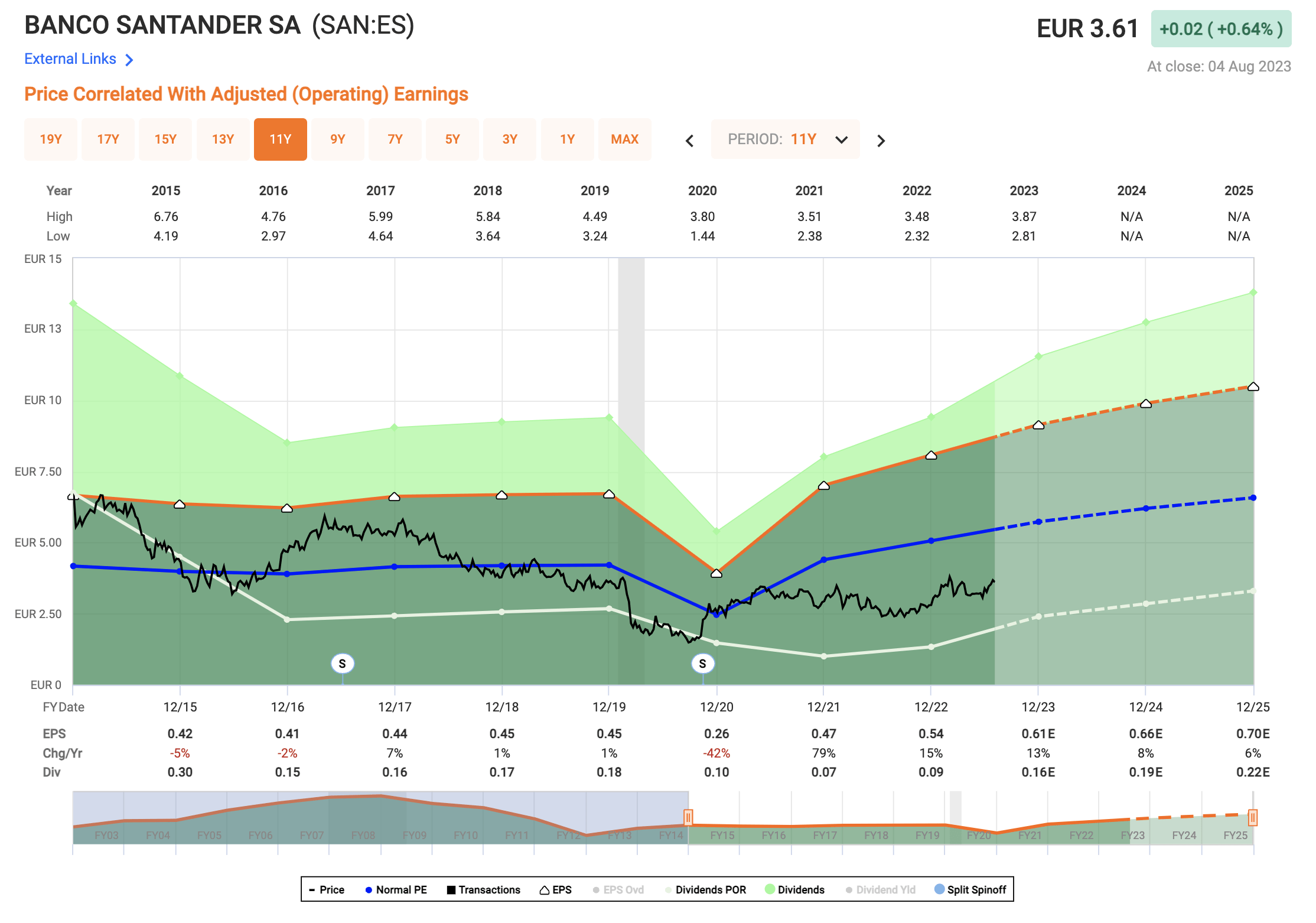

Santander trades at around a P/E of 6x. That's for a bank with A+ credit and a low double-digit or high single-digit forward estimated growth rate and a prospective forward yield starting at 4.5%, but potentially as high as 10%+ current YoC in a few years if you were to invest today, and the bank's earnings cycle up in the way that's currently being expected.

And based on the current interest rate trends, and the current expectations for when we'll introduce rate cuts again, I believe this is looking increasingly realistic.

At today's valuation, you have plenty of allowance for the company's relatively poor forecast accuracy. But again, this is historical - the past few years have been far more stable and growing.

SAN valuation/forecast (F.A.S.T graphs)

{kind=link}

Street targets reflect this increased confidence in the company. Based on the native SAN ticker, we have average PT ranges of €3.8 on the low side and €5.7 on the high side. I remind you, that my target has been around €4 for a long time - but I'm increasing it to €4.2 this article because the company is executing on many of the positives earlier than I expected.

The average PT here is €4.81 from 24 analysts. Out of those 24 analysts, 18 analysts are at a "BUY" or equivalent positive rating here. There's a high conviction here for outperformance.

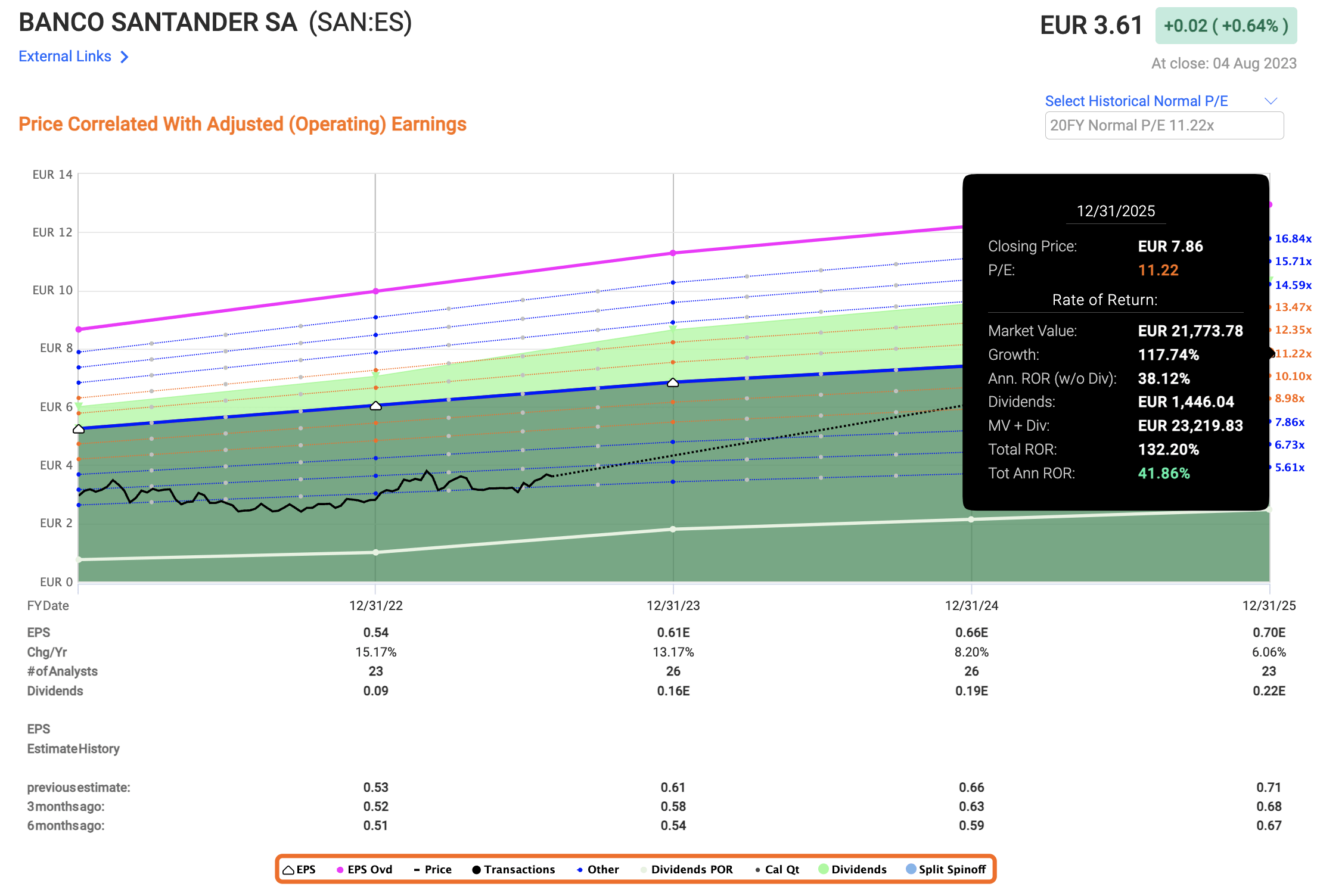

Even forecasting Santander at no more than 8x P/E , you're potentially locking in annual returns of over 25% at this time, or a total of 72% in 3 years inclusive of dividends. That's the 5-year average. We could also go higher. The 20-year average, which I don't view as being outlandish for a stable bank, that I believe Santander is poised to become.

That return at 11.22x would be well over 130%.

{kind=link}

Likely? I'd be careful with this one. Santander would have to truly outperform for this to have a chance to materialize. I expect around 7-8x P/E, and that puts us at market outperformance.

The fact is, you should have bought Santander. My RoR from my first investment here is double digits. I bought a set of shares in October, and we're seeing a closing on 50-60% ROR on that one.

Here is my current thesis for Santander.

Thesis

- Santander is one of the better banks found in the Southern European area and geography. It has significant emerging market exposure, which gives it a heightened risk profile in context to other banks - but it's also immensely qualitative, as evidenced by how it has survived previous downturns.

- I consider Santander a "Buy" at cheap valuations, and I believe this bank can deliver significant upside over time - and now is one of those times.

- I believe the company's thesis and potential have improved since my last article, and I continue to add shares, albeit at a lower rate than some other banks.

- I give Santander a PT of $4.2/share, a share price upgrade, and give it a "Buy".

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Despite a 7% RoR since my last article, I consider the company fulfilling all of my criteria - it's attractive here.

For further details see:

Banco Santander: Poised To Outperform - Here Is Why