CA - Bank of Montreal: Its Direction Shows Promise

2023-08-31 08:51:31 ET

Summary

- Bank of Montreal has maintained a consistent strategy in terms of its expansion that has paid off well in the past.

- Its latest acquisition is from the same playbook of growing and using its growth to expand the U.S., which gets the bank ready for the next acquisition.

- There is quality in its growth, and this is evidenced well in its safety metrics.

- I rate the bank as a buy and hope to benefit from its growth in the future.

I have been observing the Canadian banking space for a few years now. Canada's population is growing but the space is saturated with limited opportunities to turbocharge growth. Each bank has been coming up with its own strategy to expand its market share. But what I have witnessed so far is that the Bank of Montreal (BMO) looks the most promising in terms of the actions it has taken so far in expanding its market share. Also, I have looked at its business and the safety of its growth is quite impressive. In my analysis, I will cover:

1. How its strategic growth plan has fared so far when compared to other banking institutions?

2. Reliability and safety of its growth

3. What to expect for the future?

The Big Five

Royal Bank of Canada ( RY )

The biggest bank in Canada and also the biggest company in Canada in terms of market cap, its recent plan to buy HSBC operations in Canada is not going to be smooth sailing. Further consolidation in an already consolidated industry will face scrutiny from the Competition Bureau which is seeking input on a range of areas such as mortgages, lending, and bank accounts in addition to facing regulatory and political hurdles. The deal still has a big chance of going through but it would take some time before we see clarity and the promise of this acquisition.

Bank of Nova Scotia ( BNS )

This bank has one of the most diverse operations out of all the Canadian banks. Its strategy has been to expand in Latin American markets and has touted this as a big differentiator. But the performance has been subpar. The new head of the bank has expressed disappointment with the bank's underperforming Latin American operations and there are suggestions that the bank might scale back investments or consider selling parts of its assets in the region or exit certain countries altogether. While Scotiabank management has indicated that selling Latin assets is a low priority, there is investor pressure for change due to the underperformance of these operations. The challenges in the Latin American operations have contributed to Scotiabank's underperforming share price compared to peers. Scott Thomson the CEO of Scotiabank plans to release the bank's strategic plan by the end of the fiscal year in October.

Toronto-Dominion Bank ( TD )

TD and BMO were competing in the BMO's recently closed deal of buying Bank of the West. Shortly after losing this deal to BMO, they made an acquisition offer to First Horizon for $13.4B in cash. This faced regulatory scrutiny and after much wrangling TD decided to pull out of the deal altogether. Since pulling out of this deal, it is unclear what the long-term strategy would be for the bank.

Canadian Imperial Bank of Commerce ( CM )

The smallest of the Canadian banks among the big 5, as far as I can see the bank has not had any moves that would potentially move the needle in a big way. Its focus has been moving slowly and steadily enhancing primary Canadian retail banking operations and expanding the Commercial and Wealth Management sector both in Canada and the USA. This means there is no shot-in-the-arm growth that can be expected from this bank in the near future.

Bank of Montreal ( BMO )

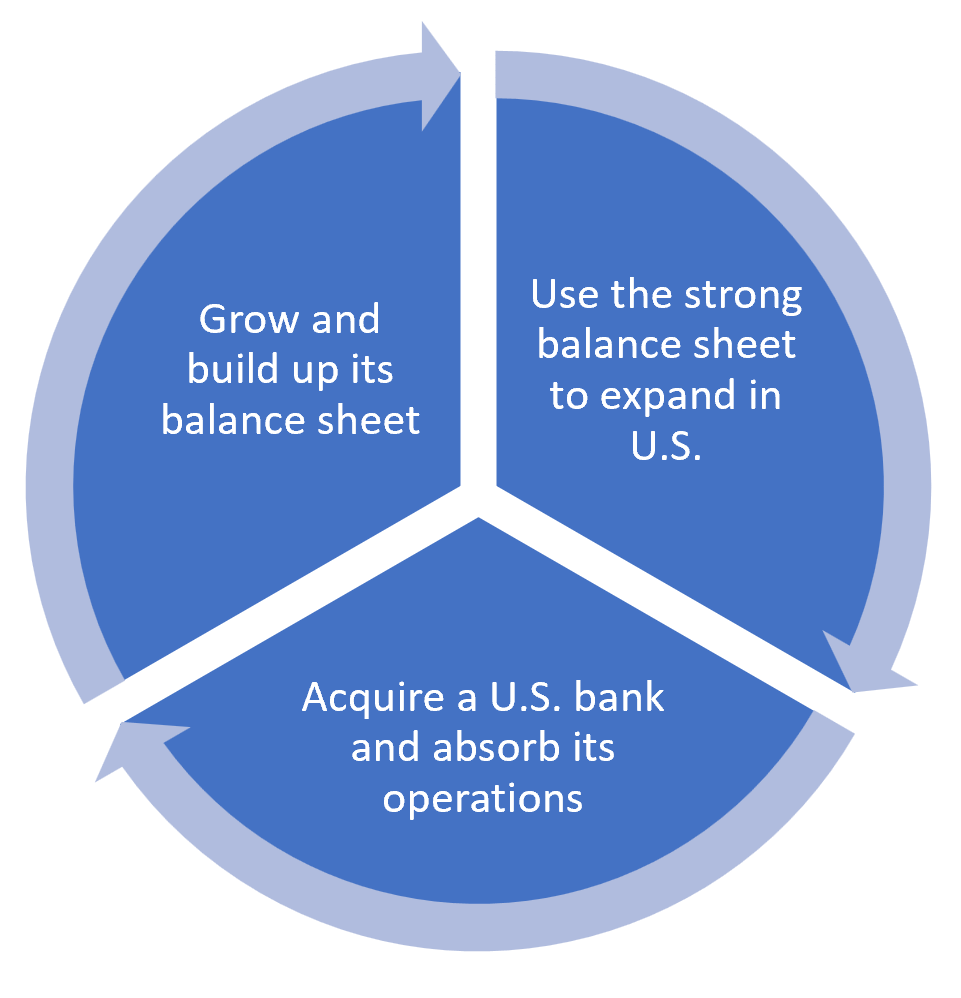

Bank of Montreal had made expanding to the U.S. a key part of its future and as such had readied a cash chest to be able to make a move and their move to acquire Bank of the West was completed successfully earlier this year (with an offer of $16.3B). As of this point, BMO is fully engaged in completely integrating Bank of the West's operations into its own. The acquisition brings nearly 1.8 million customers to BMO and extends its banking presence through more than 500 additional branches and commercial and wealth offices in key U.S. growth markets. In my opinion, at this point, this is the only bank that has been able to deliver on its strategy which can potentially move the needle for the bank in a big way. Bank of the West has a strong network in California and its population and economy are larger than Canada's. The acquisition is the latest in its series of moves to expand in the United States. After integrating Marshal & Isley in the 2010s and Harris Bankcorp in the 1980s, BMO has steadily been growing and the latest acquisition is a step in the same strategic direction. But what is the quality of its growth after it keeps rolling its acquisitions?

Total Assets have grown by close to 80% in the last ten years. Its Assets-to-equity ratio is also sufficient at 16x and 75% of its liabilities are made up of customer deposits which is far less risky than financing through external sources.

{kind=link}

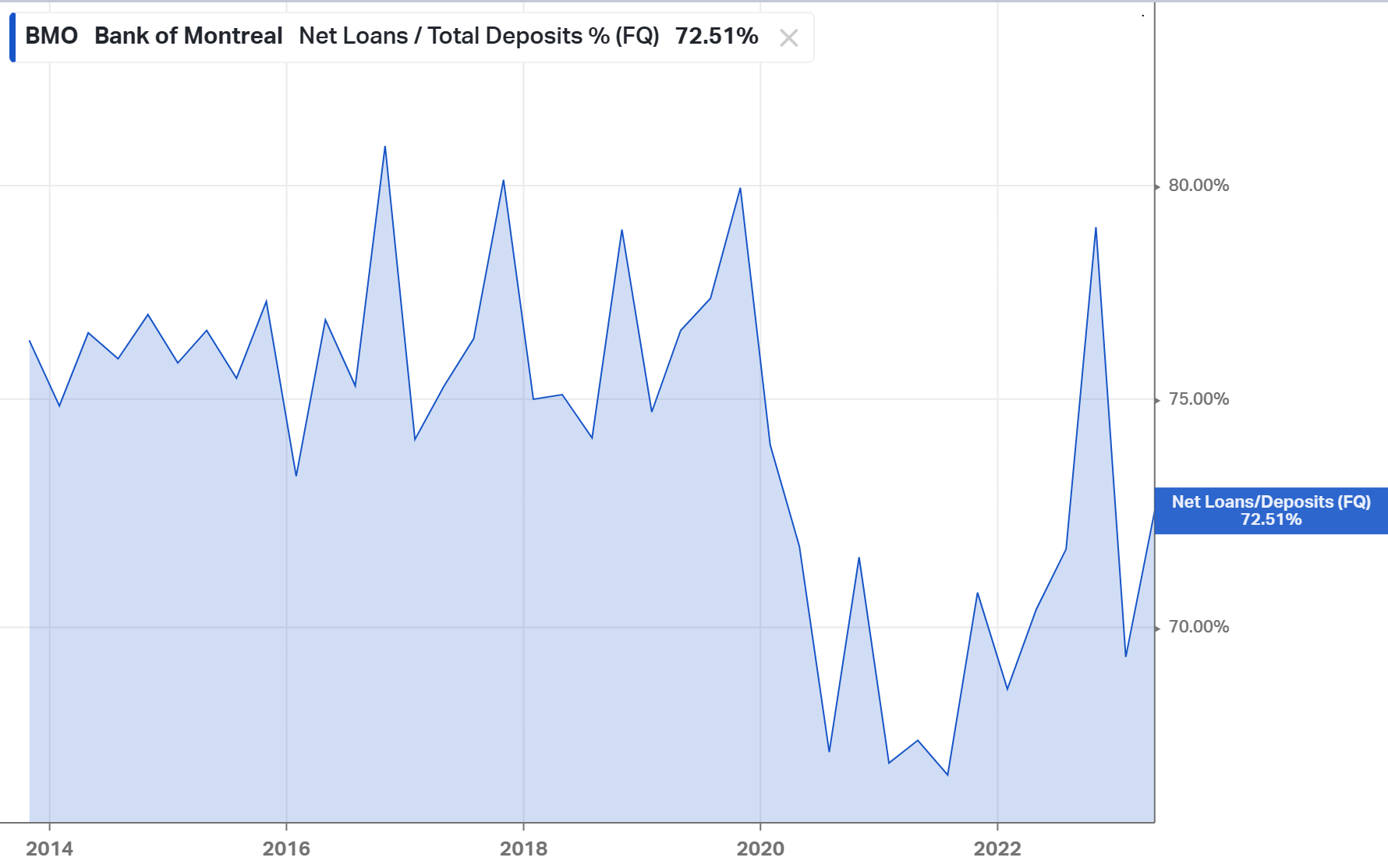

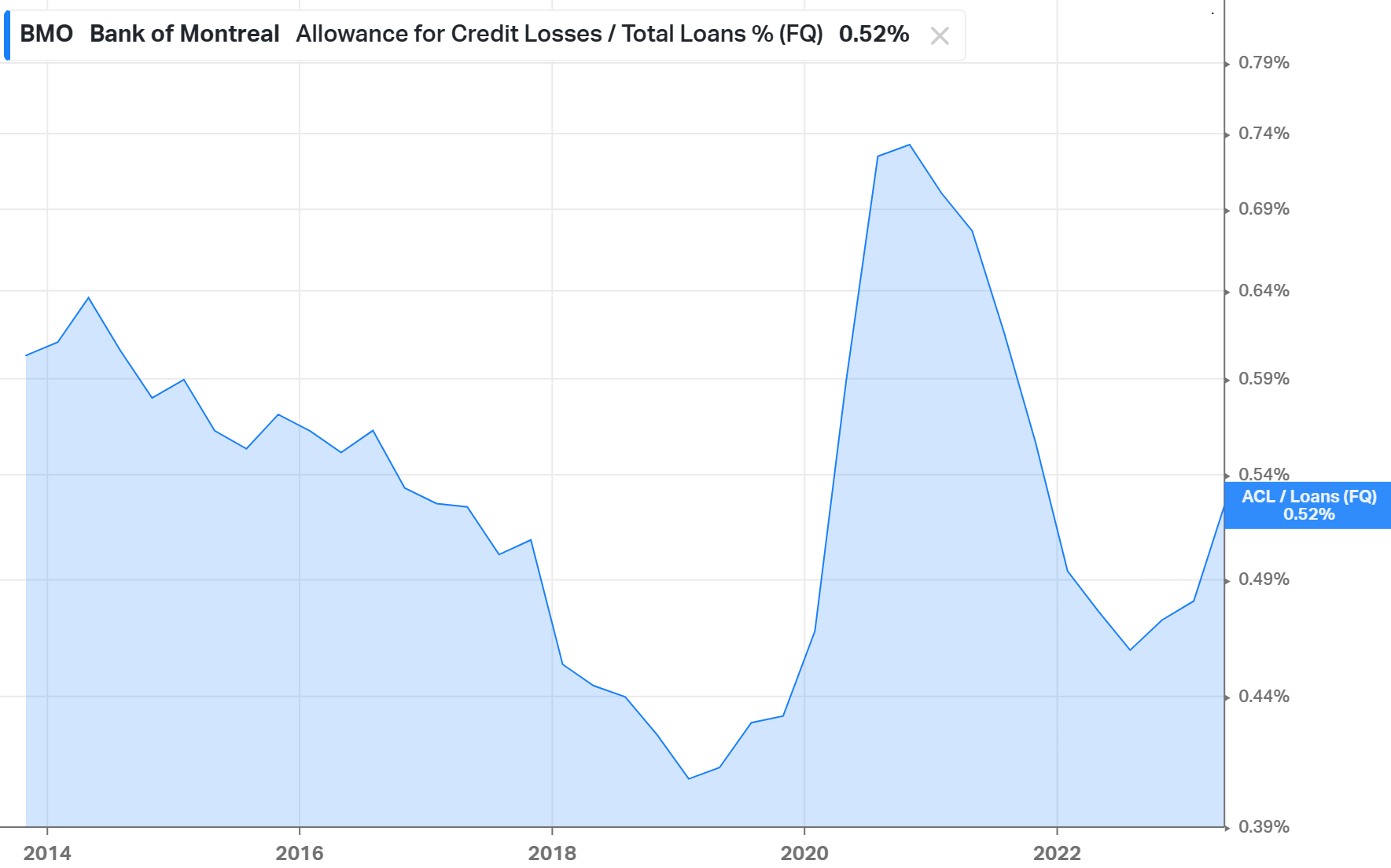

Presently its net loans to total deposits is at 72.5% and this is at a healthy level. Additionally, its allowance for credit losses to its total loans saw its peak during Covid and started dropping down again. At its present level of 0.5%, it indicates a healthy look. It also has a sufficient allowance for bad loans at 126%

{kind=link}

For banks, dividends are one of the things investors count on that boost their total return. BMO boasts of being the longest-running dividend-paying company in Canada with a policy to pay out 40% to 50% of its earnings in dividends to shareholders over time.

1. The current dividend yield is at 5%

2. Dividends have been stable and increased over the last ten years

3. Dividends are well covered by earnings and the current payout ratio is 57%

Last 2 Quarters

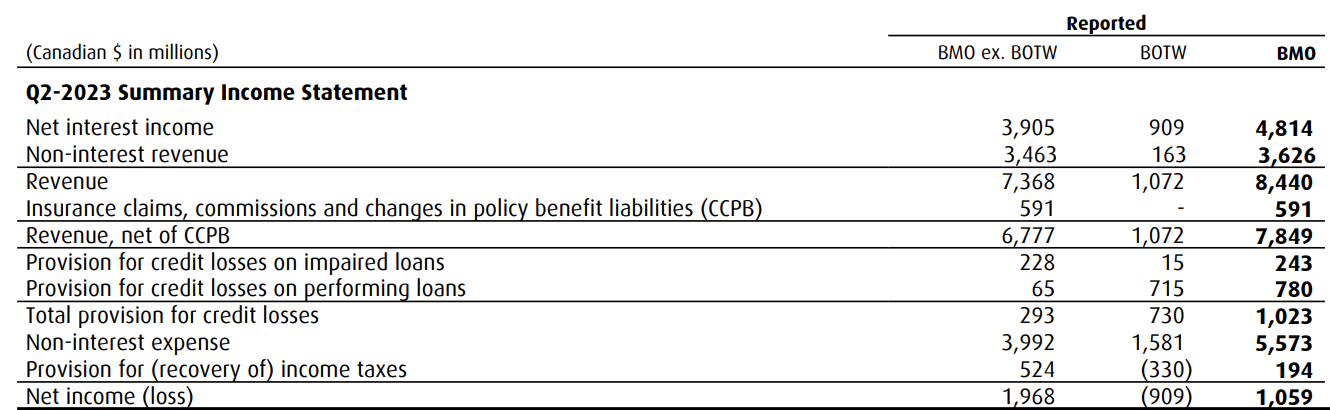

The financials for Q2 and Q3 include the impact of the BOTW acquisition. For Q2, the acquisition contributed close to 13% of its revenues and came with acquisition and integration costs of $549M. BMO's Common Equity Tier 1 (CET1) Ratio was 12.2% as of April 30, 2023, a decrease from 18.2% at the end of the first quarter of 2023, primarily attributed to the acquisition.

{kind=link}

{kind=link}

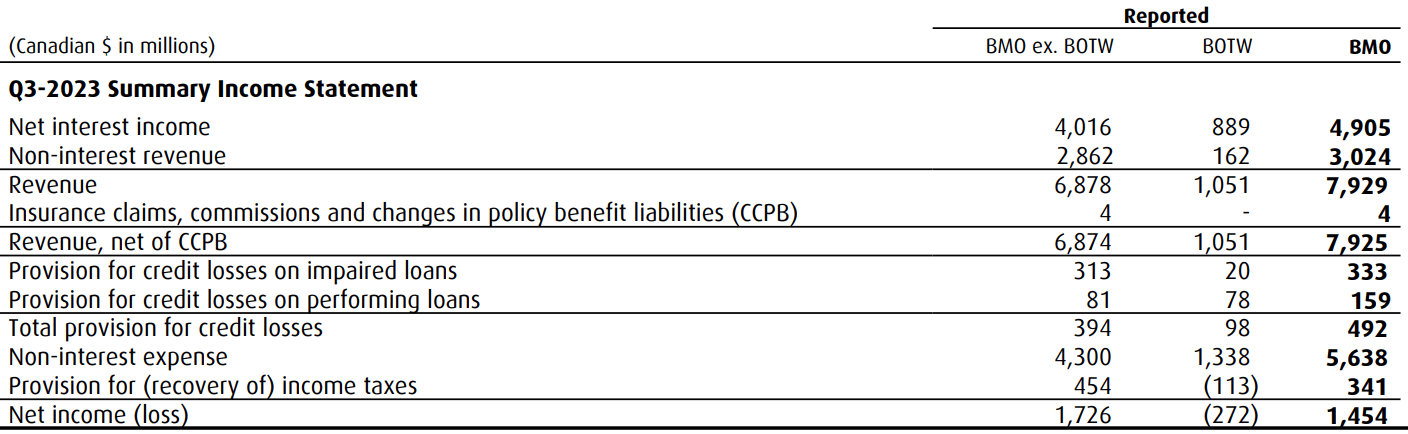

For Q3, while the acquisition contribution remained the same, overall net income showed an increase coming in at $1.4B. Acquisition and integration costs came in at $370M reported in non-interest expense. The inclusion of Bank of the West results in the current quarter decreased reported net income by $272M. Big acquisitions like this are always challenging with the full benefits that are almost never seen immediately. But BMO has been down this path a few times before and has come out bigger and stronger. This is what the CEO had to say about the latest earnings in light of the acquisition -

We continue to deliver solid financial results reflecting the strength, diversity, and active management of our businesses in an evolving environment. Record revenue in Canadian Personal and Commercial Banking and contribution from Bank of the West drove good pre-provision, pre-tax growth this quarter, and our capital and liquidity position remains strong...

We're accelerating efficiency initiatives and remain focused on dynamically positioning the bank for long-term growth and sustained profitability through disciplined expense and risk management...

Valuation

BMO trades at a price-to-earnings multiple of 11.5x, trades higher than its book value (1.1x), and has a dividend yield of 5%. For my comparables, I considered some of the biggest banks in North America.

| Bank |

| P/E |

| P/B |

| Dividend Yield |

| JPMorgan Chase (JPM) |

| 9.4x |

| 1.5x |

| 2.7% |

| Bank of America ( BAC ) |

| 8.1x |

| 0.9x |

| 3% |

| Citigroup ( C ) |

| 6.5x |

| 0.4x |

| 4.9% |

| Well Fargo ( WFC ) |

| 10.4x |

| 0.9x |

| 3% |

| Royal Bank of Canada ( RY ) |

| 11.3x |

| 1.5x |

| 4.4% |

| Toronto-Dominion Bank ( TD ) |

| 10.1x |

| 1.3x |

| 4.7% |

| Bank of Nova Scotia ( BNS ) |

| 9.5x |

| 1x |

| 6.5% |

| Canadian Imperial Bank of Commerce ( CM ) |

| 10.6x |

| 1x |

| 6.2% |

BMO trades at the highest PE multiple in this list ranks sixth in terms of book value and third in terms of its dividend yield. If you consider only the Canadian banks, the results are similar (highest PE multiple, mid-level ranking for book value and dividend yield). I believe this is because the market is willing to pay a premium mainly due to the clarity of its growth strategy and also how much success it had in the past based on this strategy. When you look at its asset growth this could be taken as a sign of its success. Out of all the banks, at the end of FY 2022, BMO had the second-highest growth in assets. This will only increase further when you consider their acquisition (the biggest acquisition in Canadian banking history) and how it will result in further growth.

| Total Assets () - 2017 |

| Total Assets () - 2022 |

| Growth |

| TD |

| 991415 |

| 1407597 |

| 42% |

| RY |

| 940145 |

| 1407370 |

| 50% |

| BNS |

| 709475 |

| 990565 |

| 40% |

| BMO |

| 550032 |

| 836250 |

| 52% |

| CM |

| 438165 |

| 692665 |

| 58% |

| JPM |

| 2533600 |

| 3665743 |

| 45% |

| BAC |

| 2281234 |

| 3051375 |

| 34% |

| C |

| 1842465 |

| 2416676 |

| 31% |

| WFC |

| 1951757 |

| 1881016 |

| -4% |

I rate the bank as a Buy. Out of all the Canadian banks, I find the most promise in its strategy. It is not just based on hope either. I have reviewed its past where it had much success in the strategy and the latest acquisition is a step in the same direction.

{kind=link}

If the bank is able to grow by absorbing the success from its latest acquisition, it will continue the flywheel effect that we have been seeing. Additionally, as we saw, it is not just empty growth either. The bank has maintained its health and shows quality even while growing by more than 50% in the last 5 years. If the story follows the same trajectory that we have seen before, we may see the bank make another sizeable acquisition move in the next 10 years.

When would I change my rating from Buy to Strong Buy?

If the bank integrates its operations successfully and turbocharges its growth while the valuation goes down

When would I change my rating from Buy to Hold?

If the bank is not able to realize the full benefits of its acquisition, shows subpar growth and valuation remains elevated

When would I change my rating to Sell?

If there are indications that the latest move was far from its promise and valuation remains elevated

I will be watching the space closely and keep my readers informed if there is a change in my thesis.

For further details see:

Bank of Montreal: Its Direction Shows Promise