CA - Bank of Montreal: Overvalued But Nice 4.5% Dividend Yield And Growth From Recent Takeover

2023-08-02 03:22:59 ET

Summary

- Bank of Montreal gets a hold rating today.

- Positives: 4.5% dividend yield higher than sector average, capital & liquidity position, share price close to 200-day SMA, balance sheet growth after the acquisition of Bank of the West (BOTW).

- Headwinds: lack of YoY net income growth trends, valuation high vs sector average.

Research Brief

With its next quarterly earnings result coming out towards the end of this month on August 29th, Bank of Montreal ( BMO ) has come across my radar screen, especially after its acquisition of Bank of the West, and so today we will discuss its potential for value investors who are looking for a solid dividend play.

Though it is Canada-based, the bank also trades on the NYSE as well.

Some notables to mention from the company website : 8th largest bank in North America by assets, 13MM customers, roots date back to 1817, operates 3 business segments: personal/commercial banking, wealth management, capital markets. Known also for the longest-running dividend payout record of any company in Canada, at 194 years.

I would, therefore, file this one in the category of "dividend quick picks."

Ratings Methodology

Our goal is to find undervalued stocks of companies with solid financial fundamentals, that pay competitive dividend yields. Our key industry focus is tech, financials, insurance, innovation.

To simplify my rating of an equity, I have broken it down into whether I would recommend or not recommend based on these individual factors:

- Valuation.

- Dividend Yield.

- Net Income Growth.

- Capital & Liquidity.

- Share Price vs 200 Day SMA.

If I recommend on all 5 categories, it is a "strong buy", 4 categories is a "buy", 3 is a hold, and less than that is a sell rating. Then I compare my rating to the consensus ratings from Seeking Alpha & Wall Street.

Valuation: Not Recommended

I like to start off this analysis by talking about the valuation of this stock, and to do so we will use two key metrics, the forward P/E and the forward P/B ratios, sourced from Seeking Alpha data .

With a P/E of 15.60, you are currently paying almost 16x earnings to buy this stock, and that valuation is over 51% above its sector average.

BMO - P/E ratio (Seeking Alpha)

I am looking for a valuation on this stock that is either below the sector average or at most a few points above it, so long as the P/B ratio is also undervalued. In this case, I would consider the price-to-earnings too high compared to the sector it's in, which is hovering closer to 10x earnings. I like it at a forward P/E range of 8.00 to 11.00.

In terms of the P/B, you are paying almost 1.25x book value, which is almost 14% above the sector average that is closer to 1.10x book value.

BMO - P/B ratio (Seeking Alpha)

Much like the P/E ratio, I consider the P/B on this stock too high when compared to the average. I like it at a range of 1.00 to 1.10.

So, when considering the data, I would not recommend this stock based on current valuation alone.

Dividend Yield: Recommend

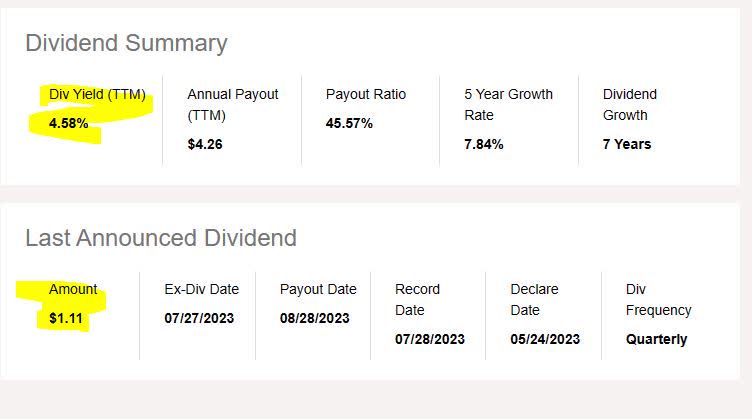

Now, if you are looking for a quick dividend pick, this is it. This stock currently offers a dividend yield of 4.58%, and a quarterly dividend of $1.11, according to Seeking Alpha data .

BMO - dividend yield (Seeking Alpha)

{kind=link}

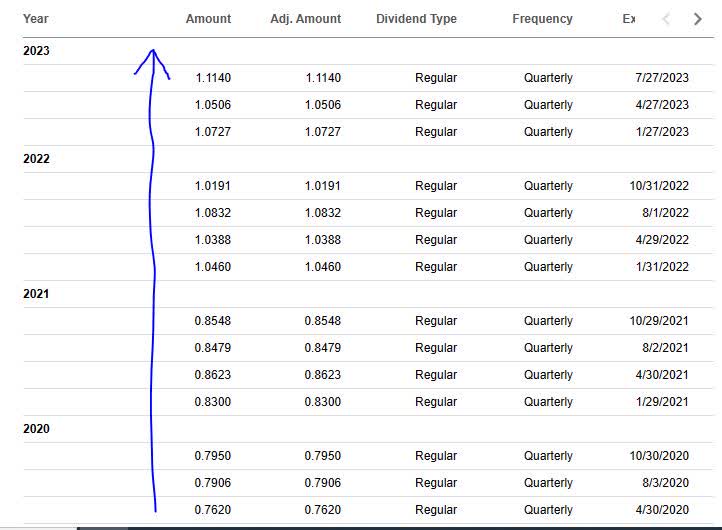

Also, another positive to mention is that this stock has a steady, reliable history of quarterly dividend payments that have been on a rising trend in the last few years, as the table below shows.

BMO - dividend history (Seeking Alpha)

{kind=link}

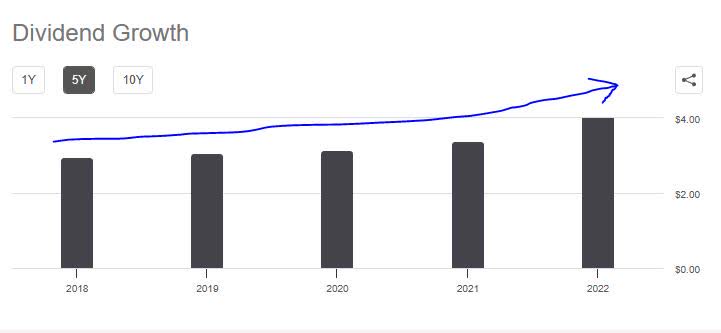

In addition, I like their 5-year positive dividend growth, going from an annual dividend of $2.95 in 2018 to $4.19 in 2022, a 42% increase.

BMO - 5 year dividend growth (Seeking Alpha)

{kind=link}

Notable to mention is that when comparing to the sector average, this stock's dividend yield is over 35% above the sector average which is hovering around 3.5%. My own target range is that it be at least 10% above average, which it is.

BMO - dividend yield vs sector average (Seeking Alpha)

Based on the data, I can confidently recommend this stock as a great dividend play for an income-oriented portfolio.

Positive YoY Net Income Growth: Not Recommended

In this category, I am looking to spot positive net income growth trends over a period of 1 year, rather than simply look at individual quarters.

In the last quarterly earnings reported, which for this bank was their Q2, it is first important to note that they undertook a major acquisition by acquiring Bank of the West. This clearly impacted their reported results for Q2.

For example, in their presentation commentary they mentioned a "517MM initial provision for credit losses on performing loans, $545MM integration costs and $77MM amortization of acquisition-related intangible assets related to the BOTW acquisition." and a "reported earnings per share of $1.30, down 82% YoY."

The following table shows the type of YoY impact to earnings they faced after this acquisition:

BMO - Q2 reported earnings (BMO - Q2 presentation)

Rather than ding a company because of a single quarterly dip due to a major acquisition, in a positive light I expect this takeover of BOTW to generate longer term earnings growth but also expands the business and is a sign that BMO is in an even stronger position with a bigger balance sheet.

Another tailwind that will, and has helped this bank is the rate environment, as you can see from YoY growth in net interest income:

BMO - net interest income (BMO - q2 presentation)

Considering that the Fed recently raised rates, and there is probability that rates will stay put after the next meeting, according to CME FedWatch , as well as the Bank of Canada recently raising rates , I think this will continue to benefit this bank's net interest income in the next quarter, possibly even more so, so I expect to see both improvement to the top line and bottom line in the Q3 results.

However, at this time I do not recommend this stock on the basis of YoY net income growth, regardless of the one-time acquisition hit they took last quarter.

When looking at the income statement on Seeking Alpha, for example, there is no longer-term trend of positive net income growth, but rather it is lopsided. Consider that the three quarters that came after April 2022 were all lower than that quarter when it came to net income:

BMO - net income growth (Seeking Alpha)

I am looking for this otherwise fine bank to show at least 10% YoY net income growth trends going forward. Consider that one of its peers in the Canada bank sector, CIBC ( CM ), has achieved nearly 5% YoY net income growth in their last quarterly result, based on their income statement .

High hopes are on this bank to take the lead in Q3 when it comes to earnings.

Capital & Liquidity: Recommend

This bank no doubt has a strong capital & liquidity position, and the evidence points to it, so I would recommend it in this category.

For example, its most recent CET1 ratio of 12.2% and Liquidity Coverage Ratio of 129%, two key metrics I track with banks, are both well above regulatory minimums, and have been so consistent in the last few quarters, as the graphic below shows.

BMO - CET1 and LCR (BMO - q2 presentation)

I am also confident in this banks' balance sheet, which is huge. Consider that in the most recent quarter the bank had 1.25T in total assets, and 1.16T in average earning assets. This is a major YoY increase.

BMO - balance sheet highlights (BMO - q2 supplementary info)

Also related to the BOTW acquisition, the impact to the balance sheet is a positive one: it "added $45B to Business & Government loans and $34B to consumer loans," according to the earnings presentation .

And, as you probably know, the nature of the business of a bank is that as it expands its "earning assets" like loans it also drives interest income on that expanding asset base as well. That is, assuming that the majority of the loan book is performing.

Stock Price vs 200 Day SMA: Recommend

Before market open on Tuesday August 1st, the share price sat at its previous close of $92.92, hovering around 0.90% above the 200-day SMA:

My investing idea calls for trading within a "range" of 5% below & above the 200-day SMA, tracking that long-term average as a benchmark. This would mean a trading range of $87.48 to $96.69.

Since the share price is currently trading within that range, I would recommend it as a buying opportunity.

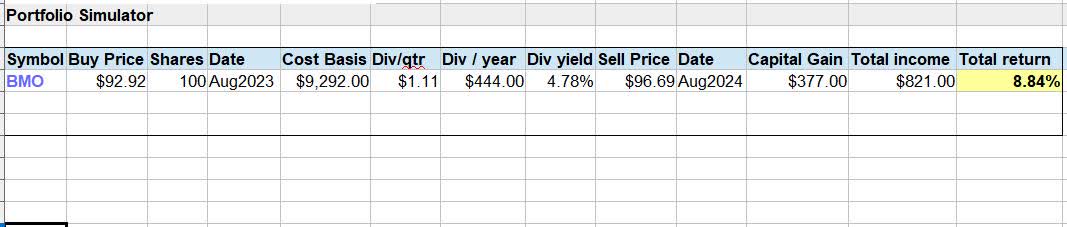

Below is a table showing my investing idea and a simulated trade:

BMO - trade simulator (Albert Anthony & Co)

{kind=link}

In the above simulated trade, I am buying 100 shares at the current share price of $92.92 as of the writing of this article, holding for 1 year to earn the full dividend income for that year, and selling at 5% above the current 200-day SMA. Achieving both a dividend yield of 4.78% and a capital gain, my total return on invested capital is projected to be 8.84%.

A risk to this investing idea is that the 200-day moving average could go in directions not favorable to this trade, thereby causing unrealized capital losses for an extended period. An idea to offset some of that risk is selling covered call options in order to earn additional income from options premiums.

Ratings Score: Hold / Neutral

As this stock won only 3 of my 5 rating categories, today it gets a neutral/ hold rating. This is in line with the Seeking Alpha quant system rating, but is less bullish than the consensus rating from SA analysts and Wall Street, as you can see below:

ratings consensus (Seeking Alpha)

Risks to my Outlook: Deposit Outflows

A risk to my neutral outlook for this bank that I can think of, that investors and analysts will be looking at, is deposit outflows. Deposits are part of the lifeblood of a bank, and this one is no different. However, we saw in the March regional bank crisis in the US but also the Credit Suisse takeover in Europe that clients can easily move their capital to any number of other banks. One reason is fear of a bank run by other depositors; another reason is seeking higher rates in the current environment by re-allocating funds to higher-rate products.

However, when looking more closely at the growth in average deposit balances at this bank, both their Canadian and US business segments have shown growth trends over 4 quarters, as the charts below show:

BMO - deposit trends (BMO - q2 presentation)

So, the data shows that the risk of deposit outflows at this bank has not made a big impact, despite a Q1 drop in the US average balances, as the bottom chart shows. What there is a trend in, however, is greater movement into the money market funds and certificates of deposit. Again, they provide better rates, and the client can keep their money in house rather than go elsewhere.

I think it's safe to say that this bank's risk of deposit outflows has proven to be a minor risk so far.

Analysis Wrap Up

To summarize today's discussion, here are the key points:

I gave this stock a hold rating today, in line with the rating consensus from the Seeking Alpha quant system.

Positives: dividend yield, share price, capital / liquidity.

Headwinds: valuation, net income growth down YoY.

The risk of deposit outflows has been addressed and determined to be minor.

As far as its next earnings call towards the end of this month, considering they missed earnings estimates in 3 of the last 4 quarters, I predict the next one will come near analyst estimates but not greatly beating it either. I expect a slight earnings beat of between $0.02 - $0.05, giving a little bullish momentum to the post-earnings share price. This should bode well for those already "holding" this stock from an earlier price point, so consider in this context that a "hold" rating is not a negative thing.

BMO - earnings beats (Seeking Alpha)

For further details see:

Bank of Montreal: Overvalued But Nice 4.5% Dividend Yield And Growth From Recent Takeover