BCS - Barclays: 6% Dividend Yield And Undervalued But Waiting On Next Dip

2023-07-14 17:37:57 ET

Summary

- Barclays gets a buy rating today on its US-traded ADR.

- Positives: Over 6% dividend yield, the company in strong financial position and recently passed stress testing, net interest margin benefits from rate environment, the company is undervalued.

- Headwinds: Price trend could use another dip very soon, to get it below its 200-day SMA, presenting a better buying opportunity.

- A known risk is a recent media article on the firm engaging consultants to help redeploy capital among some of its business units, rather than more share buybacks.

Research Brief

Today amidst bank earnings season I am shifting gears and going global covering a UK-based bank, Barclays ( BCS ), which trades both on the London Stock Exchange directly but also as an ADR on the NYSE, which is what I will be rating. Its next earnings call is coming up in a few weeks on July 27th, and I will be watching with great fervor.

Those of us who have ever flown into London's Heathrow Airport can often spot the Barclays tower on final approach, as you fly past the city financial district on a clear morning. The firm has no doubt been a mainstay of global banking circles for a long time, beyond just the City of London.

Some notable items of mention from the company website are: The firm's roots go as far back as 1690, has a diversified portfolio of solutions across consumer and small business as well as corporate & investment banking, and a strong US presence including market penetration with its Barclaycard product and online CDs.

Rating Methodology

I break down my rating into 5 individual categories: share price trend, valuation, dividends, company financial health, and macro factors affecting the company.

To get a buy rating, the stock needs to win 4 of 5 categories. If I recommend it on 3 categories, it gets a hold rating, and less than that is a sell rating.

Share Price Could Use Another Dip

To kick off this discussion, let's look at the share price as of market close on Thursday, July 13th:

Price at market close July 13 (StreetSmart Edge trading platform)

The share price closed at $8.26. As you can see in the chart I made, this is above both its 200-day SMA (red line) and 50-day SMA (blue line), and well above its March dip by now which it has recovered from nicely.

In my own portfolio strategy simulation, my target buying price (highlighted in yellow) is $7.20-$7.60. The goal is to buy when it dips below both moving averages, and holding it for a timeframe of 1 year, exiting with a capital gain target of at least 10%, which would put the exit price around $7.92-$8.36. In the meantime, it would be a dividend-generating opportunity.

Now that the March bank crisis has largely stabilized, I don't think it will dip to the March lows again anytime soon, but I like it as a buy at $7.50, not the current price necessarily. However, I welcome your thoughts in the comments section whether you think it will dip soon, and why or why not.

So, based on price trend, I do not recommend it currently, but perhaps at the next dip.

An Undervalued Opportunity

Next, let's look at valuation metrics taken from Seeking Alpha data . We will use two metrics available, GAAP-based forward P/E ratio and TTM P/B ratio, and compare with sector averages and a bank-sector peer.

Notable figures that grabbed my attention are that its P/E of 6.03 has earned a grade of A+ from Seeking Alpha and is over 35% less than the sector median, while its P/B of 0.46 also earned an A+ and is over 55% lower than the sector median.

For comparison, I will use its London-based banking peer HSBC ( HSBC ) which also trades as an ADR on the US exchange. Its valuation: forward P/E of 6.75 and TTM P/B of 0.93. Not bad, but in this case, Barclays comes in at a lower valuation.

In this category, I recommend this stock based on being undervalued and hence an opportunity.

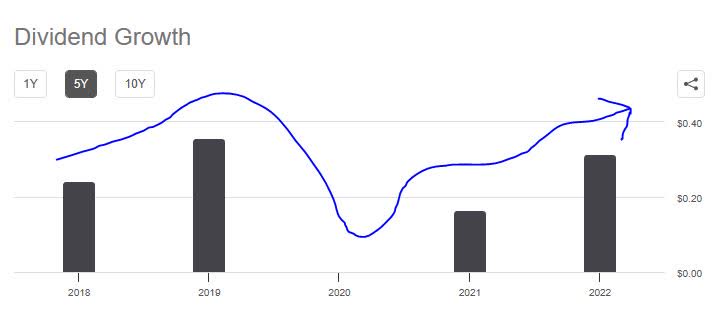

Dividend Yield Above 6%

Notable to mention is that this stock is currently paying a 6.09% dividend yield, as per its most recent dividend data .

However, its dividend of $0.25 per share is semi-annual, not quarterly, which is worth noting.

Additionally, it does not have a steady 5-year dividend growth, as the chart below shows:

Barclays - 5-year dividend growth (Seeking Alpha)

{kind=link}

In comparison, HSBC offers a lower dividend yield at 5.24% and also does not have steady 5-year growth.

In this category, Barclays wins with a yield above 6%, and I would recommend it as a dividend investor looking to add some European bank exposure to a portfolio of existing financial stocks, for diversification within the same sector, particularly if you don't mind investing in an ADR.

A Global Banking Brand in Healthy Financial Condition

Since the Q2 results are not out yet, for this section, we will deep dive into the Q1 results released in late April, as a reference for this discussion.

First, the firm achieved YoY net income growth compared to the same quarter a year ago, as shown in the income statement :

Barclays - Net income (Seeking Alpha)

{kind=link}

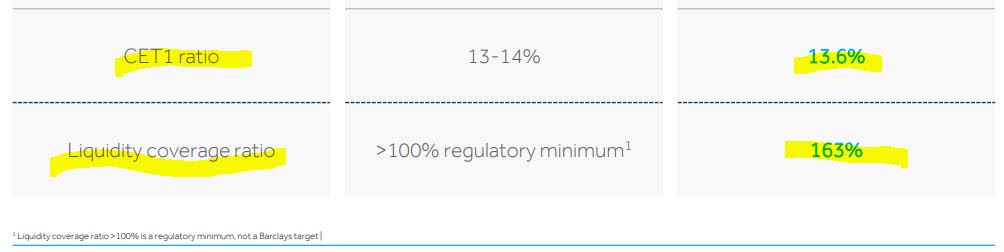

Second, from the firm's Q1 earnings presentation , both the CET1 ratio of 13.6% is within target as well as the liquidity coverage ratio of 163% being well above the 100% regulatory minimum:

Barclays - CET1 and LCR (Barclays - Q1 Presentation)

{kind=link}

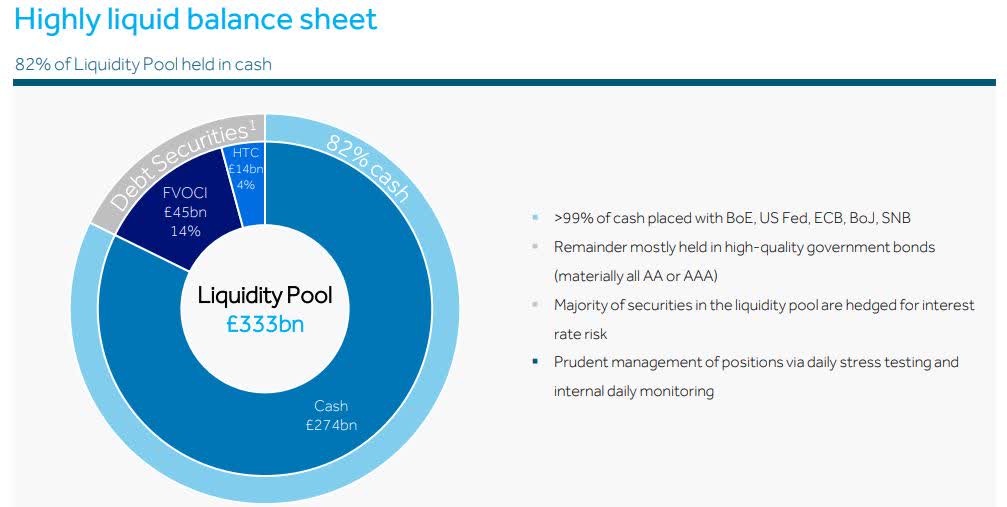

Third, they have presented a highly liquid balance sheet, with 99% of cash held at central banks and the remaining liquidity mostly in govy bonds:

Barclays - Liquidity (Barclays Q1 Presentation)

{kind=link}

Lastly, the scale of Barclays is such that it can tap into a diversified stream of multiple business segments across its entire group.

Consider what the Group Finance Director's review had to say during the Q1 earnings release :

The Group has a diverse income profile across businesses and geographies including a significant presence in the US.

Group income increased 11% to £7,237m primarily from the higher interest rate environment and continued structural hedge income momentum benefiting Barclays UK, transaction banking and the Private Bank, the benefit of higher balances in US cards, and growth in client assets and liabilities in the Private Bank.

Hence, I would recommend this stock in the category of healthy company financial condition.

Macro Factors Continue to Benefit this Firm

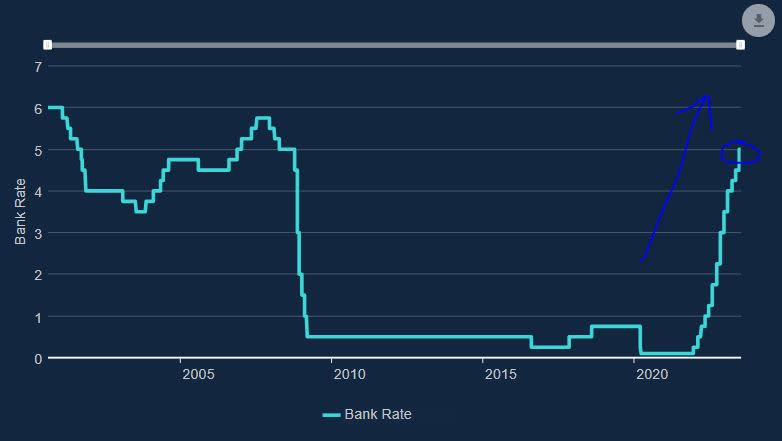

The key factor in the macro environment I can identify that would impact a firm like Barclays would clearly be the interest rate environment, since that is of significance to the banking sector.

For starters, let's look at the Bank of England's chart on rate hikes to its bank rate, which currently is at a peak of 5%, most recently raised on June 22nd:

Bank of England - Bank rate hikes (Bank of England)

{kind=link}

Why should this matter to a firm like Barclays? Because of benefits to its net interest margin.

For instance, the Bank of England explains the scenario very straightforward:

When we raise our interest rate, banks will usually raise the interest rates for both savers and borrowers. But, to cover their costs, banks normally pay less to savers than they charge to borrowers. So there's usually a gap between rates on savings and loans.

As in past banking articles, I have shown that the macro environment of rate hikes by central banks has driven increases in both net interest income as well as net interest margin, and that is true for Barclays as well.

The company stated , for example, that "in 2023, Barclays UK's net interest margin is expected to be greater than 3.20%."

Barclays UK, for example, already showed a significant YoY increase in its net interest margin:

Barclays - NIM growth (Barclays - Q1 Presentation)

It is also notable to mention that there is more good news for Barclays after the Bank of England recently released its stress test results, of which Barclays and HSBC were among the banks to participate.

According to the Bank of England's July 12th announcement :

No bank is required to strengthen its capital position as a result of the test. This indicates that major UK banks would be able to withstand the severe macroeconomic stress in this scenario.

Based on the above evidence I presented, I would recommend this stock in the category of macro factors benefiting this company in a positive way.

Rating Score

Today, I am giving this stock a buy rating, as it won in 4 of my 5 rating categories. My rating is in line with the consensus from Wall Street, as shown below, is less bullish than the consensus from SA analysts, but more bullish than the SA Quant System which gave it a hold rating:

Ratings Consensus (Seeking Alpha)

What kept it from getting a strong buy rating today was its price chart, as mentioned earlier, as I think an investor can get it at a better price at the next dip.

Risks to Our Ratings Outlook

A risk I have identified with Barclays is a report in Reuters this week on July 13th that management is engaging external consultants to do a strategy review and potentially invest more capital in smaller business segments, which drew the ire of major investors who would rather the capital be used for share buybacks to boost the share price.

I think it is a risk to my modestly bullish outlook on this stock, which would benefit from share buybacks more than it would a consultant review and playing a game of dice.

Consider what Jefferies analysts said in a note, as mentioned in the Reuters article :

We estimate the bank ought to be able to generate around 19 billion pounds of profit over the course of 2023-2025, and we believe more of this should be returned to shareholders to better address the share price weakness as opposed to another strategy review.

I think to counter this risk, the bank will have to show investors and analysts that their new strategy will drive significant returns for shareholders.

Analysis Wrap-up

In closing, I reiterate my buy rating on this stock.

Positives include: A competitive dividend yield above 6%, undervaluation, strong company financial condition, and benefiting from the macro environment of central bank interest rate decisions.

Headwinds include the current price chart, which I think can do better for a value investor during the next dip.

A risk identified was management's push to recapitalize smaller business segments rather than deploy capital to more share buybacks, sparking concern among major investors.

Nevertheless, I am adding Barclays to my watchlist of financial sector stocks, as a potential diversifier to my US banks, a solid dividend play, and a chance to own a piece of a well-established brand that was on the 2022 list of global systematically critical banks.

For further details see:

Barclays: 6% Dividend Yield And Undervalued, But Waiting On Next Dip