BCS - Barclays: Buy Rating Retained Conviction Lowered

2023-10-29 08:46:58 ET

Summary

- Barclays delivered a second consecutive quarterly update that rattled the market.

- Comfort regarding the net interest margin outlook for the group’s UK banking business is lacking, with management’s new guidance implying a wide range of potential outcomes for 4Q24.

- Management have flagged a restructure charge in the final quarter of FY23, but investors will need to wait until February 2024 for full details of the cost-out program to emerge.

- Trading at around 41% of NTA, Barclays appears to be very cheap and the price warrants retention of a Buy rating, albeit with reduced conviction.

Introduction

Barclays PLC ( BCS ) released 3Q23 results on 24 October 2023. Back in July 2023, I commented that the market had been unimpressed by the company’s 2Q23 update (the London Stock Exchange ‘LSE’ price fell by 5% on the day of the 2Q release), but the 3Q23 results struck an even more negative chord, pushing the LSE price down by -6.5% (with further subsequent declines). In this note I’ll discuss key aspects of the 3Q23 update that I believe most worried the market. I’ll also consider whether or not a Buy rating can still be supported. After back-to-back quarterly disappointments, I’m sure that a few investors in BCS might be willing to throw in the towel. BCS is currently trading at a staggeringly low price to NTA of just 0.41x – with this metric at such a depressed level, it’s entirely possible that bailing out now could imply leaving a lot of value on the table.

Barclays UK Net Interest Margin Guidance

In late 2022 and early 2023 there were a number of bullish arguments put forward about the huge earnings uplift that BCS was going to enjoy thanks to leverage to higher interest rates, which would be delivered primarily by the Barclays UK division (‘BUK’) net interest margin (‘NIM’). Despite having a Buy rating on BCS at the time, I pushed back on those arguments, as I thought that they were over-simplistic and ignored important factors regarding how banking markets typically behave. Extracts on this topic from my previous notes are set out below. Note that BUK is the group's UK retail and business banking segment.

The assumption that all (or a very high proportion) of this interest rate leverage will fall to the bottom line is optimistic in my view. As with most areas of financial services, competitive pressure remains alive and well in retail and corporate banking markets throughout Europe and North America.

May 2023 :

An interesting issue to consider: what will happen to BUK’s NIM when the upward momentum from higher interest rates fades? Will the competitive tension that is now well and truly alive simply halt, or will BUK’s NIM suffer a decline? I think that there is a good chance that BUK’s NIM will peak in late FY23 and then fall back slightly in FY24.

Whilst my analyst ego has probably enjoyed being on the correct side of the argument regarding the impact of competition on the BUK NIM (albeit that the NIM pressure has come through a little faster than I anticipated), my personal balance sheet has not enjoyed the fall in the BCS share price, and particularly the -10.3% move since the release of the 3Q23 result.

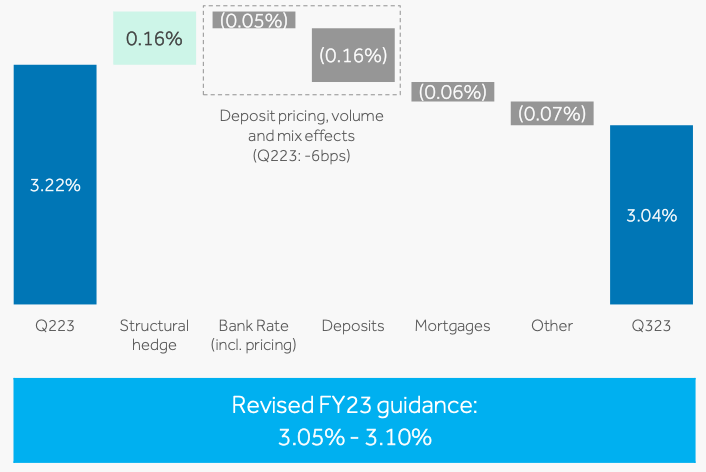

Management guidance for the BUK FY23E NIM was lowered at 3Q23, and now sits at 3.05% to 3.10%. At first read, this sounds like a narrow range, and investors might conclude that there isn't too much to worry about on the BUK NIM outlook front. But given that there is only one quarter of FY23E remaining, the revised guidance range implies a wide gap between management's upper and lower end expectations for the BUK NIM in 4Q23E. The NIM 'bridge' shown in Exhibit 1 tracks the movement in the BUK NIM over 3Q23 - the fact that the NIM could move so rapidly, from 3.22% down to 3.04% is concerning in the context of the updated management UK NIM guidance.

Exhibit 1:

{kind=link}

Comments from CFO Anna Cross during the 3Q23 management speech seemed designed to encourage investors and analysts to lean towards the top end of the new BUK NIM FY23E guidance range:

We now guide to a range of 305 to 310 basis points for the full year. To help frame this, if we see similar trends in Q4 as we did in Q3, both in terms of mix and volume, full year NIM would be towards the top end of this range.

Source: Barclays 3Q23 Management Speech .

Personally, I take little comfort from the CFO's comments. The sharp downward move in the BUK NIM in 3Q23 appears to not have been well anticipated by management, and I am concerned that the CFO may be implying an overly optimistic outcome for the final quarter of the year. (As an aside, the current CEO/CFO team strike me as more inclined to put a positive spin on things than the previous CEO/CFO team, whose commentary I found to be more balanced.)

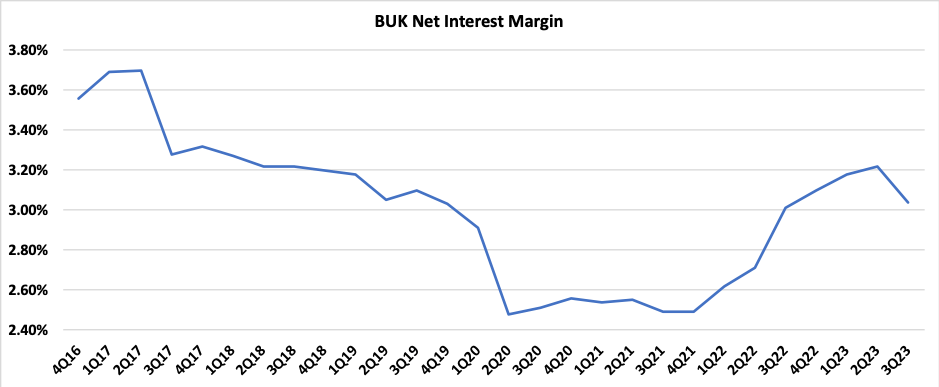

So what does the new BUK NIM guidance imply for the BUK 4Q23E NIM? A number of assumptions are required in order to answer that question, so any answer is going to be slightly rubbery. Doing some very simple math, the guidance implies a range of ~20bp between the top and bottom end of 4Q23E BUK NIM expectations. For valuation purposes I have adopted the lower end of the guidance range, which implies a 4Q23E UK NIM of ~2.75%. Were I to weigh my valuation more towards the 4Q23E scenario referenced by the CFO, I'd be looking at a 4Q23E BUK NIM of ~2.95%. Exhibit 2 below provides a time series for the BUK NIM that helps to put these numbers into a bit more context.

Exhibit 2:

Source: Author’s calculations based on Barclays financial reports.

{kind=link}

Restructure Charge Coming - Quantum Unknown

The 3Q23 management speech closed with an update on the group outlook, which included an unexpected advance warning about potentially material restructure costs in 4Q24E.

We are evaluating actions to reduce structural costs to help drive future returns, which may result in material additional charges in Q4, impacting this year’s statutory performance .

Source: Barclays 3Q23 Management Speech.

I was surprised by the lack of additional detail regarding the coming restructure program and the associated cost savings that will follow. Based on management's comments, investors will need to wait until the FY24 result is announced in February 2024 before these very important details are provided. A management team that is highly regarded by the market and that has earned investor trust can sometimes get away with giving rather vague guidance of this nature. But in the case of BCS, I don't think that this high regard/trust aspect is in play, and so it is natural for many investors and analysts to be concerned about what is coming down the pike.

In the 3Q23 Q&A session, a number of sell-side analysts attempted to draw out the details on the flagged restructure program. In response to an analyst question that referenced the potential for the 4Q23E restructure charge to push statutory 4Q23E earnings into loss making territory, the CFO offered the following reply:

I understand the maths of what you're putting in front of me. I'm going to say the same thing, that we have not yet concluded on those plans. To the extent that we do, we will update the market further at full-year, both in terms around the costs, but also the ongoing impact that we would expect them to have.

Source: Barclays 3Q23 Q&A Transcript , page 6.

It strikes me as somewhat bizarre that BCS management have left the market hanging in this manner. If the restructure plans are still nowhere near complete, or if the likely cost is going to be modest, why say anything at all? I think that the logical thing for an investor to do in this situation is to assume a hefty restructure cost in 4Q23E. I can't say with any confidence what that number might be, but a pre-tax cost of at least £500m seems quite likely. As to the ongoing cost savings that will be secured by the restructure costs, there's simply not enough detail to hazard a guess.

Investment Banking Restructure Coming?

We don't have to go back far into history to see the benefits of the diversification of BCS business lines. In the early days of the Covid pandemic, retail banking earnings were under massive pressure due to plummeting interest rates and locked down businesses and consumers, but BCS was still able to deliver income growth in FY20 thanks to a very strong performance from the investment banking business. Prior to the pandemic, a well-known activist investor pushed BCS to offload the investment banking division - in retrospect that would have been a big mistake, and it was fortunate for shareholders that the BCS board resisted the pressure . But once an idea is out in the market, it tends to linger.

Operating conditions for the investment banking business have softened since the boom-time period during the pandemic. Although it was entirely predictable that investment banking and global markets earnings would normalize, this softening may well encourage activists to start making noises once again about this segment’s capital intensity and lower RoNTA. It might not only be external activists that such noises could emanate from. Indeed, comments from CEO CS Venkatakrishnan during the 3Q23 Q&A session suggest that management and the board are paying attention to how the market values different types of banking operations, and I’m pretty confident that consideration regarding the investment banking business influenced the CEO’s words.

I also said in New York it's very, very clear that the market values different businesses differently. Right? And we obviously have to take that into account in the way in which we think about our capital allocation.

Source: Barclays 3Q23 Q&A Transcript, page 3.

Personally, I think that the CEO's view here is very questionable, if not plain wrong. Management and the board should be focussed upon the underlying economics when making capital allocation decisions, and not upon implied market multiples (which can move around over time, and which are clearly external factors that management and the board cannot control).

Summary & Conclusion

During the time that I have been writing about BCS on Seeking Alpha, I've commented several times that I see BCS as a high-quality bank. The benefit of diversified income streams contributed towards my past commentary regarding the group's quality, but I also felt that management's understanding of the business and decision making were solid. Whilst I continue to see benefits from BCS having a well-diversified structure, I struggle to maintain a high level of confidence regarding the current management team. The CEO's comment referred to above regarding capital allocation decisions is one example of situations where the CEO or CFO have made remarks that have left me scratching my head. I've also been disappointed that management appears to have failed to properly assess the potential range of outcomes for the UK NIM, and to communicate such to the market. The lack of detail provided in 3Q23 regarding the imminent restructure charge and associated cost savings is another example of a disappointing lack of clarity from management.

I can therefore no longer justify applying the label 'high-quality' to BCS. This leaves me in a slightly uncomfortable position regarding my stock rating. From a valuation perspective, using my normalized earnings valuation framework, BCS looks very cheap. However, given concerns regarding management quality, I lack conviction regarding the eventual delivery of this underlying value. I downgraded BCS from Strong Buy to Buy in late July 2023, and despite the subsequent material price fall, I do not see grounds to reverse that downgrade. On balance, relying mainly on valuation support, I am currently willing to retain a Buy rating on BCS (based on a 27 October 2023 LSE closing price of 129.20p).

For further details see:

Barclays: Buy Rating Retained, Conviction Lowered