BCS - Barclays: Macro Risks Weigh Buybacks Help Shares Are A Value

2023-10-13 14:20:36 ET

Summary

- UK stocks have performed well despite a strong US dollar, with the iShares MSCI United Kingdom ETF outperforming the S&P 500 in the last year.

- Barclays, one of the largest Financial sector holdings in the ETF, has a low valuation, high yield, and potential net income growth turnaround story in 2024.

- The stock's technical chart shows resistance just above the current price, but it is a classic value play with a decent yield in my view.

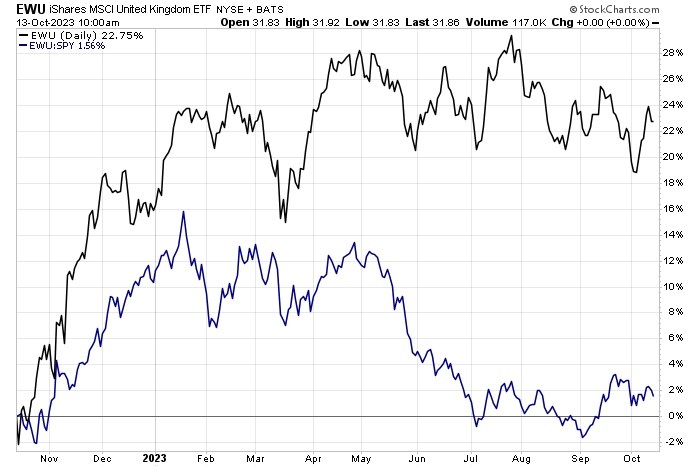

UK stocks have held their own in recent months despite a surging US dollar. The iShares MSCI United Kingdom ETF (EWU) is up 23% total return in the past year, actually outperforming the S&P 500. While relative strength has waned since hitting an early-year high, EWU has remained a decent regional performer since the start of the second half.

One of the fund’s largest Financial sector positions, Barclays ( BCS ), has not been as strong, though. Still, I have a buy rating on the bank for its low valuation, high yield, buyback program, and potential net income turnaround story in 2024.

UK Stocks Performing Well Despite A Firm Greenback

{kind=link}

According to Bank of America Global Research, Barclays is a "transatlantic" universal bank focused on UK retail and commercial banking, investment banking, and US credit cards. It offers financial services, such as retail banking, credit cards, wholesale banking, investment banking, wealth management, and investment management services.

The London-based $28.1 billion market cap Diversified Banks industry company within the Financial sector trades at a low 4.2 trailing 12-month GAAP price-to-earnings ratio and pays a high 3.6% dividend yield. Ahead of earnings later this month, shares trade with a moderate implied volatility percentage of 36%.

Back in July, the firm reported a soft net interest margin of 3.15%, below the 3.2% figure mentioned in previous guidance. High inflation in the UK, intense competition, and overall weak growth given the environment of an inverted yield curve and cold capital markets were no doubt detractors to overall performance.

Longer-term, however, rising interest rates should be a boon for the bank. Profit before tax for the quarter fell sequentially to £1.96B from £2.60B, and EPS declined 24% from year-ago levels. Total deposits were mostly unchanged from Q1. These will be some of the key metrics to watch in the quarter about to be reported. Also keep your eye on BCS’s balance sheet – its CET1 ratio came in at 13.6%, down from 13.9% as of the end of 2022.

Bigger picture, Barclays continues to face headwinds from its business mix, namely its investment banking segment, given the dearth of dealmaking lately. Recent weak IPOs in the US do it no favors, either. What’s favorable is that there is a significant share repurchase plan ( £ 750 million) that helps shareholders during this tough stretch. Better profitability will need to commence in order for continued stockholder accretive actions to persist – that is a key risk, including macro factors such as the interest rate and inflationary conditions as well as consumer trends.

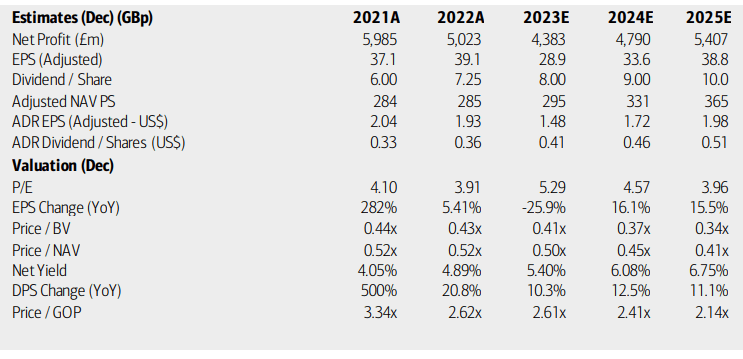

On valuation , analysts at BofA see earnings falling about 26% this year, but per-share profits are then expected to bounce back sharply in 2024 with continued growth in 2025. The consensus outlook is on par with what BofA sees, per Seeking Alpha’s figures. Dividends, meanwhile, are expected to climb at a steady pace over the coming quarters. With single-digit P/E ratios and a potentially rising yield, the bank, like so many in the Financial sector, appears attractive.

Barclays: Earnings, Valuation, Dividend Yield Forecasts

{kind=link}

Along with a mid-single-digit earnings multiple (sharply below the stock’s 5-year average), Barclays sells for less than 0.5 times book value on a trailing basis. If we apply just a 6x P/E and a conservative P/B of 0.6x, then shares should be near $10 using a blended approach. Moreover, shareholders can capture a solid dividend yield along the way.

BCS: Compelling Valuation Metrics

Seeking Alpha

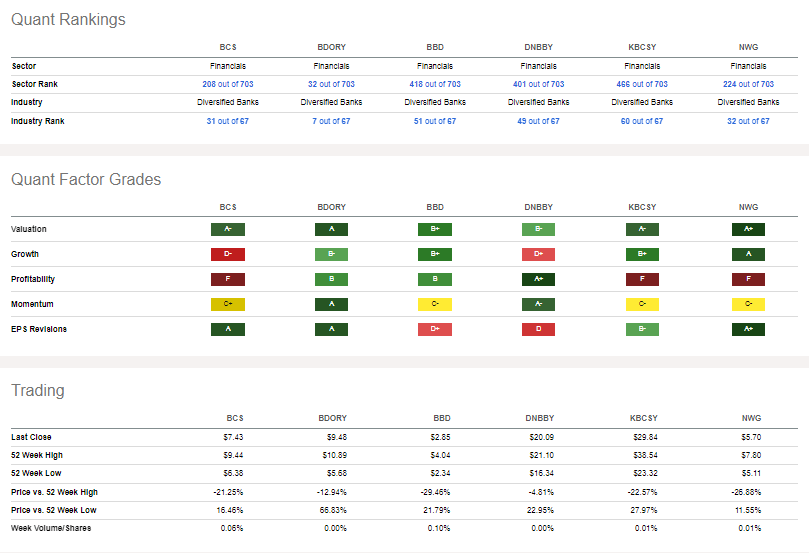

Compared to its peers, Barclays’ valuation is not as compelling as some other large banks, trading at cheap earnings multiples and price-to-book ratios. The growth grade is poor, but that is largely a reflection of the recent past. If better earnings materialize, then the stock’s overall quant factor ratings will look better in the quarters ahead. But with recent earnings trending lower, we need to see definitive signs of a positive EPS inflection to improve profitability , though EPS revisions have been very strong lately. Still, share price momentum has been weak for much of this year, which I will detail later.

Competitor Analysis

{kind=link}

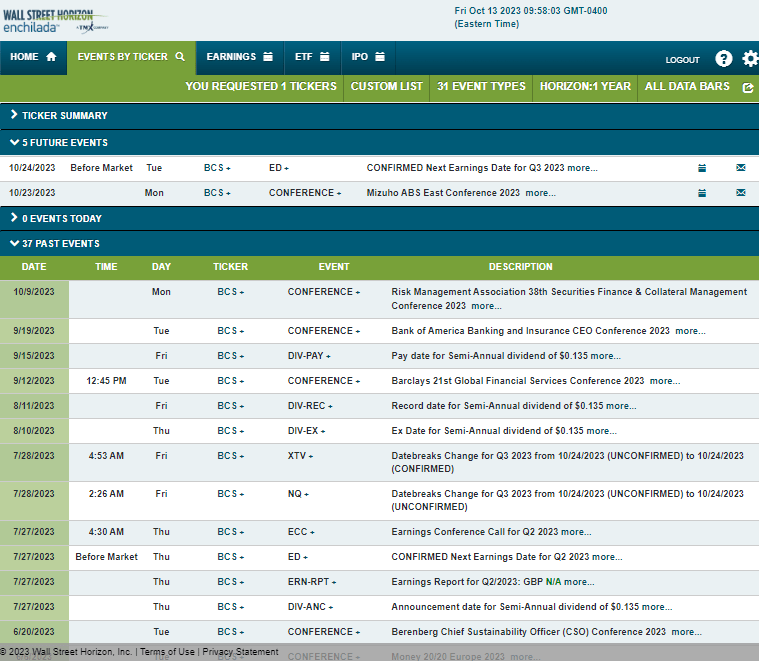

Looking ahead, corporate event risk data provided by Wall Street Horizon show a confirmed Q3 2023 earnings date of Tuesday, October 24. Before that, the bank’s management team is scheduled to present at the Mizuho ABS East Conference 2023, so be on the lookout for potential volatility later this month from the 23 rd to the 25 th .

Corporate Event Risk Calendar

{kind=link}

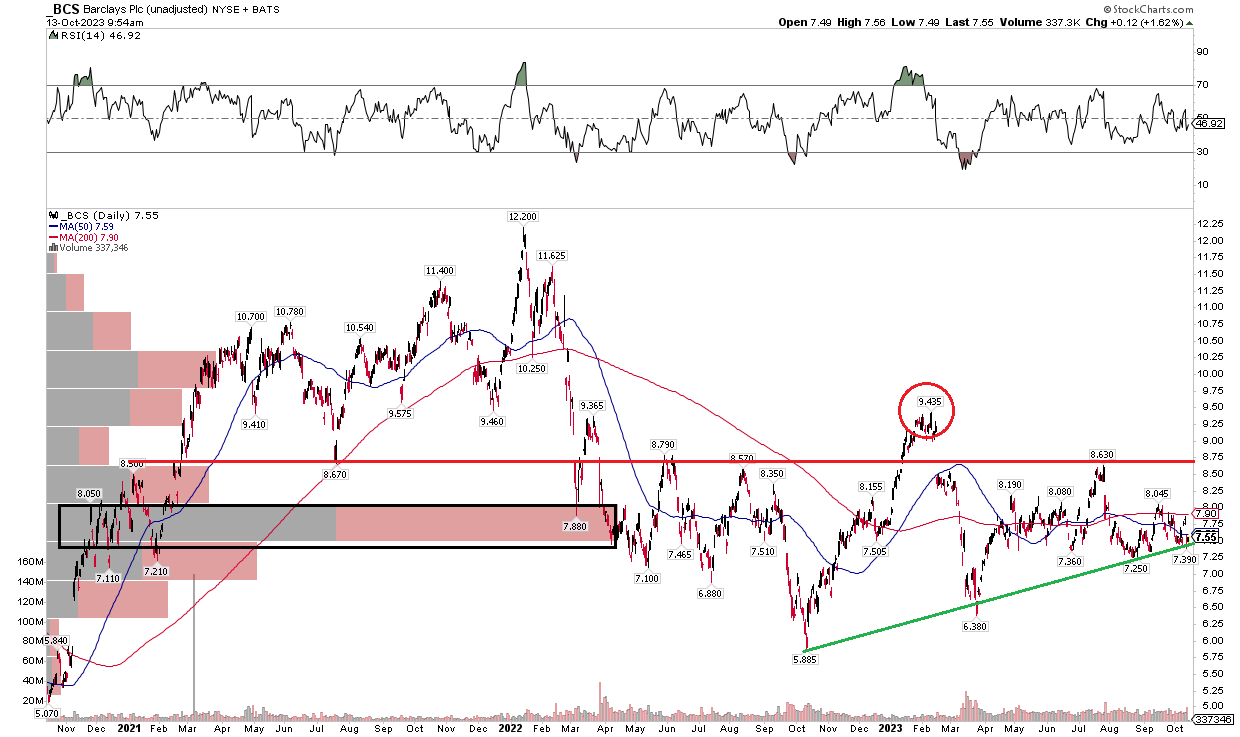

The Technical Take

Barclays has endured a tough stretch since the broader market turned lower in early 2022. Notice in the chart below that shares have stabilized, however, between $7 and $9 lately. I see important resistance in the $8.50 to $8.80 range – BCS did climb above that in a false breakout move in January and February, but the stock took a nosedive during the banking turmoil in March.

Also take a look at the long-term 200-day moving average – it is very flat and the 50dma is bouncing back and forth above and below the long-term trend indicator line. The bulls can point to a series of higher lows off the October 2022 trough below $6, and it appears near-term support between $7.25 and $7.40 is shaping up. Finally, there’s a high amount of volume by price in the $7.50 to $8 zone, right where BCS trades today.

Overall, it is a neutral chart at best, and I would like to see shares climb above the July peak to help support the technical case of a turnaround.

BCS: Higher Lows, But Key Resistance In-Play

{kind=link}

The Bottom Line

I have a buy rating on BCS. The technical picture is not impressive by any means, but it’s an inexpensive bank with a decent yield. Growth investors may want to dismiss this one, but Barclays appears as a classic value play in my view.

For further details see:

Barclays: Macro Risks Weigh, Buybacks Help, Shares Are A Value