BCS - Barclays: Updated Guidance Triggers Downgrade To Buy

2023-07-30 05:48:27 ET

Summary

- The market was disappointed by updated management guidance for the FY23E UK net interest margin.

- A weaker performance from the investment banking segment added to investor negativity.

- Bad debt loan loss rates remain low, although higher credit costs are expected in the second half of the year.

- The stock is cheap, trading at around 54% of NTA, with a healthy dividend yield of over 5% and a refreshed buyback program, but concerns regarding the nearer-term outlook trigger a downgrade from Strong Buy to Buy.

Introduction

Barclays PLC ( BCS ) released 2Q23 results on 27 July 2023. The market was clearly unimpressed by the company’s quarterly update, with the Barclays’ London Stock Exchange price falling by almost 7% during the session, and closing the day down ~5% at 155.56p. After the fall, Barclays share price is now back at around the level at which I last published a Strong Buy call in early May 2023. In this note I’ll look over the 2Q23 materials, discuss new positive and negative factors that are relevant to the Barclays investment case and consider whether or not the market’s reaction to the update is a sign that my bullishness on the stock ought to be dialled back.

2Q23 Positives

Key positives reported in the 2Q23 materials are summarized and discussed below:

- Barclays delivered a 2Q23 RoTE (return on tangible equity) of 11.4%, ahead of the FY23E target of >10%. The 1H23 RoTE was a solid 13.2%. The fact that Barclays is trading at a discount of almost 50% below TNAV (tangible net asset value per share, or NTA) suggests that the market does not believe that the level of profitability seen in 1H23 is sustainable.

- The group’s investment banking segment, Corporate and Investment Bank “CIB” is performing very well on a market share basis, achieving fee share rankings of number one in the UK, number two in Germany and number six globally.

- Regulatory capital is strong, with a CET1 ratio of 13.8%. This provided capacity for an increased dividend of 2.7p, up 20% on pcp, and the launch of a £750m buyback program.

- Operating expenses in 2Q23 were ~5% lower than 1Q23, consistent with management’s prior commentary that the first quarter of 2023 would represent a high point for FY23E operating expense levels.

- The bad debt loan loss rate came in at just 37bp for 2Q23, well below the previously guided range for FY23E of 50bp to 60bp. That said, management are still anticipating a FY23E bad debt loan loss rate of 50bp to 60bp, implying that credit conditions are expected to deteriorate in the second half of the year.

2Q23 Negatives

Key negatives reported in the 2Q23 materials are summarized and discussed below:

- Investment banking earnings were down materially on both the sequential quarter and the pcp. In prior Seeking Alpha notes on the Barclays I have pointed to the fact that CIB has been over-earning in the global markets area; whilst many analysts will have reacted negatively to the 2Q23 CIB numbers, my investment case for the company was already factoring in a downward normalisation.

- The group’s UK segment, Barclays UK “BUK” reported a NIM of 3.22%, up on the 1Q23 read of 3.18%. However, the downward revision for the FY23E BUK NIM from ‘at least 3.20%’ to ~3.15% caught the market by surprise. I will look more closely at this issue further below.

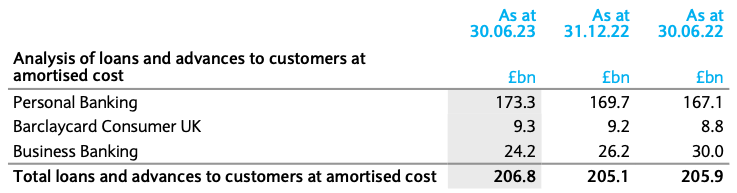

- The BUK loan book is growing very slowly. In fact, if we exclude the £2.2bn of mortgages added by the KMC acquisition, the BUK loan book actually reduced by -0.2% in the first half of 2023. Business banking loans have fallen by almost 20% since 30 June 2022; this is largely due to businesses paying off government-backed Covid-19 loans. Of the reduction of £2bn in BUK business banking loans over 1H23, ~£1.3bn related to government-backed Covid-19 loan repayments. Approximately $6bn of government-backed Covid-19 loans remain on the balance sheet, so this headwind to loan growth will continue for several more quarters.

{kind=link}

Barclays UK Net Interest Margin Disappoints Market

Over the last year or so, a common theme of many Barclays bull cases has been that the group’s ‘structural hedge portfolio’ would drive massive expansion in the reported NIM (with around 2/3 of the expected NIM benefit to emerge in the BUK division). In my previous Barclays work I have explained that it is important to maintain a balanced view about the potential upside for NIM expansion from higher interest rates, and that natural market competitive tension (which comes through via pricing of both loans and deposits) will offset much of the positive impact delivered by the structural hedge portfolio. In May 2023, I wrote the following:

I also follow the Australian banking sector – competitive pressures Down Under are already leading analysts and investors in that market to conclude that ‘peak margin’ has already passed. From my perspective, it is only a matter of time before BUK passes through its own peak margin.

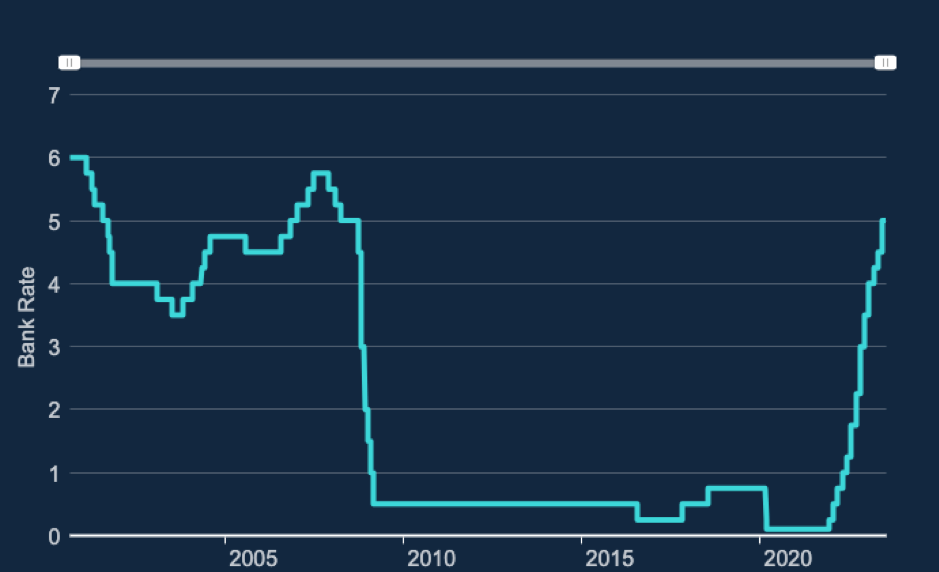

The 2Q23 results points to BUK having perhaps already passed through its peak margin point. This has occurred slightly earlier than I had anticipated, and has almost certainly been a major driver of the market’s negative reaction to Barclays’ 2Q23 numbers. At the end of 1Q23, management guided to a FY23E BUK NIM of ‘greater than 3.20%’, with this guidance based on assumption that the UK Bank of England Bank Rate would peak at 4.25% in 2023.

Exhibit 1:

{kind=link}

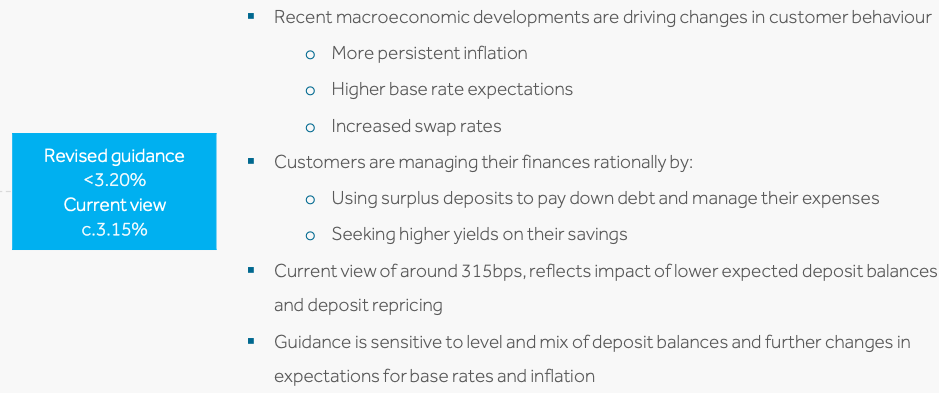

As highlighted in Exhibit 1, the UK Bank Rate has quickly blasted past the 4.25% peak assumption on which the 1Q23 guidance was based; it would therefore not have been unreasonable for investors and analysts to have expected a potential uplift in the BUK NIM guidance at 2Q23. The outcome of course was the opposite – Barclays are now guiding to an expected BUK NUM of 3.15%, implying a NIM for 2H23E of around 3.10%. Exhibit 2 highlights the new BUK NIM guidance, and shows the factors that Barclays say have contributed to the downgrade.

Exhibit 2:

{kind=link}

It is not unreasonable to wonder how management could get things so wrong in regard to the BUK NIM outlook. It is important to remember that a bank’s NIM will be affected by a range of internal and external factors, many of which are difficult or impossible to forecast with confidence. In retrospect, I’m sure that that management will wish that they had put forward the 1Q23 guidance of ‘greater than 3.20%’ with a few more caveats, and I think that the CEO and CFO can fairly be criticized for not doing so. However, as discussed above, my own work and that of others in the market has highlighted the fact that BUK’s NIM would eventually start to head downwards – in this context I do not see the revised FY23E BUK NIM guidance of ~3.15% as totally unexpected or dire news.

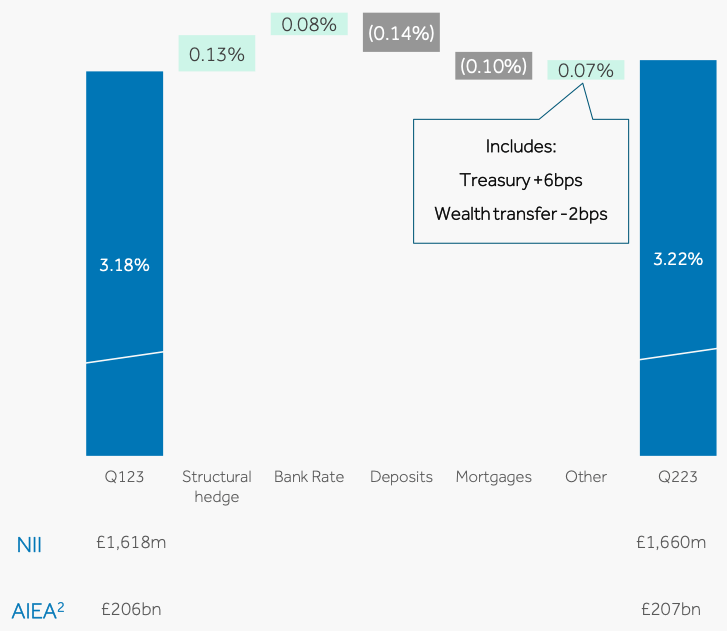

UK banks have recently been asked by the Financial Conduct Authority to justify low interest rates on certain savings accounts. The involvement of the regulator along with increasing media attention and political commentary regarding the issue is putting pressure on UK banks to increase interest rates on deposits. In addition, customer behaviour is finally starting to change, as people become more aware of and sensitive to the opportunity cost of leaving deposits in low interest paying accounts. With continued inflation driving up living-costs, the benefit that banks have enjoyed from ‘lazy deposits’ is now clearly fading. Exhibit 3 below shows that the combined effect of business mix and pricing for deposit and loan products was materially negative for BUK’s NIM in 2Q23. Indeed, the -0.14% contribution from deposits alone more than outweighed the +0.13% benefit from the structural hedge.

Exhibit 3:

{kind=link}

Bad Debt Loss Rates – Watching Closely

Arrears rates for the group’s UK and US credit card books are still not yet showing signs of significant customer stress. The rapid increase in US credit card 30-day arrears that caught my eye at 1Q23 has eased, but I will be monitoring the US book closely in coming quarters. Management have consistently referenced the maintenance of cautious settings in regard to new UK credit-card customer acquisition over recent years, and I feel reasonably confident that BUK’s credit card book will avoid a blow-out in the case of a UK recession.

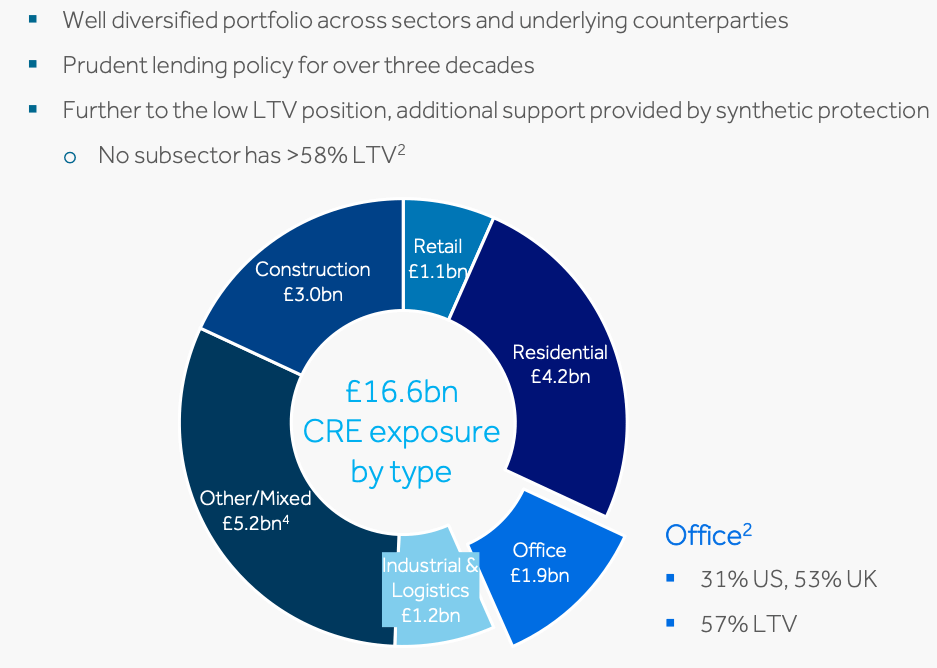

For seasoned bank investors, commercial real estate is always front of mind when it comes to thinking about downside bad debt loss risk during recessions. In the current environment, the office sector is an obvious area of concern, and I would also argue that property valuations for certain logistics and industrial segments are likely to come under pressure (given that the run-up in valuations since the pandemic is likely to reverse). The good news for Barclays investors is that the bank has a low balance sheet exposure to commercial real estate, at ~4.7% of total group loans and advances. Exhibit 4 provides an overview of the group’s commercial real estate exposure. Construction is a segment that can often drive material bad debt losses, and so I take some comfort from the fact that Barclays has less than 1% of its loan book exposed to this sector.

Exhibit 4:

{kind=link}

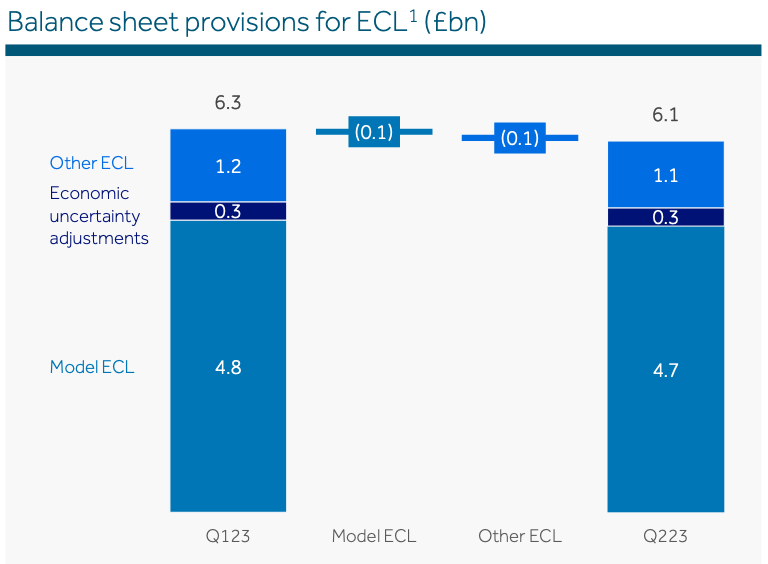

Given my sense that the outlook for the US and UK economies is far from positive, I was slightly disappointed to see Barclays reduce balance sheet provisions for bad debts during 2Q23 (refer Exhibit 5). Whilst the economic indicators that feed in to the bank’s provisioning models have improved very slightly (notably forecasts for GDP and unemployment), I would prefer to have seen Barclays utilise ‘management adjustments’ to retain a higher levels of downside protection. Given the clear message from the CFO that bad debt loan loss rates will increase during the second half of the year, investors should expect to see a build in provisions at the 3Q23 update.

Exhibit 5:

{kind=link}

Conclusion & Rating

Barclays is likely to appeal to the income-focussed investors. Based on the recent announcement of a 20% increase in the first-half dividend, I expect the total FY23E dividend to be at least 9p per share. With Barclays currently trading at ~155p, the implied dividend yield is ~5.8%.

Whilst my valuation analysis points to a Strong Buy being justifiable, I am mindful that there are several negative earnings-related factors that will influence market sentiment over the coming quarters. Bad debt loan loss rates will increase, competitive tension in the UK retail banking market may ramp up further and conditions for Barclays’ investment banking operations appear likely to be less supportive of earnings growth than in recent years. My valuation includes explicit allowances for each of these three factors - normalisation of bad debt loan loss rates, a reduction in BUK’s profitability, lower investment banking earnings – and I feel confident that on a medium-term basis Barclays is excellent value at around 155p per share (equating to ~54% of TNAV). However, history suggests that cheap stocks can get even cheaper during periods when earnings are under pressure and there is a lack of positive catalysts. I therefore conclude this review with a downgrade of BCS from Strong Buy to Buy.

For further details see:

Barclays: Updated Guidance Triggers Downgrade To Buy