BCS - Barclays: Was The Recent Rally Justified?

2024-01-10 12:27:33 ET

Summary

- Barclays has struggled in 2023 along with other UK banks and European peers due to compressed NIM and higher funding costs.

- The bank reported disappointing 3Q results, with net interest income and net fee income dropping slightly from the previous quarter.

- Barclays plans to implement cost cuts and aims for an RoTE of greater than 10% in 2023 but faces macro headwinds and a weakening deposit base.

Barclays (BCS) has struggled in 2023 along with most other UK banks and underperforming European peers as NIM compressed with higher costs of funding. Barclays shares rallied about 25% from the October/November bottom as global yields retreated. As we've noted in our Western Alliance Bancorp. (WAL) and Zions Bancorp. (ZION) articles, banks have undergone significant repricing due to lowering of cost of equity from a 100bps move in U.S. 10-year yields. But, a tide lifting all boats may only work for a short period of time before fundamentals kick back in. Barclays faces macro headwinds with a weakening deposit base despite cheap valuations.

Disappointing 3Q results

Net interest income took a dip to £3.25B (US$3.96B) from £3.27B of the prior quarter but increased from £3.07B in 3Q22. Net fee, commission, and other income of £3.01B dropped from £3.02B in the previous quarter and gained from £2.88B a year ago.

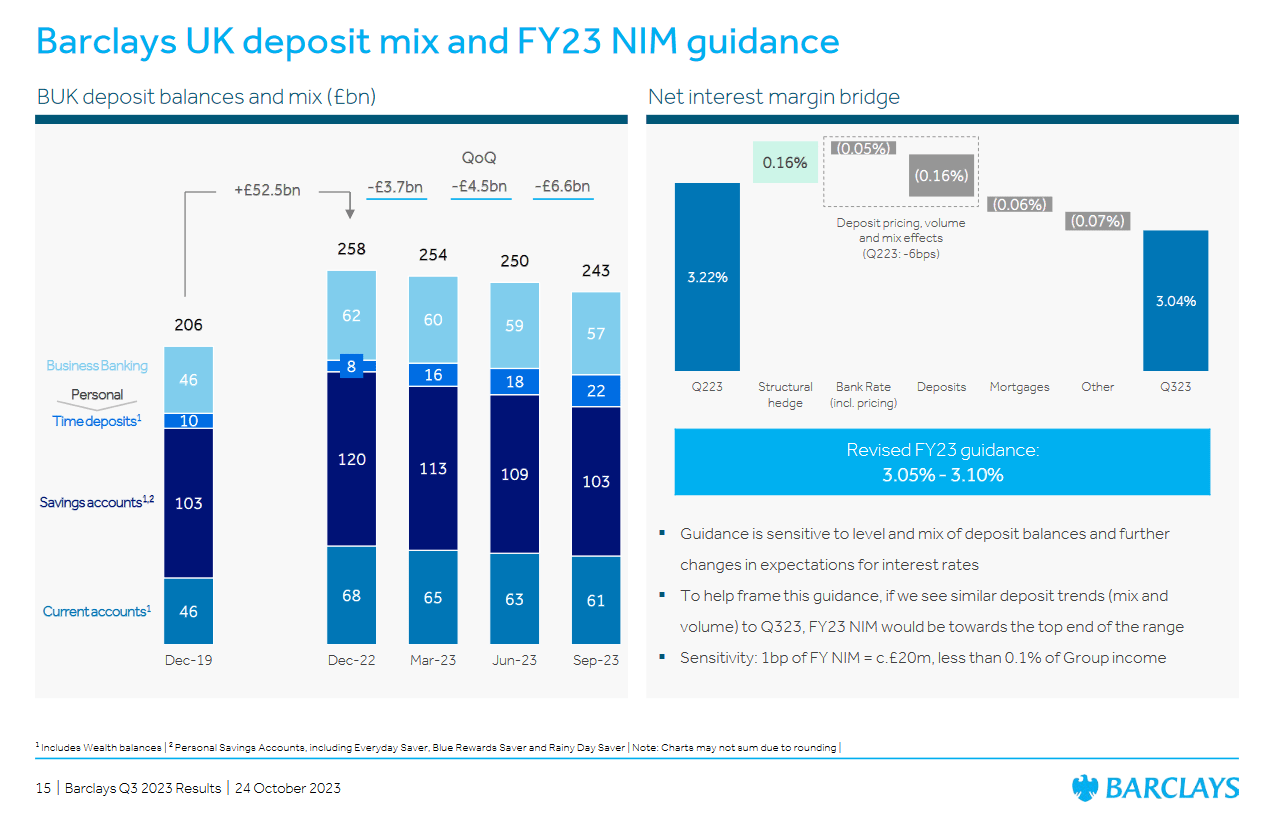

Barclays UK net interest margin was 3.04% in 3Q23, falling 18bps compared to 2Q23 but gained 3bps year-over-year.

Operating costs continued to be high in 3Q22 at £3.95B which was an increase from £3.92B in 2Q23 and £3.94B in 3Q22.

Loan loss rate of 42bps grew from 37bps in the prior quarter and 36bps year-over-year.

Average RoTE during the quarter slipped to 11.0% from 11.4% in Q2 and 12.5% in 3Q22.

Big cost cuts and forward ROE guidance

The company warned of restructuring/big cost cuts while guiding for an RoTE of greater than 10% in 2023, excluding restructuring costs. In a recent announcement, management expects to reduce its annual operating expenses by 7% which equates to £1.05B of savings. This will be mostly focused on staff costs which have run up to £2B annually.

UK NIM is expected to be 3.05%-3.10% for full year 2023 which is a slight lift to 3Q22 number of 3.04%.

Loan loss rate will reach 50bps-60bps through the cycle which is elevated from prior quarters.

The company expects to continue to operate within the CET1 ratio target range of 13-14%.

Deposit mix and trend are still headwinds

Barclays UK has had a net deposit outflow since 4Q22 (three consecutive quarters) while time deposits which carry higher rates are growing as a percentage. Time deposits were 12% of total deposits in 3Q23, up from 10% in 2Q23. Overall, deposits declined 3% q/q or 6% YTD.

Its NIM compression was due to higher costs in deposits partially offset by structural hedges. These are hedges against interest rate rises using GBP rate swaps so it may prove ineffective if BoE cuts rates in 2024.

{kind=link}

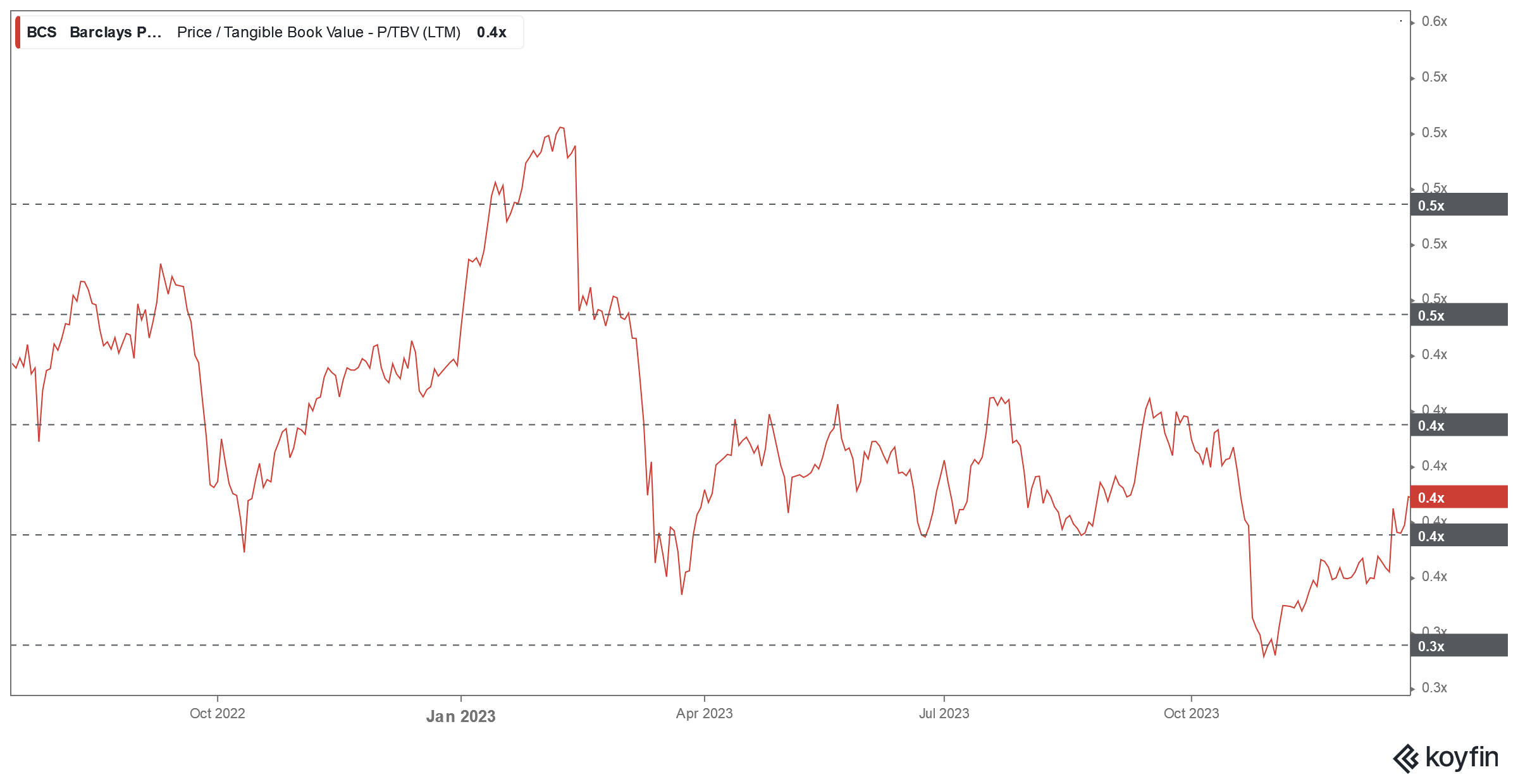

Valuation: Cheap but headwinds do exist

Barclays is currently trading at about 0.4x tangible book value with an RoTCE target of 10% in 2024. Consensus forward ROE is also in the 9-10% range with forward dividend yield at about 2.9%.

Given the forward ROE profile, the bank should be trading at 0.8x-1.0x book value range during better times, but macro headwinds are strong while the company itself is losing competitiveness via loss in deposits to other banks, including virtual banks which have seen massive growth in the retail segment.

The UK is experiencing an economic slowdown with 3Q GDP down 0.1% q/q compared with 1.2% q/q growth in the U.S, but in-line with the eurozone's 0.1% q/q decline.

The Bank of England is poised to follow the Fed in cutting rates in 2024. The banking sector as a result has rallied tremendously as long rates were repriced. Headline inflation in the UK is about 3.9% while the interest rate is 5.25%. This gives the central bank room to cut rates which should help boost the economy, but unless rates are cut by more than 1.5% in a year, the financial conditions will still be restrictive.

Thus, we are neutral as the stock has weak fundamentals that are working against it but this is partially offset by cheap valuations.

{kind=link}

For further details see:

Barclays: Was The Recent Rally Justified?