UNH - Baron Durable Advantage Fund Q1 2023 Shareholder Letter

2023-05-25 12:33:00 ET

Summary

- Baron is an asset management firm focused on delivering growth equity investment solutions known for a long-term, fundamental, active approach to growth investing.

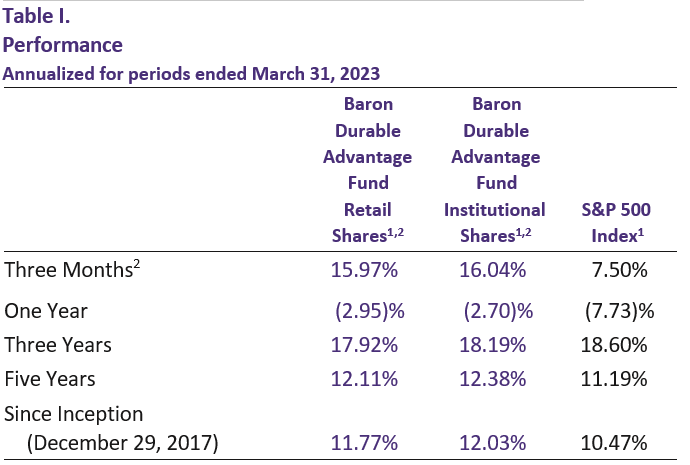

- Baron Durable Advantage Fund gained 16.0% during Q1, which compared favorably to the 7.5% gain for the S&P 500 Index, the Fund’s benchmark.

- At the risk of being accused of succumbing to confirmation bias, the first quarter demonstrated once again how little value there is in trying to forecast the market, let alone in attempting to position a portfolio to align with those forecasts.

- Turning to individual investments, we had a whopping 27 contributors versus just 4 detractors.

Performance

We had a good start to the year.

Baron Durable Advantage Fund® (the Fund) gained 16.0% (Institutional Shares) during the first quarter, which compared favorably to the 7.5% gain for the S&P 500 Index (the Index), the Fund's benchmark.

{kind=link}

|

At the risk of being accused of succumbing to confirmation bias, the first quarter demonstrated once again how little value there is in trying to forecast the market, let alone in attempting to position a portfolio to align with those forecasts. The year began with many pundits' expectations of doom and gloom in the midst of a historically aggressive Fed tightening cycle. Because 2022 was by far the worst year for equities (and most other financial assets) since the Great Financial Crisis ((GFC)) in 2008, we found it hard to tell how much of this doom and gloom was already being priced in. While business activity continued to slow in the first quarter of 2023, and many companies reported challenging environments and lowered guidance for the year ahead, the market seemed to have found its footing and the Index rose 6.3% in January of 2023. The Fund also performed well during the month with a gain of 10.1%. On February 2, the most watched technical indicator, the Golden Cross, provided the ultimate buy signal, and momentum investors piled on. That was the top. Then came the January jobs report showing an increase of 517,000 jobs and a drop in the unemployment rate to 3.4%, a 53-year low! Since we are still in the good-news-is-bad-news world implying more rate hikes ahead, the market went down with the Index losing 2.4% in the month of February. The Fund held up a little better, declining 1.5% for the month. On March 9 we witnessed the collapse of Silicon Valley Bank (SIVBQ), the 16th largest bank in the U.S., followed by the Swiss government-induced takeover of Credit Suisse by UBS for pennies on the dollar. Also, on March 9, the 200-day moving average of the Index, another widely used market indicator, broke down, sending a "sell-all" signal to the investing public. Forty-eight hours later the market turned around and went back up. The Fund gained 7.1% in the month of March, besting the 3.7% gain for the Index, and finished the quarter up 16.0% - a good start from both the absolute and relative perspectives.

In terms of performance attribution, stock selection drove 780bps of the Fund's 854bps relative gain, or just over 90%. Historically speaking, stock selection has often driven the Fund's returns, but we cannot recall another instance (i.e., another quarter) when stock selection contributed positively in every sector to which we allocated capital. The effect of sector allocation was responsible for the remaining relative gains.

Communication Services, Financials, and Information Technology ((IT)) represented 71.4% of the portfolio on average and were our three best performing sectors, generating 633bps of relative gains. Interestingly, Financials, at 30% of the Fund, was by far our largest overweight sector (we picked a great time, right?) relative to the Index, costing us 187bps. We were, however, in mostly the right names and just a few of the wrong ones, which added 396bps of alpha, netting us a neat 209bps of overall contribution to quarterly returns. Not having any investments in Energy, Utilities, Real Estate, or Materials added another 127bps.

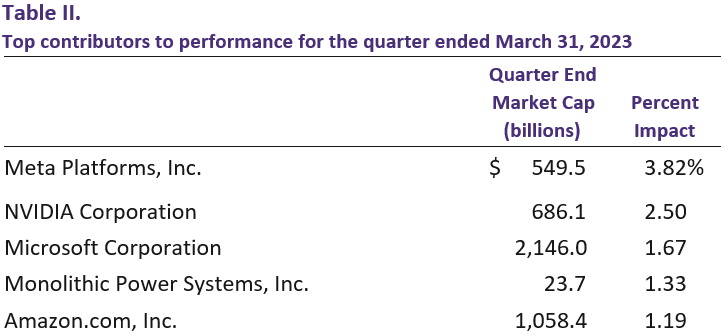

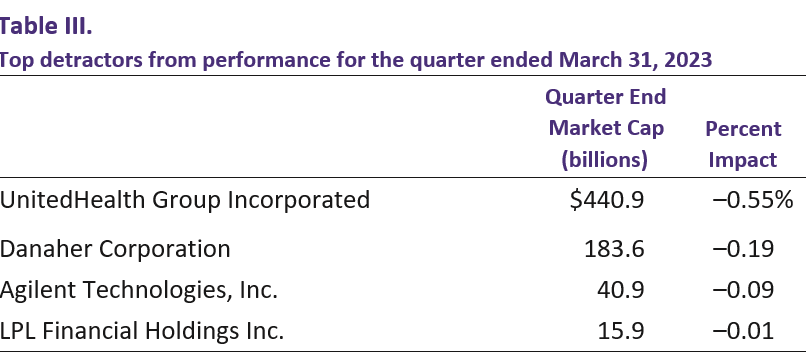

Turning to individual investments, we had a whopping 27 contributors versus just 4 detractors. While 2022 was unkind to equity investors and our shareholders alike, we took advantage of the significant sell-off to initiate positions in NVIDIA ( NVDA ) and Amazon ( AMZN ) , and to add meaningfully to our investments in Meta ( META ) , Microsoft ( MSFT ) , and Monolithic Power Systems ( MPWR ) . These top five contributors generated over 100bps each, and added 1,052bps combined to absolute returns. Fifteen out of our 27 contributors saw their stock prices rise double digits, with 8 investments contributing over 50bps each, and 22 holdings adding at least 20bps each. On the other side of the ledger, UnitedHealth (UNH) and Danaher (DHR) were the only two detractors of note, costing the Fund 55bps and 19bps, respectively.

"Change is always around the corner.… When you see it coming, you have to embrace it. And, the companies that do this well over a long period of time usually succeed." - Andy Jassy, CEO of Amazon (from the shareholder letter dated April 2023)

Although the concept is hardly original (it was Charles Darwin who famously said that it is not the strongest, nor the most intelligent species that survives, but the one most adaptable to change), its application to the world of business and investing strongly resonates with us. We have written in the past about how we expect the transformation to the "digital" economy to bring about a rapid acceleration in the rate of change , making adaptability more important than ever. Some, including us, refer to it as the Kurzweil effect (after the famed American inventor Ray Kurzweil, who wrote at length about it in the early 2000s). Most recent examples range from the proliferation of ChatGPT, which reached 1 million users in five days after launch and 100 million in two months (it took TikTok nine months and Instagram 2 1 ?2 years to reach the same milestone), to the recent bank run on steroids culminating with the collapse of SVB. One day SVB's stock was trading at $267, with a market cap of $16 billion. Two days later it was worthless, as clients tried to withdraw $42 billion in deposits in a span of 24 hours (an astounding rate of almost $500,000 per second). For comparison, the biggest recorded bank run during the 2008 GFC had clients pulling $17 billion from Washington Mutual over the course of 10 days. After SVB went under, Signature Bank followed within hours , and First Republic Bank and Credit Suisse needed to be rescued within days.

The factors that enable, or impact a business' ability to adapt to change, include the following in our view:

Culture of experimentation, willingness to fail fast, and not punishing failure

For a business to be adaptable, it must be willing to wander, constantly tinker and experiment, see what works and what doesn't, and adjust its capital allocation accordingly. Employees need to feel free to admit failure without the fear of retribution and be allowed to continue to experiment.

Short feedback loops with customers

A business needs to know what customers want and then be able to build products quickly to meet their customers' ever-changing requirements. Quick innovation cycles are critical.

Financial flexibility

Excessive indebtedness reduces a business's ability to invest in its future.

Management team focused on building for the long term who think and operate like owners

An appropriate incentive structure for management must be in place to enable the team to forgo short-term glory for long-term success. Investing for the future often penalizes near-term earnings and stock performance but is often necessary in order to adapt to increasingly higher-paced change.

Platform businesses that benefit from disruptive change

A company with strong competitive advantages that is able to build platforms and eco-systems around its core products and services will likely be more capable of adapting rapidly because: 1) the platform serves as an anchor for durable growth, allowing the business to try and fail quickly when introducing new products or functionalities around its core offerings; and 2) a platform company with strong and vibrant ecosystems incentivizes third parties and would-be competitors to co-create value by dynamically enabling diversity of solutions as market demands change (think of the large number of apps Android and iOS have - numbers that would never be possible had they all been developed internally by Google and Apple).

Baron Durable Advantage Fund focuses on businesses with these characteristics. Microsoft, our largest holding, is a good case study of a business's ability to adapt and pivot after years of suffering the consequences of a stale management team that was resting on its laurels. The company's de facto monopoly position (Microsoft Windows + Office) in enterprise desktop and worker productivity suites in the client-server world made the company complacent and reluctant to take risks and continue to innovate. The stock languished for almost 15 years while Apple, Amazon, Google, and Facebook led the transition to mobile. Satya Nadella finally took the reins in 2014 and immediately changed the company's focus from the Windows-centric, on-prem legacy businesses to a cloud-first platform that could be accessed and used from any (mobile) device anywhere in the world. He also made the decision to open the platform to third parties, such as Linux, even though it was likely to hurt Microsoft's core Windows franchises. Nadella was willing to risk the high-margin on-prem business, recognizing that the world was going to change, and that cloud computing was going to be the future. This bold decision (and a massive multi-year investment) has reinvigorated the company and its stock, with Microsoft Azure, its cloud infrastructure business, surpassing $55 billion in annualized recurring revenue in the last quarter, while still growing 38% year-over-year . The price of Microsoft stock has increased seven-fold since Satya Nadella took over as CEO.

Amazon is probably the best example of a company that was built with an ability to rapidly adapt to change from its very inception. We have written a lot over the years about how Amazon's culture and organizational structures prioritize and enable rapid innovation. Historically, programming code was written in a sequential waterfall fashion, creating significant interdependencies between different developer teams in the organization and slowing down innovation. Amazon famously required all developers to expose their work externally via standardized Application Programming Interfaces (APIs). A novel and risky approach, it enabled development teams to work in parallel, created a rapid feedback loop with customers, and turned Amazon into one of the most innovative companies in the world. The culture of constant experimentation and the willingness to take risks and fail fast (remember the Amazon Fire phone?) became the core pillars of the company's culture and led to revolutionary ideas like third-party sales (letting competitors sell similar products alongside your own), Amazon Prime Video, and Amazon Web Services (AWS), making the company a disruptor and leader in multiple multi-trillion-dollar industries.

We believe adaptability is important not only for businesses but also for investors. We have discussed in the past that the best investors we know do not measure success in dollars and cents or in percentage returns or downside capture. They measure it in lessons learned. As investors, we learned that one of the most difficult tasks is to be able to maintain balance, especially during the times of extreme uncertainty and stress. The need and the pressure to adapt to the changing environment is very strong in the world of investing. But so is the need to stay disciplined and true to one's process and core skillset. Adapt too much to the changing environment, and you find yourself chasing the latest fads and whims (and memes?) and risk forgetting who you really are as an investor. Adapt too little, and you will be left behind. Warren Buffett notably wrote about his own adaptability over time in his 1989 shareholder letter:[3] "It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price. Charlie understood this early; I was a slow learner. But now, when buying companies or common stocks, we look for first-class businesses accompanied by first-class managements."

We have a lot of conviction that investing in a select, well-researched portfolio of first-class businesses that have sustainable competitive advantages, durable growth characteristics, and great managements will outperform the market over the long term, while minimizing the risk of permanent loss of capital. Finding companies that are resilient and adaptable to change, while maintaining an adaptable and flexible mindset of our own should help us generate good investment results over the long term. (Pat Patalino, our General Counsel prudently reminds us that there is no guarantee that in fact will be the case.)

{kind=link}

Shares of Meta Platforms, Inc. , the world's largest social network, were up 76.0% this quarter due to decisive cost discipline actions, improving adoption of new advertising products, the company's work in generative artificial intelligence ((AI)), and the broader rally in technology stocks. Meta is the mega-cap technology company most focused on profitability through cost cutting, including layoffs of more than 20% of its staff and reductions in its data center and office footprint. On the top line, Meta continues growing its user base with daily average users up 5% year-over-year in the last quarter. Engagement remains healthy with impressions up 23% year-over-year, and newer advertising formats (like Instagram Reels) are reportedly picking up steam with 40% of advertisers now using Reels. Longer term, we believe Meta will utilize its leadership in mobile advertising, massive user base, innovative culture, and technological scale to sustain durable growth for years to come, with further monetization opportunities ahead in newer areas such as WhatsApp.

NVIDIA Corporation is a fabless semiconductor mega-cap company and global leader in gaming cards and accelerated computing hardware and software. Despite subdued demand for gaming cards due to an ongoing PC slowdown and inventory correction, shares of NVIDIA rose 90.5% during the first quarter as a result of material developments in generative AI as evidenced by the release of ChatGPT and GPT-4. These technologies hold the promise of enabling significant productivity gains across domains from content creation, coding, and even biologic discovery. During its annual GTC conference in March, NVIDIA announced new products that expand its addressable market, such as the L4 chip, which opens the opportunity for video processing, representing 80% of internet traffic. We continue to believe NVIDIA's end-to-end AI platform and leading market share in gaming, data centers, and autonomous machines, along with the size of these markets, will enable the company to benefit from durable growth for years to come, and therefore we remain shareholders.

Shares of mega-cap software company Microsoft Corporation increased 20.4% during the quarter as the company reported results that beat investor expectations. In the Consumer business, Windows revenue was roughly in line, although Surface revenue missed investor expectations due to execution issues around new hardware launches. On the Commercial side, despite some technical snafus with Azure, year-over-year revenue growth came in at more than 38%, or 1% better than guidance, after missing by 1% in the prior two quarters. Stepping back from the short-term noise, in the first half of fiscal 2023, more than 70% of revenue was generated by the Commercial business, with 70% of that from Microsoft Cloud, the company's key long-term growth driver. Innovation appears to be getting even stronger, with significant enhancements in areas such as Power Apps, Security, and most recently, Azure OpenAI, which the company has said it plans to infuse across the entire portfolio over time. We are confident Microsoft is well positioned to continue taking share through any downturn and come out the other side better positioned than ever.

Monolithic Power Systems, Inc. is a fabless high-performance analog and power semiconductor company serving diverse end markets across the semiconductor industry. The company, a relatively small player in the industry, leverages its deep system-level and applications knowledge, strong design experience, and innovative process technologies to provide highly integrated, energy-efficient, cost-effective, and easy-to-use monolithic products. Shares rose 41.8% during the quarter as the company delivered solid financial results with revenues up 37% year-over-year and EPS up 50% year-over-year while also providing a favorable outlook driven by share gains across key end markets, including automotive and data center. Investor anticipation of a broader semiconductor industry recovery into the second half of 2023 also helped boost shares. The company continues to expand its addressable market and drive strong revenue growth by taking advantage of areas where its competition has failed to innovate. It has also started to sell more integrated, higher-ASP module products as opposed to discrete products, generating additional above-market growth.

Amazon.com, Inc. is the world's largest retailer and cloud services provider. Shares were up 23.0% in the quarter, driven by solid financial results. Revenues were up 12% year-over-year and AWS revenues were up 20% year-over-year to a run rate of over $85 billion, even though the company guided to a deceleration as a result of the weaker macro environment, which is driving budget optimizations at customers. Shares also benefited from continued actions around cost discipline, including steps to meaningfully improve core North American retail profitability to pre-pandemic levels. While near-term uncertainty remains, Amazon has substantially more room to grow in e-commerce, where it has less than 15% penetration in its total addressable market in the U.S. (with a longer runway internationally). Amazon also remains the clear leader in the vast and growing cloud infrastructure market, with large opportunities in application software, including enabling AI workloads. Additional areas such as advertising (where Amazon still holds less than 5% market share), logistics, and health care further solidify the company's growth durability.

{kind=link}

UnitedHealth Group Incorporated is the leading health care franchise in the U.S., with more than $350 billion in annual revenue. Following relatively strong performance in 2022, shares corrected 10.1% during the first quarter, along with other managed-care companies, primarily on sector rotation. Despite solid fourth-quarter results with 12% year-over-year revenue growth, 19% EPS growth, and a conservative initial 2023 guidance that fell within its 12% to 15% long-term earnings growth goal, investors stepped to the sidelines on concerns about proposed changes to the Medicare audit program, preliminary 2024 Medicare Advantage ((MA)) rates, and the impact of Medicaid recertification. We believe UnitedHealth is the best-positioned managed-care player, with a leading franchise in MA, the market's fastest growing segment. We expect continued strong growth and profitability, driven by positive demographic trends, effective cost management through economies of scale, industry-leading technology investments, enhanced expertise in population health, and a growing portfolio of providers, all of which enables UnitedHealth to keep and effectively manage more of its health care spending in-house.

Danaher Corporation is a life sciences and diagnostics company. For life sciences, Danaher supplies instruments for lab research, genomics services, and bioproduction tools. For the diagnostics business, the company supplies instruments to run clinical tests in large core labs, hospitals, pathology labs, and point of care. Shares declined 4.9% during the first quarter driven by a near-term headwind due to existing inventory reduction by biopharmaceutical customers. This is an industry-wide issue, and we remain positive on Danaher's long-term growth story. In particular, Danaher has a market-leading position and broad portfolio within bioprocessing, which addresses a biologics market growing by double digits and is positioned to benefit in the medium term from a wave of biosimilars entering the market after key patents expire. Danaher has a collection of high-quality assets, with targets of durable high single-digit core revenue growth and double-digit EPS growth.

Agilent Technologies, Inc. (A) provides instruments, software, services, and consumables for the life sciences, diagnostics, and applied chemicals markets. Despite reporting solid financial results with 10% year-over-year core revenue growth and 13% EPS growth, shares declined 7.6% during the first quarter on investor anticipation of a tougher macro environment later in 2023. We continue to believe Agilent is well positioned for long-term durable growth, driven by innovation, new product development, and its end market and geographic mix. Over time, Agilent will benefit from a shift in its business mix to higher-growth pharmaceutical, diagnostics, and research markets, while its leading competitive positioning and scale should enable it to raise margins over time.

LPL Financial Holdings Inc. , ( LPLA ) the largest independent broker-dealer in the U.S., is a new position for the Fund. The stock declined 6.4% in the first quarter, yet the favorable timing of our purchase led the stock to detract only a single basis point (0.01%) from our results. The weakness was largely driven by the stress to the banking system resulting from the bankruptcy of SVB, which caused investors to sour on financial stocks in general due to fears of contagion. We believe LPL is not exposed to the vast majority of issues facing banks. LPL is not a bank, has different regulators, and has a relatively small balance sheet. Over 95% of client cash is covered by FDIC insurance, and the limited securities LPL holds are U.S. Treasury bills with almost no interest rate or credit risk. The banking crisis has caused investors to take a more dovish view on the path of interest rates, which is a headwind to LPL's earnings as the economics on a large portion of client cash is tied to floating rates. However, we believe the company has a strong long-term earnings profile even in a lower interest rate environment, and stock weakness is being influenced by the short-term narrative. We go into more details over our long-term thesis and the reasons behind our decision to buy LPL in the Recent Activity section below.

Portfolio Structure

The portfolio is constructed on a bottom-up basis with the quality of ideas and conviction level (rather than benchmark composition and weights) determining the size of each individual investment. Sector weights tend to be an outcome of the stock selection process and are not meant to indicate a positive or a negative view .

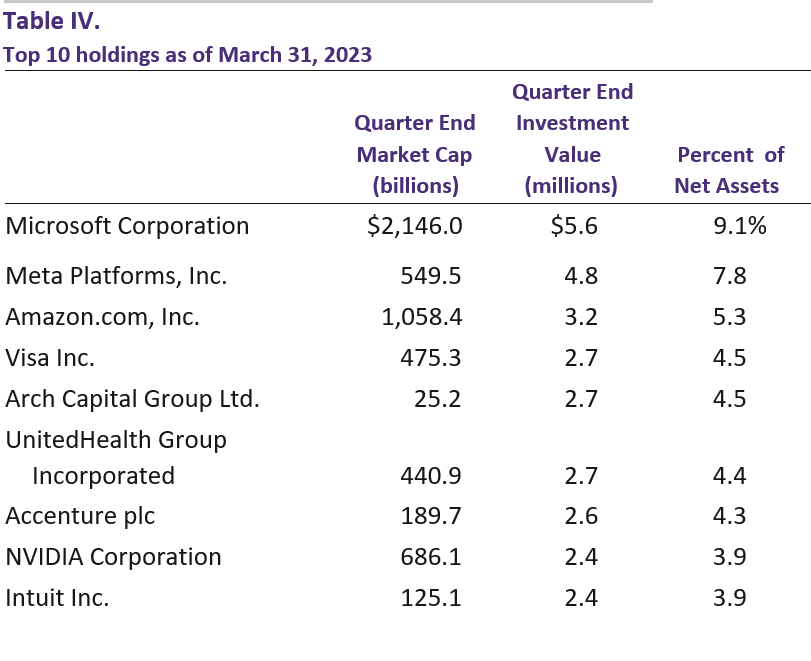

As of March 31, 2023, our top 10 positions represented 51.4% of the Fund, the top 20 were 83.4%, and we exited the first quarter with 30 investments (this compares to 49.9%, 82.6%, and 29 investments as of the end of 2022, respectively). As of the end of the first quarter, IT and Financials represented 62.7% of the Fund. Health Care, Communication Services, Consumer Discretionary, Consumer Staples, and Industrials represented another 36.5% of the Fund. Cash was the remaining 0.8%.

{kind=link}

{kind=link}

Recent Activity

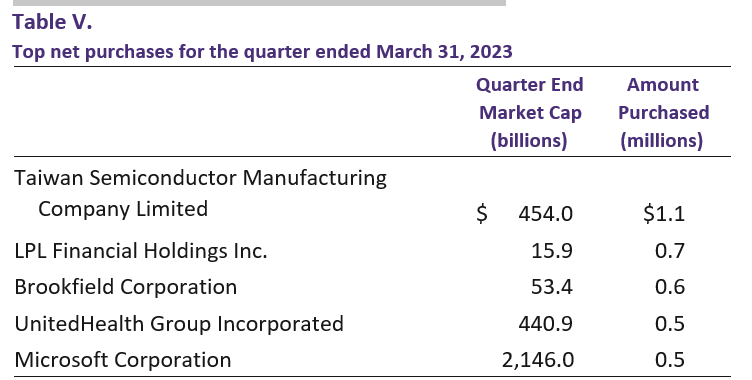

During the first quarter, we initiated two new investments, taking advantage of their share price volatility: the leading independent brokerdealer, LPL , and the leading global semiconductor manufacturer, Taiwan Semiconductor Manufacturing Company ( TSM ) . We also took advantage of fund flows to increase 17 of our holdings. We reduced three positions and sold Brookfield Asset Management ( BAM ) , the spun-off, pure asset-manager subsidiary of Brookfield Corporation, as we saw a better risk-reward in owning the parent company, to which we added.

{kind=link}

We have admired Taiwan Semiconductor Manufacturing Company Limited (TSMC) for years and believe that short-term, industry-wide cyclical pressure has provided an attractive entry point for long-term investors.

Morris Chang founded TSMC in 1987 as the world's first dedicated semiconductor foundry. Until then, semiconductor chips were always designed and manufactured by the same company. TSMC introduced a groundbreaking new business model in which TSMC acted purely as a contract manufacturer. This business model proved to be highly successful. TSMC maintained a single-minded focus on improving its manufacturing process technology and enabled the emergence of innovative fabless companies, including NVIDIA, Apple, and Qualcomm, who became its key customers. While many other foundry competitors emerged over the years, TSMC has outcompeted them with superior execution, operating efficiency, high-quality customer service, and the benefits of economies of scale. Today, TSMC controls approximately 60% of the total semiconductor foundry market and has a near-monopoly in manufacturing the world's most advanced chips. TSMC enjoys high barriers to entry given the ever-increasing cost and technological complexity of semiconductor manufacturing, while customer relationships are becoming increasingly sticky.

We believe TSMC will sustain strong double-digit earnings growth for years to come, with continued market share gains driven by its superior technology, reliability, and customer service. We expect TSMC to continue to benefit from the virtuous cycle of its scale advantage - higher profits leading to higher R&D and capex investments, allowing for further technological differentiation, resulting in more profits. We expect TSMC will remain a key enabler of future technological innovation, including AI and High Performance Computing, and a major beneficiary of the increasing pervasiveness of chips, including in electric vehicles and IoT.

During the first quarter, we also took advantage of the sell-off in LPL Financial Holdings Inc. to establish a new position. LPL is the largest independent broker-dealer ((IBD)) in the U.S. The company helps independent financial advisors run their practices more efficiently and serve their clients more effectively. As Americans continue to seek financial advice and as the number of retirees grows, the total pool of assets managed by financial advisors continues to grow. Traditionally, most financial advisors worked as employees of large banks (known as wirehouses), but over time, advisors have begun to favor independent models in which they are the owner-operator of their own advisory practice. Advisors are favoring this independence as it allows them to both retain far more of the revenue they generate and affords them greater flexibility over how to run their business.

As the largest IBD, LPL can invest more than its competitors in developing the technology and capabilities that allow advisors to run their practices efficiently. LPL's scale allows it to spread these significant costs over a $1 trillion-plus asset base. Crucially this ability to manage costs also allows LPL to pay industry-leading economics to its advisors, who can earn payouts of over 90% of the revenue they generate.

Beyond technology, LPL has innovated a range of different advisor models that allow the advisor to outsource as much of their practice operations as they choose. This provides advisors a high degree of flexibility as they make the transition to independence and means that LPL can position itself as an attractive IBD to a wide range of advisors. As CEO Dan Arnold put it at LPL's 2022 Investor Day: "[B]ack in '19, that [our traditional models] positioned us to serve about 100,000 advisors.… Now by extending those models, we now compete, at that time, for 200,000 of the advisors in the marketplace. And I think you've seen over the last couple of years, we've added as many as 50 practices, over 150 advisors in those models. It's been cool to continuously sort of invest and position those for what we believe are really interesting, appealing models that will create sustainable growth as we go forward."

The combination of these benefits enables LPL to continue taking market share and attracting more assets onto its platform. This, in turn, reinforces LPL's scale advantages and the ability to make crucial investments that enhance the advisor experience. Besides adding assets and recruiting advisors to the platform, LPL is also a beneficiary of rising asset prices, which grow its base of assets under management. LPL also sweeps the uninvested cash balances that are held in its clients' accounts and earns a yield by placing this cash with banks that are seeking deposits, while maintaining a capital-light business model. With higher interest rates, LPL can earn a higher yield on client cash, which contributes to high margin earnings.

The sell-off in LPL's stock was caused by changing interest rate expectations, with the market now believing we are closer to peak interest rates, with possible cuts to come. While this is a headwind to LPL's earnings, we believe the risk-reward balance is favorable, as the company remains well positioned to continue winning new advisors and asset inflows. By leveraging its scale to continue developing its advisor offerings and reinforcing its competitive position, LPL should be a share gainer in a growing market. We believe that low-teens asset growth can generate similar growth in gross profit, while improving margins and significant share repurchases will drive earnings-per-share growth at a mid-high teens rate.

We also took advantage of the sell-off in UnitedHealth Group Incorporated 's stock to add to our position as we continue to like the company's long-term opportunity and competitive advantages. We also added to our Microsoft Corporation position because we believe the company will remain a key beneficiary of digitization trends for years to come. While the macro-driven slowdown in IT budgets may create near-term volatility, Microsoft remains well positioned to benefit from the growing adoption of cloud computing and the progress in AI (with its 49% ownership of ChatGPT's builder, OpenAI). Lastly, as mentioned earlier, we consolidated our Brookfield Asset Management holding into the parent company, Brookfield Corporation , following the spin-off.

{kind=link}

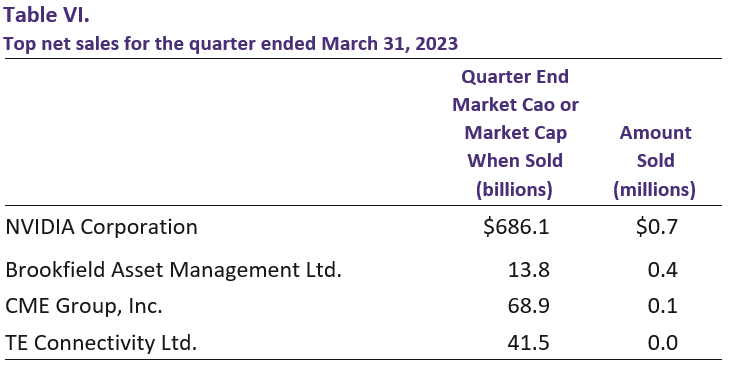

As mentioned above, we eliminated our investment in Brookfield Asset Management Ltd. and reallocated capital into the parent company, Brookfield Corporation. The only other sale of any consequence was our trim of NVIDIA Corporation . We took some profits due to the stock's significant outperformance during the quarter in order to manage the position size, as it was becoming uncomfortably large and a little too "in vogue" for our taste. Despite the reduction, NVIDIA remains a high-conviction investment and is a top 10 holding in the Fund.

Outlook

First Quarter 2020 - For the first time in 100 years, we are reintroduced to a global pandemic.

First Quarter 2021 - The reopening trade leads to significant outperformance for "value" sectors (e.g., energy, legacy banks, and airlines) for the first time in over a decade.

First Quarter 2022 - Russia invades Ukraine and exacerbates COVID-19-driven supply-chain challenges, pushing up inflation and compressing the pace of the Fed's tightening cycle.

First Quarter 2023 - SVB, the 16th largest bank in the U.S., collapses after a run on the bank, the largest bank crash since 2008. The 167-year-old financial institution, Credit Suisse, is sold for $3.2 billion to UBS in a takeover brokered by the Swiss National Bank.

Care to offer the outlook for the first quarter of 2024? We sure do not.

Skeptical investors often ask, if we have no confidence in forecasting the next three months or the next year, how can we have confidence in forecasting 5 or 10 years into the future? While this skepticism is understandable, we believe it is misplaced. Short-term stock price fluctuations (and company fundamentals) are disproportionately affected by the macro and by factors outside a company's control. We believe most of these factors are impossible to predict accurately with any consistency. However, it turns out that a business's uniqueness, the durability of its competitive advantages, its management's ability to prudently allocate capital and to earn high rates of return on the company's investments can be analyzed and therefore forecasted far more accurately over longer periods of time. Sure, qualitative things like a company's culture, the strength of its management team, and even the disruptive change analysis are all subjective; assessing them requires both analytical experience and a healthy margin of safety, but at the end of the day, there are only a handful of variables that go into the intrinsic value equation:

- How big is the opportunity?

- What market share can the company reasonably expect to get?

- How economically profitable would this business be at maturity?

- What is the cost of capital?

- And what is the terminal growth rate?

These are the variables that long-term owners of a business care about and spend their time researching. Over the last three months, we believe these variables have been moving in the right direction for most of our portfolio companies. Interestingly, although the Fed's rhetoric remains hawkish with "more inflation fighting left to be done," the 10-Year U.S. Treasury yield has fallen from around 3.9% at year-end 2022 to around 3.4% as we write this letter. Similarly, real rates, as measured by the yield on 10-Year U.S. TIPS have dropped from around 1.6% to around 1.1% over the same period. Just sayin'…

Every day, we live and invest in an uncertain world. Well-known conditions and widely anticipated events, such as Federal Reserve rate changes, ongoing trade disputes, government shutdowns, and the unpredictable behavior of important politicians the world over, are shrugged off by the financial markets one day and seem to drive them up or down the next. We often find it difficult to know why market participants do what they do over the short term. The constant challenges we face are real and serious, with clearly uncertain outcomes. History would suggest that most will prove passing or manageable. The business of capital allocation (or investing) is the business of taking risk, managing the uncertainty, and taking advantage of the long-term opportunities that those risks and uncertainties create. We are confident that our process is the right one, and we believe that it will enable us to make good investment decisions over time.

Our goal is to invest in large-cap companies with, in our view, strong and durable competitive advantages, proven track records of successful capital allocation, high returns on invested capital, and high free-cash-flow generation, a significant portion of which is regularly returned to shareholders in the form of dividends or share repurchases. It is our belief that investing in great businesses at attractive valuations will enable us to earn excess risk-adjusted returns for our shareholders over the long term. We are optimistic about the prospects of the companies in which we are invested and continue to search for new ideas and investment opportunities.

Sincerely,

Alex Umansky, Portfolio Manager

Footnotes

[1] The S&P 500 Index measures the performance of 500 widely held large cap U.S. companies. The index and the Fund include reinvestment of dividends, net of withholding taxes, which positively impact the performance results. The index is unmanaged. Index performance is not Fund performance; one cannot invest directly into an index. 2 The performance data in the table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

[2] Not annualized.

Investors should consider the investment objectives, risks, and charges and expenses of the investment carefully before investing. The prospectus and summary prospectus contain this and other information about the Funds. You may obtain them from the Funds' distributor, Baron Capital, Inc., by calling 1-800-99BARON or visiting www.BaronFunds.com . Please read them carefully before investing.

Risks: The Fund invests primarily in equity securities, which are subject to price fluctuations in the stock market. In addition, because the Fund invests primarily in large-cap company securities, it may underperform other funds during periods when the Fund's securities are out of favor. The Fund may not achieve its objectives. Portfolio holdings are subject to change. Current and future portfolio holdings are subject to risk.

The discussions of the companies herein are not intended as advice to any person regarding the advisability of investing in any particular security. The views expressed in this report reflect those of the respective portfolio managers only through the end of the period stated in this report. The portfolio manager's views are not intended as recommendations or investment advice to any person reading this report and are subject to change at any time based on market and other conditions and Baron has no obligation to update them.

This report does not constitute an offer to sell or a solicitation of any offer to buy securities of Baron Fifth Avenue Growth Fund by anyone in any jurisdiction where it would be unlawful under the laws of that jurisdiction to make such offer or solicitation.

Alpha measures the difference between a fund's actual returns and its expected performance, given its level of risk as measured by beta. Downside Capture measures how well a fund performs in time periods where the benchmark's returns are less than zero.

BAMCO, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission (SEC). Baron Capital, Inc. is a broker-dealer registered with the SEC and member of the Financial Industry Regulatory Authority, Inc. (FINRA).

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Baron Durable Advantage Fund Q1 2023 Shareholder Letter