CA - Barrick Gold: Ignore The Weak Q3 Results

2023-11-03 11:45:00 ET

Summary

- Barrick Gold reported softer Q3 results with lower gold production than planned and is expected to just miss the low end of its annual guidance.

- That said, the big picture remains as bullish, with Barrick set to see further margin expansion in Q4, additional margin recovery in FY24, and significant production growth from 2023-2031.

- In this update, we'll look at the Q3 results, how Mark Bristow has been vindicated by his decision to focus on exploration vs. M&A and Barrick's updated low-risk buy zone.

We're nearly halfway through the Q3 Earnings Season for the VanEck Gold Miners ETF ( GDX ) and the most recent major producer to report its results is Barrick Gold Corporation ( GOLD ). On the surface, the headline results were softer than planned, with just ~1.04 million ounces of gold produced and production tracking to just below the low end of annual guidance. However, we saw a significant improvement in margins and several capital projects are nearing completion that will ultimately deliver cost savings. Plus, free cash flow was up materially year-over-year and should improve to $2.0+ billion in FY2024 if gold prices can continue to cooperate. Let's take a closer look at the quarter below, recent developments, and where the stock's updated low-risk buy zone lies.

{kind=link}

All figures are in United States Dollars unless otherwise noted, with all production figures on an attributable basis unless otherwise noted.

Q3 Production & Sales

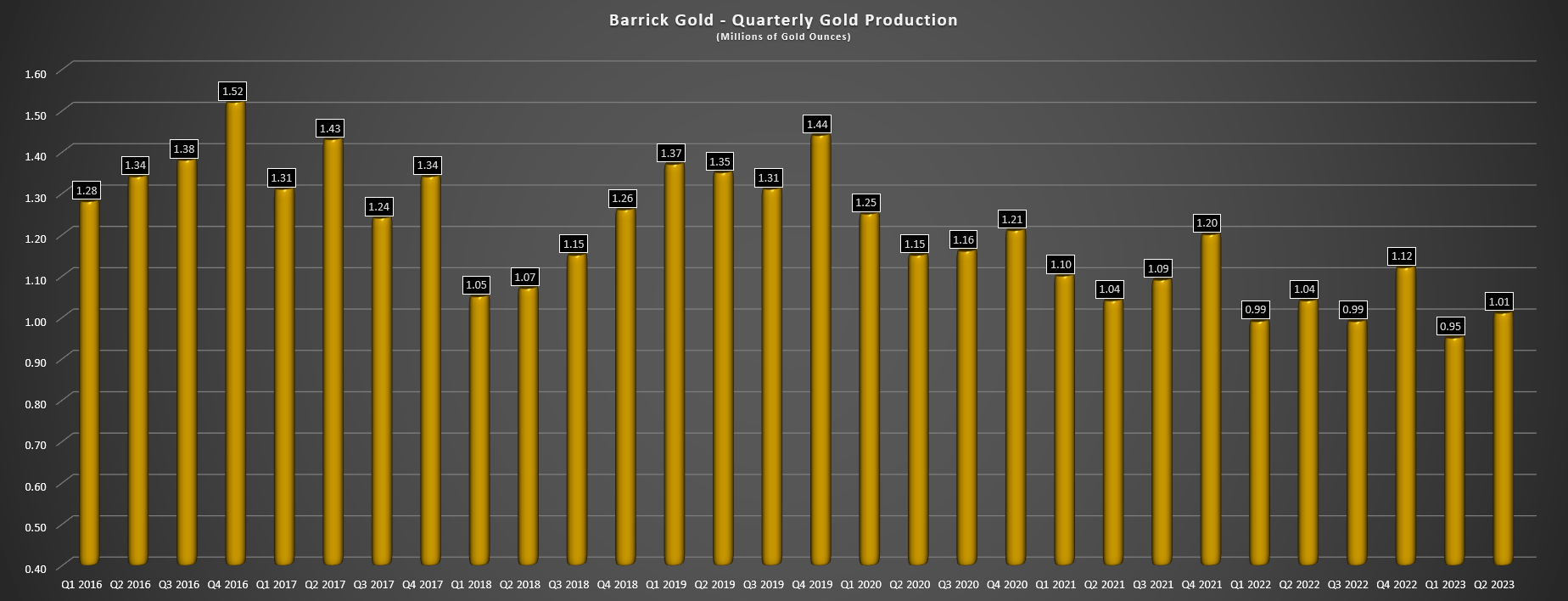

Barrick Gold released its Q3 results this week, reporting quarterly production of ~1.04 million ounces of gold, a 5% increase from the year-ago period. The higher production was driven by higher production at Cortez (~137,000 ounces), Turquoise Ridge (~83,000 ounces), Tongon (~47,000 ounces), Kibali (~99,000 ounces), Veladero (~55,000 ounces), and Loulo-Gounkoto (~142,000 ounces). Unfortunately, this was partially offset by a much weaker quarter at Pueblo Viejo (delayed ramp-up due to minor issues), and lower production at Long Canyon (Phase 1 mining completed last year), and North Mara (lower grades and tough comps vs. strong Q3-22). Meanwhile, production was flat (but below expectations) at its majority-owned Carlin Complex (unplanned downtime at Goldstrike autoclave and lower mining rates at GQ Pit). The result was that while production was up year-over-year, it's set to come in up to 3% below the low end of the annual guidance range, a disappointing development.

Barrick Gold - Quarterly Gold Production - Company Filings, Author's Chart

{kind=link}

Digging into the miss a little closer, the primary culprit for the softness was Pueblo Viejo, which saw lower grades, recoveries, and throughput during the ramp-up of its planned expansion to ~14 million tonnes per annum that was expected to push production to 800,000+ ounces per annum and significantly extend the mine life. However, the ramp-up was affected by the failure of the gearboxes for the floatation cells and the partial failure of the end of the new conveyor belt to the single-stage SAG mill. Barrick Gold's CEO Mark Bristow shared more on this in the Q3-23 Conference Call, but noted that temporary fixes are in place and while this will lead to a slower ramp-up (nameplate capacity now expected in Q1-24), the company remains confident in the asset's ability to produce 800,000 ounces per annum (100% basis) next year.

"When we commissioned the largest float cells ever built, and the OEM who supplied those float cells, and they under-designed the gearboxes. So we've been able to retrofit and engineer a temporary solution so those float cells are now working, but the supplier has agreed to send us completely new assemblages by the end of this year. So by the end of the year, we'll have that problem properly put to bed..."

- Barrick Gold CEO, Mark Bristow, Q3 2023 Conference Call

Unfortunately, this wasn't the only hiccup in the period, and the company's Nevada production was also impacted by minor setbacks. At its Carlin Complex (61.5% ownership) under its Nevada Gold Mines JV, production was flat at ~230,000 ounces of gold with fewer tonnes mined than planned at the Gold Quarry Pit and unplanned downtime at the Goldstrike autoclave (which will also affect Q4 production). Meanwhile, Barrick noted that production at Cortez was affected by lower than planned oxide grades from Crossroads and a slower than planned ramp-up at Goldrush. On a positive note, the Goldrush Record of Decision is still expected by year-end 2023, even if it arrives later than initial plans, and the Porgera restart is on track by year-end with a new Special Mining Lease granted in mid-October. Once in production, with attributable production to Barrick of ~160,000 ounces once optimized from this 650,000+ ounce per annum mine once it's back at full capacity.

As noted in Barrick's Q1 2023 update, Porgera would average annual gold production of ~700,000 ounces once the ramp-up and optimization of the Wangima Pit was complete.

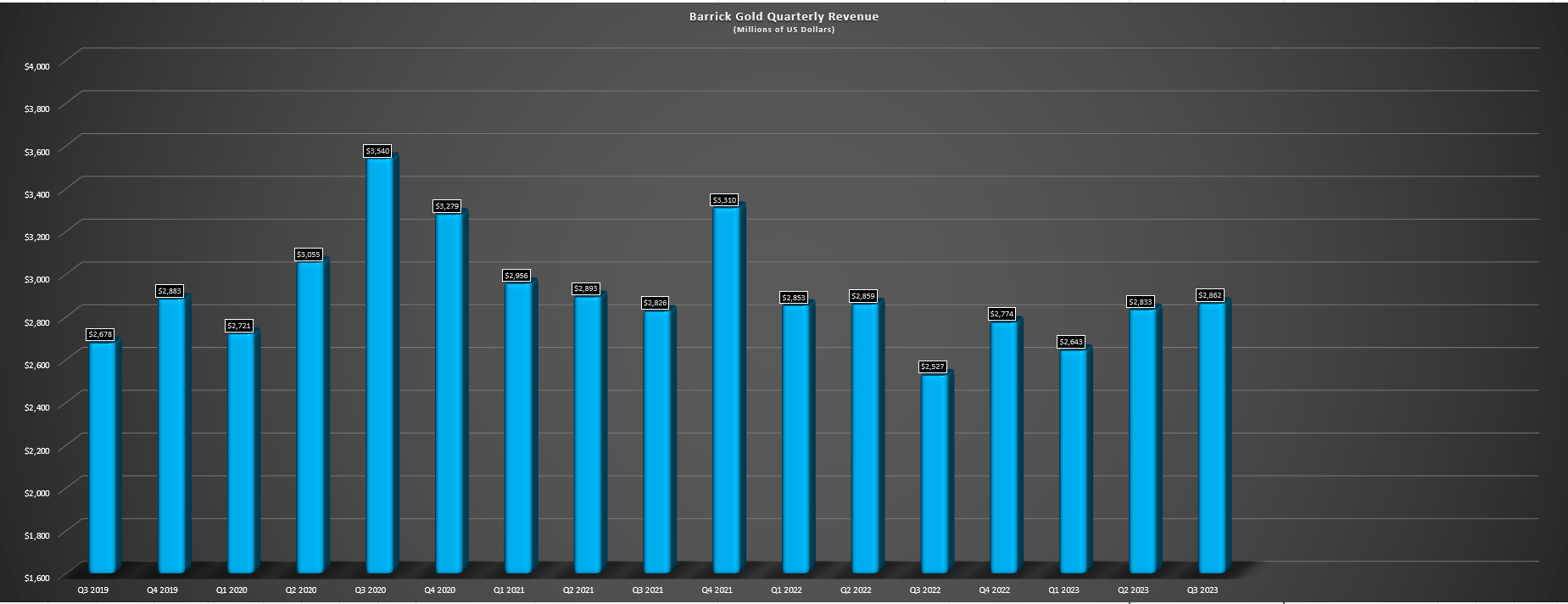

Barrick Gold Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

Digging into Barrick's financial results, revenue was 13% higher year-over-year despite the setback, benefiting from more ounces sold (and slightly below production levels at ~1.03 million ounces) and fewer copper pounds sold. This is because the company benefited from a much stronger copper ($3.78/lb) and gold price ($1,928/oz), and the gold price strength has certainly continued into Q4 after a brief departure lower to start the quarter, with the gold price averaging ~$1,990/oz over the past 10 days. Meanwhile, while revenue was up 13% to ~$2.86 billion, operating cash flow also soared to ~$1.13 billion, benefiting from higher realized metals prices and lower cash taxes paid.

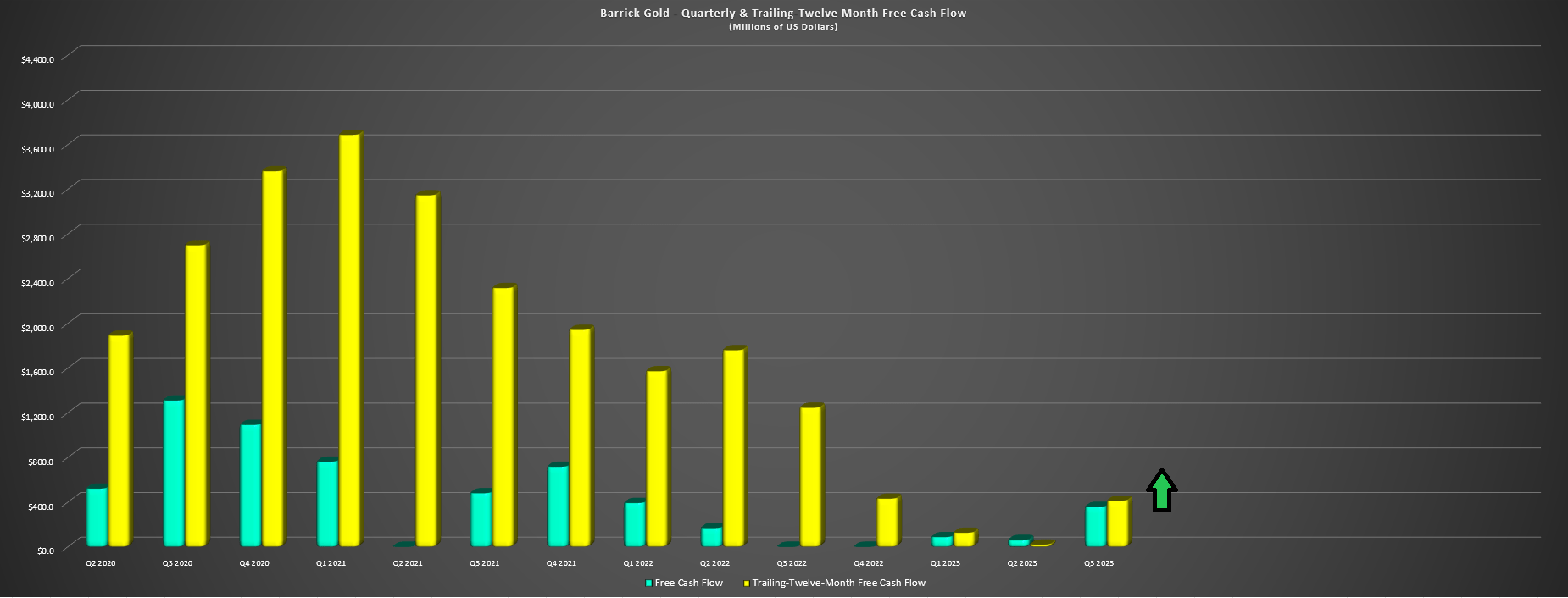

Finally, free cash flow soared to $359 million (Q3 2022: free cash outflow of $34 million) despite still elevated capital expenditures (Loulo Phase 2 Solar Plant set to be completed by year-end, TS Solar Project at its Nevada operations, and owner mining truck fleet purchases at Lumwana). As it stands, the TS Solar Project (200 MW PV Solar Farm) is nearly complete ($250 million of ~$300 million spent), and Barrick noted that it is now looking at the potential for a 16 MW Solar Plant at its massive shared Kibali Mine. Overall, the completion of the Pueblo Viejo Expansion and near completion of several other projects is positive, and this should help to positively impact all-in-sustaining costs and free cash flow in 2024/2025 when combined with increased ounces sold (higher denominator).

Barrick Gold - Quarterly & Trailing Twelve Month Free Cash Flow - Company Filings, Author's Chart

{kind=link}

Costs & Margins

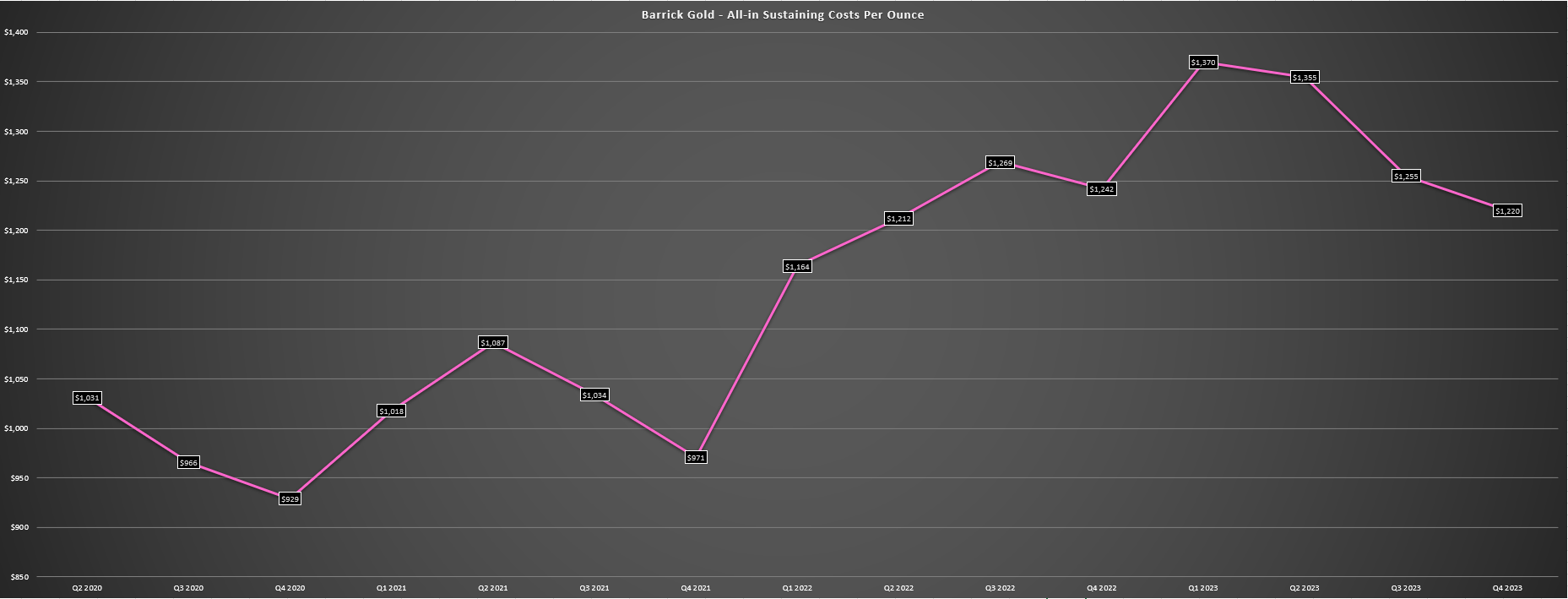

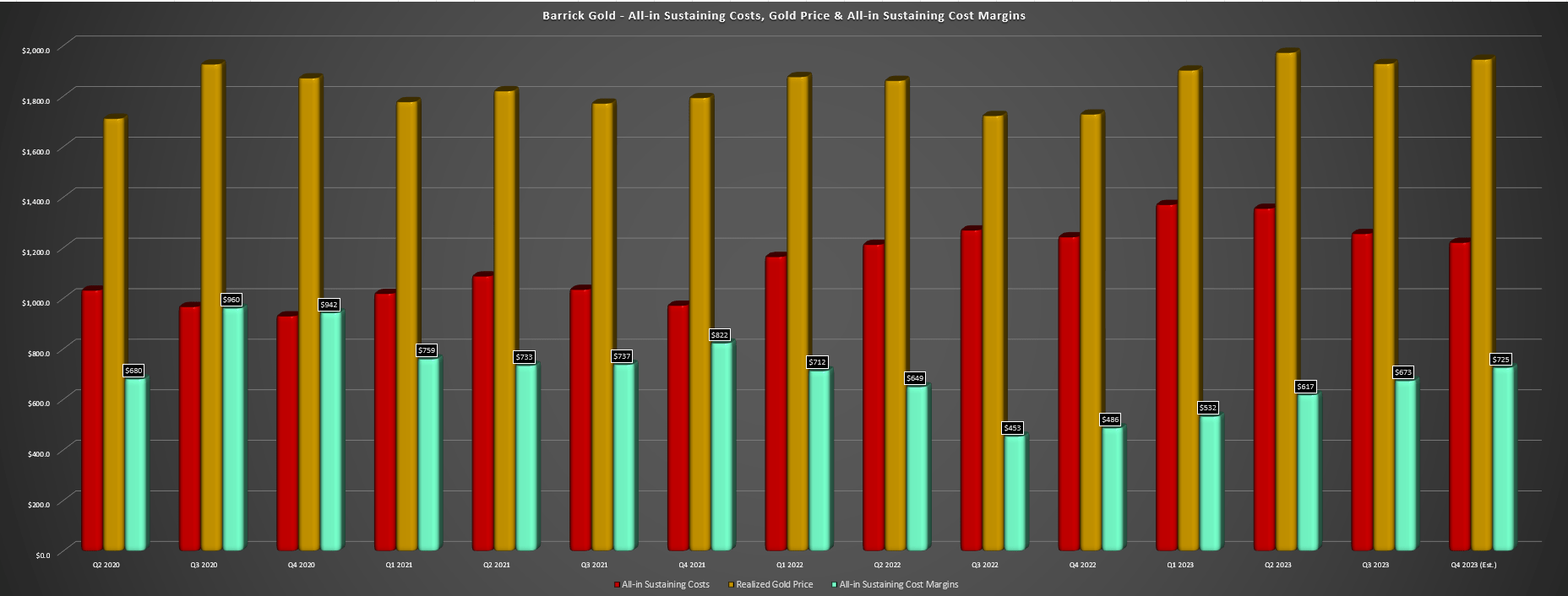

Moving over to costs and margins, Barrick reported all-in sustaining costs [AISC] of $1,255/oz in Q3, a 1% improvement year-over-year and a more than 8% improvement from peak costs in Q1 2023. This was a welcome development with investors worrying about rising costs, and it was helped by lower mine-site sustaining capital expenditures and higher production. And when combined with a much stronger average realized gold price, all-in sustaining cost margins soared to $673/oz, a 49% increase year-over-year. Finally, it's worth noting that while AISC margins improved meaningfully on a year-over-year and sequential basis, we should see further improvement in Q4, and even assuming $1,220/oz AISC and a $1,945/oz gold price, AISC margins should improve to ~$725/oz (+8% sequentially). And under a more bullish gold price scenario ($1,975/oz in Q4), AISC margins will come above $750/oz or a ~55% increase year-over-year (Q4 2022: $486/oz).

Barrick Gold - Quarterly AISC - Company Filings, Author's Chart Barrick Gold - Quarterly AISC & AISC Margins + Q4 Estimates - Company Filings, Author's Chart & Estimates

{kind=link}

{kind=link}

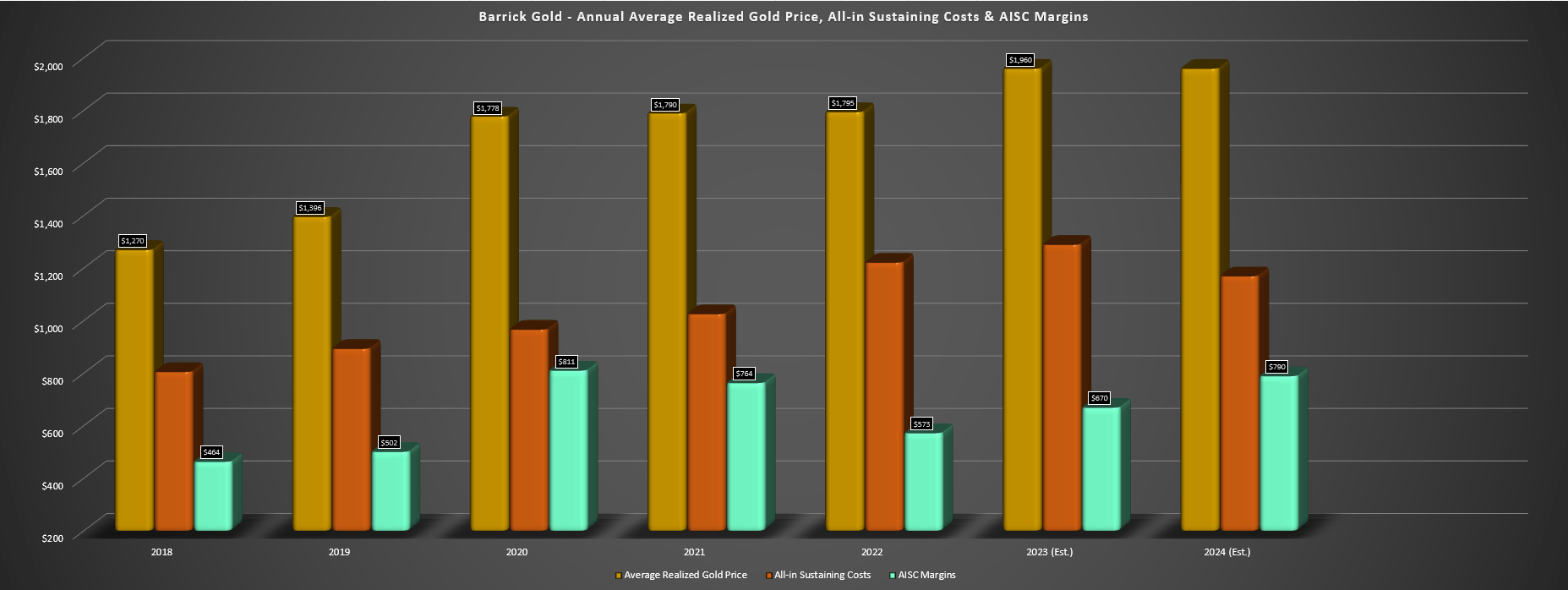

While this is encouraging, it's worth looking at the bigger picture for miners even if we can see significant volatility around quarterly results. And when it comes to Barrick's bigger picture from a margin standpoint, it's quite bullish. This is because while AISC should come in near $1,290/oz in FY2023, I would expect to see AISC improve to $1,170/oz or lower in 2024 with improved unit costs from higher gold production and more normalized lower mine-site sustaining capital. And assuming this is the case and the gold price even just manages to hold steady at $1,960/oz, we would see AISC margins improve more than 18% year-over-year to $790/oz vs. expectations of ~$670/oz in FY2023. Plus, with high-margin production coming from Goldrush (commercial production expected in 2026), and the Pueblo Viejo Expansion, there's certainly a path back to sub $1,125/oz AISC longer-term vs. the peak costs is expected this year (albeit already declining on a quarterly basis).

Barrick Gold - Annual AISC & AISC Margins + 2024 Estimates - Company Filings, Author's Chart & Estimates

{kind=link}

Recent Developments

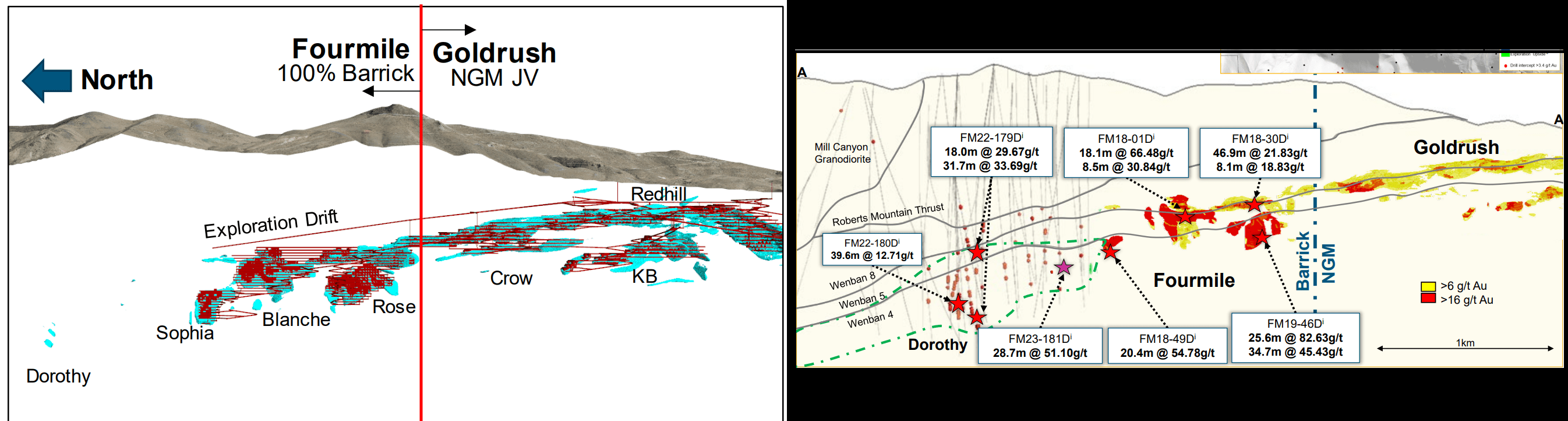

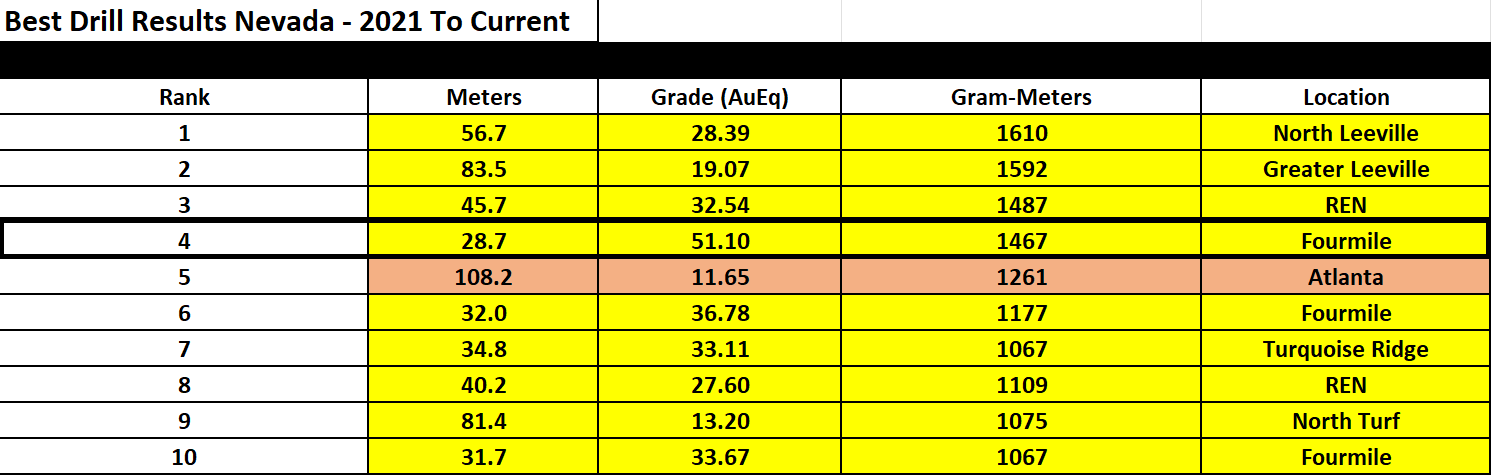

Digging into recent developments, there were several positives worth highlighting, but the main one is certainly Fourmile. Barrick noted in its release that its 100% owned Fourmile (which will eventually be contributed to its NGM JV) delivered an incredible intercept of 28.7 meters at 51.1 grams per tonne of gold, making it one of the top-5 intercepts drilled across all Nevada projects since 2021 that I'm aware of. Notably, this intercept testing for mineralization between Sophia and the Northernmost discovery (Dorothy) suggests the potential to significantly grow the Fourmile resource to the north (shown below). Elsewhere and 400 meters east at the new Anna Marie target, Barrick noted that it has further potential with significant alteration and "many similar geological characteristics to the Fourmile corridor" .

Fourmile Drilling & Goldrush/Fourmile Deposits - Company Website Top-10 Drill Intercepts in Nevada (2021-Current) - Company Filings, Author's Chart

{kind=link}

{kind=link}

Given the exploration success, Barrick has not only unveiled a new exploration target of 13 to 20 million tonnes at 13.3 to 20.0 grams per tonne of gold. And even using just below the low point of this figure, this could lift Fourmile's resource from ~3.0 million ounces to 8.0+ million ounces at higher grades assuming 16.0 million tonnes at 16.0 grams per tonne of gold (~8.2 million ounces of gold). This is a huge deal as not only would Fourmile dwarf Windfall in size and grade (a shared joint venture in Canada on North America's best current high-grade asset), but it could potentially contribute an incremental 350,000 ounces long-term to Goldrush. The result? Goldrush/Fourmile would be a behemoth at ~800,000 ounces per annum (Goldrush: ~440,000 ounces, Fourmile: 350,000+ ounces) at industry-leading costs. In summary, the recent results are extremely encouraging and certainly vindicate Bristow's choice to focus on organic growth in the vicinity of considerable sunk infrastructure (roasters, autoclaves) with the drill bit vs. M&A.

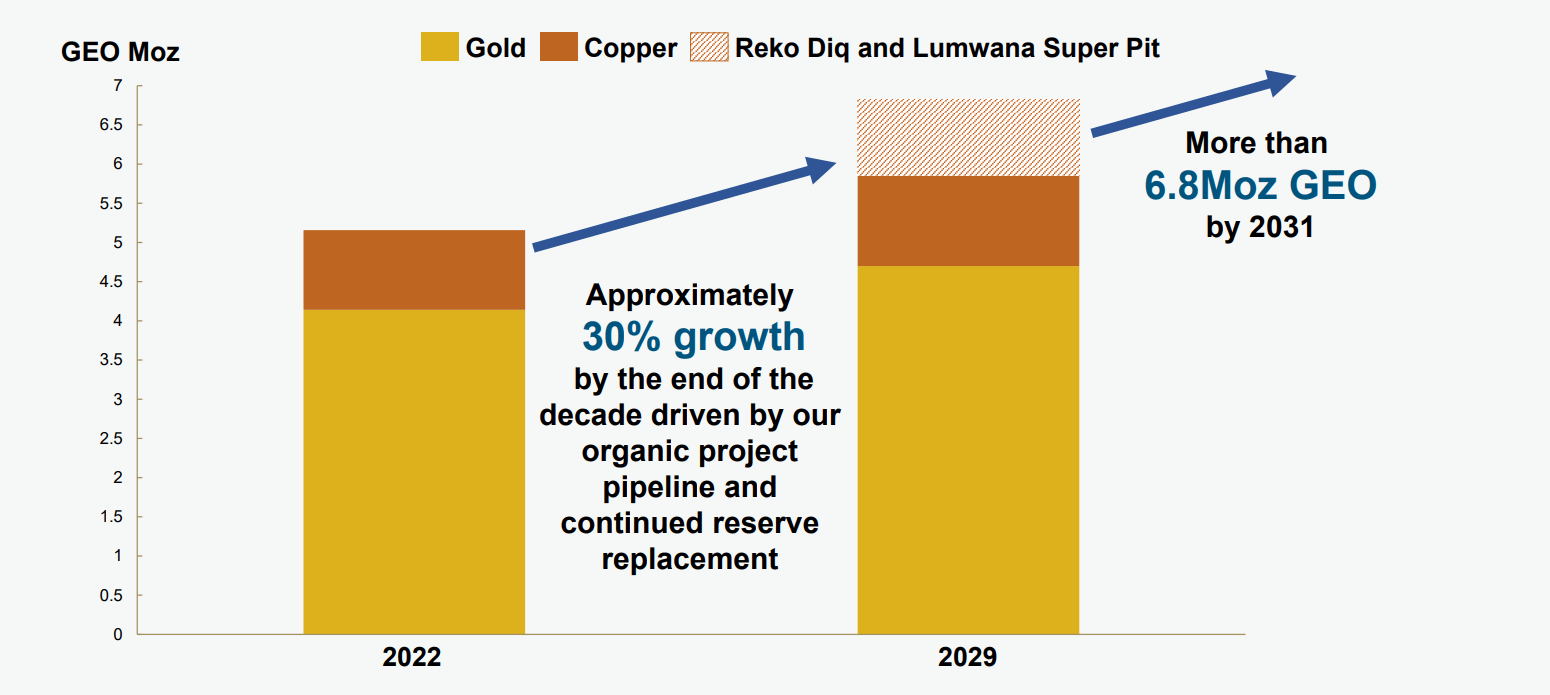

Meanwhile, for Reko Diq, the company expects to release a Feasibility Study by year-end 2024, followed by construction in 2025. Assuming the company can execute against this schedule with no hiccups, this would translate to first production in 2028, a key pillar for gold-equivalent ounce production growth (besides Robertson, Goldrush/Fourmile, Porgera restart, Lumwana Super Pit and the recently completed Pueblo Viejo Expansion). And assuming all goes to plan and even without any contribution from the massive Donlin Project in Alaska that might make sense at higher gold prices and if optimized (once higher priority Lumwana Super Pit and Reko Diq are put into production), Barrick could see its annual production grow to ~6.8 million gold-equivalent ounces according to the company, up from ~5.0 million gold-equivalent ounces in 2023.

{kind=link}

Summary

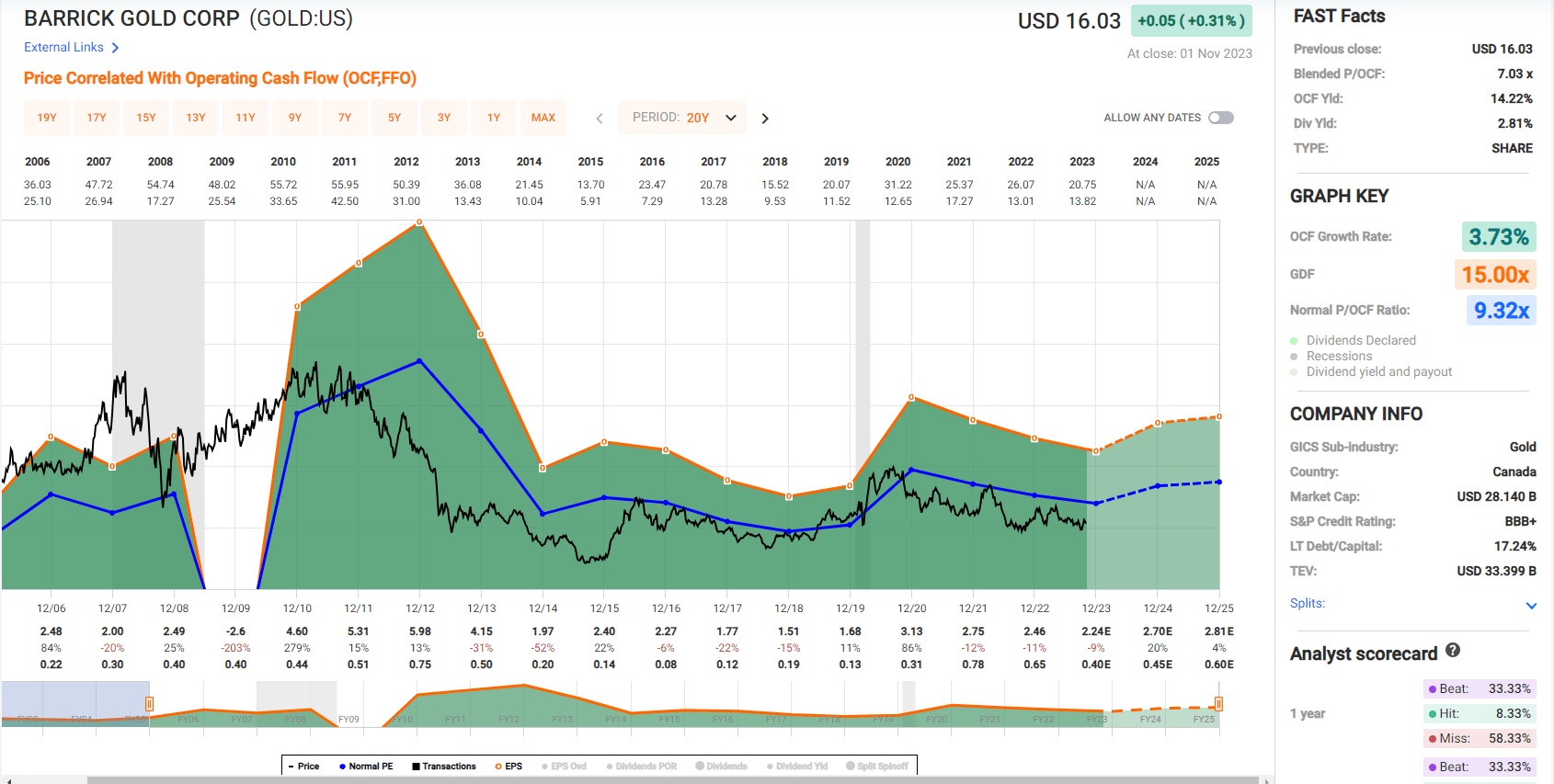

Barrick's Q3 results may have come in a little below my expectations and the miss on its annual guidance mid-point is disappointing, but the long-term picture remains better than ever. This is because we'll see significant production growth over the rest of the decade, margins have hit their trough and are already trending higher (with further improvement in Q4 sequentially and year-over-year) yet the stock is trading at a depressed multiple at less than 6.0x FY2024 operating cash flow estimates. Not only is this ~40% below its long-term average (~9.3x), but these estimates assume no further upside in gold and copper prices, and a further improvement in costs expected in FY2025.

{kind=link}

Meanwhile, from an exploration/reserve growth standpoint, Barrick continues to enjoy success, with Fourmile's drilling certainly being a highlight with the potential for an 8.0+ million ounce resource based on its upgraded exploration target. This could ultimately turn Fourmile/Goldrush into an ~800,000 ounce per annum operation (making it one of the largest gold mines in North America next to Detour Lake and Malartic in an expansion case). And just as importantly, this is translating to reserve/resource growth per share with consistent reserve/resource growth while Barrick is opportunistically reducing its share count (24.3 million shares purchased last year) and rigid capital discipline (no overpriced M&A). Hence, with the stock trading at a ~10% FY2024 free cash flow yield, I would view any pullbacks below US$15.25 as buying opportunities.

For further details see:

Barrick Gold: Ignore The Weak Q3 Results