CA - Barrick Gold: The Significantly Undervalued Harmony Of Copper And Gold

2023-10-09 07:58:58 ET

Summary

- Copper demand is expected to surge due to the transition to net-zero, with a potential 54% growth in supply needed for a net-zero emissions future.

- Gold prices are influenced by expected Federal Reserve interest rate decisions, and a bullish outlook is predicted due to potential rate cuts.

- Barrick Gold Corporation offers an attractive investment opportunity with its ambitious growth plans, particularly in copper, including a $2 billion investment in Zambia.

Introduction

My two favorite metals to invest in, analyze, and monitor are copper and gold.

Copper , which is a semi-precious metal, is one of the world's most important metals for industrial purposes. Using 2019 data (4 years old but still valid for the purpose of this article), we see that the biggest part of copper demand comes from construction industries, which includes wiring and related. A combined 40% comes from electrical uses and transportation equipment.

Global X

Transportation equipment is expected to experience a massive surge in demand as the world transitions to net-zero.

The same goes for technologies related to that.

Looking at the chart below, an electric car uses twice as much copper as an average conventional car. Offshore windmills use more than 8 tonnes of copper!

International Energy Agency

Hence, earlier this year, the Wall Street Journal wrote that copper shortages are threatening the green transition.

By 2031, annual copper demand is predicted to reach 36.6 million metric tons, while supply is forecasted to be around 30.1 million tons, resulting in a 6.5 million ton shortfall at the start of the next decade.

While anticipated shifts in technology, including changes in battery packs reducing copper usage in electric vehicles, could help offset growing demand pressures, copper's crucial role in green technologies is expected to raise its consumption from 4% in 2020 to an estimated 17% by 2030, potentially causing the need for 54% copper supply growth by 2030 for a net-zero emissions path.

Needless to say, this is a big deal.

I anticipate an increase in global supply growth, but it is unlikely to keep up with demand, leading to price acceleration when global economic demand expectations improve. Copper is currently suffering from a lackluster global cyclical demand growth.

Gold is my preferred precious metal because of its timeless value, perpetual shine, and universal acceptance as a currency alternative that cannot be printed.

Unlike copper, gold is a metal that trades based on expected Federal Reserve interest rate expectations. The (not updated) chart below shows that gold is highly related to forward Fed Funds Futures. In other words, if the market expects the Fed to cut rates in the future, it tends to benefit gold prices.

CME Group (Not Updated)

With regard to my gold outlook, this is what I wrote in a recent article :

In a world where economic uncertainties are on the rise, I'm diving back into gold (miners). My conviction stems from the mounting risks that could force the Fed's hand into rate cuts.

While I've long advocated for extended inflation and economic strength, my current focus is on the potential weakness that might push the Fed towards rate cuts, setting the stage for another wave of inflation.

Given weak consumer sentiment and a shaky labor market, I am investing in gold to strategically boost my portfolio. By monitoring gold's correlation with future rate expectations, I am predicting potential shifts.

This brings me to the Barrick Gold Corporation (GOLD), the Toronto-based mining giant that is currently expanding both its gold and copper footprints. The company is positioning itself to be a great company that delivers the best of two worlds.

FINVIZ

I believe that after dropping 15% year-to-date and 50% from its 2020 highs, Barrick offers a highly attractive risk/reward.

What Makes Barrick So Special

This may be the longest introduction I've ever written. However, I believe that the bigger picture is almost as important as company-specific developments. After all, if the bigger picture is bearish, odds are even the best miners will suffer.

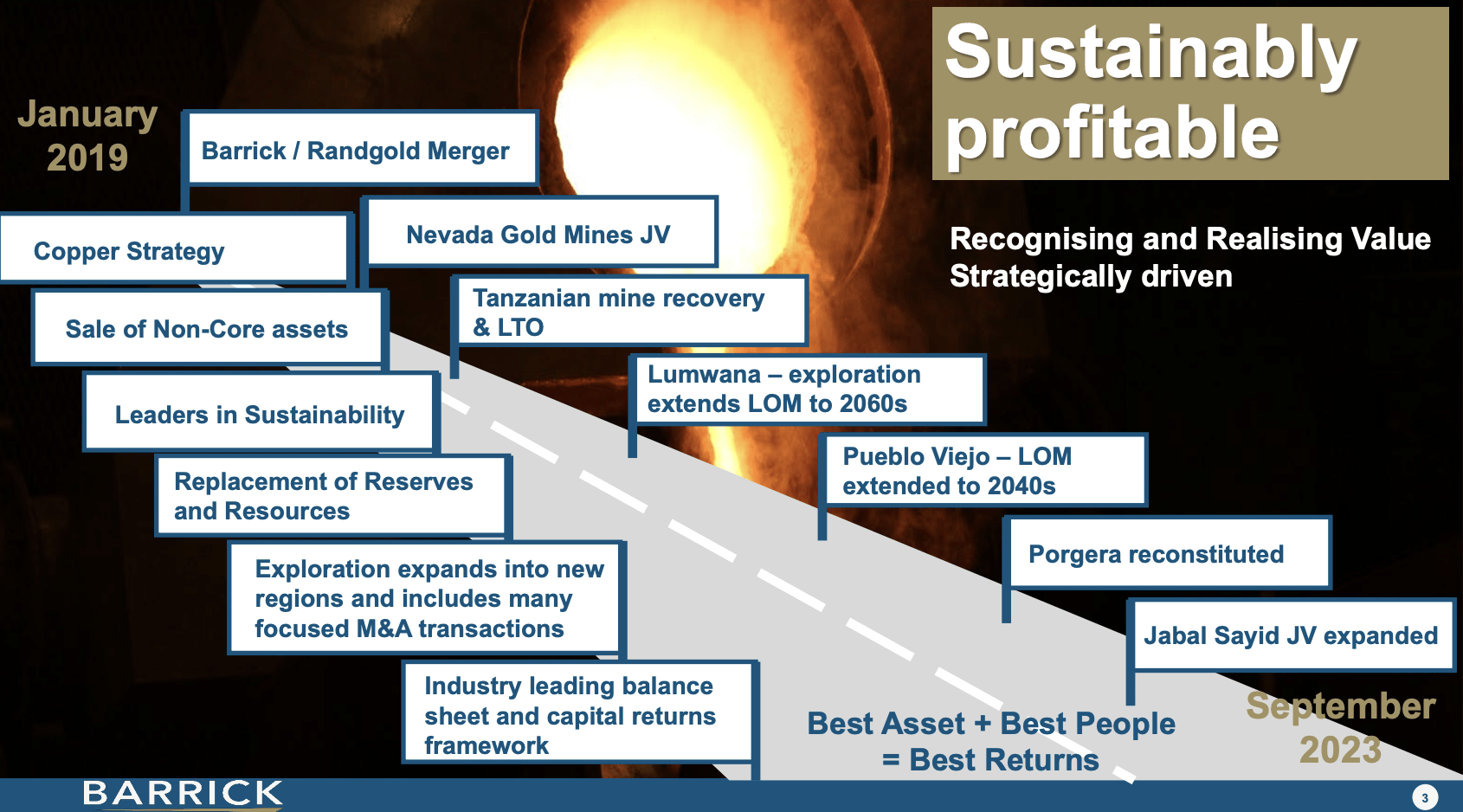

During last month's Gold Forum Americas Conference, Barrick focused on its strategy set in 2019 to transform into a leading gold and copper business.

{kind=link}

The vision encompassed Tier One assets, prudent capital allocation, and sustainable profitability.

The company emphasized its progress in delivering on this strategy, emphasizing strong balance sheets and top-tier assets. The plan included M&A, asset rationalization, and capital strengthening. Some of this is visible in the overview above.

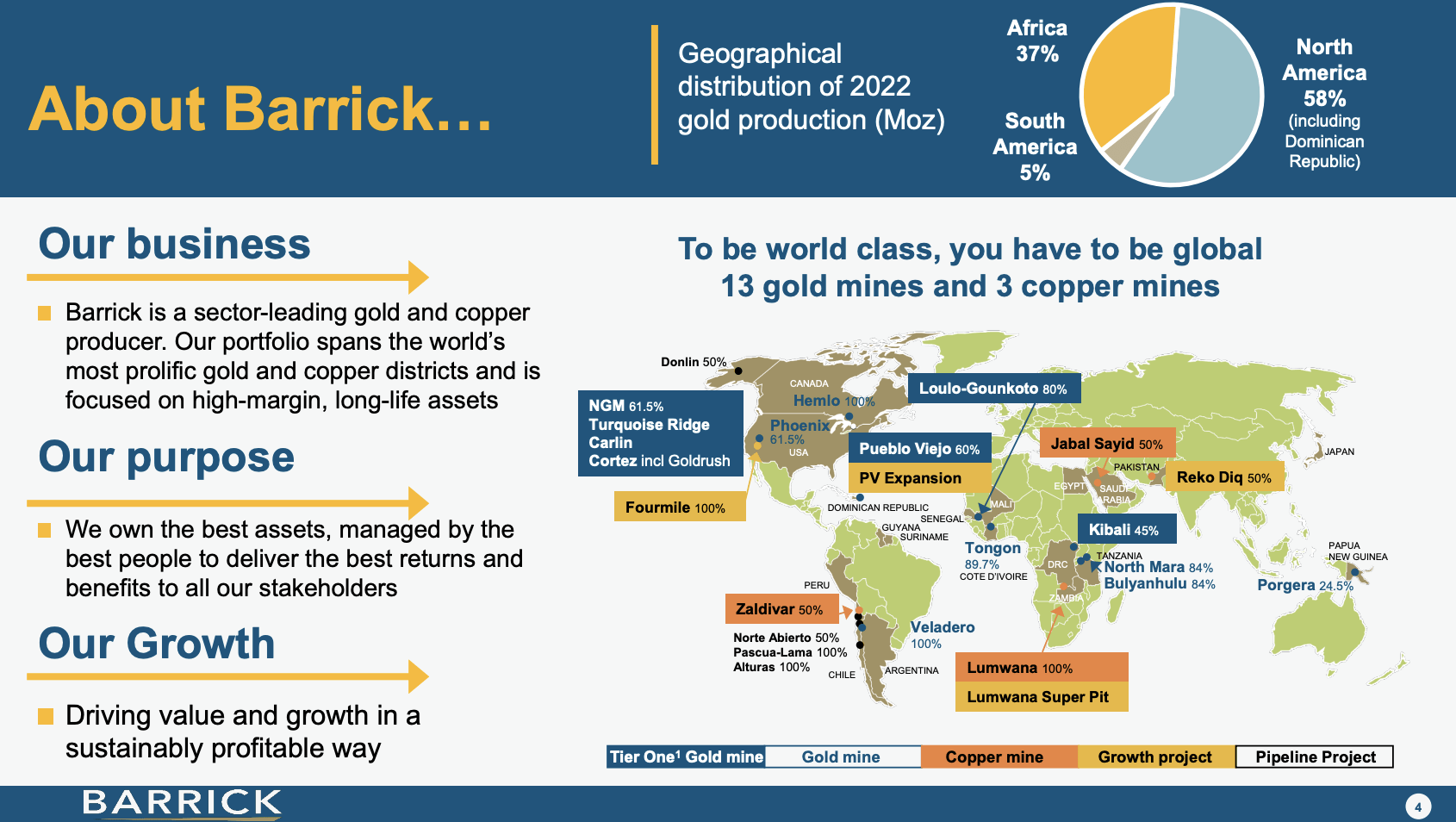

For example, Barrick currently owns and operates six Tier One gold mines globally, providing a strong base plan for the next decade. It also generates more than half of its money in North America, which tremendously lowers geopolitical risks.

{kind=link}

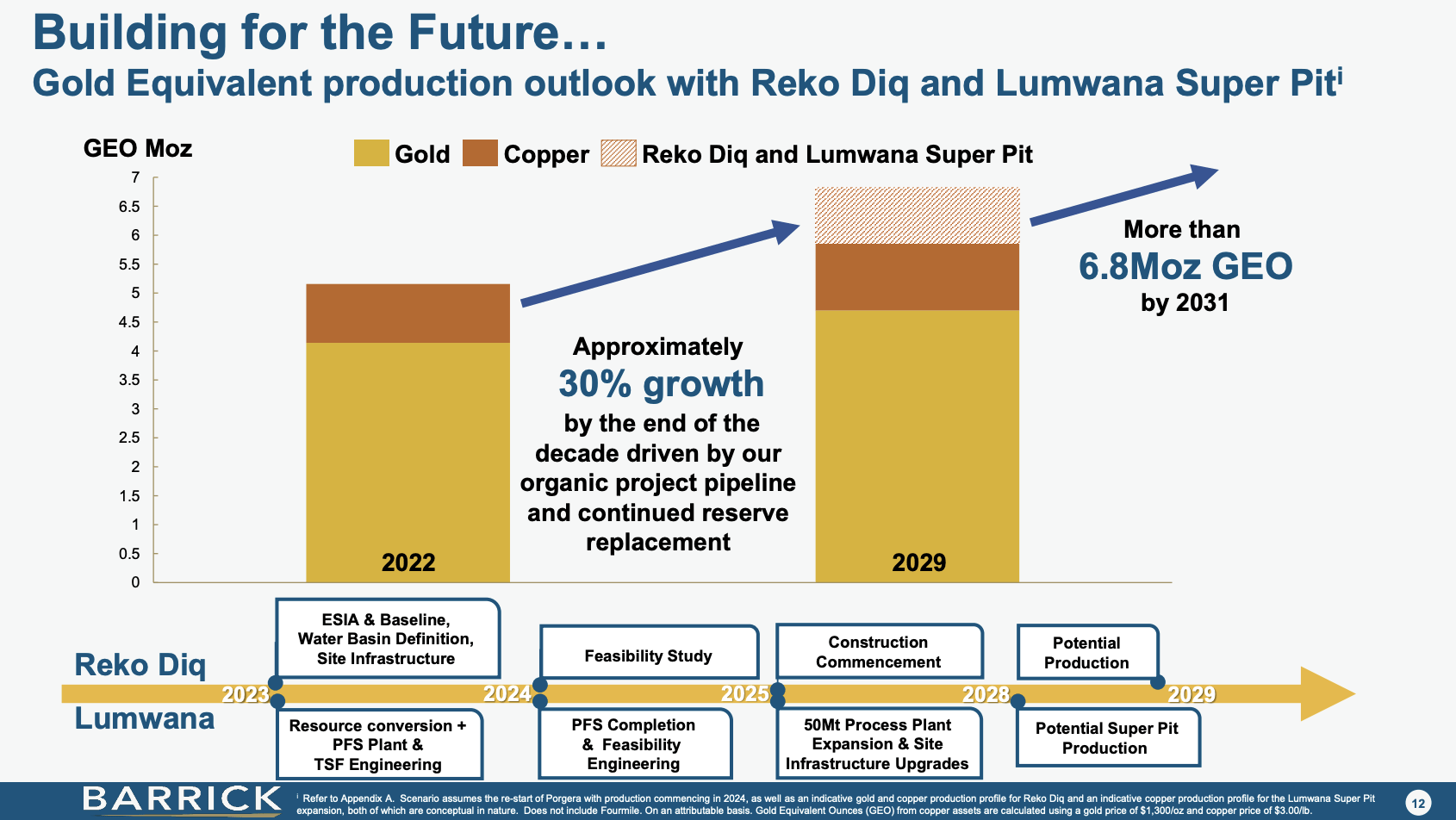

Beyond this, the company unveiled an ambitious growth plan, projecting a 30% increase in production by the end of the decade.

As the overview below shows, by 2031, the company is expected to produce more than 6.8 million ounces of gold equivalent. A big part of this could be copper production.

{kind=link}

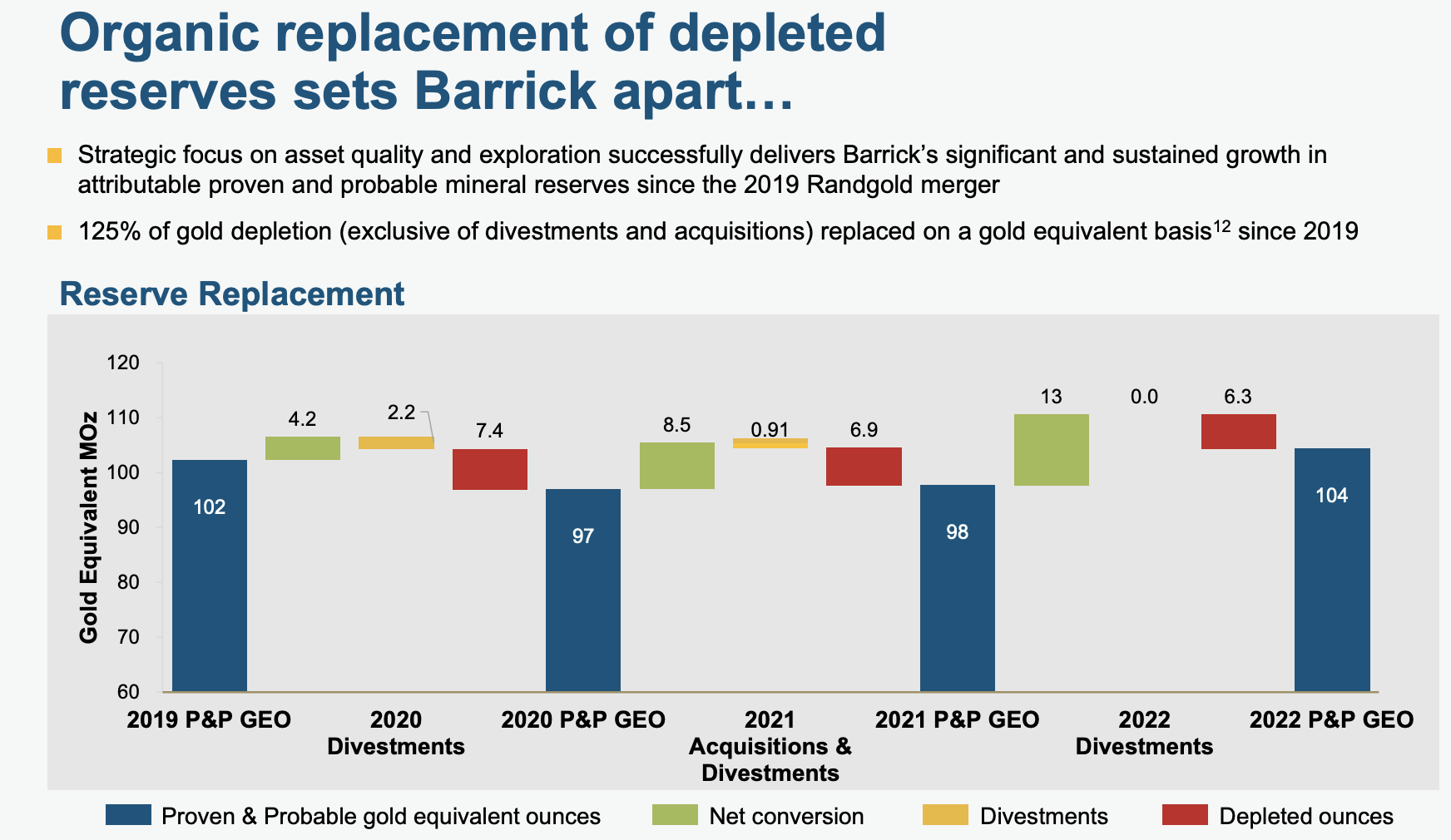

During its 2Q23 earnings call, the company also emphasized its ability to grow, indicating a 125% replacement of total production since the 2019 merger, including copper, and future strategies for resource replacement.

[...] we still have a wealth of opportunities, with the potential to be big value drivers, and are confident that exploration will sustain reserve replacement and deliver an inventory that will secure a 15 year planning horizon and beyond [...] - GOLD 2Q23 Earnings Call

In other words, the company found and bought more new reserves than it is mining and sees plenty of opportunities to sustain reserves.

{kind=link}

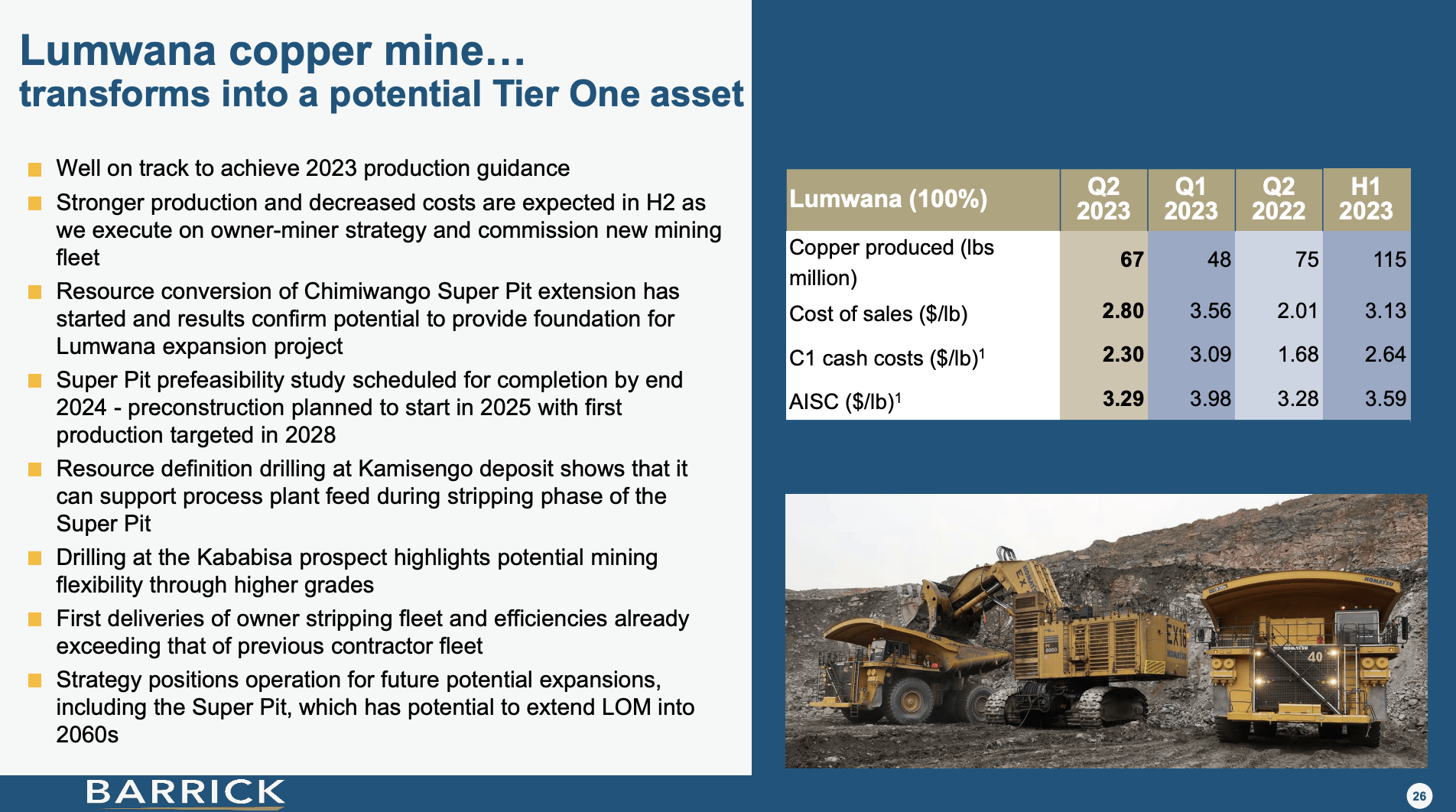

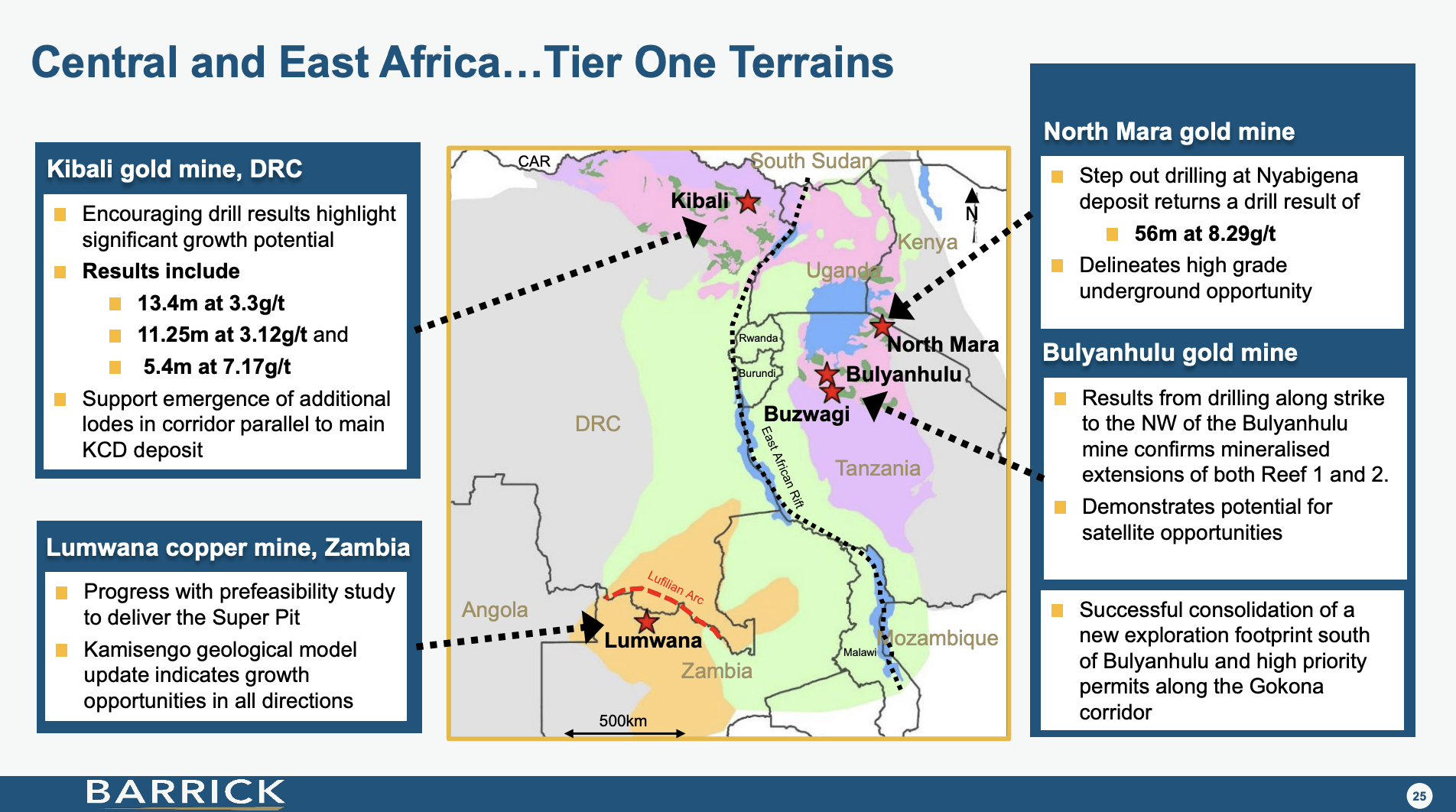

Furthermore, Barrick Gold placed a spotlight on its copper operations, notably emphasizing Lumwana's potential transformation into a Tier One asset.

The company outlined strategic moves, including the owner-miner strategy implementation and commissioning of a new fleet, foreseeing a reduction in operational costs.

{kind=link}

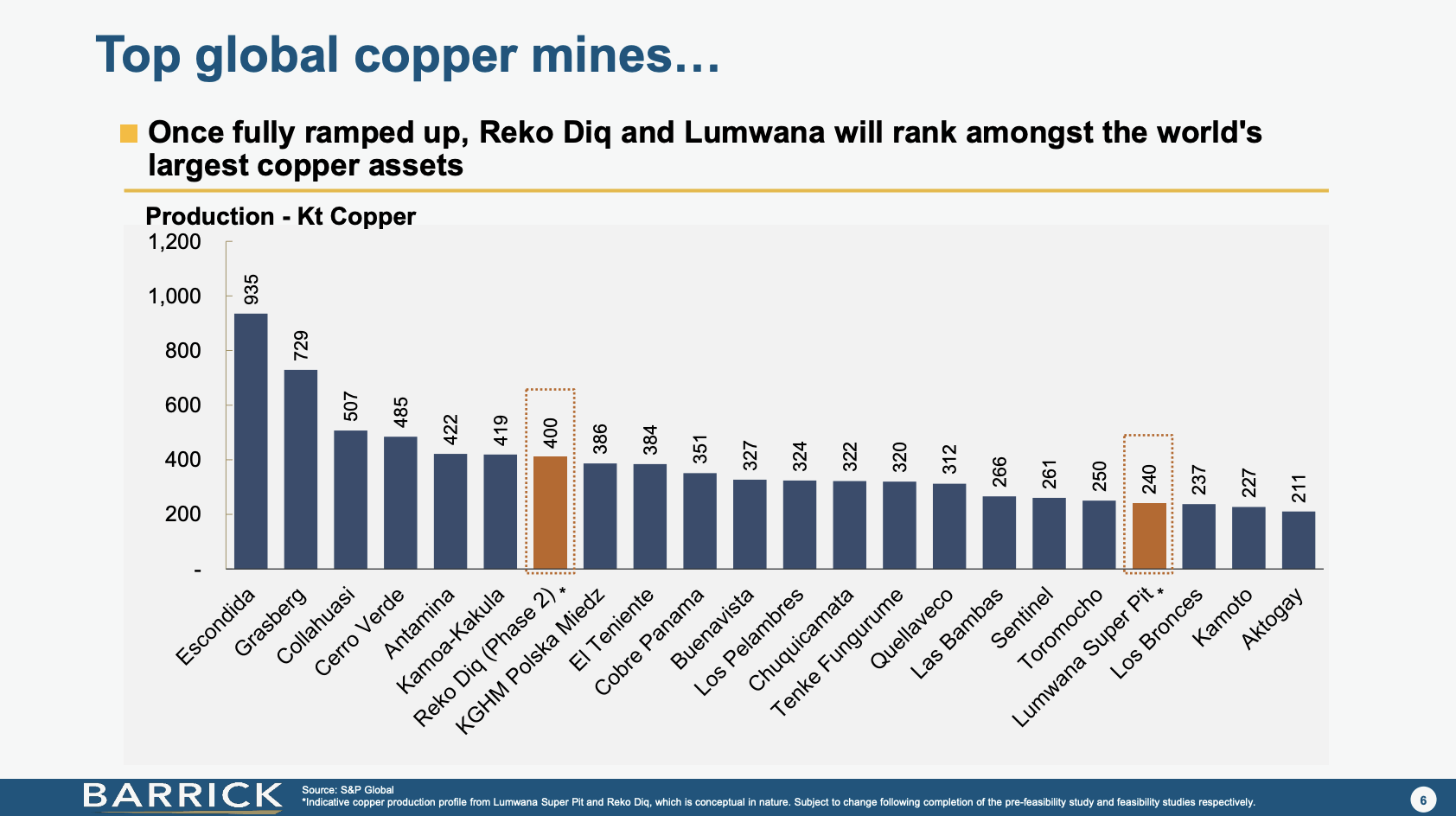

With expansion plans and projections extending Lumwana's mine life to 2060, the company indicated a clear path towards increased copper reserves, which benefits tremendously from the aforementioned secular growth tailwinds.

Together with Reko Diq, Barrick is on track to operate two of the world's biggest copper mines.

{kind=link}

On top of that, Barrick Gold has positioned its African ventures at the forefront of its growth strategy. Notably, the Kibali mine in the Democratic Republic of Congo showed substantial improvements in production during the second quarter.

Moving across to the Democratic Republic of Congo and Kibali, again, Kibali overcame its first quarter challenges to deliver substantial improvement, as you can see here in production for quarter two. And it's -- it has its back on -- this has really set it back on course to achieve its full year guidance. And we also are really focusing on our underground development to build additional flexibility and be able to support the new 10-year mine plan. - GOLD 2Q23 Earnings Call

{kind=link}

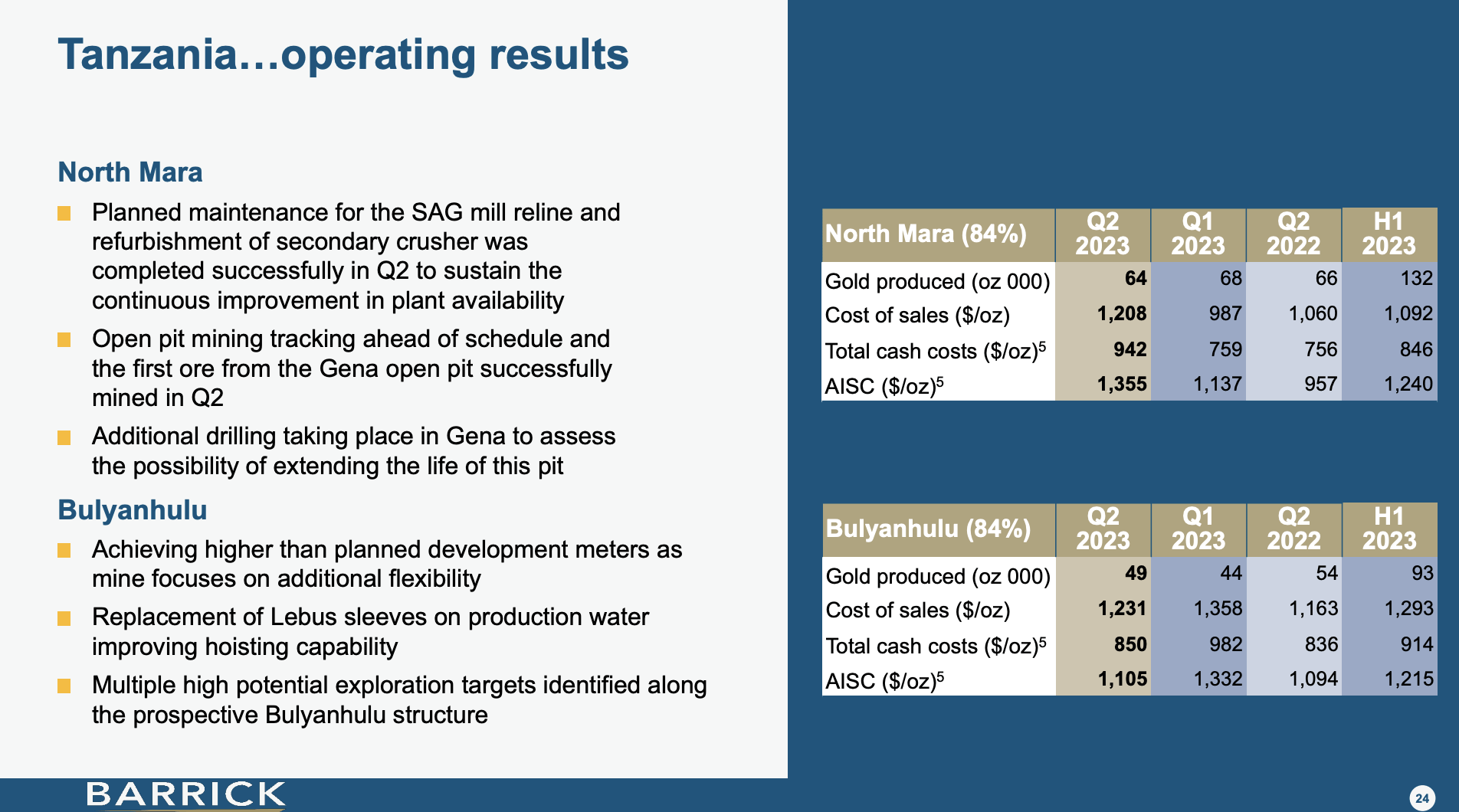

Furthermore, exploration initiatives in Tanzania have yielded promising results, exemplifying Barrick's vision of mining as a catalyst for transformation, making underdeveloped countries more investment-friendly.

And in Tanzania, which is a real success story. Our Twiga joint venture with the Tanzanian government is a poster child for my thesis that mining can be the force that makes undeveloped countries investable. And there is no better example than Tanzania. And it's great to see BHP putting its toe in the water in Tanzania on the nickel project. - GOLD 2Q23 Earnings Call

{kind=link}

Adding to that, on October 4, the company announced a $2 billion copper expansion in Zambia.

As reported by Mining.com (emphasis added):

Barrick Gold (TSX: ABX)(NYSE: GOLD) plans to invest almost $2 billion in an expansion of its Lumwana copper mine in Zambia, with the purpose of increasing production.

The project will increase Lumwana's annual production to an estimated 240,000 tonnes of copper from a 50 million tonnes per annum process plant over a 36-year life of mine, Barrick said on Wednesday.

The move is part of the company's wider plan to extend the life of the mine to 2060 and help Zambia revive its copper industry, chief executive Mark Bristow said.

"Barrick believes that its host countries are its key stakeholders and that partnering with them creates sustainable value for both of us," Bristow said .

Zambia already is Africa's second-largest copper producer after its northern neighbour, the Democratic Republic of Congo.

Barrick said it aims to complete the full feasibility study by the end of 2024, bringing the expanded production forward to 2028.

It also needs to be said that the company has an A3 credit rating, indicating tremendous balance sheet strength.

This brings me to the valuation.

Valuation

Putting a valuation on a stock that is tied to commodity prices is always tricky. The company is trading at 6.2x NTM EBITDA.

In 2024, the company is expected to generate $6.6 billion in EBITDA, up from $5.6 billion in 2023 (expected). I believe that number could be 10% to 20% higher, as I do not expect gold prices to remain at current levels in a scenario where central banks are potentially forced to ease to deal with economic weakness.

The current consensus stock price (for NY-listed shares) is $22.40, which is 50% above the current price.

I agree with that and see much more upside on a 2-3-year basis - especially if the company gets support from both gold and copper prices.

The only reason I do not own GOLD shares is because I decided to mainly focus on mining equipment companies like Caterpillar (CAT). However, GOLD is on my watchlist, as I do like the value close to $14 per share. I just haven't figured out how I'm going to structure my portfolio in light of new opportunities.

Takeaway

In a world where industrial demand and green technologies are on the rise, my investment radar is firmly locked onto copper and gold.

Copper, a cornerstone of industrial progress, faces a looming supply-demand gap as the world pivots towards sustainability. Electric cars, windmills, and more depend heavily on this versatile metal, leaving us with a substantial copper shortfall by 2030. The result? A potential 54% growth in copper supply is needed for a net-zero emissions future.

As for gold, it is dependent on expected future Federal Reserve interest rate decisions. In increasingly uncertain economic times, gold tends to shine brighter. My outlook on gold is bullish, as I anticipate potential Fed rate cuts, creating a favorable environment for gold prices to soar.

For investors eyeing both metals, Barrick Gold Corporation stands out with its ambitious growth plans, particularly in copper. With strategic expansions, including the recent $2 billion investment in Zambia, Barrick positions itself as a key player in the global copper market, presenting a compelling investment prospect for the future.

For further details see:

Barrick Gold: The Significantly Undervalued Harmony Of Copper And Gold