BBWI - Bath & Body Works: A High-Quality Business Model But With No Upside

2023-06-16 08:00:00 ET

Summary

- Bath & Body Works is capitalizing on trends such as clean beauty, wellness and self-care, and the digital transition to drive growth.

- BBWI has an EBITDA-M of 20% and is generating consistently strong cash flows.

- Key risks to BBWI is the performance in the coming 12 months as investors are pricing in a resilient performance.

- Our DCF valuation implies the company is trading at its fair value.

Investment thesis

Our current investment thesis is:

- BBWI has a high-quality business model and is benefiting from tailwinds. We suspect it will be a resilient retailer in the coming year.

- Margins are very good and look defensible, owing to the products the company sells.

- BBWI's valuation does not imply upside based on a DCF calculation. When factoring in near-term risk, we suggest a hold.

Company description

Bath & Body Works, Inc. ( BBWI ) is a specialty retailer that focuses on offering a wide range of home fragrances, body care, soaps, and sanitizer products.

Share price

BBWI stock price made gains during a period of strong demand post-Covid. Since then, the share price has declined in line with cooling market conditions and is trading flat.

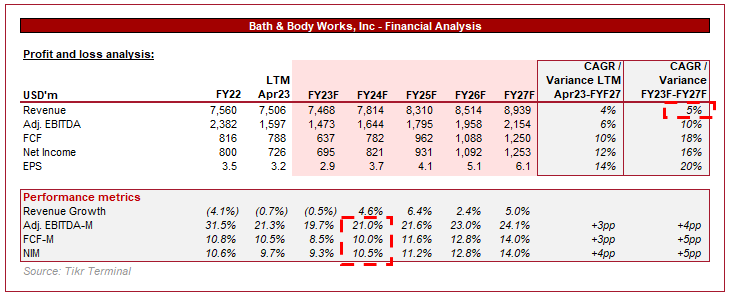

Financial analysis

Financials ( TIKR Terminal )

Presented above is BBWI's financial performance for the last decade.

Revenue & Commercial Factors

BBWI has maintained a strong growth trajectory following the spin-off of the business. Revenue grew by 19% in FY20 and 23% in FY21, with only a small decline subsequently.

BBWI operates c.1800 stores, primarily across the US. The company operates as a specialty retailer with affordable prices, allowing the company to partake in industry growth by providing a wide range of products. As a specialist, BBWI has garnered a strong customer following, developing this relationship with a rewards scheme to improve the number of repeat purchases. The large variety of products in a specific industry alongside its scale is a primary selling point with BBWI. Further, BBWI has expanded overseas through physical locations (Partnerships), such as with Next in the UK, for example.

Store growth continues to be strong, which should support continued growth on an absolute basis. Management is forecasting a 3% net increase in store count and a 4-5% increase in sq ft within the US and Canada. The international business is forecasting an impressive net 15% increase.

The retail industry is highly competitive due to the inability to build genuine barriers to entry. The industry as a whole has experienced several key trends that have impacted BBWI.

Firstly, the rise of e-commerce has significantly changed the dynamics of the industry. E-commerce has contributed to increased competition, as online-only businesses compete aggressively on prices against retailers with high overheads. This has pressured BBWI to further develop its value proposition as a means of remaining competitive. We do believe BBWI is insulated somewhat by the products it sells, as hesitancy around the quality of ingredients means consumers are more likely to go with a business they trust.

This does not mean brick-and-mortar retailers are dead but instead a need to innovate their business model. An omnichannel approach is a critical development in our view. E-commerce provides consumers with convenience due to the ability to purchase without leaving the home but what if you want to try a product? or realize you do not like it? The system isn't perfect. An omnichannel approach allows the digital and physical stores to complement themselves (Such as by ordering online and picking up in-store).

Consumers are increasingly concerned about the ingredients used in personal care products. We are seeing increased demand for sustainable, vegan, and cruelty-free products. BBWI has leaned into this trend, producing a range of products with environmentally-friendly ingredients. Research suggests consumers are willing to pay a premium for sustainable products, supporting margins and revenue growth.

Further, there is a general trend toward wellness and self-care which is gaining significant momentum, with consumers seeking products that promote relaxation, stress relief, and overall health and well-being. The reason for this is likely a mix of several socio-economic factors and the impact of social media. BBWI is positioned well to benefit from this and is utilizing social media to expand its reach. BBWI has over 7m followers on Instagram and regularly partners with celebrities for promotional activities.

Finally, BBWI's products are primarily targeted at women. Women account for c.85% of all consumer purchases, with an estimated 80% for healthcare products. As a result of this, BBWI's marketing and strategic focus is on the most lucrative segment of the population.

These commercial factors are the primary reason for BBWI's strong growth in recent years. Although the company lacks a tangible moat, its scale, and brand recognition afford the business a leading position through loyalty and market visibility.

Economic & External Consideration

Economic conditions are the primary reason for the slowing demand in our view. This is not to say consumers are suddenly unable to afford fragrances or body care, but we are seeing a general slowdown in retail spending in response to heightened inflation.

We suspect BBWI will be resilient compared to other retailers. Body care and fragrances are generally sticky in demand due to the importance consumers place on the products and the low cost relative to income. We suspect this will support revenue.

Margins

BBWI has impressive margins. In the LTM23 period, the company boasted an EBITDA-M of 20% and a NIM of 10%.

These margins are a reflection of the products sold. Body care / fragrances have notoriously low production costs, allowing brands to focus on marketing investment while maintaining strong margins.

The recent slide in margins is likely due to inflation continuing to bite, as well as increased discounting as Management attempts to maintain growth.

Balance sheet

BBWI's ND/EBITDA ratio is 2.6x, which we believe to be a manageable maximum. Its interest coverage is 5.5x and interest payments represent 5% of revenue. Any further could become a concern for the business.

Cash flows have been impressively consistent, reflecting impressive working capital management (namely inventory). This has allowed the business to distribute well with shareholders, with dividends sustainable in the coming year in our view.

Outlook

{kind=link}

Presented above is Wall St. consensus forecast for the coming 5 years.

Revenue growth is expected to remain healthy, with a CAGR of 5%. This implies a continuation of the company's current trajectory, which looks reasonable in our view.

Further, margin improvement is also forecast. We have less conviction in this. Although it is certainly possible, we do not see sufficient evidence to support this view.

Valuation

BBWI is currently trading at 9.7x LTM and NTM EBITDA. In order to value BBWI, we have conducted a DCF valuation.

The key assumptions we have made are:

- Revenue growth of 4-5%, in line with analysts' estimates and the current trajectory of the business.

- Margin decline in FY23, followed by small incremental improvements, although not to the extent forecast by Management.

- An exit multiple of 7x, WACC of 9%, and a perpetual growth rate of 7x.

Based on this, we imply an upside of only 1%. This implies BBWI is trading at its current fair value. The key risks we see are the return to growth, and the normalization of margins, given the slippage of both in the LTM. Although we expect a rapid turnaround in FY24, this is far from certain. We do not see upside based on this risk.

Final thoughts

BBWI is a strong brick-and-mortar business in the highly competitive retail industry. BBWI is positioned extremely well to continue its positive trajectory, given the industry tailwinds and its fundamental characteristics. We also like its margins. Unfortunately, we do not see upside at the current valuation.

For further details see:

Bath & Body Works: A High-Quality Business Model But With No Upside