BBWI - Bath & Body Works: Near Term Challenges But Fragrant Medium Term Prospects

2023-08-21 12:13:37 ET

Summary

- Bath & Body Works is facing near-term challenges, but has cautiously optimistic medium-term prospects.

- Category expansion, international expansion could support medium term growth. Ongoing cost saving initiatives a positive for margins.

- Specialized focus on fragrances, and fragrance innovation capabilities are a competitive differentiator against crowded market.

- Execution risks may dampen growth prospects.

American toiletries retailer Bath & Body Works ( BBWI ) is facing sluggish near term conditions, but their medium term prospects are cautiously optimistic, driven by a number of growth initiatives. Their valuation appears fair.

Company Overview

Bath & Body Works is a specialty retailer of home fragrance, and personal care products such as scented candles, soaps, shampoos, and sanitizers. The company operates an offline store network of 1,802 stores in North America, 427 franchise-operated stores worldwide, and 31 eCommerce websites. The vast majority of revenues are generated in North America.

Since splitting from L Brands in 2021, Bath & Body Works is now free to forge its own path and management has in place numerous initiatives to drive growth. Leveraging on their differentiated positioning as a fragrance-focused brand, BBWI is expanding into new categories, notably into men's personal care, and laundry care, as well as tapping into international markets which seem relatively underpenetrated. Management is aiming to become a $10 billion business with 20% operating margins (from $7.5 billion revenues and 18% operating margin currently).

Background

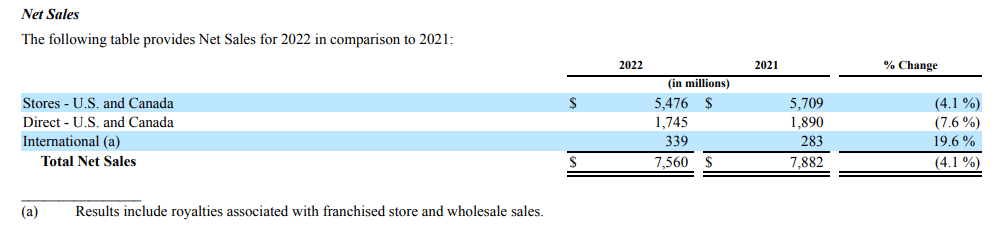

Since the company's position as a standalone entity began only in 2021, there are limited long term figures to gauge historical performance. The company generated revenues of $7.5 billion in FY2022, down 4% YoY due to normalizing pandemic tailwinds and macro challenges which cut into consumer spending on discretionary purchases. The company's gross margin of 43% is down from 49% the previous year due to input cost pressures. Operating margin of 18% is also down from 25.5% the previous year.

{kind=link}

Bath & Body Works 10-K, FY2022

Ongoing headwinds are expected to continue this year. Revenues and profits have been dipping over the past several quarters, and margins have also continued to see downward pressure due to rising cost pressures amid a softening demand environment.

Author

The company’s near term outlook is expected to remain sluggish. Management expects a flat to mid-single sales decline for FY2023, and gross margins are expected to dip to 42% from 43% last year impacting free cash flows which are forecasted to amount to $650 million to $725 million in FY2023, down from $816 million the previous year. Although EPS guidance was revised upwards (due to better than anticipated Q1 performance) to $2.7-$3.10 , it still remains well below last year's EPS of $3.40.

Liquidity remains decent with a current ratio of 1.63 and a quick ratio of 0.9.

Capitalizing on growth opportunities from category expansion, international expansion

A number of medium term growth opportunities could support medium term revenue growth for the company. The company is branching out from their core scented candles and home fragrances business and into adjacent categories, notably men’s personal care, and fabric care products. Both of these markets are highly competitive, but there are reasons to be optimistic about BBWI’s prospects; their men’s care business has so far shown encouraging results (growing 50% over the past three years) and management is optimistic about doubling their men’s business to $800 million from $400 million in 2022 which could support sales growth in North American markets which currently accounts for 95% of their total $7.5 billion revenues in 2022 (their men’s range has so far been available in all their 1,800 U.S. and Canadian stores.

Their new fabric care business meanwhile was announced in May this year, so it remains to be seen how successful the expansion would be however, prospects again are cautiously optimistic considering the initiative was born as a result of direct customer requests, and decisions on fragrance options for their new fabric care line are being made together with input from members of their 37 million -strong loyalty program who collectively account for two-thirds of U.S. sales.

Increasing penetration in international markets (which currently account for around 5% of sales or under $500 million in FY2022) presents a further growth opportunity. Late last year, Bath & Body Works opened their first store in the U.K. , and in Belgium , and this year opened their first high-street store in India , their first store in Israel , as well as stores in the Philippines . There may be further growth left considering the company’s North American store footprint is over four times bigger than their entire international store footprint ( 1,802 stores in North America compared with 427 stores outside North America). While North American stores are company-owned, their international expansion has been driven by a capital-light franchise model which should enable relatively rapid expansion.

Again, it remains to be seen how successful their international expansion efforts would be, however there are reasons to be optimistic; Bath & Body Works’ differentiated positioning as a fragrance-innovation-focused player could help it carve a niche in the global scented candles market which is projected to grow in the mid single digits over the coming years. Moreover, Bath & Body Works has products across a wide spectrum of price points, enabling them to cater to customers in fast-growing but more price-sensitive emerging markets. Management is forecasting double-digit international net sales growth for 2023.

Cost saving initiatives to help offset margin pressures

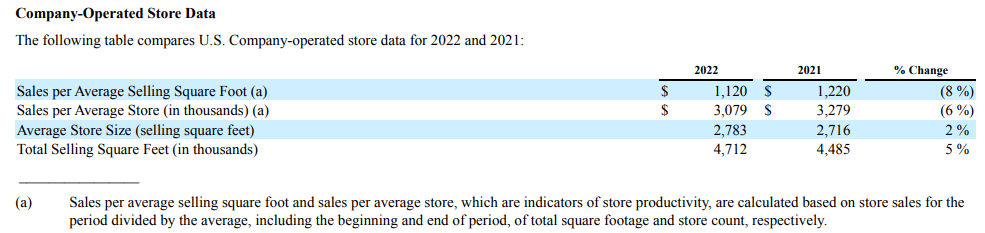

Near term margins are expected to continue seeing downward pressure driven by a weak demand environment and inflationary pressures. Moreover, despite ongoing headwinds, average store size and selling square footage has been on an upward trend. Management foresees a further 4% growth in square footage for FY2023, while sales are expected to continue dropping. Declining store unit economics should further exacerbate margin pressures.

{kind=link}

Bath & Body Works 10-K, FY2022

Bath & Body Works’ ongoing cost savings initiative is expected to generate annual cost savings of $200 million over the coming years. Over half of those cost savings are expected to be realized this year (in the latter half, helping offset near term margin pressures), while a substantial portion of the remainder is expected to be realized in 2024, helping the company move closer to their 20% operating margin target. For perspective, the company's operating expenses totaled around $2.5 billion in FY2022. Together with the benefits of scale economies as the business expands and moderating inflation, a 20% operating margin target seems not unfeasible assuming their new fabric care and men's grooming products are not margin dilutive, and marketing expenses remain largely unchanged as a proportion of revenues.

BBWI's interest expenses, at nearly $350 million in FY2022, is quite high, accounting for nearly a fifth of their operating expenses that year. The company however has been deleveraging, and assuming interest rates remain unchanged and the company's debt burden continues to drop, a corresponding drop in interest expenses could be positive for net margins and cash flows.

Differentiation thanks to fragrance focus

Bath & Body Works’ products are essentially commodity products, however their branding, constant innovation, and specialized focus on their products' fragrance attributes serve as a decent differentiators in a crowded market. The company continues to innovate with new and very unique scents being rolled out on a regular basis (releasing new fragrances and products every four to six weeks , a pace it expects to maintain going forward), providing a competitive edge in terms of rapid innovation capabilities that smaller players and new entrants may find difficult to match.

Risks

Execution risks

Execution risks could prevent strategic initiatives from bearing anticipated returns and in the worst case, costly missteps could lead to losses and possible erosion of market value.

If the company delivers better than anticipated financial performance, the stock could materially benefit

A higher-than projected growth (8% or higher) over the next six years, while maintaining projected margin expansion trajectory, could have a meaningfully positive impact on the company's share price. Moreover, their forecasted free cash flows of over $600 million amply covers their dividend (payments for which amounted to $186 million last year), opening the possibility of a dividend hike down the road as revenue growth resumes, and margins expand benefiting cash flows. Activist investor Dan Loeb of Third Point Capital could be the catalyst to trigger a dividend hike.

Conclusion

Bath & Body Works has a moderate buy analyst consensus rating.

Seeking Alpha

A DCF valuation suggests the valuation is fair (base case scenario).

Assumptions

{kind=link}

Author

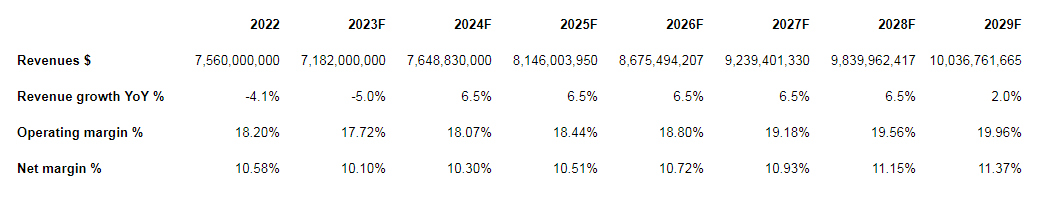

| Revenue growth = 5% revenue decline this year, 6.5% revenue growth 5 years afterwards |

| 6.5% growth rate is based on management’s target of reaching $10 billion revenues, assumed over a roughly 6-year period |

| Terminal growth rate = 2% |

| In line with anticipated long term economic growth |

| Operating margin = dipping to 17.7% this year then gradually increasing to 20% |

| Based on management’s 20% operating margin target from around 18% currently |

| Net margin = dipping to 10.1% this year, then gradually increasing to 11.4% |

| Roughly assuming effective tax rate, interest costs remain unchanged |

Together with the above growth assumptions, assuming depreciation and CAPEX of around 3% and 4% of revenues respectively, neutral working capital, and a discount rate of 10% suggests the company is worth around $9 billion, just slightly higher than their current $8.3 billion market value currently. The stock could be viewed as a hold for investors willing to tolerate the risks.

For further details see:

Bath & Body Works: Near Term Challenges But Fragrant Medium Term Prospects