BBWI - Bath & Body Works: Short-Term Pain Provides An Attractive Entry Point

2023-11-21 03:56:42 ET

Summary

- Bath & Body Works is a retail that specializes in personal care and home fragrance products.

- The brand has crafted its identity around providing a sensory in-store experience, limiting the risk of being replaced by e-commerce.

- During the 2008 crisis, B&BW experienced a sales decrease of only 2%, which shows its ability to resist crises.

- The current valuation is highly attractive because it is already priced in a negative scenario.

Investment Thesis

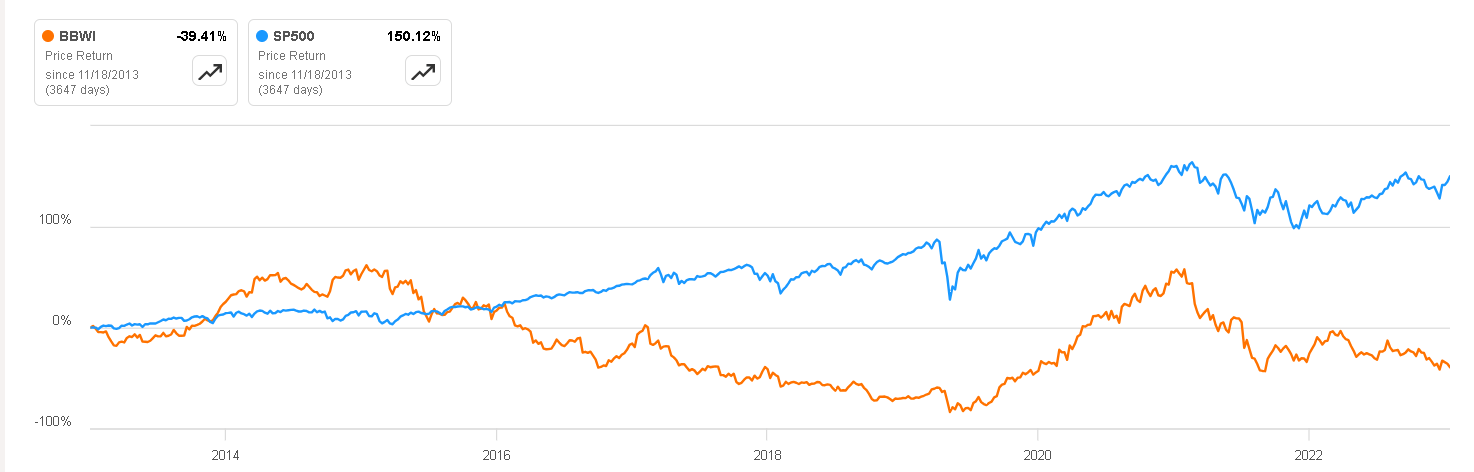

Bath & Body Works ( BBWI ) is an intriguing tale of a company that, in the past, was somewhat overshadowed by Victoria's Secret, hindering its remarkable growth and margins. Recognizing the need for independence, the board made the strategic decision to separate the two entities in 2021, allowing Bath & Body Works to showcase its true value. However, the timing proved to be less than ideal as subsequent challenges, including a bear market, high inflation, and an economic slowdown, have influenced investor perception, leading to its current trading status at an LTM P/FCF of 8x .

This article will delve into the business model, aiming to understand the qualities that have driven its impressive results in recent years. Additionally, a valuation will be conducted to justify why, even in a conservative scenario where 2023 and 2024 might be challenging, the current valuation remains highly attractive for a business that possesses a reasonable degree of quality

{kind=link}

Business Overview

Bath & Body Works (B&BW) was born after L Brands spun off Victoria's Secret and rename itself to Bath & Body Works, in 2021. The company is a retail that specializes in personal care and home fragrance products. They are well-known for their extensive range of scented products, including body lotions, shower gels, candles, and a wide variety of seasonal offerings.

{kind=link}

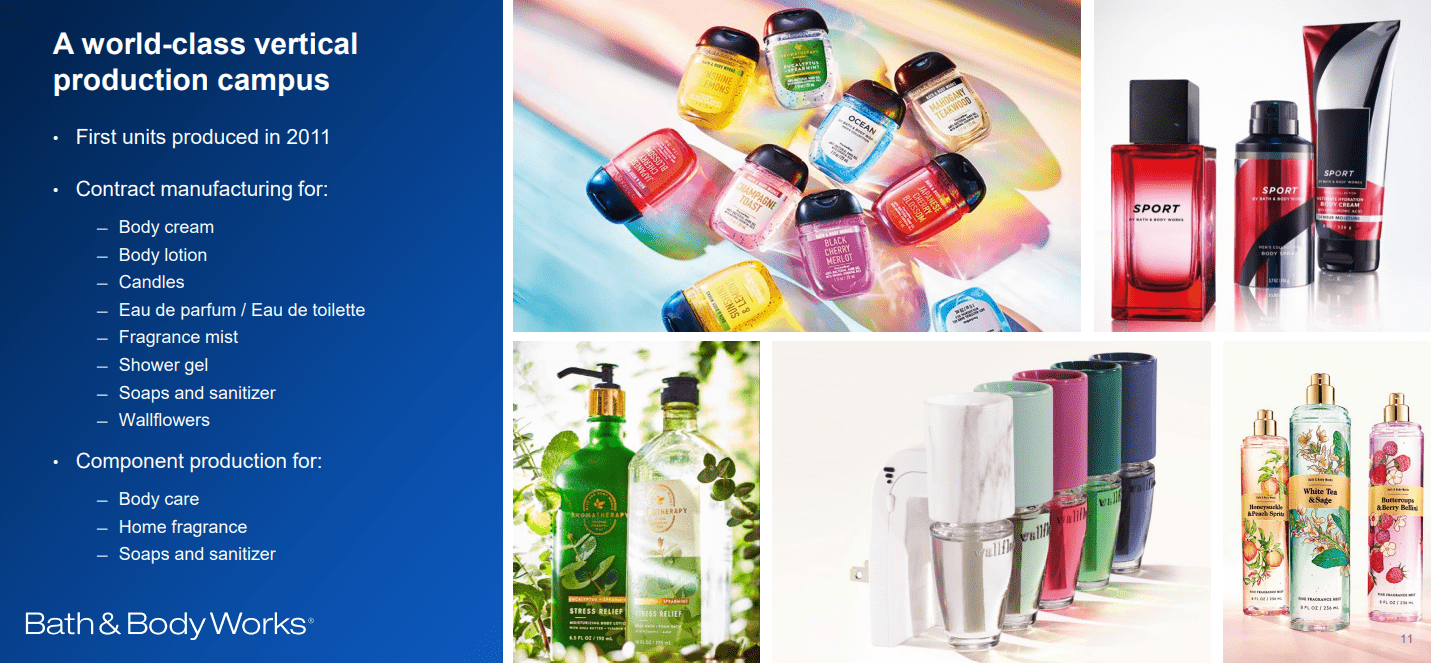

One of the most favorable aspects of the company is its nearly complete vertical integration . It primarily sells products under its own brand in its stores, so instead of purchasing items from third parties and reselling them, the company manufactures most of its products, often within the U.S. Additionally, it manages the distribution process, although some aspects are delegated to third-party logistics providers. As the point of sale, the company has real-time information about product demand, enabling it to respond efficiently and meet customer needs effectively.

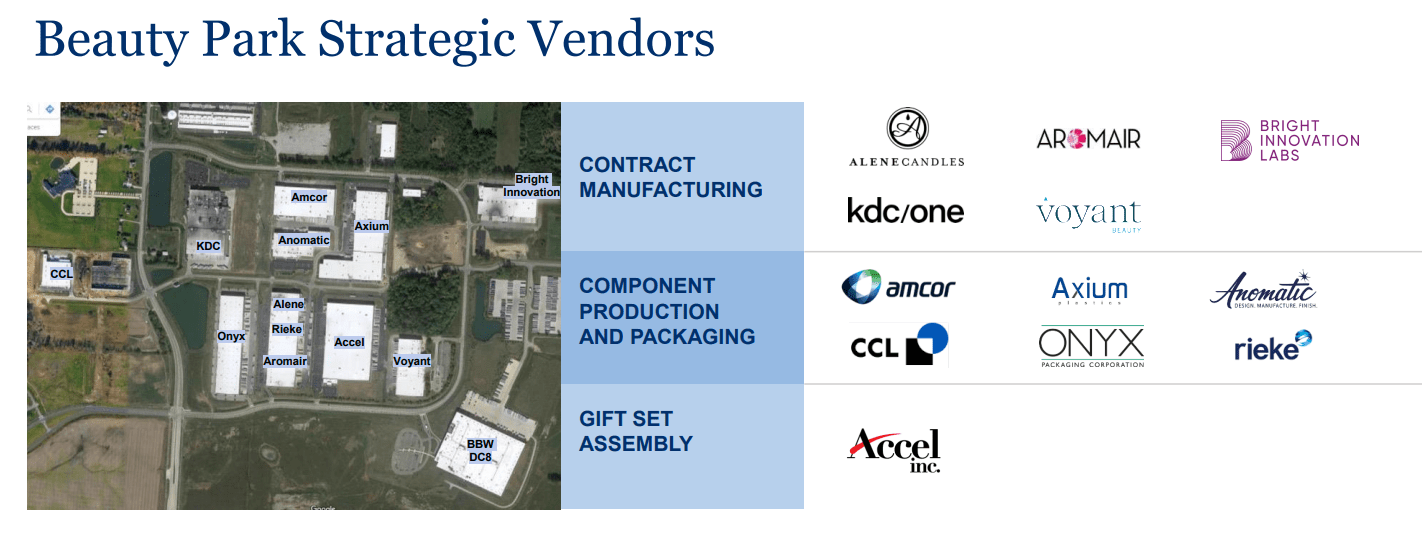

The company remains committed to enhancing its supply chain and has directed efforts towards what they term ' Beauty Park '—a business park strategically housing key vendors in close proximity to the company's vital distribution points. This initiative significantly reduces transportation times, lowers logistics and transportation costs, enhances overall efficiency, and affords greater flexibility and adaptability in responding to market trends, production challenges, and other dynamic factors.

These endeavors are expected to yield favorable results on the company's future margins. These strategic investments, while possibly overlooked by investors, hold great promise for the future of B&BW.

{kind=link}

A Sensory Experience

One of the primary concerns in the retail sector is the potential shift of customer purchases from traditional brick-and-mortar stores to e-commerce platforms like Amazon or Facebook Marketplace. This concern is particularly relevant in businesses like Bath & Body Works, where their products can be perceived as commodities. However, I believe the company possesses features that significantly mitigate this potential risk.

While the trend towards e-commerce has experienced significant growth in recent years, with many consumers opting for online shopping due to its convenience, there are unique aspects of the Bath & Body Works shopping experience that prove challenging to replicate in a digital environment. The brand has crafted its identity around providing a sensory in-store experience, enabling customers to sample and smell various products before making a purchase.

The ability to physically try different scents and products is a crucial component of the shopping experience for many customers. This tangible experience, impossible to replicate in a digital setting with current technology, creates a memorable and personalized encounter. Smell and memory share a close link, and scents possess a powerful impact on emotions and memories. This aspect not only enhances customer satisfaction but also contributes to word-of-mouth marketing, as customers enthusiastically share their favorite scents with friends and family.

However, that doesn't mean e-commerce can't play a significant role in the retail strategy of Bath & Body Works. Many retailers, including those in the personal care and beauty industry like Ulta Beauty or Sephora, have successfully incorporated e-commerce into their business models. So we could say that the physical presence of the company can enhance customers' perception , prompting them to choose Bad & Body Works' own digital store when making online purchases.

Image Source: Modern Retail

Recurring Consumer Spend

Another advantageous aspect is that, in contrast to other retail businesses like Foot Locker, Target, or DICK'S Sporting Goods, the purchase of skincare products, body lotions, liquid soap, and especially antibacterial hand products since the COVID-19 pandemic, has a much more recurring nature compared to items like clothing, footwear, or household goods.

The shorter lifespan and daily, routine use of these products contribute to a consistent demand. Additionally, as they address fundamental human needs such as hygiene and the desire to feel clean, these products retain their significance in customer purchases even during challenging economic periods.

While this doesn't imply that Bath & Body products are as essential as those from a grocery store, it does confer a degree of resilience to crises that surpasses that of many other retail businesses. Consequently, in an economic slowdown, we may anticipate a modest growth or a slight decline in sales, but not a perilous plummet.

B&BW During Crisis

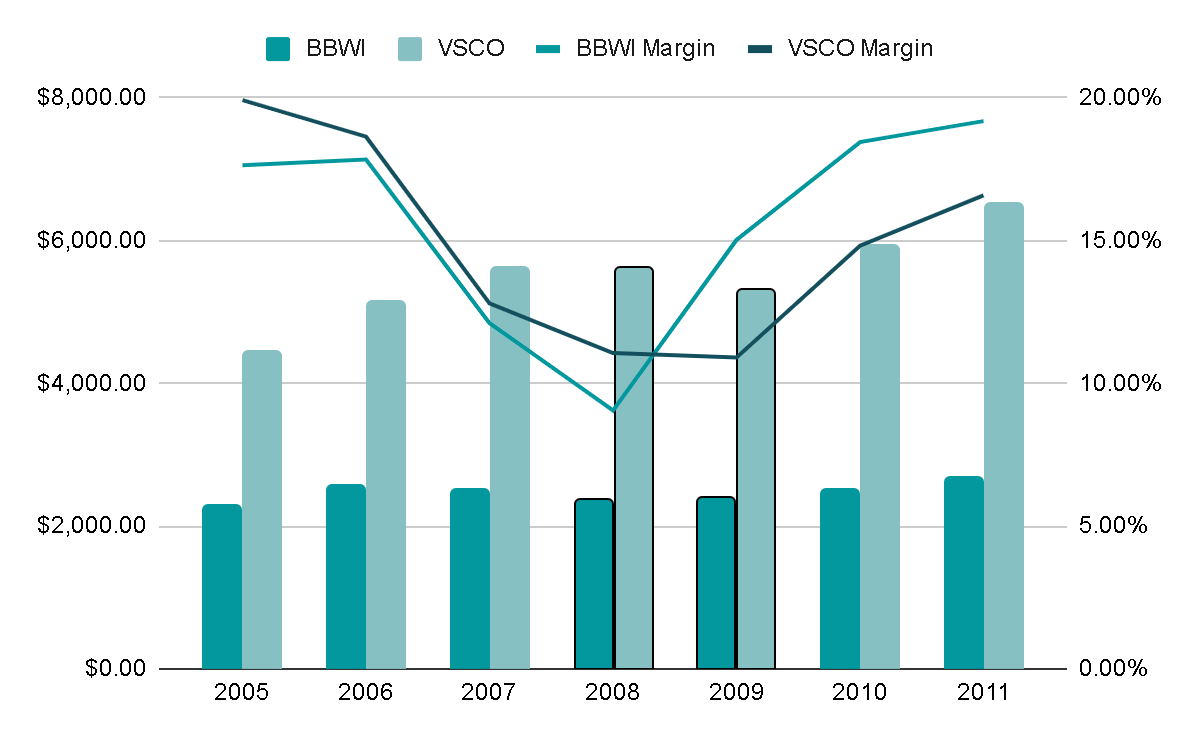

An illustrative example is the performance of the company's revenues during the 2008 financial crisis . From 2007 to 2009, Bath & Body Works experienced a total sales decrease of 4.5%. In comparison, Victoria's Secret, although still resilient considering the magnitude of the crisis, saw a 5.5% decline during the same period.

A similar trend is observed in 2023, where overall consumption is weakening, and the challenging comparables of 2020/2021 were particularly formidable due to the excess money circulating in the system. Despite these factors, the company anticipates a sales decrease ranging between 2% and 5% this year. Remarkably, this is considered a positive outcome, especially when contrasted with the exceptionally high, atypical growth rates of 20% annually witnessed in 2020/2021.

If revenues decreased 3% during this year, this would imply that between 2019 pre-covid and 2023 the top line would have grown 8% annually, quite in line with the 10% growth in the last decade. It wouldn't be so bad after all .

{kind=link}

Key Ratios

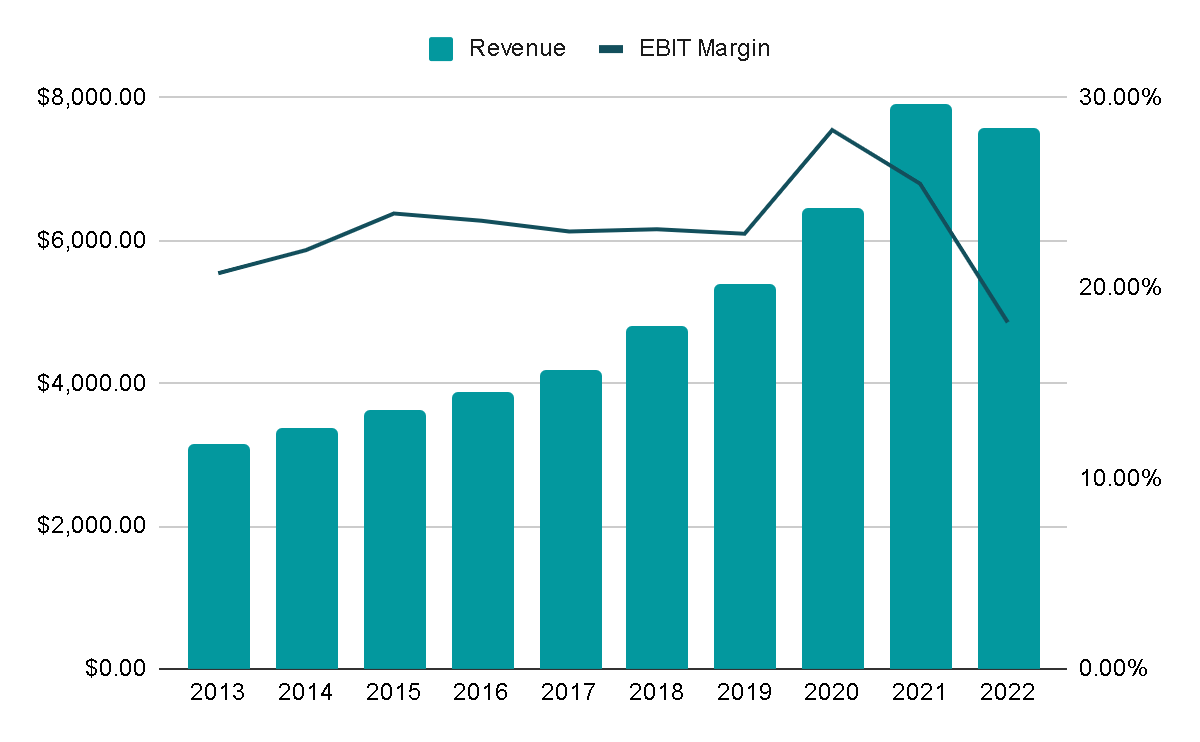

The company's overall revenue has consistently grown at an annual rate of 10% over the last decade, with an accompanying EBIT margin hovering around 23%. While this overarching financial performance is crucial for valuation considerations, we will now delve into the specifics of the two segments that constitute the company's revenue.

{kind=link}

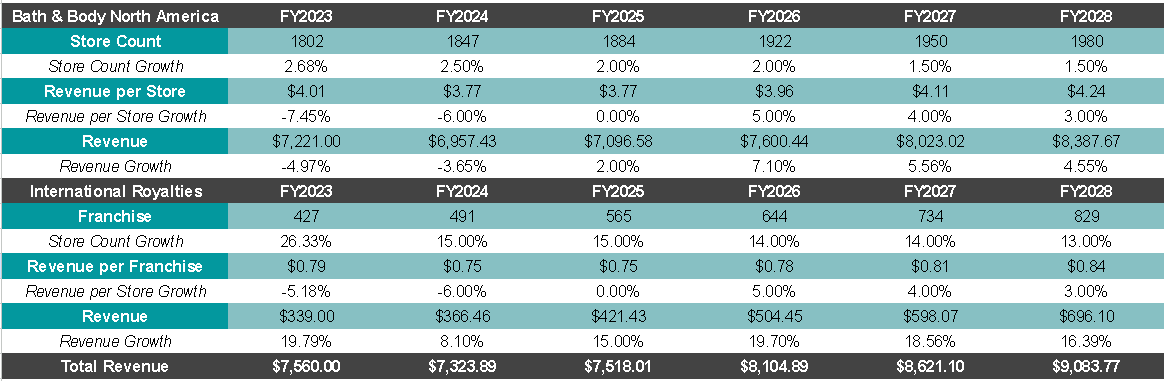

Bath & Body North America

The company operates its own physical stores in the United States and Canada, with the latter contributing to only 6% of the total store count. Presently, roughly half of the stores are situated off-mall , and there is a strategic initiative to further increase this proportion. This approach allows Bath & Body Works to mitigate its exposure to potentially vulnerable mall locations, enhance accessibility and appeal to its most loyal customers, and boost brand visibility in areas characterized by high pedestrian or vehicular traffic.

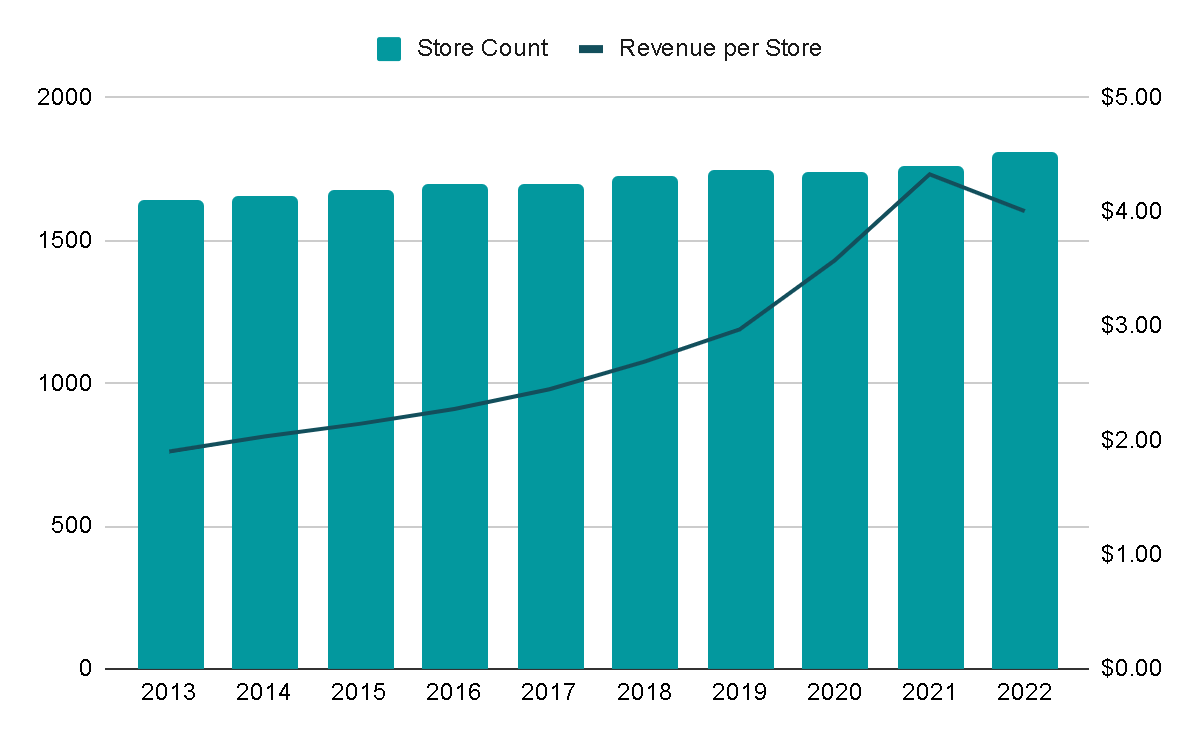

It can be noted that in the last decade the growth of new stores has been sustained, although at slow rates of 1%. On the other hand, revenue per store has grown 8% annually in the last decade and currently each store generates close to $4M annually. As we mentioned previously, during 2021 there was a peak in profits, but these are already normalizing.

{kind=link}

We gain additional insights into this segment as L Brands, the former parent company of Bath & Body Works, provided a breakdown of revenues and EBIT for the stores operated by the company. Despite the peak in 2021, revenue has demonstrated consistent annual growth of almost 10% , with margins consistently around 23%.

{kind=link}

International Royalties

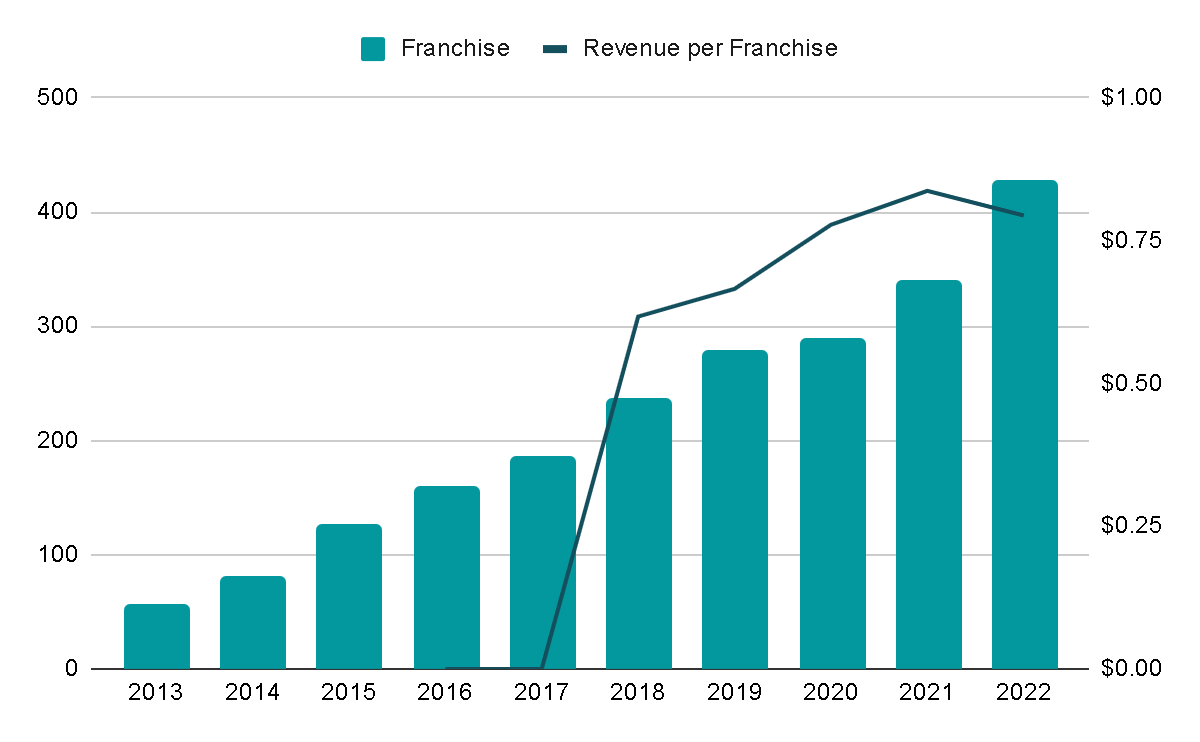

In addition to the Company-operated stores, the company operates 'partner-operated locations'—international sales acquired through franchise, license, and wholesale agreements. While these revenues constitute only 5% of the total, they boast high margins as the company's role is primarily providing its brand and support to franchisees.

This model serves as an effective means of international expansion without the risk of testing the concept beyond North America. Many companies initiate their global expansion through franchises and subsequently consider repurchasing to gain control over all generated profits.

The number of franchises has experienced an impressive annual growth rate of 25% over the last decade. The Revenue per Franchise (royalties) stands at $790,000 annually. It's worth noting that the company began disclosing revenue breakdowns from this segment in 2018, providing a more comprehensive understanding of its financial performance.

{kind=link}

Valuation

To estimate the company's value, I plan to project the future growth of the two segments by considering their past performance and management's guidance.

For the Bath & Body North America segment, I anticipate an annual increase in the number of stores at a rate of 1.75%. The company has indicated its goal of reaching approximately 1,847 stores this year. Historically, the growth rate for the number of stores has been around 1% annually, but there's potential for an uptick given that the company now operates independently, and capital is no longer divided between Bath & Body Works and Victoria's Secret.

As for the International Royalties segment, the company aims to reach a range of 480 to 500 franchises . Following this, I project a more conservative growth rate of 14% annually, a reduction from the 25% observed in the last decade.

{kind=link}

Collectively, I anticipate total sales to increase between 5% and 6% annually over the next five years, factoring in a decline in 2023 (FY2024) based on the observed performance in the first nine months of the year. I anticipate a somewhat subdued 2024 (FY2025) to maintain a conservative outlook .

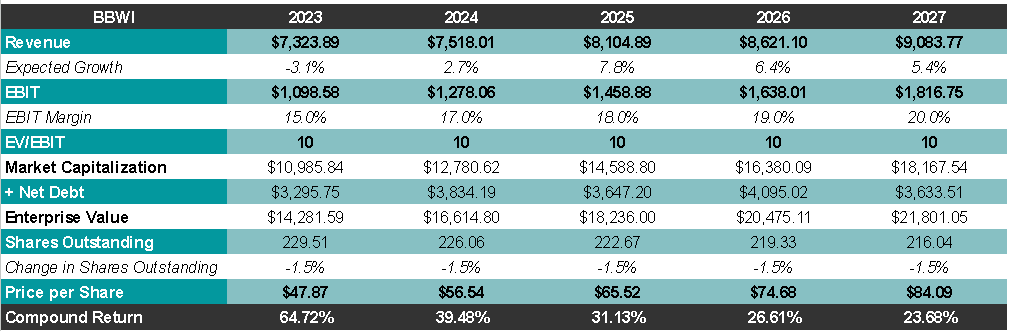

Additionally, I believe the company has the potential to elevate its EBIT margins to the 23% achieved between 2013 and 2019. However, in the spirit of conservatism, I will estimate a more moderate margin of 20% by 2027 (FY2028). This implies an EBIT of $1.8 billion within the next five years.

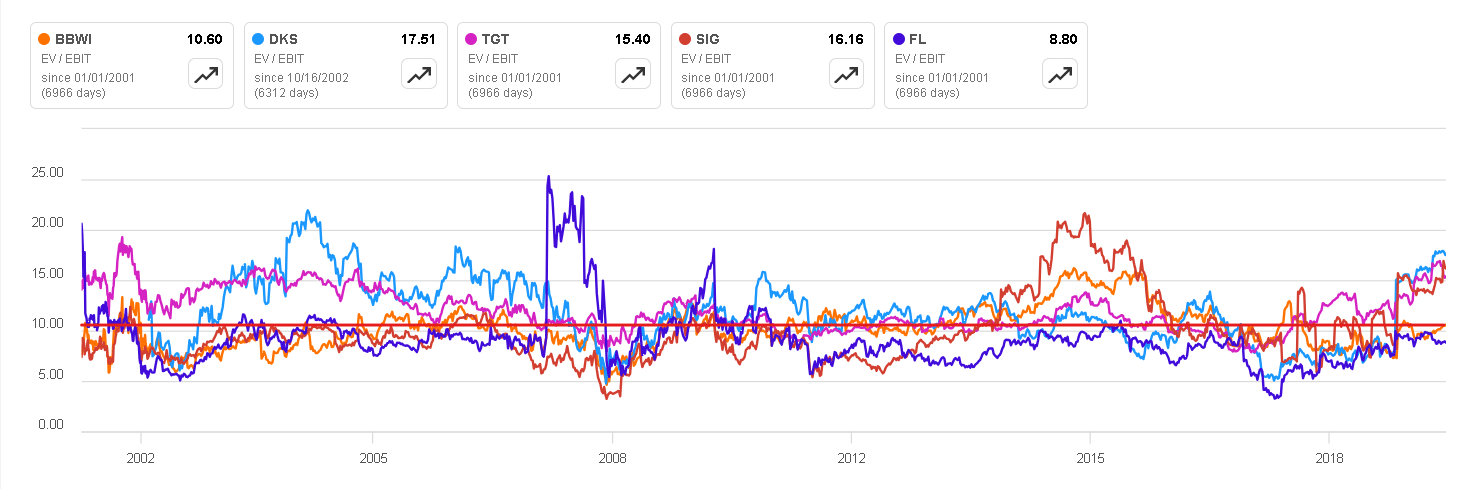

Utilizing an exit multiple of 10x EV/EBIT , in line with the average of various retail businesses and BBWI, we could expect a Market Capitalization of $18 billion in 2027. This implies an almost tripling of the current Market Cap of $6.60 billion, translating to an annual return of 24% based on this conservative valuation.

Author's Representation Seeking Alpha

{kind=link}

{kind=link}

Another perspective to consider the valuation is the company's guidance for this year, which falls within the range of $675 million to $725 million in Free Cash Flow. Put differently, the current valuation implies a trading multiple of approximately 9 to 10 times P/FCF , accompanied by a dividend yield of nearly 3%. It appears that the potential negative scenarios are already factored into the existing valuation .

Final Thoughts

While Bath & Body Works may not boast a perfect business model and is not entirely immune to economic downturns, its distinctive characteristics, including a loyal customer base and relatively recurring revenue streams, position it as a r esilient business . The current valuation, marked by a -32% YTD decline in the stock, seems highly attractive too. The market's fear of falling revenues and margins, has occurred in the past. Yet, the company not only weathered such challenges but also demonstrated the ability to maintain stable revenues and resume growth once macroeconomic conditions stabilized.

Considering these factors, I believe the current state of the company presents a ' buy ' opportunity. While the upcoming months may pose challenges, the solid fundamentals and appealing valuation make it an attractive long-term investment.

For further details see:

Bath & Body Works: Short-Term Pain Provides An Attractive Entry Point