BBWI - Bath & Body Works Still Has Upside Potential

Summary

- Bath & Body Works is reporting mediocre results with steeply declining operating income.

- Despite short-term headwinds, there seems to be still long-term growth potential for the business.

- And the stock remains undervalued in my opinion.

In my last article about Bath & Body Works ( BBWI ), I was clearly bullish about the stock and although I questioned if the business has an economic moat around its business, I saw the stock being clearly undervalued. Since my last article was published, the stock increased about 30%, while the S&P 500 ( SPX ) is basically trading at the same level it was about six months ago. And especially when the main argument to buy a stock is the undervaluation, we need to monitor the stock performance closely as the picture can change within a few months.

Quarterly Results

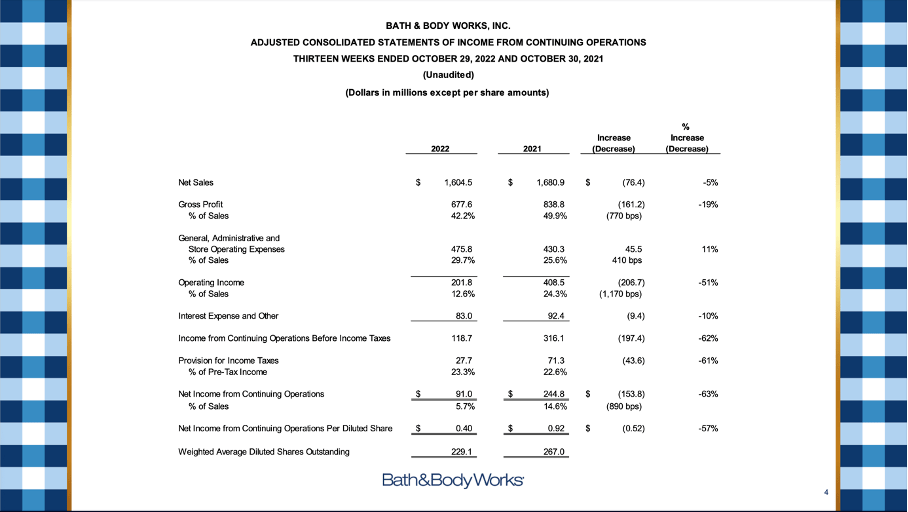

We start by looking at the quarterly results , which were not great (and in line with the year-to-date performance of the business). Sales in the third quarter of fiscal 2022 declined 4.6% year-over-year from $1,681 million in the same quarter last year to $1,604 million this quarter. Operating income declined from $408 million in Q3/21 to $202 million in Q3/22 - resulting in 50.5% year-over-year decline. And net income per diluted share increased from $0.33 in the same quarter last year to $0.40 this quarter - 21.2% year-over-year increase.

{kind=link}

The reason for the increasing bottom line is a loss of $90.8 million the company had to report in Q3/21, which had a huge negative effect on the results in the same quarter last year. This loss was primarily due to an $89 million pre-tax loss associated with the early extinguishment of outstanding notes.

Share Buybacks Using Cash Reserves

One aspect that is striking when looking at the income statement is the steeply declining number of outstanding shares. In the last twelve months, the number of outstanding shares declined from 267.0 million in Q3/21 to 229.1 million in Q3/22 - resulting in a decrease of 14.2% in just one year. In the last few earnings calls, management did not comment in any way on the share repurchase program, but during the Q4/21 earnings call , management made a short statement:

Our balance sheet and cash position are strong. We ended the year with approximately $2 billion in cash and our gross adjusted debt to EBITDAR leverage ratio at 2.3 below our target of mid twos. The Board and management team are committed to continuing to return free cash to shareholders as evidenced by the Board's recent authorization of a new $1.5 billion share repurchase program and a 33% increase in our annual dividend.

As I have pointed out in my last article, Bath & Body Works was undervalued (and still is - we will get to this) and hence share buybacks are a good idea. And as the free cash flow was not enough it seems like Bath & Body Works also used its cash and cash equivalents for share buybacks.

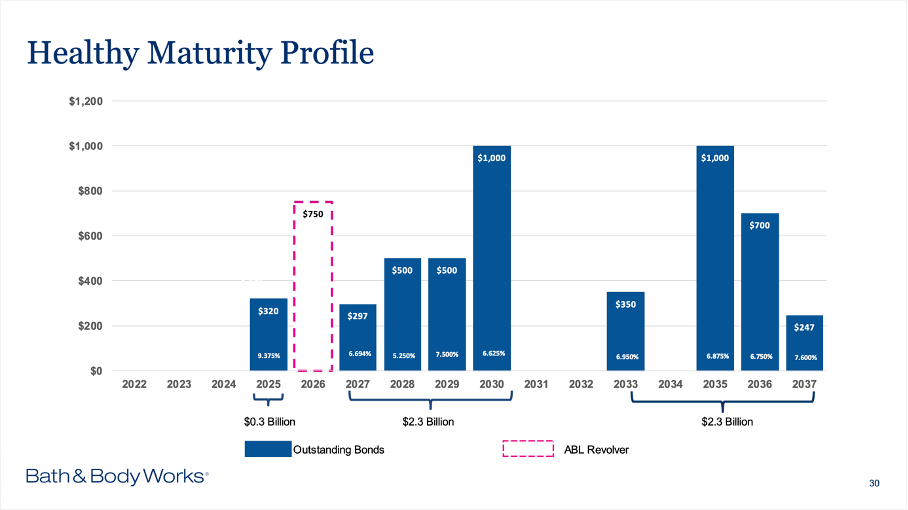

There is no reason to dispute management using cash and cash equivalents for share buybacks -especially when the stock is trading below its intrinsic value. And about half a year ago, the stock was trading for only 5.7 times earnings and 6.7 times free cash flow. And overall, I think the share buybacks were a good move. But management should not ignore the long-term debt it has on its balance sheet. On October 29, 2022, Bath & Body Works had $4,860 million in long-term debt on its balance sheet. Usually, I would compare that amount to the shareholder's equity, but as Bath & Body Works is reporting a shareholder's deficit of $2,609 million, we won't get any useful numbers. And it is certainly not a good sign that the shareholder's deficit increased from $1,677 million one year ago to $2,609 million right now.

However, when comparing the total debt to the operating income of the last four quarters of $1,603 million, it would take about three years to repay the outstanding debt - a metric that seems acceptable. And when looking at the maturity dates of the outstanding debt, we should also not assume that Bath & Body Works will run into any major troubles. Especially in the next few years almost no debt is due and therefore the company can use its cash reserves and generated free cash flow for share buybacks.

BBWI Investor Presentation November 2022

{kind=link}

And as the stock remains undervalued (we will get to this), it could be a smart move for the company to continue using its generated free cash flow to buy back shares - as long as there are no better ways to use the generated cash.

Growth Potential

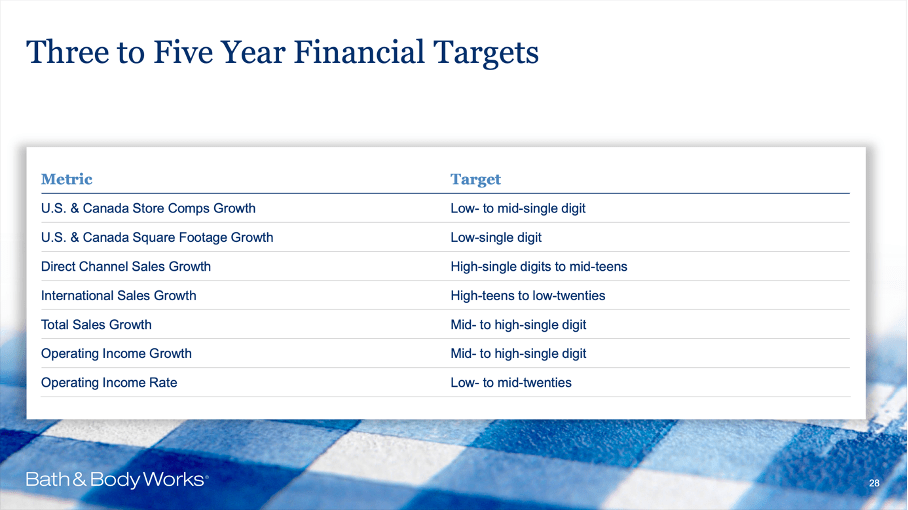

Aside from growing the bottom line by using share buybacks and reducing the number of outstanding shares, management is also confident that Bath & Body Works can remain on its growth path in the years to come. Over the next 3 to 5 years, the company is expecting revenue to increase from $7.9 billion in fiscal 2021 to about $10 billion. Overall, it is expecting sales to grow in the mid to high single digits.

BBWI Investor Presentation November 2022

{kind=link}

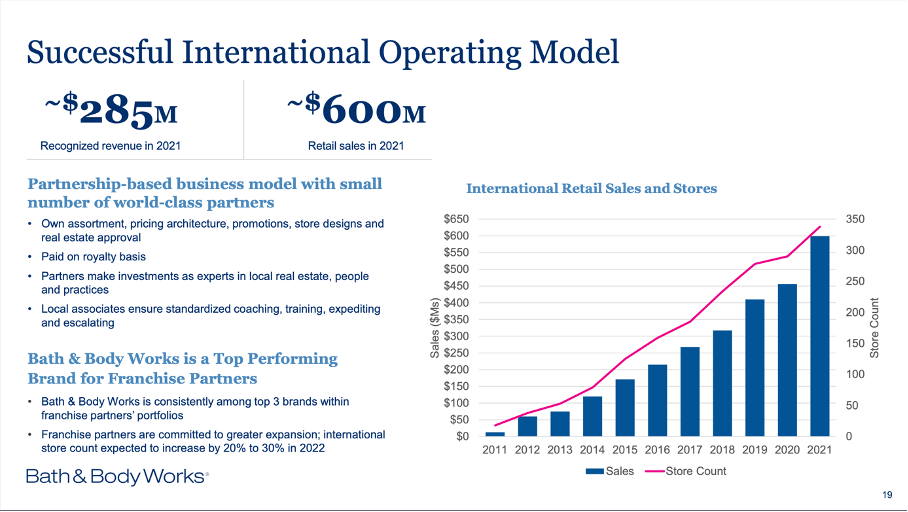

And when looking at the different segments (or regions), especially "North America" and "Digital" should contribute to growth. While North America stores are expected to increase sales between $850 million and $900 million due to the continued roll-out of the White Barn format and increased overall selling square footage as well as new and scaled omnichannel capabilities, "Digital" might contribute even about $1,000 million in additional sales. Especially an evolving digital experience as well as introducing new marketing channels will contribute to growth. And finally, "International" will increase sales about $200 million to $250 million due to different growth strategies (including potential growth in new regions).

BBWI Investor Presentation November 2022

{kind=link}

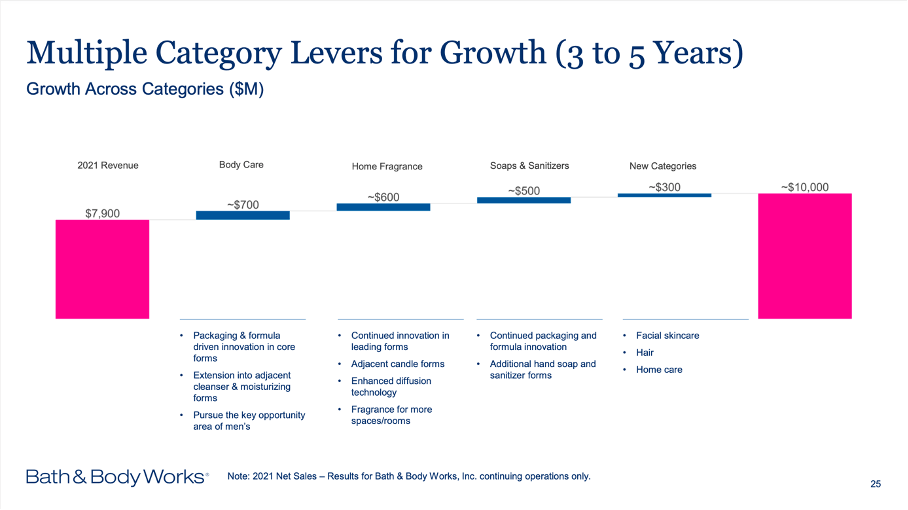

And when looking at the different product categories, all four are expected to contribute to growth - especially Body Care will contribute about $700 million, and Home Fragrance will contribute about $600 million.

One way to grow is by increasing the number of stores and when looking at the past few quarters, the company was growing with a solid pace: Since the beginning of 2022, the number of company-operated stores also increased from 1,755 on January 29th, 2022, to 1,787 on October 29th, 2022. And totally partner-operated stores increased from 338 at the end of January 2022 to 394 at the end of October 2022. When looking at the last few years, especially international retail stores increased with a high pace.

BBWI Investor Presentation November 2022

{kind=link}

The growth rates management is expecting for the business in the years to come are also in line with the growth rates analysts and researchers are expecting for the overall industry. When looking at different studies for the fragrance market (see here , here and here ) all are expecting growth rates between 5% and 6%. And when looking at the skin care market, expected growth rates are more or less in a similar range: one study is expecting a CAGR of 5.5% until 2028 and another study is expecting sales to grow 4.2% annually until 2030. And finally, the soap market is expected to grow with a CAGR of 5.0% until 2027.

Recession

And despite the growth potential Bath & Body Works could have, we should not ignore the macro headwinds and the fact that the business is certainly faced with short-to-mid-term challenges (as reflected in the quarterly results). As I already pointed out in my last article, Bath & Body Works will most likely be affected by a recession (like its previous parent company L Brands).

We still can discuss how essential the products Bath & Body Works is selling are. On the one hand, soaps and lotions can be classified as essential and everyday products that consumers will also buy during a recession. On the other hand, most of these products are rather expensive and there are certainly cheaper alternatives - and during an economic downturn customers might turn to cheaper alternatives.

Intrinsic Value Calculation

When looking at the valuation multiples, Bath & Body Works is trading still for low double digits multiples. Right now, Bath & Body Works is trading for a price-earnings ratio of 12.20 and a price-to-free-cash-flow ratio of 13.59. When looking at the last year, the current valuation multiples seem rather expensive, but we should not forget that Bath & Body Works was extremely cheap last summer and valuation multiples in the low double digits are definitely reasonable for growing businesses.

And we can also show the undervaluation of Bath & Body Works by using a discount cash flow calculation. As basis we can for example use the free cash flow of the last four quarters, which was $831 million. In this case, the company must grow slightly above 2% from now till perpetuity to be fairly valued. This is assuming 229 million outstanding shares and a 10% discount rate. But we should also not ignore that management is expecting free cash flow for fiscal 2022 only to be between $475 million and $550 million.

When trying to calculate with more realistic assumptions, we can assume that Bath & Body Works is able to grow about 5% annually from now till perpetuity. For fiscal 2023 we assume a free cash flow of $0 to reflect the risk of a recession with the usual negative effects on the business. For fiscal 2024 we assume a free cash flow of $750 (assuming a sales/free cash flow ratio of about 9% - in line with past results of L Brands). When calculating with these assumptions, we get an intrinsic value of $59.55 for Bath & Body Works and the stock would still be trading for a 20% discount. And I am still assuming these are rather cautious assumptions.

Conclusion

While the stock is not so cheap as it was when my last article was published, I would still see Bath & Body Works rather as a buy. And despite the questionable moat (see my last article), I would still consider the stock a solid investment and as it is trading below its intrinsic value, we could accept the risk of a questionable moat.

For further details see:

Bath & Body Works Still Has Upside Potential