CA - Bausch + Lomb: Brent Saunders Return Bodes Well For Shareholders

Summary

- Brent Saunders led Bausch + Lomb Corporation when it was sold to Valeant Pharmaceuticals.

- He later led and sold competitor Allergan to AbbVie.

- Brent Saunders likely signed on as CEO with the expectation of operating Bausch + Lomb Corporation as a fully standalone company.

- Full separation is an important catalyst for shareholder value creation.

Bausch + Lomb Corporation ( BLCO ) reported Q4 earnings and held an earnings call . The call was more important than usual, with the incoming CEO Brent Saunders (ex-Allergan) appearing. Currently, BLCO is 89% owned by Bausch Health ( BHC ). Both sides are interested in changing this by spinning off more shares of Bausch & Lomb to Bausch Health shareholders. The announcement of a new CEO is further confirmation this plan is on track.

BHC spin-off process (BHC earnings call presentation)

Alternatively, another company could come in and buy the entire stake. I think the market is aware of this possibility, as the shares have done quite well since the appointment of Saunders. Saunders previously led Bausch & Lomb when it was sold to Valeant Pharmaceuticals (the current Bausch Health). Later, as CEO of Allergan, he sold that company to AbbVie Inc. ( ABBV ). This isn't a CEO afraid to be out of a job.

This seems important to both sides as Bausch & Lomb is generally considered the superior business, with good visibility into long-term sustainable low-growth cash flows. However, as a fully owned subsidiary of Bausch Health, you could argue it hasn't searched for growth or pursued R&D in the way it could have as a stand-alone business. Under the Bausch Health umbrella, the priority (and rightfully so) has been to reduce company-wide debt. When the company is finally a fully stand-alone business, we'll be able to see what it can really do.

Here are a few select quotes from the call that I think are informative for the prospects over the next year:

Here's what the incoming CEO says (emphasis added):

Thank you, Joe. Let me begin by saying what an honor it is to have this opportunity and how excited I am to be here today. Bausch + Lomb was the first company I led as CEO. So in many ways, this feels like coming home. Ophthalmology and eye health are two areas that I cared deeply about and have stayed close to due to Allergan's presence in the eye care space. I strongly believe that there is a great need in the marketplace for an integrated company that is solely focused on advancing eye health. And I'd like to thank the Board for their trust that they have placed in me to grow this great company into the future.

He also already laid out how he's thinking about the future ahead of truly being CEO and no doubt launching a fresh vision initiative of some kind:

Bausch + Lomb has always stood at the forefront of cutting-edge scientific and technological optical advancements, and I believe continued innovation will be key to the company's success going forward.

On previous calls, I found the company frustratingly reserved in talking about the spin-off of from its parent company. This call there was a markedly change, here's what Joe Papa said (emphasis mine):

...Now let's come to the agenda for today's call. I will begin with an update on the separation process...

Turning to Slide 6. We continue to see compelling opportunities for standalone Bausch + Lomb as a pure-play eye health company. We believe the company is well positioned for growth in large, durable markets. We continue to see potential margin expansion over the long-term, and we expect to have balance sheet flexibility to expand investment in the business. Substantial progress was made in 2022 towards the completion of the separation process. After filing our registration statement and launching the roadshow, we completed the IPO and began trading as a public company on the New York and Toronto Stock Exchanges on May 6, 2022. Importantly, Bausch + Lomb is not a guarantor of the debt of our parent Bausch Health. And on November 29, Bausch Health made Bausch + Lomb an unrestricted under the Bausch Health debt covenant, which helps provide us with greater potential flexibility and we have one more obstacle to full separation. And as a final comment, we understand that Bausch Health continues to believe that the separation of Bausch + Lomb makes strategic sense and have stated that they're going to thoughtfully evaluate all the factors related to the B&L separation.

It sounds like separation is imminent, and it could coincide with Saunders's first quarter starting on March 6. The company also guides during the first quarter of 2023. Ideally, Saunders wants to present a vision that's based on BLCO being a fully standalone company.

The CFO went over an example of how this is helpful, as he believes the company will be able to refinance debt more favorably if the company is fully separated:

As a reminder, we have an interim capital structure in place with interest expense at a variable rate of SOFR plus 3.25%. Upon full separation from BHC, we plan to refinance our debt and transition to a longer-term capital structure. As a standalone company, we expect to have a more favorable credit profile and potentially lower cost of debt.

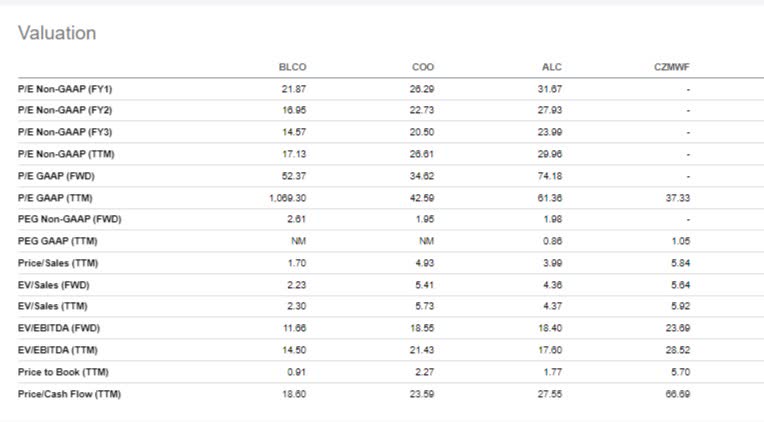

Normalizing the BLCO/BHC structure is important because both companies' share prices appear to be held back by the status quo. I put together an overview of eye healthcare companies, including peers like Cooper Companies ( COO ) Alcon ( ALC ) and Carl Zeiss Meditec ( CZMWF ). This paint a clear picture of BLCO trading at the lower end of the range. I'm paying special attention to P/E, P/S, EV/S and EV/EBITDA. But BLCO trades at a discount across the board.

{kind=link}

To an extent, the lower multiple for BLCO is justified because its 1-year and 3-year growth (within a growing category) has been relatively muted over the past compared to peers. However, I think this gap is likely to disappear when R&D and innovation is no longer skimped on.

This seems like an opportune time to buy or add to Bausch + Lomb Corporation with the new CEO incoming. There is a catalyst ahead in full separation from BHC. R&D is likely to be ramped back up. The new CEO has a track record of selling major pharmaceutical businesses, and finally, there's still a valuation gap to peers, indicating 30% of multiple expansion is possible. This leaves some room for error and temporary setbacks while the Bausch + Lomb Corporation investment can still work out well.

For further details see:

Bausch + Lomb: Brent Saunders Return Bodes Well For Shareholders